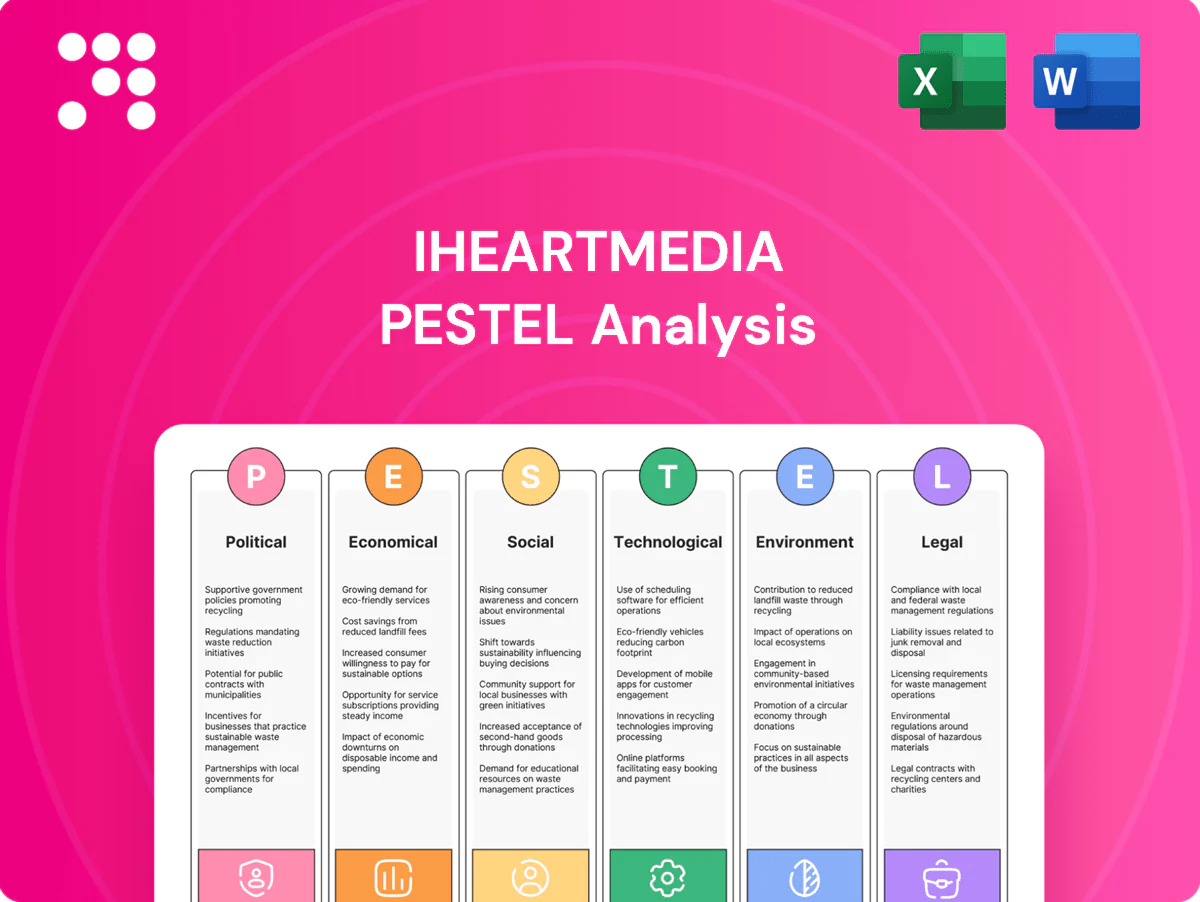

iHeartMedia PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and rapid tech change are reshaping iHeartMedia with our focused PESTLE analysis; three to five actionable insights highlight regulatory risk, audience trends, and digital opportunity. Purchase the full report for the complete breakdown and ready-to-use strategic recommendations.

Political factors

FCC oversight and spectrum policy

FCC sets broadcast licenses, spectrum allocation and ownership limits (e.g., local radio caps: up to 8 stations in markets with 45+ stations, no more than 5 in same service), directly shaping iHeartMedia’s ~860-station footprint and consolidation options. Changes to ownership caps would expand or restrict market-clustering strategies and M&A economics. FCC enforcement, license renewals and the 2017 AM Revitalization initiatives (FM translators for AM relief) materially affect coverage and capital planning.

