Idemitsu Kosan Porter's Five Forces Analysis

Don't Miss the Bigger Picture

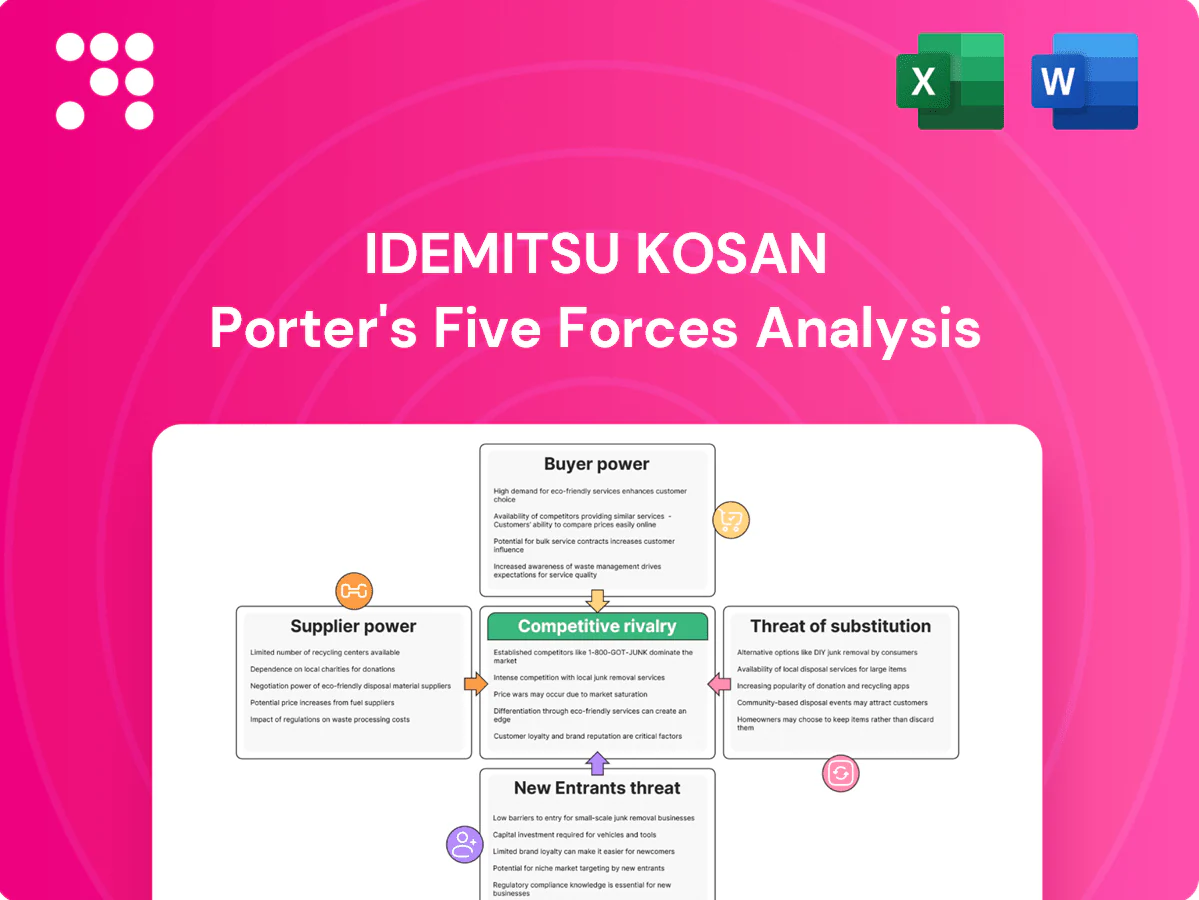

Idemitsu Kosan faces intense rivalry across refining and petrochemicals, moderate supplier power, evolving buyer dynamics, rising substitute threats from renewables, and regulatory barriers shaping margins and strategy; this snapshot highlights key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated crude sources

Idemitsu relies on a concentrated set of crude suppliers—OPEC+ which controls roughly 50% of global oil output in 2024—and select national oil companies, giving those suppliers pricing and volume leverage. Supply disruptions or quota changes transmit quickly into refinery feedstock costs and margins. Diversifying grades and long-term contracts reduce but do not remove exposure. Hedging cuts volatility but cannot counter structural supplier concentration.

