IIFL Finance Porter's Five Forces Analysis

From Overview to Strategy Blueprint

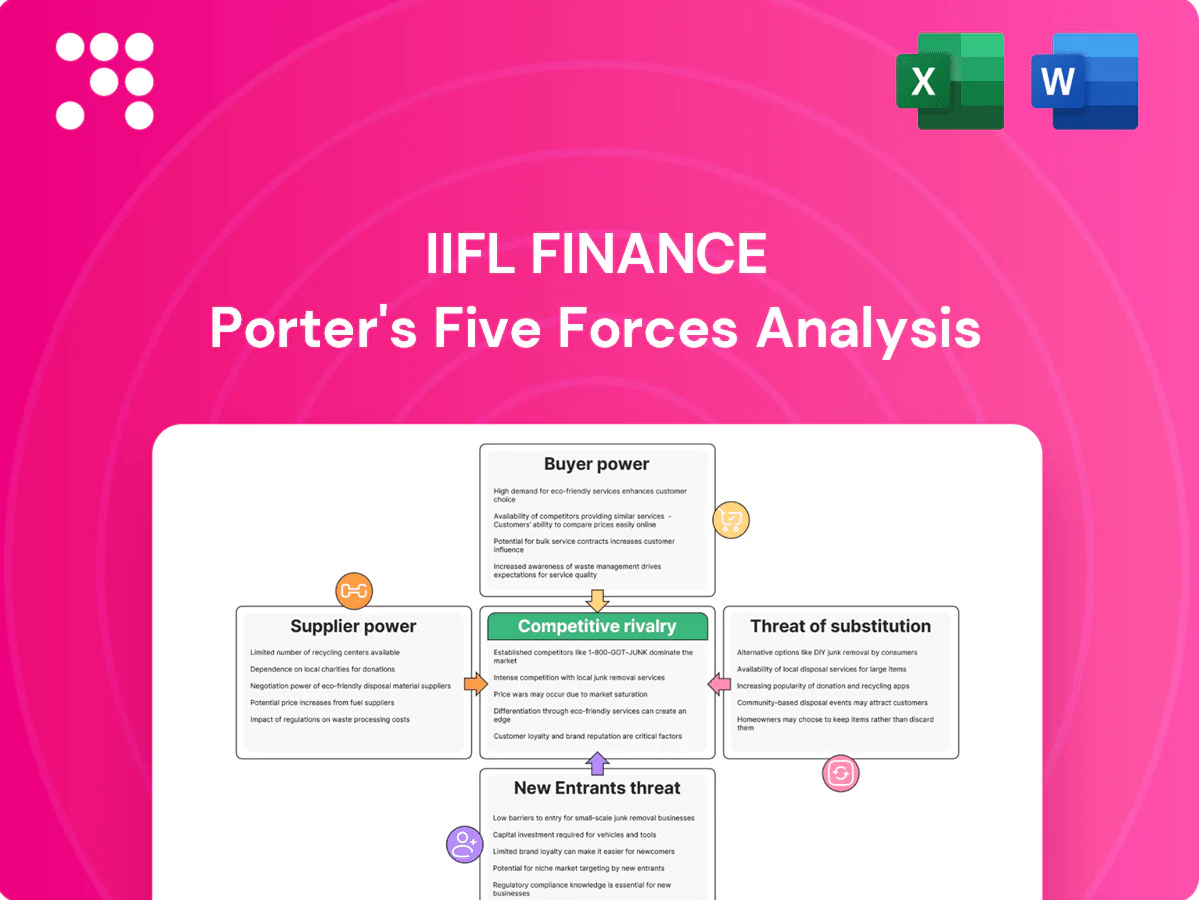

IIFL Finance faces moderate buyer power and rising competitive pressure from NBFCs and fintechs, while regulatory shifts and lender dependencies shape its margin dynamics; this snapshot highlights key risks and opportunities. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Diverse funding sources concentration

IIFL funds operations through banks, bond markets, securitisation and NBFC lines, and when a few large lenders dominate they can impose tighter covenants and higher spreads; diversifying maturities and broadening the investor base has reduced dependence and improved pricing. Periods of tight liquidity, such as the 2023–24 stress episodes, amplified supplier leverage and raised short-term funding costs materially.