Political advertising rules and cycles

Election cycles drive high-margin political ad spend—US 2024 outlays were roughly $9–10 billion.

FCC equal-time and lowest unit charge rules plus FEC disclosure and record-keeping apply across broadcast and digital.

Shifts in campaign finance rules can swing demand and pricing, while polarization heightens inventory pressure and brand-safety controls for iHeartMedia.

Net neutrality and broadband policy

Digital audio distribution depends on open, reliable broadband and mobile networks; iHeartMedia reports about 150 million monthly listeners, making network access critical. Reversal of net neutrality (2017 repeal) risks paid prioritization that could raise carriage costs or impair competitive parity. IIJA committed $65 billion for broadband, including BEAD's $42.45 billion to expand rural access (~14% of US), enlarging addressable audience and lowering delivery risk.

Localism and public interest mandates

Stations must serve local communities, shaping programming mix and news obligations; political scrutiny spikes after emergencies or misinformation incidents, drawing FCC and Congressional attention. Enhanced public-file transparency raises compliance workload; iHeartMedia operates over 860 stations in 150+ markets and reaches over 150 million monthly listeners.

- Local service mandates

- Heightened post-crisis scrutiny

- More public-file reporting

- Community engagement aids regulatory reviews

Trade, taxation, and incentives

Changes in state and federal tax policy, including the US federal corporate tax rate of 21%, directly affect iHeartMedia’s after-tax cash flows and capital available for content and station investments; state production incentives (some up to 30% tax credits) can underwrite studio expansions or live events. Tariffs such as 25% Section 232 steel duties and supply-chain constraints raise costs for transmitters/studio equipment, while the 2023 EU-US Data Privacy Framework reshapes cross-border adtech partnerships.

- federal-corporate-tax: 21%

- state-incentives: up to 30% tax credits

- tariffs: up to 25% (steel, Section 232)

- data-framework: EU-US Data Privacy Framework (2023)

Regulation, $9-10B political ads and broadband funding reshape 860 stations, 150M listeners

FCC ownership caps, license renewals and AM revitalization shape iHeartMedia’s ~860‑station footprint and M&A options; regulatory shifts can expand or restrict market clustering. US political ad spend (~$9–10B in 2024) drives high-margin inventory but raises brand‑safety exposure. Broadband funding (IIJA/BEAD $65B/$42.45B) and net‑neutrality policy affect digital reach for ~150M monthly listeners.

| Metric | Value |

|---|---|

| Stations | ~860 |

| Monthly listeners | ~150M |

| 2024 political ad spend | $9–10B |

| Federal tax rate | 21% |

What is included in the product

Explores how macro-environmental forces uniquely affect iHeartMedia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and industry-specific examples. Designed to guide executives and investors in spotting risks, opportunities, and actionable strategic responses.

A clean, visually segmented and editable PESTLE summary of iHeartMedia that can be dropped into presentations, supports quick external risk discussions, and is easily shareable for cross-team alignment.

Economic factors

Advertising cycle sensitivity

iHeartMedia revenue tracks U.S. macro ad spend closely—advertising dips in downturns and typically rebounds with GDP and consumer confidence; industry ad revenues swung roughly 15–25% in past recessions. Key categories—auto, retail, CPG and finance—drive pacing volatility and explain quarter-to-quarter swings. Political and major sports cycles (election years, NFL/CWS seasons) produce periodic uplifts. Growth in podcasting (company reports ~175 million monthly listeners) smooths but does not remove cyclicality.

Interest rates and leverage

Rising Fed policy rates (target 5.25–5.50% at end‑2024) increase iHeartMedia’s debt service, tightening cash available for content and tech investment. Refinancing windows and wider credit spreads materially affect valuation and cost of capital. Strong free cash flow generation and strict cost discipline have partially mitigated this leverage risk. Rating actions influence covenant flexibility and refinancing terms.

Shift to digital and programmatic

Shift to digital/programmatic shifts iHeartMedia margin mix as podcast CPMs run roughly $18–50 for host‑read and $10–20 programmatic, versus streaming CPMs around $5–15 and legacy spot radio lower per-impression costs; fill rates for podcasts/streaming commonly range 60–85%, shaping revenue per impression. Programmatic audio and improved attribution tools (2024 rollouts) can expand mid‑market demand, while active yield management between linear inventory and digital impressions is critical and measurement consistency drives advertiser confidence.

