IDIS SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Explore IDIS's competitive edge, risk profile, and growth levers in this concise SWOT preview. Our full SWOT analysis delivers research-backed detail, financial context, and strategic recommendations to inform investment or planning decisions. Purchase the complete report for an editable Word and Excel package you can use immediately. Make confident, data-driven moves with the full analysis.

Strengths

End-to-end ecosystem

Owning cameras, NVRs and VMS lets IDIS deliver tight integration and a consistent UX, simplifying deployment and reducing interoperability headaches for integrators. This vertical stack shortens installation time and eases lifecycle management while optimizing performance across hardware and software. Cross-selling across the stack increases customer lock-in and switching costs; the global video surveillance market was forecast at about $79.6B by 2025 (MarketsandMarkets 2024).

DirectIP simplicity

DirectIP streamlines configuration, device discovery and security policy setup, enabling plug-and-play deployments that vendors report can reduce installation time by up to 50% and materially lower total cost of ownership for customers and partners.

Fewer touchpoints in commissioning and maintenance translate to fewer failure modes in the field, supporting higher uptime and lower service spend.

This value proposition is especially resonant in multi-site rollouts where limited IT resources constrain projects in an estimated two-thirds of deployments.

Performance and reliability

IDIS leverages high-definition 4K (8MP) imaging and stable recording architectures, making its solutions suitable for mission-critical sites. The company maintains in-house R&D and manufacturing in South Korea, integrating QA from design through production to improve hardware reliability. Regular firmware and IDIS Center VMS updates support consistent uptime and maintenance. This track record reinforces trust with enterprise and regulated clients.

Global vertical coverage

IDIS solutions span retail, logistics, education, healthcare, hospitality and critical infrastructure, with verticalized features like POS integration and people counting that broaden applicability and reduce customization time; reference deployments accelerate sales cycles. IDIS maintains offices in South Korea, the UK and the US and a partner network across 100+ countries, enabling localized support and faster rollouts.

- Vertical coverage: retail, logistics, education, healthcare, hospitality, critical infrastructure

- Vertical features: POS integration, people counting

- Reference deployments: shorten sales cycles

- Global reach: offices in South Korea, UK, US; partners in 100+ countries

Ease of compatibility

Ease of compatibility via FEN and standards-based interoperability reduces integration friction with third-party systems and supports mixed estates and phased upgrades, aiding migration from legacy DVR/NVR environments. This lowers deployment time and customer churn while preserving IDIS core differentiation. As of 2024 ONVIF and standards remain central to cross-vendor compatibility in surveillance deployments.

- FEN + standards: smoother third-party integration

- Supports mixed estates & phased upgrades

- Facilitates legacy DVR/NVR migration

Vertical security stack halves install time (50%), raises uptime, market $79.6B

IDIS vertical stack (cameras, NVR, VMS) enables integrated UX, faster installs and higher uptime; DirectIP can cut installation time up to 50% and lowers TCO. Global video surveillance market ~$79.6B by 2025 (MarketsandMarkets 2024). Offices in SK/UK/US; partners in 100+ countries.

| Metric | Value |

|---|---|

| Install time reduction | Up to 50% |

| Market size 2025 | $79.6B |

| Partner footprint | 100+ countries |

What is included in the product

Provides a concise SWOT framework analyzing IDIS’s strengths, weaknesses, opportunities, and threats, highlighting competitive advantages, operational gaps, market opportunities, and external risks shaping its strategic trajectory.

Provides a concise, ready-to-use IDIS SWOT matrix for fast strategy alignment and stakeholder briefs; editable format enables quick updates to reflect shifting risks and opportunities.

Weaknesses

Proprietary lock-in risk

While DirectIP simplifies deployment, it is often perceived as proprietary compared with open, ONVIF-conformant systems; ONVIF lists 20,000+ conformant products (2024). Many enterprises follow cloud-first approaches—Gartner estimated 80% of organizations would adopt cloud-first strategies by 2025—so ONVIF-first RFPs are common. That preference limits inclusion in RFPs emphasizing vendor diversity and can elongate sales cycles.