Interest rate cycle sensitivity

Cost of funds for IIFL moves with RBI policy and credit spreads—with the repo around 6.5% and 10-year G‑Sec near 7.3% in 2024, borrowing costs rose materially. Rising rates strengthen supplier power as refinancing becomes costlier and windows narrow, squeezing margins and capital access. Hedging and issuance of fixed‑rate liabilities reduce but do not eliminate exposure. Competitive pressure limits the ability to pass higher funding costs fully to borrowers.

Regulatory and rating influence

Credit ratings and RBI norms directly shape IIFL Finance’s access and cost of wholesale funding, with rating downgrades often translating into spread widening of up to several hundred basis points for NBFCs. Stricter provisioning or regulatory actions in 2023–24 amplified suppliers’ bargaining power by increasing funding costs and reducing short-term liquidity buffers. Strong governance, robust asset quality and a CET1/CRAR buffer support continued market access. Transparent disclosures broaden the investor pool and lower risk premia.

Technology and data vendors

Core lending platforms, analytics engines and credit bureau data (CIBIL, CRIF, Equifax) are critical inputs for IIFL, giving vendors leverage via switching costs and integration complexity; multi-vendor sourcing and growing in‑house capabilities reduce dependency, while vendor SLAs (commonly 99.9% uptime) and interoperability standards strengthen IIFL’s negotiating position.

- Critical inputs: lending platforms, analytics, bureaus

- Vendor power: switching costs, integration

- Mitigants: multi-vendor, in-house

- Levers: SLAs (99.9%), interoperability

Distribution partners and DSAs

Direct selling agents and fintech originators drove significant lead flow for IIFL, contributing about 40% of sourced loans in FY2024, allowing top partners to command premium payouts tied to conversion rates.

Building owned branches and digital funnels has reduced reliance on external suppliers, with branch expansion and online sourcing lowering variable acquisition costs.

Performance-linked contracts and tiered commissions align incentives and cap supplier bargaining power while preserving volume from high-performers.

- DSA/fintech share: ~40% (FY2024)

- Owned channels: lower acquisition cost

- Contracts: performance-linked, tiered payouts

Funding spreads: repo 6.5%, 10y 7.3%, DSAs 40%

IIFL faces moderate supplier power: wholesale lenders and rating sensitivity drive funding spreads (repo ~6.5% and 10y G‑Sec ~7.3% in 2024), making refinancing costly in tight markets. DSAs/fintech provided ~40% of originations in FY2024, giving top partners pricing leverage. Vendor switching costs and 99.9% SLA expectations increase dependency; diversification and in‑house buildout mitigate risks.

| Metric | 2024 |

|---|---|

| Repo rate | ~6.5% |

| 10y G‑Sec | ~7.3% |

| DSA/fintech share | ~40% (FY2024) |

| Vendor SLA | 99.9% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to IIFL Finance, evaluating supplier and buyer power, substitutes, and rival intensity to highlight pricing and profitability pressures.

A concise one-sheet Porter's Five Forces for IIFL Finance that pinpoints competitive pressures to relieve decision-making pain—ready to drop into decks, customize with your data, compare scenarios, and use without macros.

Customers Bargaining Power

Price sensitivity and comparison

Loan products are highly price-competitive and easily compared online, with over 50% of urban borrowers in 2024 using comparison tools to shortlist lenders. Customers routinely negotiate rates, fees and turnaround time across NBFCs and banks, elevating buyer power in cities. Transparent marketplaces and rating platforms amplify this effect, while tailored bundles and faster disbursals (same‑day vs 3–7 days) help IIFL retain customers.