Labor, talent, and content costs

On-air talent, production teams, and salesforces are primary expense lines for iHeartMedia; competition for top podcast creators has pushed guarantees and revenue shares higher amid a U.S. podcast ad market of about $2.1 billion in 2023 (IAB/PwC). Syndication and automation enable scale and lower marginal content costs, while varying royalty and licensing structures materially affect per-hour unit economics across radio and podcast formats.

- Cost drivers: on-air talent, production, sales

- Podcast market: US ad revenue ~2.1B (2023, IAB/PwC)

- Competition: higher guarantees/rev shares for top creators

- Mitigants: syndication, automation

- Margin pressure: royalties/license structures

Automotive and mobility trends

In-car listening remains core to iHeartMedia, with US new-vehicle sales around 15.5 million in 2024, so auto sales cycles and OEM ad budgets materially affect spot and streaming revenue. Connected dashboards and Android Auto/CarPlay proliferation raise competition yet boost iHeartRadio discovery. Shifts from ride-sharing and remote work alter daypart reach, while rising EV share (global ~14% of new sales in 2023, IEA) may reprioritize infotainment integration.

- Auto sales 2024 ~15.5M

- Global EV new-sales share ~14% (2023)

- Connected dashboards ↑ discovery and competition

- Ride-share/commute shifts change daypart reach

Regulation, $9-10B political ads and broadband funding reshape 860 stations, 150M listeners

iHeartMedia revenue remains cyclical with U.S. ad spend and GDP—auto, retail, CPG and finance drive quarter volatility; podcasting (~175M monthly listeners) cushions but does not remove cycles. Higher Fed rates (5.25–5.50% end‑2024) raise debt service and refinancing risk despite strong free cash flow. Digital/programmatic and podcast CPMs boost margin mix but talent guarantees and royalties pressure margins.

| Metric | Value | Year/Source |

|---|---|---|

| Monthly listeners | ~175M | iHeartMedia 2024 |

| US podcast ad rev | $2.1B | 2023 IAB/PwC |

| New vehicle sales (US) | ~15.5M | 2024 |

| Fed funds target | 5.25–5.50% | end‑2024 |

What You See Is What You Get

iHeartMedia PESTLE Analysis

This iHeartMedia PESTLE Analysis provides a concise review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it to inform strategy, valuation and risk assessment immediately upon download.

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and rapid tech change are reshaping iHeartMedia with our focused PESTLE analysis; three to five actionable insights highlight regulatory risk, audience trends, and digital opportunity. Purchase the full report for the complete breakdown and ready-to-use strategic recommendations.

Political factors

FCC oversight and spectrum policy

FCC sets broadcast licenses, spectrum allocation and ownership limits (e.g., local radio caps: up to 8 stations in markets with 45+ stations, no more than 5 in same service), directly shaping iHeartMedia’s ~860-station footprint and consolidation options. Changes to ownership caps would expand or restrict market-clustering strategies and M&A economics. FCC enforcement, license renewals and the 2017 AM Revitalization initiatives (FM translators for AM relief) materially affect coverage and capital planning.

Political advertising rules and cycles

Election cycles drive high-margin political ad spend—US 2024 outlays were roughly $9–10 billion.

FCC equal-time and lowest unit charge rules plus FEC disclosure and record-keeping apply across broadcast and digital.

Shifts in campaign finance rules can swing demand and pricing, while polarization heightens inventory pressure and brand-safety controls for iHeartMedia.

Net neutrality and broadband policy

Digital audio distribution depends on open, reliable broadband and mobile networks; iHeartMedia reports about 150 million monthly listeners, making network access critical. Reversal of net neutrality (2017 repeal) risks paid prioritization that could raise carriage costs or impair competitive parity. IIJA committed $65 billion for broadband, including BEAD's $42.45 billion to expand rural access (~14% of US), enlarging addressable audience and lowering delivery risk.

Localism and public interest mandates

Stations must serve local communities, shaping programming mix and news obligations; political scrutiny spikes after emergencies or misinformation incidents, drawing FCC and Congressional attention. Enhanced public-file transparency raises compliance workload; iHeartMedia operates over 860 stations in 150+ markets and reaches over 150 million monthly listeners.