Brand visibility gap

Against giants like Hikvision (≈25% global market share in 2023), Dahua (≈12%), Axis (≈6%) and Hanwha (≈6%), IDIS faces lower global brand recall. Limited marketing scale reduces top-of-funnel leads versus these incumbents. End users often default to incumbents with broader mindshare, reflected in channel preference trends. Winning enterprise deals requires extra proof-of-concept effort and extended pilots.

Channel concentration

Heavy dependence on distributor/integrator networks creates sales volatility; IDC reported in 2024 that about 68% of physical security solutions were sold through channel partners, exposing vendors like IDIS to partner-driven demand swings. Misaligned incentives can push lowest-cost alternatives, eroding margin. Limited direct enterprise relationships reduce product feedback loops for roadmap prioritization, while partner enablement and certification complexity add significant overhead.

Hardware margin exposure

IDIS shows hardware margin exposure: revenue remains device-heavy while ASP pressure saw industry hardware prices decline ~5–10% year‑over‑year in 2024, squeezing margins as sensor, memory and SoC costs remain volatile. Without scaled SaaS/recurring streams, recurring revenue trails software-first peers; software-heavy rivals continue to out-invest in R&D, widening capability gaps.

- device-concentration: higher price sensitivity

- component-cost swings: sensors/memory/SoCs

- recurring-rev shortfall vs software peers

- competitors invest more in R&D

Scale of R&D

Keeping pace in AI analytics, cybersecurity and cloud requires sizable investment; IDC reported global spending on AI systems reached 154 billion USD in 2023, pressuring mid-sized vendors. Larger rivals iterate faster on edge AI and VSaaS, widening feature gaps. Fragmented regional compliance (NIS2, varied US state privacy laws) adds workload and roadmap trade-offs risk feature gaps in verticals.

- High R&D capex vs larger rivals

- Slower AI/VSaaS iteration

- Compliance fragmentation burden

- Roadmap trade-offs → vertical gaps

Proprietary vendor lagging vs 20,000+ ONVIF devices; cloud-first shift and AI lag squeeze margins

IDIS faces proprietary perception vs 20,000+ ONVIF products (2024), limiting RFP inclusion amid Gartner's 80% cloud‑first trend (2025). Lower global brand recall vs Hikvision (~25% 2023), Dahua (~12%), Axis/Hanwha (~6% each) increases proof‑of‑concept needs. Channel dependence (68% channel sales, IDC 2024), hardware ASP decline (~5–10% 2024) and lagging AI spend (global AI systems $154B 2023) pressure margins and roadmap speed.