LNG and coal feedstock leverage

Global LNG and coal markets remain tight and cyclical, giving upstream producers strong leverage on pricing and indexation; spot JKM volatility has fallen but long-term contracts still command premium. Japan imports over 90% of its gas and nearly all coal, magnifying exposure to freight and JPY/USD swings. Long-term take-or-pay deals—covering roughly 60–80% of volumes—reduce spot exposure but lock in obligations, while origin and index diversification moderates counterparty power.

Process licensors and OEMs

Refining and petrochemical units, including Idemitsu Kosan, rely on a small set of process licensors such as Honeywell UOP, Axens and Lummus Technologies, and critical OEMs for compressors and control systems. Limited alternatives for catalysts, compressors and DCS raise switching costs and allow suppliers to command service and replacement margins. The global refinery catalyst market was about USD 9.2 billion in 2024, underscoring supplier leverage. Multi-sourcing and standardization mitigate but do not eliminate technical lock-in.

Maritime logistics constraints

Tanker availability and marine fuel costs materially affect landed feedstock economics; port congestion and chokepoints like the Suez Canal (≈12% of global seaborne trade in 2024) can shift bargaining power to shipowners, while long-term charters and preferred fleet relationships provide partial insulation; insurance and regulatory compliance narrow the pool of viable carriers.

- Tanker availability

- Marine fuel cost impact

- Chokepoints boost shipowner leverage

- Charters/fleet ties mitigate risk

- Insurance/compliance concentrate carriers

Renewables component suppliers

For solar, wind and geothermal projects, turbine, module and inverter suppliers can extract leverage in upcycles—spot module prices swung ~20–30% in 2023–24 and OEM lead times extended to 4–8 months in peak demand, pressuring developers like Idemitsu Kosan. Trade policies and tariffs have raised component costs by roughly 10–25% in targeted markets, while framework agreements and onshore localization programs have mitigated some exposure. Performance guarantees and availability clauses partially rebalance bargaining power toward developers by tying payments to output and reliability.

- Upcycle price swing: ~20–30% (2023–24)

- Typical lead times: 4–8 months in peak periods

- Tariff/cost impact: ~10–25% in affected markets

- Mitigants: framework agreements, localization, performance guarantees

Concentrated crude supply and tight LNG/coal markets strengthen supplier power

Idemitsu faces concentrated crude suppliers (OPEC+ ~50% of global output in 2024) and tight LNG/coal markets, giving upstreams strong price leverage. Technical licensors and catalyst suppliers (global catalyst market ~USD 9.2bn in 2024) and tanker/chokepoint risks (Suez ~12% seaborne trade) raise switching costs. Long-term contracts, hedges and charters mitigate but do not remove supplier power.

| Factor | 2024 metric |

|---|---|

| OPEC+ share | ~50% |

| Japan gas imports | >90% |

| Catalyst market | USD 9.2bn |

| Suez trade | ~12% |

What is included in the product

Tailored Porter’s Five Forces analysis of Idemitsu Kosan uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic barriers protecting incumbency. Identifies disruptive forces, pricing pressures, and strategic levers to inform investors, managers, and academics.

A one-sheet Porter's Five Forces for Idemitsu Kosan highlighting supplier power, buyer pressure, rivalry, substitutes, and entry threats—clean, customizable, and ready to drop into decks for fast strategic decision-making and boardroom clarity.

Customers Bargaining Power

Price-sensitive fuel buyers

Wholesale and retail fuel buyers remain highly price-sensitive with low switching costs, pressuring margins in 2024. Real-time price boards and comparison platforms have intensified transparency and accelerated price-driven behavior. Loyalty programs and convenience offerings deliver limited differentiation against pure price competition. Idemitsu’s regional footprint and logistics reliability are key levers to retain volumes.

Industrial and utility contracts

Large industrials and power utilities negotiate multi-year fuel and feedstock contracts, leveraging scale and the ability to dual-source to extract discounts and flexibility from suppliers like Idemitsu. Index-linked formulas tied to benchmarks such as Brent (Brent averaged about 87 USD/bbl in 2024) limit supplier margin upside while protecting buyers from spot volatility. Performance bonuses and security-of-supply clauses (firm delivery windows, take-or-pay adjustments) soften pure price pressure by valuing reliability and penalties, narrowing buyer bargaining to service-plus-price tradeoffs.