Switching costs by product

Gold loans exhibit low switching costs—tenors are typically 3–12 months in 2024 and closures are simple, driving higher churn risk. Home loans carry higher switching costs from refinancing fees (commonly 0.25–0.5%) and extensive documentation, reducing elasticity. Business and microfinance borrower switching varies with formalization and collateral; informal microloans show higher churn. Step-down rate schedules (eg, 25–50 bps over time) are used to curb churn.

Service speed and convenience

Service speed and convenience drive customer bargaining: turnaround times (TAT) and doorstep service plus digital KYC now weigh as heavily as rate in negotiations, with IIFL Finance reporting faster digital onboarding in 2024 and AUM near Rs 55,000 crore, strengthening its positioning. Buyers leverage written service promises to extract fee or rate concessions, while strong omnichannel processes blunt buyer power by delivering superior experience. Missed SLAs rapidly trigger switching in competitive retail lending markets.

Credit access alternatives

Prime customers face strong bargaining power as banks and an estimated 75 million credit cards in India by 2024 give them alternative credit channels, while new-to-credit and rural borrowers—with roughly 40% formal credit penetration in many rural districts in 2024—have limited leverage; growing formalization will raise buyer power, making responsible pricing key to long-term retention.

- Prime alternatives: banks, ~75m credit cards (2024)

- Rural/new-to-credit: ~40% formal penetration (2024)

- Trend: formalization → rising buyer power

- Action: responsible pricing for retention

Collateral-driven negotiations

High-LTV collateral (gold often up to 75% LTV) strengthens borrower confidence to negotiate pricing and tenure, shifting bargaining power toward customers; IIFL can offer sharper rates to lower-risk, high-collateral profiles while protecting margin via haircuts and tenor limits. Dynamic risk-based pricing links quoted rates to credit metrics and LTV bands, and transparent collateral policies reduce disputes and collection costs.

- High-LTV up to 75% reinforces borrower leverage

- Lower-risk profiles justify tighter IIFL pricing

- Risk-based pricing ties rate to LTV/score

- Clear collateral rules cut disputes and recovery time

Customers' pricing power: >50% compare rates; speed drives retention

Customers wield strong bargaining power in urban lending—>50% use comparison tools in 2024 and prime borrowers have 75m card alternatives, forcing rate and fee negotiation; IIFL’s faster digital onboarding and AUM ~Rs 55,000 crore mitigate this. Gold loans (LTV up to 75%) and short tenors increase churn risk; rural/formal penetration ~40% limits leverage but is rising. Service speed (same‑day vs 3–7 days) and risk‑based pricing are key retention levers.

| Metric | 2024 Value |

|---|---|

| Urban comparison tool use | >50% |

| IIFL AUM | ~Rs 55,000 crore |

| Credit cards (India) | ~75 million |

| Rural formal credit penetration | ~40% |

| Gold loan LTV | Up to 75% |

Full Version Awaits

IIFL Finance Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of IIFL Finance you'll receive after purchase—no placeholders or mockups. The document is professionally formatted, comprehensive, and ready for immediate download and use. Once you buy, you’ll get instant access to this same complete file.

From Overview to Strategy Blueprint

IIFL Finance faces moderate buyer power and rising competitive pressure from NBFCs and fintechs, while regulatory shifts and lender dependencies shape its margin dynamics; this snapshot highlights key risks and opportunities. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Diverse funding sources concentration

IIFL funds operations through banks, bond markets, securitisation and NBFC lines, and when a few large lenders dominate they can impose tighter covenants and higher spreads; diversifying maturities and broadening the investor base has reduced dependence and improved pricing. Periods of tight liquidity, such as the 2023–24 stress episodes, amplified supplier leverage and raised short-term funding costs materially.

Interest rate cycle sensitivity

Cost of funds for IIFL moves with RBI policy and credit spreads—with the repo around 6.5% and 10-year G‑Sec near 7.3% in 2024, borrowing costs rose materially. Rising rates strengthen supplier power as refinancing becomes costlier and windows narrow, squeezing margins and capital access. Hedging and issuance of fixed‑rate liabilities reduce but do not eliminate exposure. Competitive pressure limits the ability to pass higher funding costs fully to borrowers.