| Metric | Value |

|---|---|

| ONVIF conformant products (2024) | 20,000+ |

| Cloud‑first orgs (Gartner) | 80% by 2025 |

| Top vendor share (Hikvision, 2023) | ≈25% |

| Channel sales (IDC, 2024) | 68% |

| Hardware ASP change (2024) | −5 to −10% |

| Global AI systems spend (2023) | $154B |

What You See Is What You Get

IDIS SWOT Analysis

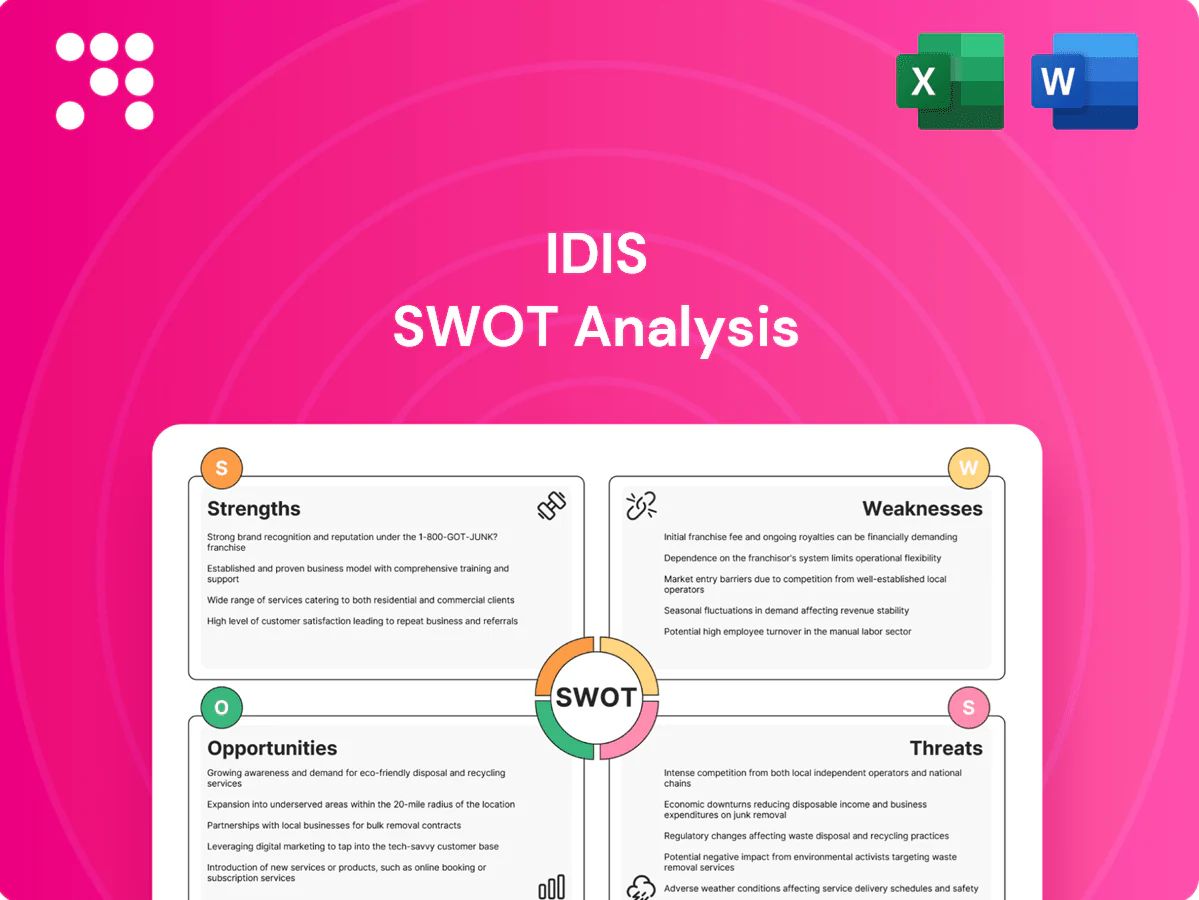

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and purchase unlocks the complete, editable version. You’re viewing a live preview of the real file; the full document becomes available after checkout.

Elevate Your Analysis with the Complete SWOT Report

Explore IDIS's competitive edge, risk profile, and growth levers in this concise SWOT preview. Our full SWOT analysis delivers research-backed detail, financial context, and strategic recommendations to inform investment or planning decisions. Purchase the complete report for an editable Word and Excel package you can use immediately. Make confident, data-driven moves with the full analysis.

Strengths

End-to-end ecosystem

Owning cameras, NVRs and VMS lets IDIS deliver tight integration and a consistent UX, simplifying deployment and reducing interoperability headaches for integrators. This vertical stack shortens installation time and eases lifecycle management while optimizing performance across hardware and software. Cross-selling across the stack increases customer lock-in and switching costs; the global video surveillance market was forecast at about $79.6B by 2025 (MarketsandMarkets 2024).

DirectIP simplicity

DirectIP streamlines configuration, device discovery and security policy setup, enabling plug-and-play deployments that vendors report can reduce installation time by up to 50% and materially lower total cost of ownership for customers and partners.

Fewer touchpoints in commissioning and maintenance translate to fewer failure modes in the field, supporting higher uptime and lower service spend.

This value proposition is especially resonant in multi-site rollouts where limited IT resources constrain projects in an estimated two-thirds of deployments.

Performance and reliability

IDIS leverages high-definition 4K (8MP) imaging and stable recording architectures, making its solutions suitable for mission-critical sites. The company maintains in-house R&D and manufacturing in South Korea, integrating QA from design through production to improve hardware reliability. Regular firmware and IDIS Center VMS updates support consistent uptime and maintenance. This track record reinforces trust with enterprise and regulated clients.

