IDIS Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

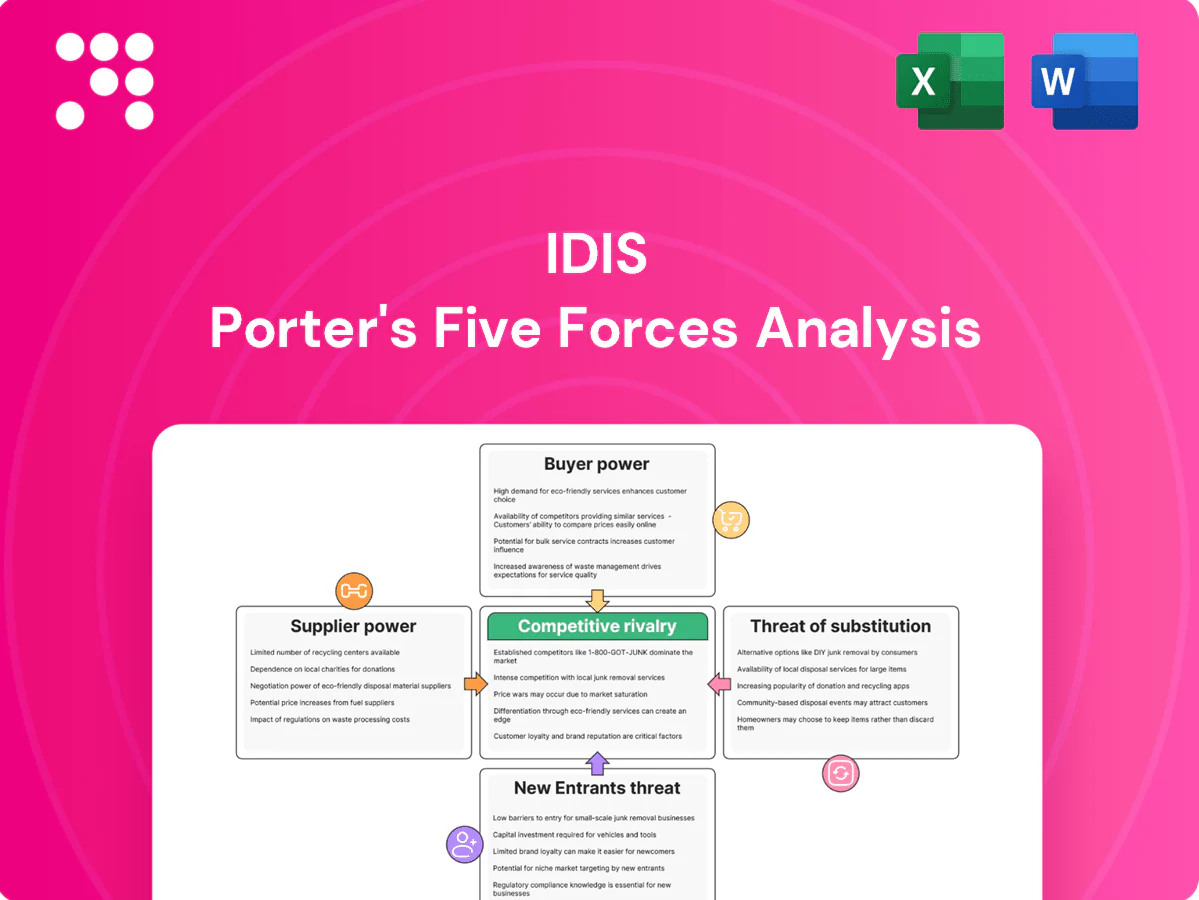

IDIS faces varied competitive pressures across Porter's Five Forces—supplier leverage, buyer consolidation, rivalry intensity, threat of entrants, and substitutes—that shape margins and strategic choices. This snapshot highlights key dynamics and tactical implications. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Semiconductor dependence

Core components—image sensors (Sony ~42% share in 2023), ISPs and AI SoCs—come from a concentrated supplier base (top vendors >70%), raising switching costs and lead-time risks. Geopolitics and 2023 US export controls on advanced nodes have disrupted access and certifications. IDIS uses dual-sourcing, platform flexibility, long-term supply contracts and buffer inventory but remains exposed to node shortages and vendor roadmaps, so cycle volatility persists.