- Local service mandates

- Heightened post-crisis scrutiny

- More public-file reporting

- Community engagement aids regulatory reviews

Trade, taxation, and incentives

Changes in state and federal tax policy, including the US federal corporate tax rate of 21%, directly affect iHeartMedia’s after-tax cash flows and capital available for content and station investments; state production incentives (some up to 30% tax credits) can underwrite studio expansions or live events. Tariffs such as 25% Section 232 steel duties and supply-chain constraints raise costs for transmitters/studio equipment, while the 2023 EU-US Data Privacy Framework reshapes cross-border adtech partnerships.

- federal-corporate-tax: 21%

- state-incentives: up to 30% tax credits

- tariffs: up to 25% (steel, Section 232)

- data-framework: EU-US Data Privacy Framework (2023)

Regulation, $9-10B political ads and broadband funding reshape 860 stations, 150M listeners

FCC ownership caps, license renewals and AM revitalization shape iHeartMedia’s ~860‑station footprint and M&A options; regulatory shifts can expand or restrict market clustering. US political ad spend (~$9–10B in 2024) drives high-margin inventory but raises brand‑safety exposure. Broadband funding (IIJA/BEAD $65B/$42.45B) and net‑neutrality policy affect digital reach for ~150M monthly listeners.

| Metric | Value |

|---|---|

| Stations | ~860 |

| Monthly listeners | ~150M |

| 2024 political ad spend | $9–10B |

| Federal tax rate | 21% |

What is included in the product

Explores how macro-environmental forces uniquely affect iHeartMedia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and industry-specific examples. Designed to guide executives and investors in spotting risks, opportunities, and actionable strategic responses.

A clean, visually segmented and editable PESTLE summary of iHeartMedia that can be dropped into presentations, supports quick external risk discussions, and is easily shareable for cross-team alignment.

Economic factors

Advertising cycle sensitivity

iHeartMedia revenue tracks U.S. macro ad spend closely—advertising dips in downturns and typically rebounds with GDP and consumer confidence; industry ad revenues swung roughly 15–25% in past recessions. Key categories—auto, retail, CPG and finance—drive pacing volatility and explain quarter-to-quarter swings. Political and major sports cycles (election years, NFL/CWS seasons) produce periodic uplifts. Growth in podcasting (company reports ~175 million monthly listeners) smooths but does not remove cyclicality.

Interest rates and leverage

Rising Fed policy rates (target 5.25–5.50% at end‑2024) increase iHeartMedia’s debt service, tightening cash available for content and tech investment. Refinancing windows and wider credit spreads materially affect valuation and cost of capital. Strong free cash flow generation and strict cost discipline have partially mitigated this leverage risk. Rating actions influence covenant flexibility and refinancing terms.

Shift to digital and programmatic

Shift to digital/programmatic shifts iHeartMedia margin mix as podcast CPMs run roughly $18–50 for host‑read and $10–20 programmatic, versus streaming CPMs around $5–15 and legacy spot radio lower per-impression costs; fill rates for podcasts/streaming commonly range 60–85%, shaping revenue per impression. Programmatic audio and improved attribution tools (2024 rollouts) can expand mid‑market demand, while active yield management between linear inventory and digital impressions is critical and measurement consistency drives advertiser confidence.

Labor, talent, and content costs

On-air talent, production teams, and salesforces are primary expense lines for iHeartMedia; competition for top podcast creators has pushed guarantees and revenue shares higher amid a U.S. podcast ad market of about $2.1 billion in 2023 (IAB/PwC). Syndication and automation enable scale and lower marginal content costs, while varying royalty and licensing structures materially affect per-hour unit economics across radio and podcast formats.

- Cost drivers: on-air talent, production, sales

- Podcast market: US ad revenue ~2.1B (2023, IAB/PwC)

- Competition: higher guarantees/rev shares for top creators

- Mitigants: syndication, automation

- Margin pressure: royalties/license structures

Automotive and mobility trends

In-car listening remains core to iHeartMedia, with US new-vehicle sales around 15.5 million in 2024, so auto sales cycles and OEM ad budgets materially affect spot and streaming revenue. Connected dashboards and Android Auto/CarPlay proliferation raise competition yet boost iHeartRadio discovery. Shifts from ride-sharing and remote work alter daypart reach, while rising EV share (global ~14% of new sales in 2023, IEA) may reprioritize infotainment integration.