Global vertical coverage

IDIS solutions span retail, logistics, education, healthcare, hospitality and critical infrastructure, with verticalized features like POS integration and people counting that broaden applicability and reduce customization time; reference deployments accelerate sales cycles. IDIS maintains offices in South Korea, the UK and the US and a partner network across 100+ countries, enabling localized support and faster rollouts.

- Vertical coverage: retail, logistics, education, healthcare, hospitality, critical infrastructure

- Vertical features: POS integration, people counting

- Reference deployments: shorten sales cycles

- Global reach: offices in South Korea, UK, US; partners in 100+ countries

Ease of compatibility

Ease of compatibility via FEN and standards-based interoperability reduces integration friction with third-party systems and supports mixed estates and phased upgrades, aiding migration from legacy DVR/NVR environments. This lowers deployment time and customer churn while preserving IDIS core differentiation. As of 2024 ONVIF and standards remain central to cross-vendor compatibility in surveillance deployments.

- FEN + standards: smoother third-party integration

- Supports mixed estates & phased upgrades

- Facilitates legacy DVR/NVR migration

Vertical security stack halves install time (50%), raises uptime, market $79.6B

IDIS vertical stack (cameras, NVR, VMS) enables integrated UX, faster installs and higher uptime; DirectIP can cut installation time up to 50% and lowers TCO. Global video surveillance market ~$79.6B by 2025 (MarketsandMarkets 2024). Offices in SK/UK/US; partners in 100+ countries.

| Metric | Value |

|---|---|

| Install time reduction | Up to 50% |

| Market size 2025 | $79.6B |

| Partner footprint | 100+ countries |

What is included in the product

Provides a concise SWOT framework analyzing IDIS’s strengths, weaknesses, opportunities, and threats, highlighting competitive advantages, operational gaps, market opportunities, and external risks shaping its strategic trajectory.

Provides a concise, ready-to-use IDIS SWOT matrix for fast strategy alignment and stakeholder briefs; editable format enables quick updates to reflect shifting risks and opportunities.

Weaknesses

Proprietary lock-in risk

While DirectIP simplifies deployment, it is often perceived as proprietary compared with open, ONVIF-conformant systems; ONVIF lists 20,000+ conformant products (2024). Many enterprises follow cloud-first approaches—Gartner estimated 80% of organizations would adopt cloud-first strategies by 2025—so ONVIF-first RFPs are common. That preference limits inclusion in RFPs emphasizing vendor diversity and can elongate sales cycles.

Brand visibility gap

Against giants like Hikvision (≈25% global market share in 2023), Dahua (≈12%), Axis (≈6%) and Hanwha (≈6%), IDIS faces lower global brand recall. Limited marketing scale reduces top-of-funnel leads versus these incumbents. End users often default to incumbents with broader mindshare, reflected in channel preference trends. Winning enterprise deals requires extra proof-of-concept effort and extended pilots.

Channel concentration

Heavy dependence on distributor/integrator networks creates sales volatility; IDC reported in 2024 that about 68% of physical security solutions were sold through channel partners, exposing vendors like IDIS to partner-driven demand swings. Misaligned incentives can push lowest-cost alternatives, eroding margin. Limited direct enterprise relationships reduce product feedback loops for roadmap prioritization, while partner enablement and certification complexity add significant overhead.

Hardware margin exposure

IDIS shows hardware margin exposure: revenue remains device-heavy while ASP pressure saw industry hardware prices decline ~5–10% year‑over‑year in 2024, squeezing margins as sensor, memory and SoC costs remain volatile. Without scaled SaaS/recurring streams, recurring revenue trails software-first peers; software-heavy rivals continue to out-invest in R&D, widening capability gaps.

- device-concentration: higher price sensitivity

- component-cost swings: sensors/memory/SoCs

- recurring-rev shortfall vs software peers

- competitors invest more in R&D

Scale of R&D

Keeping pace in AI analytics, cybersecurity and cloud requires sizable investment; IDC reported global spending on AI systems reached 154 billion USD in 2023, pressuring mid-sized vendors. Larger rivals iterate faster on edge AI and VSaaS, widening feature gaps. Fragmented regional compliance (NIS2, varied US state privacy laws) adds workload and roadmap trade-offs risk feature gaps in verticals.