Optics and storage inputs

Lenses, IR modules and HDDs/SSDs are concentrated among Tier-1 suppliers (HDDs: Seagate ~40%, WDC ~35%, Toshiba ~20% in 2024), giving suppliers pricing and allocation leverage. Tight performance specs (low-light sensitivity, MTBF) limit interchangeability and force 3–6 month validation cycles, slowing substitution. IDIS can qualify multiple vendors and use volume bundling across cameras/NVRs to extract price concessions (typ. 5–10%).

ODM/EMS and yield

Manufacturing partners directly affect IDIS cost, yield, and time-to-market, with EMS lead times and SMT capacity often dictating ramp speed; EMS labor costs in Southeast Asia rose roughly 5–10% in 2024, tightening supplier leverage. Tight labor markets and rising wages in South Korea and Vietnam increased bargaining power for EMS/ODM providers in 2024. IDIS’s in-house design and test capabilities limit dependence, but specialized SMT lines and optical calibration keep EMS partners strategically important. Geographic diversification of suppliers through 2024 lowered single-region disruption risk.

Software stack components

Third-party codecs, cyber modules and AI toolchains (SDKs, CUDA/OpenVINO equivalents) create vendor lock-in and license exposure; version support and security updates directly affect VMS reliability and regulatory compliance. IDIS offsets some risk with proprietary VMS and DirectIP while maintaining interoperability via ONVIF (18,000+ conformant products, 2024) and cloud connectors. Negotiating enterprise licenses at scale commonly reduces per-unit software costs by 15–30%.

- lock-in: third-party SDKs/codecs

- security: patch/version risk

- mitigation: IDIS DirectIP + ONVIF (18,000+)

- cost: enterprise licensing saves ~15–30%

Logistics and compliance

Global distribution mandates NDAA, TAA, CE and UL compliance, which narrows the qualified supplier pool and raises supplier leverage through certification premiums; IDIS’s brand depends on certified BOMs, limiting substitution and amplifying supplier power. Advanced planning and regional warehouses reduce exposure but do not remove compliance-driven leverage.

- Qualified suppliers constrained

- Certification premiums boost supplier margins

- Certified BOMs limit substitution

- Regional warehousing cushions risk

High supplier concentration raises costs and lead times; dual-sourcing and licensing reduce risk

Suppliers are highly concentrated (core image sensors/vendor share >70%; Sony ~42% in 2023), raising switching costs, lead-time and pricing risk. HDD/SSD and optics concentration (Seagate ~40%, WDC ~35%, Toshiba ~20% in 2024) plus EMS labor up 5–10% in 2024 increase supplier leverage. IDIS mitigates via dual-sourcing, long-term contracts, DirectIP/ONVIF (18,000+), and enterprise licensing discounts (15–30%).

| Metric | Value |

|---|---|

| Image sensor market | Sony ~42% (2023) |

| Top vendors (core) | >70% concentration |

| HDD shares (2024) | Seagate 40% / WDC 35% / Toshiba 20% |

| EMS labor change (2024) | +5–10% |

| ONVIF products (2024) | 18,000+ |

| License savings | 15–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis for IDIS that uncovers competitive drivers, buyer and supplier power, barriers to entry, and substitute threats, with data-backed insights and strategic implications. Fully editable for use in investor decks, business plans, or internal strategy reviews.

Single-sheet IDIS Porter's Five Forces that instantly highlights competitive pain points with a customizable radar chart and scenario tabs, clean layout ready for decks, no macros required—swap in your data to tailor insights for swift strategic decisions.

Customers Bargaining Power

Integrator-driven procurement

System integrators aggregate demand and steer vendor shortlists, increasing price pressure as they leverage scale across a global video surveillance market that exceeded $45 billion in 2023; ONVIF reported over 20,000 conformant products by 2024, lowering switching friction. IDIS must compete on TCO, ease-of-install via DirectIP, and targeted rebates, while strong channel programs can temper discount expectations.

Enterprise and public RFPs

In enterprise and public RFPs (2024) large contracts are awarded via competitive tenders that prioritize price, compliance, and SLA metrics; buyers routinely pit vendors to extract concessions. IDIS gains where performance and cybersecurity carry heavy weight—often 30–40% of RFP scoring—but still faces sharp bid pressure; multi‑year support commitments (commonly 3–5 years) serve as key differentiators.