Regulatory and rating influence

Credit ratings and RBI norms directly shape IIFL Finance’s access and cost of wholesale funding, with rating downgrades often translating into spread widening of up to several hundred basis points for NBFCs. Stricter provisioning or regulatory actions in 2023–24 amplified suppliers’ bargaining power by increasing funding costs and reducing short-term liquidity buffers. Strong governance, robust asset quality and a CET1/CRAR buffer support continued market access. Transparent disclosures broaden the investor pool and lower risk premia.

Technology and data vendors

Core lending platforms, analytics engines and credit bureau data (CIBIL, CRIF, Equifax) are critical inputs for IIFL, giving vendors leverage via switching costs and integration complexity; multi-vendor sourcing and growing in‑house capabilities reduce dependency, while vendor SLAs (commonly 99.9% uptime) and interoperability standards strengthen IIFL’s negotiating position.

- Critical inputs: lending platforms, analytics, bureaus

- Vendor power: switching costs, integration

- Mitigants: multi-vendor, in-house

- Levers: SLAs (99.9%), interoperability

Distribution partners and DSAs

Direct selling agents and fintech originators drove significant lead flow for IIFL, contributing about 40% of sourced loans in FY2024, allowing top partners to command premium payouts tied to conversion rates.

Building owned branches and digital funnels has reduced reliance on external suppliers, with branch expansion and online sourcing lowering variable acquisition costs.

Performance-linked contracts and tiered commissions align incentives and cap supplier bargaining power while preserving volume from high-performers.

- DSA/fintech share: ~40% (FY2024)

- Owned channels: lower acquisition cost

- Contracts: performance-linked, tiered payouts

Funding spreads: repo 6.5%, 10y 7.3%, DSAs 40%

IIFL faces moderate supplier power: wholesale lenders and rating sensitivity drive funding spreads (repo ~6.5% and 10y G‑Sec ~7.3% in 2024), making refinancing costly in tight markets. DSAs/fintech provided ~40% of originations in FY2024, giving top partners pricing leverage. Vendor switching costs and 99.9% SLA expectations increase dependency; diversification and in‑house buildout mitigate risks.

| Metric | 2024 |

|---|---|

| Repo rate | ~6.5% |

| 10y G‑Sec | ~7.3% |

| DSA/fintech share | ~40% (FY2024) |

| Vendor SLA | 99.9% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to IIFL Finance, evaluating supplier and buyer power, substitutes, and rival intensity to highlight pricing and profitability pressures.

A concise one-sheet Porter's Five Forces for IIFL Finance that pinpoints competitive pressures to relieve decision-making pain—ready to drop into decks, customize with your data, compare scenarios, and use without macros.

Customers Bargaining Power

Price sensitivity and comparison

Loan products are highly price-competitive and easily compared online, with over 50% of urban borrowers in 2024 using comparison tools to shortlist lenders. Customers routinely negotiate rates, fees and turnaround time across NBFCs and banks, elevating buyer power in cities. Transparent marketplaces and rating platforms amplify this effect, while tailored bundles and faster disbursals (same‑day vs 3–7 days) help IIFL retain customers.

Switching costs by product

Gold loans exhibit low switching costs—tenors are typically 3–12 months in 2024 and closures are simple, driving higher churn risk. Home loans carry higher switching costs from refinancing fees (commonly 0.25–0.5%) and extensive documentation, reducing elasticity. Business and microfinance borrower switching varies with formalization and collateral; informal microloans show higher churn. Step-down rate schedules (eg, 25–50 bps over time) are used to curb churn.

Service speed and convenience

Service speed and convenience drive customer bargaining: turnaround times (TAT) and doorstep service plus digital KYC now weigh as heavily as rate in negotiations, with IIFL Finance reporting faster digital onboarding in 2024 and AUM near Rs 55,000 crore, strengthening its positioning. Buyers leverage written service promises to extract fee or rate concessions, while strong omnichannel processes blunt buyer power by delivering superior experience. Missed SLAs rapidly trigger switching in competitive retail lending markets.