- Auto sales 2024 ~15.5M

- Global EV new-sales share ~14% (2023)

- Connected dashboards ↑ discovery and competition

- Ride-share/commute shifts change daypart reach

Regulation, $9-10B political ads and broadband funding reshape 860 stations, 150M listeners

iHeartMedia revenue remains cyclical with U.S. ad spend and GDP—auto, retail, CPG and finance drive quarter volatility; podcasting (~175M monthly listeners) cushions but does not remove cycles. Higher Fed rates (5.25–5.50% end‑2024) raise debt service and refinancing risk despite strong free cash flow. Digital/programmatic and podcast CPMs boost margin mix but talent guarantees and royalties pressure margins.

| Metric | Value | Year/Source |

|---|---|---|

| Monthly listeners | ~175M | iHeartMedia 2024 |

| US podcast ad rev | $2.1B | 2023 IAB/PwC |

| New vehicle sales (US) | ~15.5M | 2024 |

| Fed funds target | 5.25–5.50% | end‑2024 |

What You See Is What You Get

iHeartMedia PESTLE Analysis

This iHeartMedia PESTLE Analysis provides a concise review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it to inform strategy, valuation and risk assessment immediately upon download.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and rapid tech change are reshaping iHeartMedia with our focused PESTLE analysis; three to five actionable insights highlight regulatory risk, audience trends, and digital opportunity. Purchase the full report for the complete breakdown and ready-to-use strategic recommendations.

Political factors

FCC oversight and spectrum policy

FCC sets broadcast licenses, spectrum allocation and ownership limits (e.g., local radio caps: up to 8 stations in markets with 45+ stations, no more than 5 in same service), directly shaping iHeartMedia’s ~860-station footprint and consolidation options. Changes to ownership caps would expand or restrict market-clustering strategies and M&A economics. FCC enforcement, license renewals and the 2017 AM Revitalization initiatives (FM translators for AM relief) materially affect coverage and capital planning.

Political advertising rules and cycles

Election cycles drive high-margin political ad spend—US 2024 outlays were roughly $9–10 billion.

FCC equal-time and lowest unit charge rules plus FEC disclosure and record-keeping apply across broadcast and digital.

Shifts in campaign finance rules can swing demand and pricing, while polarization heightens inventory pressure and brand-safety controls for iHeartMedia.

Net neutrality and broadband policy

Digital audio distribution depends on open, reliable broadband and mobile networks; iHeartMedia reports about 150 million monthly listeners, making network access critical. Reversal of net neutrality (2017 repeal) risks paid prioritization that could raise carriage costs or impair competitive parity. IIJA committed $65 billion for broadband, including BEAD's $42.45 billion to expand rural access (~14% of US), enlarging addressable audience and lowering delivery risk.

Localism and public interest mandates

Stations must serve local communities, shaping programming mix and news obligations; political scrutiny spikes after emergencies or misinformation incidents, drawing FCC and Congressional attention. Enhanced public-file transparency raises compliance workload; iHeartMedia operates over 860 stations in 150+ markets and reaches over 150 million monthly listeners.

- Local service mandates

- Heightened post-crisis scrutiny

- More public-file reporting

- Community engagement aids regulatory reviews

Trade, taxation, and incentives

Changes in state and federal tax policy, including the US federal corporate tax rate of 21%, directly affect iHeartMedia’s after-tax cash flows and capital available for content and station investments; state production incentives (some up to 30% tax credits) can underwrite studio expansions or live events. Tariffs such as 25% Section 232 steel duties and supply-chain constraints raise costs for transmitters/studio equipment, while the 2023 EU-US Data Privacy Framework reshapes cross-border adtech partnerships.

- federal-corporate-tax: 21%

- state-incentives: up to 30% tax credits

- tariffs: up to 25% (steel, Section 232)

- data-framework: EU-US Data Privacy Framework (2023)

Regulation, $9-10B political ads and broadband funding reshape 860 stations, 150M listeners

FCC ownership caps, license renewals and AM revitalization shape iHeartMedia’s ~860‑station footprint and M&A options; regulatory shifts can expand or restrict market clustering. US political ad spend (~$9–10B in 2024) drives high-margin inventory but raises brand‑safety exposure. Broadband funding (IIJA/BEAD $65B/$42.45B) and net‑neutrality policy affect digital reach for ~150M monthly listeners.

| Metric | Value |

|---|---|

| Stations | ~860 |

| Monthly listeners | ~150M |

| 2024 political ad spend | $9–10B |

| Federal tax rate | 21% |

What is included in the product

Explores how macro-environmental forces uniquely affect iHeartMedia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and industry-specific examples. Designed to guide executives and investors in spotting risks, opportunities, and actionable strategic responses.