Standardization lowers lock-in

ONVIF’s 500+ members and thousands of conformant products in 2024 plus open APIs reduce proprietary lock-in and raise buyer leverage. Deep VMS workflows and analytics integrations still impose moderate switching costs, and IDIS’s integrated suite increases stickiness once deployed. Migration tools and backward compatibility help retain accounts.

Performance and compliance sensitivity

Security buyers pay premiums for uptime and certifications and expect >99.9% SLAs; IBM reports average breach cost $4.45M (2023), so failures prompt rapid vendor replacement. IDIS must deliver frequent firmware patches and regular pen-tests to defend pricing, while transparent roadmaps and warranties calm risk-averse buyers.

- Uptime: >99.9% SLA

- Cost of breach: $4.45M (IBM 2023)

- Controls: frequent firmware + pen-tests

- Trust: roadmaps + warranties

Global price transparency

Global price transparency in 2024 lets online benchmarks and distributor networks expose street pricing, driving buyers to negotiate aggressively using comparable SKUs from Axis, Hanwha, Hikvision, and Dahua. IDIS counters with bundled solutions and superior service quality to sustain margins and protect ASPs. Regional value-add through local support and managed services softens price-only decisions and improves renewal rates.

- Benchmarking: online price exposure

- Buyers: aggressive SKU-based negotiation

- IDIS: bundles + service to defend margins

- Regional support: reduces price sensitivity

Price pressure in >$45B video market as ONVIF lowers switching friction

System integrators and global distributors aggregate demand, increasing price pressure in a video-surveillance market >$45B (2023) while ONVIF conformity (~20,000 products by 2024) lowers switching friction. Enterprise RFPs award 30–40% to performance/cybersecurity, yet buyers push aggressive SKU-based bids. IDIS defends via lower TCO (DirectIP), bundles, SLAs >99.9% and regional managed services.

| Metric | Value |

|---|---|

| Market size (2023) | $45B+ |

| ONVIF conformant (2024) | ~20,000 |

| RFP weight: perf/cyber | 30–40% |

| Required SLA | >99.9% |

| Avg breach cost (IBM 2023) | $4.45M |

Full Version Awaits

IDIS Porter's Five Forces Analysis

This preview shows the exact IDIS Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, sourced, and ready for use. The analysis covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and data-backed conclusions. No placeholders or mockups; download access is instant upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

IDIS faces varied competitive pressures across Porter's Five Forces—supplier leverage, buyer consolidation, rivalry intensity, threat of entrants, and substitutes—that shape margins and strategic choices. This snapshot highlights key dynamics and tactical implications. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Semiconductor dependence

Core components—image sensors (Sony ~42% share in 2023), ISPs and AI SoCs—come from a concentrated supplier base (top vendors >70%), raising switching costs and lead-time risks. Geopolitics and 2023 US export controls on advanced nodes have disrupted access and certifications. IDIS uses dual-sourcing, platform flexibility, long-term supply contracts and buffer inventory but remains exposed to node shortages and vendor roadmaps, so cycle volatility persists.

Optics and storage inputs

Lenses, IR modules and HDDs/SSDs are concentrated among Tier-1 suppliers (HDDs: Seagate ~40%, WDC ~35%, Toshiba ~20% in 2024), giving suppliers pricing and allocation leverage. Tight performance specs (low-light sensitivity, MTBF) limit interchangeability and force 3–6 month validation cycles, slowing substitution. IDIS can qualify multiple vendors and use volume bundling across cameras/NVRs to extract price concessions (typ. 5–10%).

ODM/EMS and yield

Manufacturing partners directly affect IDIS cost, yield, and time-to-market, with EMS lead times and SMT capacity often dictating ramp speed; EMS labor costs in Southeast Asia rose roughly 5–10% in 2024, tightening supplier leverage. Tight labor markets and rising wages in South Korea and Vietnam increased bargaining power for EMS/ODM providers in 2024. IDIS’s in-house design and test capabilities limit dependence, but specialized SMT lines and optical calibration keep EMS partners strategically important. Geographic diversification of suppliers through 2024 lowered single-region disruption risk.