- High R&D capex vs larger rivals

- Slower AI/VSaaS iteration

- Compliance fragmentation burden

- Roadmap trade-offs → vertical gaps

Proprietary vendor lagging vs 20,000+ ONVIF devices; cloud-first shift and AI lag squeeze margins

IDIS faces proprietary perception vs 20,000+ ONVIF products (2024), limiting RFP inclusion amid Gartner's 80% cloud‑first trend (2025). Lower global brand recall vs Hikvision (~25% 2023), Dahua (~12%), Axis/Hanwha (~6% each) increases proof‑of‑concept needs. Channel dependence (68% channel sales, IDC 2024), hardware ASP decline (~5–10% 2024) and lagging AI spend (global AI systems $154B 2023) pressure margins and roadmap speed.

| Metric | Value |

|---|---|

| ONVIF conformant products (2024) | 20,000+ |

| Cloud‑first orgs (Gartner) | 80% by 2025 |

| Top vendor share (Hikvision, 2023) | ≈25% |

| Channel sales (IDC, 2024) | 68% |

| Hardware ASP change (2024) | −5 to −10% |

| Global AI systems spend (2023) | $154B |

What You See Is What You Get

IDIS SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and purchase unlocks the complete, editable version. You’re viewing a live preview of the real file; the full document becomes available after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

Explore IDIS's competitive edge, risk profile, and growth levers in this concise SWOT preview. Our full SWOT analysis delivers research-backed detail, financial context, and strategic recommendations to inform investment or planning decisions. Purchase the complete report for an editable Word and Excel package you can use immediately. Make confident, data-driven moves with the full analysis.

Strengths

End-to-end ecosystem

Owning cameras, NVRs and VMS lets IDIS deliver tight integration and a consistent UX, simplifying deployment and reducing interoperability headaches for integrators. This vertical stack shortens installation time and eases lifecycle management while optimizing performance across hardware and software. Cross-selling across the stack increases customer lock-in and switching costs; the global video surveillance market was forecast at about $79.6B by 2025 (MarketsandMarkets 2024).

DirectIP simplicity

DirectIP streamlines configuration, device discovery and security policy setup, enabling plug-and-play deployments that vendors report can reduce installation time by up to 50% and materially lower total cost of ownership for customers and partners.

Fewer touchpoints in commissioning and maintenance translate to fewer failure modes in the field, supporting higher uptime and lower service spend.

This value proposition is especially resonant in multi-site rollouts where limited IT resources constrain projects in an estimated two-thirds of deployments.

Performance and reliability

IDIS leverages high-definition 4K (8MP) imaging and stable recording architectures, making its solutions suitable for mission-critical sites. The company maintains in-house R&D and manufacturing in South Korea, integrating QA from design through production to improve hardware reliability. Regular firmware and IDIS Center VMS updates support consistent uptime and maintenance. This track record reinforces trust with enterprise and regulated clients.

Global vertical coverage

IDIS solutions span retail, logistics, education, healthcare, hospitality and critical infrastructure, with verticalized features like POS integration and people counting that broaden applicability and reduce customization time; reference deployments accelerate sales cycles. IDIS maintains offices in South Korea, the UK and the US and a partner network across 100+ countries, enabling localized support and faster rollouts.

- Vertical coverage: retail, logistics, education, healthcare, hospitality, critical infrastructure

- Vertical features: POS integration, people counting

- Reference deployments: shorten sales cycles

- Global reach: offices in South Korea, UK, US; partners in 100+ countries

Ease of compatibility

Ease of compatibility via FEN and standards-based interoperability reduces integration friction with third-party systems and supports mixed estates and phased upgrades, aiding migration from legacy DVR/NVR environments. This lowers deployment time and customer churn while preserving IDIS core differentiation. As of 2024 ONVIF and standards remain central to cross-vendor compatibility in surveillance deployments.