Aviation and marine customers

Aviation and marine customers pool procurement and benchmark globally, pushing down premiums and demanding services plus sustainability attributes such as SAF and low-sulfur fuels. Operational reliability at major hubs is a competitive differentiator but rarely creates full lock-in. Co-investment in decarbonized fuels can deepen relationships; industry targets like IATA net-zero by 2050 and IMO 50% GHG reduction by 2050 raise customers′ leverage on suppliers.

Lubricants OEM and aftermarket

Automakers and industrial OEMs set technical specs and certification gates that limit suppliers and allow approved lubricants to command price premiums; OEM approvals drive long-term contracts and accounted for a large share of B2B volumes in 2024, supporting stronger margins for certified suppliers vs commodity grades. Aftermarket demand is fragmented but brand-aware, with private labels and global brands expanding buyer choice while technical support and extended drain intervals create modest switching frictions.

- Global lubricant market ~38 billion USD (2024)

- OEM-certified products often command price premiums

- Private labels vs global brands increase buyer options

- Technical support and drain intervals reduce churn

Petrochemicals customers

Commodity petrochemical buyers arbitrage across Asian suppliers, driving tighter margins and intensifying price competition; spot volumes rose to about 25% of regional trade in 2024 as buyers chased cost advantages. Contract/spot mixes swing with capacity cycles, while consistent quality and expedited logistics can secure premiums of 1–3%. Sustainability grades and recyclate integration are becoming active negotiation levers.

- Arbitrage across Asia — higher

- Spot share ~25% (2024)

- Quality/logistics = 1–3% premium

- Sustainability/recyclates = growing leverage

Wholesale margins squeezed: real-time pricing vs index deals; Brent ~87

Wholesale buyers are highly price-sensitive with low switching costs, pushing margins in 2024; real-time pricing amplifies this. Large industrials use index-linked multi-year contracts (Brent ~87 USD/bbl in 2024) to constrain supplier upside. Lubricant OEM approvals and technical support command premiums (global market ~38bn USD, 2024). Petrochemical spot share rose to ~25% (2024), tightening margins.

| Metric | 2024 |

|---|---|

| Brent avg | ~87 USD/bbl |

| Lubricant market | ~38 bn USD |

| Petrochemical spot share | ~25% |

Preview Before You Purchase

Idemitsu Kosan Porter's Five Forces Analysis

This Idemitsu Kosan Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—fully formatted, complete and ready for immediate download. No placeholders or samples; the content shown is the final deliverable. Buy once and gain instant access to this precise analysis for your strategic or investment use.

Don't Miss the Bigger Picture

Idemitsu Kosan faces intense rivalry across refining and petrochemicals, moderate supplier power, evolving buyer dynamics, rising substitute threats from renewables, and regulatory barriers shaping margins and strategy; this snapshot highlights key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated crude sources

Idemitsu relies on a concentrated set of crude suppliers—OPEC+ which controls roughly 50% of global oil output in 2024—and select national oil companies, giving those suppliers pricing and volume leverage. Supply disruptions or quota changes transmit quickly into refinery feedstock costs and margins. Diversifying grades and long-term contracts reduce but do not remove exposure. Hedging cuts volatility but cannot counter structural supplier concentration.

LNG and coal feedstock leverage

Global LNG and coal markets remain tight and cyclical, giving upstream producers strong leverage on pricing and indexation; spot JKM volatility has fallen but long-term contracts still command premium. Japan imports over 90% of its gas and nearly all coal, magnifying exposure to freight and JPY/USD swings. Long-term take-or-pay deals—covering roughly 60–80% of volumes—reduce spot exposure but lock in obligations, while origin and index diversification moderates counterparty power.

Process licensors and OEMs

Refining and petrochemical units, including Idemitsu Kosan, rely on a small set of process licensors such as Honeywell UOP, Axens and Lummus Technologies, and critical OEMs for compressors and control systems. Limited alternatives for catalysts, compressors and DCS raise switching costs and allow suppliers to command service and replacement margins. The global refinery catalyst market was about USD 9.2 billion in 2024, underscoring supplier leverage. Multi-sourcing and standardization mitigate but do not eliminate technical lock-in.

Maritime logistics constraints

Tanker availability and marine fuel costs materially affect landed feedstock economics; port congestion and chokepoints like the Suez Canal (≈12% of global seaborne trade in 2024) can shift bargaining power to shipowners, while long-term charters and preferred fleet relationships provide partial insulation; insurance and regulatory compliance narrow the pool of viable carriers.