Software stack components

Third-party codecs, cyber modules and AI toolchains (SDKs, CUDA/OpenVINO equivalents) create vendor lock-in and license exposure; version support and security updates directly affect VMS reliability and regulatory compliance. IDIS offsets some risk with proprietary VMS and DirectIP while maintaining interoperability via ONVIF (18,000+ conformant products, 2024) and cloud connectors. Negotiating enterprise licenses at scale commonly reduces per-unit software costs by 15–30%.

- lock-in: third-party SDKs/codecs

- security: patch/version risk

- mitigation: IDIS DirectIP + ONVIF (18,000+)

- cost: enterprise licensing saves ~15–30%

Logistics and compliance

Global distribution mandates NDAA, TAA, CE and UL compliance, which narrows the qualified supplier pool and raises supplier leverage through certification premiums; IDIS’s brand depends on certified BOMs, limiting substitution and amplifying supplier power. Advanced planning and regional warehouses reduce exposure but do not remove compliance-driven leverage.

- Qualified suppliers constrained

- Certification premiums boost supplier margins

- Certified BOMs limit substitution

- Regional warehousing cushions risk

High supplier concentration raises costs and lead times; dual-sourcing and licensing reduce risk

Suppliers are highly concentrated (core image sensors/vendor share >70%; Sony ~42% in 2023), raising switching costs, lead-time and pricing risk. HDD/SSD and optics concentration (Seagate ~40%, WDC ~35%, Toshiba ~20% in 2024) plus EMS labor up 5–10% in 2024 increase supplier leverage. IDIS mitigates via dual-sourcing, long-term contracts, DirectIP/ONVIF (18,000+), and enterprise licensing discounts (15–30%).

| Metric | Value |

|---|---|

| Image sensor market | Sony ~42% (2023) |

| Top vendors (core) | >70% concentration |

| HDD shares (2024) | Seagate 40% / WDC 35% / Toshiba 20% |

| EMS labor change (2024) | +5–10% |

| ONVIF products (2024) | 18,000+ |

| License savings | 15–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis for IDIS that uncovers competitive drivers, buyer and supplier power, barriers to entry, and substitute threats, with data-backed insights and strategic implications. Fully editable for use in investor decks, business plans, or internal strategy reviews.

Single-sheet IDIS Porter's Five Forces that instantly highlights competitive pain points with a customizable radar chart and scenario tabs, clean layout ready for decks, no macros required—swap in your data to tailor insights for swift strategic decisions.

Customers Bargaining Power

Integrator-driven procurement

System integrators aggregate demand and steer vendor shortlists, increasing price pressure as they leverage scale across a global video surveillance market that exceeded $45 billion in 2023; ONVIF reported over 20,000 conformant products by 2024, lowering switching friction. IDIS must compete on TCO, ease-of-install via DirectIP, and targeted rebates, while strong channel programs can temper discount expectations.

Enterprise and public RFPs

In enterprise and public RFPs (2024) large contracts are awarded via competitive tenders that prioritize price, compliance, and SLA metrics; buyers routinely pit vendors to extract concessions. IDIS gains where performance and cybersecurity carry heavy weight—often 30–40% of RFP scoring—but still faces sharp bid pressure; multi‑year support commitments (commonly 3–5 years) serve as key differentiators.

Standardization lowers lock-in

ONVIF’s 500+ members and thousands of conformant products in 2024 plus open APIs reduce proprietary lock-in and raise buyer leverage. Deep VMS workflows and analytics integrations still impose moderate switching costs, and IDIS’s integrated suite increases stickiness once deployed. Migration tools and backward compatibility help retain accounts.

Performance and compliance sensitivity

Security buyers pay premiums for uptime and certifications and expect >99.9% SLAs; IBM reports average breach cost $4.45M (2023), so failures prompt rapid vendor replacement. IDIS must deliver frequent firmware patches and regular pen-tests to defend pricing, while transparent roadmaps and warranties calm risk-averse buyers.

- Uptime: >99.9% SLA

- Cost of breach: $4.45M (IBM 2023)

- Controls: frequent firmware + pen-tests

- Trust: roadmaps + warranties

Global price transparency

Global price transparency in 2024 lets online benchmarks and distributor networks expose street pricing, driving buyers to negotiate aggressively using comparable SKUs from Axis, Hanwha, Hikvision, and Dahua. IDIS counters with bundled solutions and superior service quality to sustain margins and protect ASPs. Regional value-add through local support and managed services softens price-only decisions and improves renewal rates.