A clean, visually segmented and editable PESTLE summary of iHeartMedia that can be dropped into presentations, supports quick external risk discussions, and is easily shareable for cross-team alignment.

Economic factors

Advertising cycle sensitivity

iHeartMedia revenue tracks U.S. macro ad spend closely—advertising dips in downturns and typically rebounds with GDP and consumer confidence; industry ad revenues swung roughly 15–25% in past recessions. Key categories—auto, retail, CPG and finance—drive pacing volatility and explain quarter-to-quarter swings. Political and major sports cycles (election years, NFL/CWS seasons) produce periodic uplifts. Growth in podcasting (company reports ~175 million monthly listeners) smooths but does not remove cyclicality.

Interest rates and leverage

Rising Fed policy rates (target 5.25–5.50% at end‑2024) increase iHeartMedia’s debt service, tightening cash available for content and tech investment. Refinancing windows and wider credit spreads materially affect valuation and cost of capital. Strong free cash flow generation and strict cost discipline have partially mitigated this leverage risk. Rating actions influence covenant flexibility and refinancing terms.

Shift to digital and programmatic

Shift to digital/programmatic shifts iHeartMedia margin mix as podcast CPMs run roughly $18–50 for host‑read and $10–20 programmatic, versus streaming CPMs around $5–15 and legacy spot radio lower per-impression costs; fill rates for podcasts/streaming commonly range 60–85%, shaping revenue per impression. Programmatic audio and improved attribution tools (2024 rollouts) can expand mid‑market demand, while active yield management between linear inventory and digital impressions is critical and measurement consistency drives advertiser confidence.

Labor, talent, and content costs

On-air talent, production teams, and salesforces are primary expense lines for iHeartMedia; competition for top podcast creators has pushed guarantees and revenue shares higher amid a U.S. podcast ad market of about $2.1 billion in 2023 (IAB/PwC). Syndication and automation enable scale and lower marginal content costs, while varying royalty and licensing structures materially affect per-hour unit economics across radio and podcast formats.

- Cost drivers: on-air talent, production, sales

- Podcast market: US ad revenue ~2.1B (2023, IAB/PwC)

- Competition: higher guarantees/rev shares for top creators

- Mitigants: syndication, automation

- Margin pressure: royalties/license structures

Automotive and mobility trends

In-car listening remains core to iHeartMedia, with US new-vehicle sales around 15.5 million in 2024, so auto sales cycles and OEM ad budgets materially affect spot and streaming revenue. Connected dashboards and Android Auto/CarPlay proliferation raise competition yet boost iHeartRadio discovery. Shifts from ride-sharing and remote work alter daypart reach, while rising EV share (global ~14% of new sales in 2023, IEA) may reprioritize infotainment integration.

- Auto sales 2024 ~15.5M

- Global EV new-sales share ~14% (2023)

- Connected dashboards ↑ discovery and competition

- Ride-share/commute shifts change daypart reach

Regulation, $9-10B political ads and broadband funding reshape 860 stations, 150M listeners

iHeartMedia revenue remains cyclical with U.S. ad spend and GDP—auto, retail, CPG and finance drive quarter volatility; podcasting (~175M monthly listeners) cushions but does not remove cycles. Higher Fed rates (5.25–5.50% end‑2024) raise debt service and refinancing risk despite strong free cash flow. Digital/programmatic and podcast CPMs boost margin mix but talent guarantees and royalties pressure margins.

| Metric | Value | Year/Source |

|---|---|---|

| Monthly listeners | ~175M | iHeartMedia 2024 |

| US podcast ad rev | $2.1B | 2023 IAB/PwC |

| New vehicle sales (US) | ~15.5M | 2024 |

| Fed funds target | 5.25–5.50% | end‑2024 |

What You See Is What You Get

iHeartMedia PESTLE Analysis

This iHeartMedia PESTLE Analysis provides a concise review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it to inform strategy, valuation and risk assessment immediately upon download.