- Tanker availability

- Marine fuel cost impact

- Chokepoints boost shipowner leverage

- Charters/fleet ties mitigate risk

- Insurance/compliance concentrate carriers

Renewables component suppliers

For solar, wind and geothermal projects, turbine, module and inverter suppliers can extract leverage in upcycles—spot module prices swung ~20–30% in 2023–24 and OEM lead times extended to 4–8 months in peak demand, pressuring developers like Idemitsu Kosan. Trade policies and tariffs have raised component costs by roughly 10–25% in targeted markets, while framework agreements and onshore localization programs have mitigated some exposure. Performance guarantees and availability clauses partially rebalance bargaining power toward developers by tying payments to output and reliability.

- Upcycle price swing: ~20–30% (2023–24)

- Typical lead times: 4–8 months in peak periods

- Tariff/cost impact: ~10–25% in affected markets

- Mitigants: framework agreements, localization, performance guarantees

Concentrated crude supply and tight LNG/coal markets strengthen supplier power

Idemitsu faces concentrated crude suppliers (OPEC+ ~50% of global output in 2024) and tight LNG/coal markets, giving upstreams strong price leverage. Technical licensors and catalyst suppliers (global catalyst market ~USD 9.2bn in 2024) and tanker/chokepoint risks (Suez ~12% seaborne trade) raise switching costs. Long-term contracts, hedges and charters mitigate but do not remove supplier power.

| Factor | 2024 metric |

|---|---|

| OPEC+ share | ~50% |

| Japan gas imports | >90% |

| Catalyst market | USD 9.2bn |

| Suez trade | ~12% |

What is included in the product

Tailored Porter’s Five Forces analysis of Idemitsu Kosan uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic barriers protecting incumbency. Identifies disruptive forces, pricing pressures, and strategic levers to inform investors, managers, and academics.

A one-sheet Porter's Five Forces for Idemitsu Kosan highlighting supplier power, buyer pressure, rivalry, substitutes, and entry threats—clean, customizable, and ready to drop into decks for fast strategic decision-making and boardroom clarity.

Customers Bargaining Power

Price-sensitive fuel buyers

Wholesale and retail fuel buyers remain highly price-sensitive with low switching costs, pressuring margins in 2024. Real-time price boards and comparison platforms have intensified transparency and accelerated price-driven behavior. Loyalty programs and convenience offerings deliver limited differentiation against pure price competition. Idemitsu’s regional footprint and logistics reliability are key levers to retain volumes.

Industrial and utility contracts

Large industrials and power utilities negotiate multi-year fuel and feedstock contracts, leveraging scale and the ability to dual-source to extract discounts and flexibility from suppliers like Idemitsu. Index-linked formulas tied to benchmarks such as Brent (Brent averaged about 87 USD/bbl in 2024) limit supplier margin upside while protecting buyers from spot volatility. Performance bonuses and security-of-supply clauses (firm delivery windows, take-or-pay adjustments) soften pure price pressure by valuing reliability and penalties, narrowing buyer bargaining to service-plus-price tradeoffs.

Aviation and marine customers

Aviation and marine customers pool procurement and benchmark globally, pushing down premiums and demanding services plus sustainability attributes such as SAF and low-sulfur fuels. Operational reliability at major hubs is a competitive differentiator but rarely creates full lock-in. Co-investment in decarbonized fuels can deepen relationships; industry targets like IATA net-zero by 2050 and IMO 50% GHG reduction by 2050 raise customers′ leverage on suppliers.

Lubricants OEM and aftermarket

Automakers and industrial OEMs set technical specs and certification gates that limit suppliers and allow approved lubricants to command price premiums; OEM approvals drive long-term contracts and accounted for a large share of B2B volumes in 2024, supporting stronger margins for certified suppliers vs commodity grades. Aftermarket demand is fragmented but brand-aware, with private labels and global brands expanding buyer choice while technical support and extended drain intervals create modest switching frictions.

- Global lubricant market ~38 billion USD (2024)

- OEM-certified products often command price premiums

- Private labels vs global brands increase buyer options

- Technical support and drain intervals reduce churn

Petrochemicals customers

Commodity petrochemical buyers arbitrage across Asian suppliers, driving tighter margins and intensifying price competition; spot volumes rose to about 25% of regional trade in 2024 as buyers chased cost advantages. Contract/spot mixes swing with capacity cycles, while consistent quality and expedited logistics can secure premiums of 1–3%. Sustainability grades and recyclate integration are becoming active negotiation levers.