- Benchmarking: online price exposure

- Buyers: aggressive SKU-based negotiation

- IDIS: bundles + service to defend margins

- Regional support: reduces price sensitivity

Price pressure in >$45B video market as ONVIF lowers switching friction

System integrators and global distributors aggregate demand, increasing price pressure in a video-surveillance market >$45B (2023) while ONVIF conformity (~20,000 products by 2024) lowers switching friction. Enterprise RFPs award 30–40% to performance/cybersecurity, yet buyers push aggressive SKU-based bids. IDIS defends via lower TCO (DirectIP), bundles, SLAs >99.9% and regional managed services.

| Metric | Value |

|---|---|

| Market size (2023) | $45B+ |

| ONVIF conformant (2024) | ~20,000 |

| RFP weight: perf/cyber | 30–40% |

| Required SLA | >99.9% |

| Avg breach cost (IBM 2023) | $4.45M |

Full Version Awaits

IDIS Porter's Five Forces Analysis

This preview shows the exact IDIS Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, sourced, and ready for use. The analysis covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and data-backed conclusions. No placeholders or mockups; download access is instant upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

IDIS faces varied competitive pressures across Porter's Five Forces—supplier leverage, buyer consolidation, rivalry intensity, threat of entrants, and substitutes—that shape margins and strategic choices. This snapshot highlights key dynamics and tactical implications. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Semiconductor dependence

Core components—image sensors (Sony ~42% share in 2023), ISPs and AI SoCs—come from a concentrated supplier base (top vendors >70%), raising switching costs and lead-time risks. Geopolitics and 2023 US export controls on advanced nodes have disrupted access and certifications. IDIS uses dual-sourcing, platform flexibility, long-term supply contracts and buffer inventory but remains exposed to node shortages and vendor roadmaps, so cycle volatility persists.

Optics and storage inputs

Lenses, IR modules and HDDs/SSDs are concentrated among Tier-1 suppliers (HDDs: Seagate ~40%, WDC ~35%, Toshiba ~20% in 2024), giving suppliers pricing and allocation leverage. Tight performance specs (low-light sensitivity, MTBF) limit interchangeability and force 3–6 month validation cycles, slowing substitution. IDIS can qualify multiple vendors and use volume bundling across cameras/NVRs to extract price concessions (typ. 5–10%).

ODM/EMS and yield

Manufacturing partners directly affect IDIS cost, yield, and time-to-market, with EMS lead times and SMT capacity often dictating ramp speed; EMS labor costs in Southeast Asia rose roughly 5–10% in 2024, tightening supplier leverage. Tight labor markets and rising wages in South Korea and Vietnam increased bargaining power for EMS/ODM providers in 2024. IDIS’s in-house design and test capabilities limit dependence, but specialized SMT lines and optical calibration keep EMS partners strategically important. Geographic diversification of suppliers through 2024 lowered single-region disruption risk.

Software stack components

Third-party codecs, cyber modules and AI toolchains (SDKs, CUDA/OpenVINO equivalents) create vendor lock-in and license exposure; version support and security updates directly affect VMS reliability and regulatory compliance. IDIS offsets some risk with proprietary VMS and DirectIP while maintaining interoperability via ONVIF (18,000+ conformant products, 2024) and cloud connectors. Negotiating enterprise licenses at scale commonly reduces per-unit software costs by 15–30%.

- lock-in: third-party SDKs/codecs

- security: patch/version risk

- mitigation: IDIS DirectIP + ONVIF (18,000+)

- cost: enterprise licensing saves ~15–30%

Logistics and compliance

Global distribution mandates NDAA, TAA, CE and UL compliance, which narrows the qualified supplier pool and raises supplier leverage through certification premiums; IDIS’s brand depends on certified BOMs, limiting substitution and amplifying supplier power. Advanced planning and regional warehouses reduce exposure but do not remove compliance-driven leverage.