- FEN + standards: smoother third-party integration

- Supports mixed estates & phased upgrades

- Facilitates legacy DVR/NVR migration

Vertical security stack halves install time (50%), raises uptime, market $79.6B

IDIS vertical stack (cameras, NVR, VMS) enables integrated UX, faster installs and higher uptime; DirectIP can cut installation time up to 50% and lowers TCO. Global video surveillance market ~$79.6B by 2025 (MarketsandMarkets 2024). Offices in SK/UK/US; partners in 100+ countries.

| Metric | Value |

|---|---|

| Install time reduction | Up to 50% |

| Market size 2025 | $79.6B |

| Partner footprint | 100+ countries |

What is included in the product

Provides a concise SWOT framework analyzing IDIS’s strengths, weaknesses, opportunities, and threats, highlighting competitive advantages, operational gaps, market opportunities, and external risks shaping its strategic trajectory.

Provides a concise, ready-to-use IDIS SWOT matrix for fast strategy alignment and stakeholder briefs; editable format enables quick updates to reflect shifting risks and opportunities.

Weaknesses

Proprietary lock-in risk

While DirectIP simplifies deployment, it is often perceived as proprietary compared with open, ONVIF-conformant systems; ONVIF lists 20,000+ conformant products (2024). Many enterprises follow cloud-first approaches—Gartner estimated 80% of organizations would adopt cloud-first strategies by 2025—so ONVIF-first RFPs are common. That preference limits inclusion in RFPs emphasizing vendor diversity and can elongate sales cycles.

Brand visibility gap

Against giants like Hikvision (≈25% global market share in 2023), Dahua (≈12%), Axis (≈6%) and Hanwha (≈6%), IDIS faces lower global brand recall. Limited marketing scale reduces top-of-funnel leads versus these incumbents. End users often default to incumbents with broader mindshare, reflected in channel preference trends. Winning enterprise deals requires extra proof-of-concept effort and extended pilots.

Channel concentration

Heavy dependence on distributor/integrator networks creates sales volatility; IDC reported in 2024 that about 68% of physical security solutions were sold through channel partners, exposing vendors like IDIS to partner-driven demand swings. Misaligned incentives can push lowest-cost alternatives, eroding margin. Limited direct enterprise relationships reduce product feedback loops for roadmap prioritization, while partner enablement and certification complexity add significant overhead.

Hardware margin exposure

IDIS shows hardware margin exposure: revenue remains device-heavy while ASP pressure saw industry hardware prices decline ~5–10% year‑over‑year in 2024, squeezing margins as sensor, memory and SoC costs remain volatile. Without scaled SaaS/recurring streams, recurring revenue trails software-first peers; software-heavy rivals continue to out-invest in R&D, widening capability gaps.

- device-concentration: higher price sensitivity

- component-cost swings: sensors/memory/SoCs

- recurring-rev shortfall vs software peers

- competitors invest more in R&D

Scale of R&D

Keeping pace in AI analytics, cybersecurity and cloud requires sizable investment; IDC reported global spending on AI systems reached 154 billion USD in 2023, pressuring mid-sized vendors. Larger rivals iterate faster on edge AI and VSaaS, widening feature gaps. Fragmented regional compliance (NIS2, varied US state privacy laws) adds workload and roadmap trade-offs risk feature gaps in verticals.

- High R&D capex vs larger rivals

- Slower AI/VSaaS iteration

- Compliance fragmentation burden

- Roadmap trade-offs → vertical gaps

Proprietary vendor lagging vs 20,000+ ONVIF devices; cloud-first shift and AI lag squeeze margins

IDIS faces proprietary perception vs 20,000+ ONVIF products (2024), limiting RFP inclusion amid Gartner's 80% cloud‑first trend (2025). Lower global brand recall vs Hikvision (~25% 2023), Dahua (~12%), Axis/Hanwha (~6% each) increases proof‑of‑concept needs. Channel dependence (68% channel sales, IDC 2024), hardware ASP decline (~5–10% 2024) and lagging AI spend (global AI systems $154B 2023) pressure margins and roadmap speed.

| Metric | Value |

|---|---|

| ONVIF conformant products (2024) | 20,000+ |

| Cloud‑first orgs (Gartner) | 80% by 2025 |

| Top vendor share (Hikvision, 2023) | ≈25% |

| Channel sales (IDC, 2024) | 68% |

| Hardware ASP change (2024) | −5 to −10% |

| Global AI systems spend (2023) | $154B |

What You See Is What You Get

IDIS SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and purchase unlocks the complete, editable version. You’re viewing a live preview of the real file; the full document becomes available after checkout.