- Arbitrage across Asia — higher

- Spot share ~25% (2024)

- Quality/logistics = 1–3% premium

- Sustainability/recyclates = growing leverage

Wholesale margins squeezed: real-time pricing vs index deals; Brent ~87

Wholesale buyers are highly price-sensitive with low switching costs, pushing margins in 2024; real-time pricing amplifies this. Large industrials use index-linked multi-year contracts (Brent ~87 USD/bbl in 2024) to constrain supplier upside. Lubricant OEM approvals and technical support command premiums (global market ~38bn USD, 2024). Petrochemical spot share rose to ~25% (2024), tightening margins.

| Metric | 2024 |

|---|---|

| Brent avg | ~87 USD/bbl |

| Lubricant market | ~38 bn USD |

| Petrochemical spot share | ~25% |

Preview Before You Purchase

Idemitsu Kosan Porter's Five Forces Analysis

This Idemitsu Kosan Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—fully formatted, complete and ready for immediate download. No placeholders or samples; the content shown is the final deliverable. Buy once and gain instant access to this precise analysis for your strategic or investment use.

Description

Don't Miss the Bigger Picture

Idemitsu Kosan faces intense rivalry across refining and petrochemicals, moderate supplier power, evolving buyer dynamics, rising substitute threats from renewables, and regulatory barriers shaping margins and strategy; this snapshot highlights key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated crude sources

Idemitsu relies on a concentrated set of crude suppliers—OPEC+ which controls roughly 50% of global oil output in 2024—and select national oil companies, giving those suppliers pricing and volume leverage. Supply disruptions or quota changes transmit quickly into refinery feedstock costs and margins. Diversifying grades and long-term contracts reduce but do not remove exposure. Hedging cuts volatility but cannot counter structural supplier concentration.

LNG and coal feedstock leverage

Global LNG and coal markets remain tight and cyclical, giving upstream producers strong leverage on pricing and indexation; spot JKM volatility has fallen but long-term contracts still command premium. Japan imports over 90% of its gas and nearly all coal, magnifying exposure to freight and JPY/USD swings. Long-term take-or-pay deals—covering roughly 60–80% of volumes—reduce spot exposure but lock in obligations, while origin and index diversification moderates counterparty power.

Process licensors and OEMs

Refining and petrochemical units, including Idemitsu Kosan, rely on a small set of process licensors such as Honeywell UOP, Axens and Lummus Technologies, and critical OEMs for compressors and control systems. Limited alternatives for catalysts, compressors and DCS raise switching costs and allow suppliers to command service and replacement margins. The global refinery catalyst market was about USD 9.2 billion in 2024, underscoring supplier leverage. Multi-sourcing and standardization mitigate but do not eliminate technical lock-in.

Maritime logistics constraints

Tanker availability and marine fuel costs materially affect landed feedstock economics; port congestion and chokepoints like the Suez Canal (≈12% of global seaborne trade in 2024) can shift bargaining power to shipowners, while long-term charters and preferred fleet relationships provide partial insulation; insurance and regulatory compliance narrow the pool of viable carriers.

- Tanker availability

- Marine fuel cost impact

- Chokepoints boost shipowner leverage

- Charters/fleet ties mitigate risk

- Insurance/compliance concentrate carriers

Renewables component suppliers

For solar, wind and geothermal projects, turbine, module and inverter suppliers can extract leverage in upcycles—spot module prices swung ~20–30% in 2023–24 and OEM lead times extended to 4–8 months in peak demand, pressuring developers like Idemitsu Kosan. Trade policies and tariffs have raised component costs by roughly 10–25% in targeted markets, while framework agreements and onshore localization programs have mitigated some exposure. Performance guarantees and availability clauses partially rebalance bargaining power toward developers by tying payments to output and reliability.