- Qualified suppliers constrained

- Certification premiums boost supplier margins

- Certified BOMs limit substitution

- Regional warehousing cushions risk

High supplier concentration raises costs and lead times; dual-sourcing and licensing reduce risk

Suppliers are highly concentrated (core image sensors/vendor share >70%; Sony ~42% in 2023), raising switching costs, lead-time and pricing risk. HDD/SSD and optics concentration (Seagate ~40%, WDC ~35%, Toshiba ~20% in 2024) plus EMS labor up 5–10% in 2024 increase supplier leverage. IDIS mitigates via dual-sourcing, long-term contracts, DirectIP/ONVIF (18,000+), and enterprise licensing discounts (15–30%).

| Metric | Value |

|---|---|

| Image sensor market | Sony ~42% (2023) |

| Top vendors (core) | >70% concentration |

| HDD shares (2024) | Seagate 40% / WDC 35% / Toshiba 20% |

| EMS labor change (2024) | +5–10% |

| ONVIF products (2024) | 18,000+ |

| License savings | 15–30% |

What is included in the product

Comprehensive Porter's Five Forces analysis for IDIS that uncovers competitive drivers, buyer and supplier power, barriers to entry, and substitute threats, with data-backed insights and strategic implications. Fully editable for use in investor decks, business plans, or internal strategy reviews.

Single-sheet IDIS Porter's Five Forces that instantly highlights competitive pain points with a customizable radar chart and scenario tabs, clean layout ready for decks, no macros required—swap in your data to tailor insights for swift strategic decisions.

Customers Bargaining Power

Integrator-driven procurement

System integrators aggregate demand and steer vendor shortlists, increasing price pressure as they leverage scale across a global video surveillance market that exceeded $45 billion in 2023; ONVIF reported over 20,000 conformant products by 2024, lowering switching friction. IDIS must compete on TCO, ease-of-install via DirectIP, and targeted rebates, while strong channel programs can temper discount expectations.

Enterprise and public RFPs

In enterprise and public RFPs (2024) large contracts are awarded via competitive tenders that prioritize price, compliance, and SLA metrics; buyers routinely pit vendors to extract concessions. IDIS gains where performance and cybersecurity carry heavy weight—often 30–40% of RFP scoring—but still faces sharp bid pressure; multi‑year support commitments (commonly 3–5 years) serve as key differentiators.

Standardization lowers lock-in

ONVIF’s 500+ members and thousands of conformant products in 2024 plus open APIs reduce proprietary lock-in and raise buyer leverage. Deep VMS workflows and analytics integrations still impose moderate switching costs, and IDIS’s integrated suite increases stickiness once deployed. Migration tools and backward compatibility help retain accounts.

Performance and compliance sensitivity

Security buyers pay premiums for uptime and certifications and expect >99.9% SLAs; IBM reports average breach cost $4.45M (2023), so failures prompt rapid vendor replacement. IDIS must deliver frequent firmware patches and regular pen-tests to defend pricing, while transparent roadmaps and warranties calm risk-averse buyers.

- Uptime: >99.9% SLA

- Cost of breach: $4.45M (IBM 2023)

- Controls: frequent firmware + pen-tests

- Trust: roadmaps + warranties

Global price transparency

Global price transparency in 2024 lets online benchmarks and distributor networks expose street pricing, driving buyers to negotiate aggressively using comparable SKUs from Axis, Hanwha, Hikvision, and Dahua. IDIS counters with bundled solutions and superior service quality to sustain margins and protect ASPs. Regional value-add through local support and managed services softens price-only decisions and improves renewal rates.

- Benchmarking: online price exposure

- Buyers: aggressive SKU-based negotiation

- IDIS: bundles + service to defend margins

- Regional support: reduces price sensitivity

Price pressure in >$45B video market as ONVIF lowers switching friction

System integrators and global distributors aggregate demand, increasing price pressure in a video-surveillance market >$45B (2023) while ONVIF conformity (~20,000 products by 2024) lowers switching friction. Enterprise RFPs award 30–40% to performance/cybersecurity, yet buyers push aggressive SKU-based bids. IDIS defends via lower TCO (DirectIP), bundles, SLAs >99.9% and regional managed services.

| Metric | Value |

|---|---|

| Market size (2023) | $45B+ |

| ONVIF conformant (2024) | ~20,000 |

| RFP weight: perf/cyber | 30–40% |

| Required SLA | >99.9% |

| Avg breach cost (IBM 2023) | $4.45M |

Full Version Awaits

IDIS Porter's Five Forces Analysis

This preview shows the exact IDIS Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, sourced, and ready for use. The analysis covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and data-backed conclusions. No placeholders or mockups; download access is instant upon payment.