- Upcycle price swing: ~20–30% (2023–24)

- Typical lead times: 4–8 months in peak periods

- Tariff/cost impact: ~10–25% in affected markets

- Mitigants: framework agreements, localization, performance guarantees

Concentrated crude supply and tight LNG/coal markets strengthen supplier power

Idemitsu faces concentrated crude suppliers (OPEC+ ~50% of global output in 2024) and tight LNG/coal markets, giving upstreams strong price leverage. Technical licensors and catalyst suppliers (global catalyst market ~USD 9.2bn in 2024) and tanker/chokepoint risks (Suez ~12% seaborne trade) raise switching costs. Long-term contracts, hedges and charters mitigate but do not remove supplier power.

| Factor | 2024 metric |

|---|---|

| OPEC+ share | ~50% |

| Japan gas imports | >90% |

| Catalyst market | USD 9.2bn |

| Suez trade | ~12% |

What is included in the product

Tailored Porter’s Five Forces analysis of Idemitsu Kosan uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic barriers protecting incumbency. Identifies disruptive forces, pricing pressures, and strategic levers to inform investors, managers, and academics.

A one-sheet Porter's Five Forces for Idemitsu Kosan highlighting supplier power, buyer pressure, rivalry, substitutes, and entry threats—clean, customizable, and ready to drop into decks for fast strategic decision-making and boardroom clarity.

Customers Bargaining Power

Price-sensitive fuel buyers

Wholesale and retail fuel buyers remain highly price-sensitive with low switching costs, pressuring margins in 2024. Real-time price boards and comparison platforms have intensified transparency and accelerated price-driven behavior. Loyalty programs and convenience offerings deliver limited differentiation against pure price competition. Idemitsu’s regional footprint and logistics reliability are key levers to retain volumes.

Industrial and utility contracts

Large industrials and power utilities negotiate multi-year fuel and feedstock contracts, leveraging scale and the ability to dual-source to extract discounts and flexibility from suppliers like Idemitsu. Index-linked formulas tied to benchmarks such as Brent (Brent averaged about 87 USD/bbl in 2024) limit supplier margin upside while protecting buyers from spot volatility. Performance bonuses and security-of-supply clauses (firm delivery windows, take-or-pay adjustments) soften pure price pressure by valuing reliability and penalties, narrowing buyer bargaining to service-plus-price tradeoffs.

Aviation and marine customers

Aviation and marine customers pool procurement and benchmark globally, pushing down premiums and demanding services plus sustainability attributes such as SAF and low-sulfur fuels. Operational reliability at major hubs is a competitive differentiator but rarely creates full lock-in. Co-investment in decarbonized fuels can deepen relationships; industry targets like IATA net-zero by 2050 and IMO 50% GHG reduction by 2050 raise customers′ leverage on suppliers.

Lubricants OEM and aftermarket

Automakers and industrial OEMs set technical specs and certification gates that limit suppliers and allow approved lubricants to command price premiums; OEM approvals drive long-term contracts and accounted for a large share of B2B volumes in 2024, supporting stronger margins for certified suppliers vs commodity grades. Aftermarket demand is fragmented but brand-aware, with private labels and global brands expanding buyer choice while technical support and extended drain intervals create modest switching frictions.

- Global lubricant market ~38 billion USD (2024)

- OEM-certified products often command price premiums

- Private labels vs global brands increase buyer options

- Technical support and drain intervals reduce churn

Petrochemicals customers

Commodity petrochemical buyers arbitrage across Asian suppliers, driving tighter margins and intensifying price competition; spot volumes rose to about 25% of regional trade in 2024 as buyers chased cost advantages. Contract/spot mixes swing with capacity cycles, while consistent quality and expedited logistics can secure premiums of 1–3%. Sustainability grades and recyclate integration are becoming active negotiation levers.

- Arbitrage across Asia — higher

- Spot share ~25% (2024)

- Quality/logistics = 1–3% premium

- Sustainability/recyclates = growing leverage

Wholesale margins squeezed: real-time pricing vs index deals; Brent ~87

Wholesale buyers are highly price-sensitive with low switching costs, pushing margins in 2024; real-time pricing amplifies this. Large industrials use index-linked multi-year contracts (Brent ~87 USD/bbl in 2024) to constrain supplier upside. Lubricant OEM approvals and technical support command premiums (global market ~38bn USD, 2024). Petrochemical spot share rose to ~25% (2024), tightening margins.

| Metric | 2024 |

|---|---|

| Brent avg | ~87 USD/bbl |

| Lubricant market | ~38 bn USD |

| Petrochemical spot share | ~25% |

Preview Before You Purchase

Idemitsu Kosan Porter's Five Forces Analysis

This Idemitsu Kosan Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—fully formatted, complete and ready for immediate download. No placeholders or samples; the content shown is the final deliverable. Buy once and gain instant access to this precise analysis for your strategic or investment use.