Credit access alternatives

Prime customers face strong bargaining power as banks and an estimated 75 million credit cards in India by 2024 give them alternative credit channels, while new-to-credit and rural borrowers—with roughly 40% formal credit penetration in many rural districts in 2024—have limited leverage; growing formalization will raise buyer power, making responsible pricing key to long-term retention.

- Prime alternatives: banks, ~75m credit cards (2024)

- Rural/new-to-credit: ~40% formal penetration (2024)

- Trend: formalization → rising buyer power

- Action: responsible pricing for retention

Collateral-driven negotiations

High-LTV collateral (gold often up to 75% LTV) strengthens borrower confidence to negotiate pricing and tenure, shifting bargaining power toward customers; IIFL can offer sharper rates to lower-risk, high-collateral profiles while protecting margin via haircuts and tenor limits. Dynamic risk-based pricing links quoted rates to credit metrics and LTV bands, and transparent collateral policies reduce disputes and collection costs.

- High-LTV up to 75% reinforces borrower leverage

- Lower-risk profiles justify tighter IIFL pricing

- Risk-based pricing ties rate to LTV/score

- Clear collateral rules cut disputes and recovery time

Customers' pricing power: >50% compare rates; speed drives retention

Customers wield strong bargaining power in urban lending—>50% use comparison tools in 2024 and prime borrowers have 75m card alternatives, forcing rate and fee negotiation; IIFL’s faster digital onboarding and AUM ~Rs 55,000 crore mitigate this. Gold loans (LTV up to 75%) and short tenors increase churn risk; rural/formal penetration ~40% limits leverage but is rising. Service speed (same‑day vs 3–7 days) and risk‑based pricing are key retention levers.

| Metric | 2024 Value |

|---|---|

| Urban comparison tool use | >50% |

| IIFL AUM | ~Rs 55,000 crore |

| Credit cards (India) | ~75 million |

| Rural formal credit penetration | ~40% |

| Gold loan LTV | Up to 75% |

Full Version Awaits

IIFL Finance Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of IIFL Finance you'll receive after purchase—no placeholders or mockups. The document is professionally formatted, comprehensive, and ready for immediate download and use. Once you buy, you’ll get instant access to this same complete file.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

IIFL Finance faces moderate buyer power and rising competitive pressure from NBFCs and fintechs, while regulatory shifts and lender dependencies shape its margin dynamics; this snapshot highlights key risks and opportunities. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Diverse funding sources concentration

IIFL funds operations through banks, bond markets, securitisation and NBFC lines, and when a few large lenders dominate they can impose tighter covenants and higher spreads; diversifying maturities and broadening the investor base has reduced dependence and improved pricing. Periods of tight liquidity, such as the 2023–24 stress episodes, amplified supplier leverage and raised short-term funding costs materially.

Interest rate cycle sensitivity

Cost of funds for IIFL moves with RBI policy and credit spreads—with the repo around 6.5% and 10-year G‑Sec near 7.3% in 2024, borrowing costs rose materially. Rising rates strengthen supplier power as refinancing becomes costlier and windows narrow, squeezing margins and capital access. Hedging and issuance of fixed‑rate liabilities reduce but do not eliminate exposure. Competitive pressure limits the ability to pass higher funding costs fully to borrowers.

Regulatory and rating influence

Credit ratings and RBI norms directly shape IIFL Finance’s access and cost of wholesale funding, with rating downgrades often translating into spread widening of up to several hundred basis points for NBFCs. Stricter provisioning or regulatory actions in 2023–24 amplified suppliers’ bargaining power by increasing funding costs and reducing short-term liquidity buffers. Strong governance, robust asset quality and a CET1/CRAR buffer support continued market access. Transparent disclosures broaden the investor pool and lower risk premia.

Technology and data vendors

Core lending platforms, analytics engines and credit bureau data (CIBIL, CRIF, Equifax) are critical inputs for IIFL, giving vendors leverage via switching costs and integration complexity; multi-vendor sourcing and growing in‑house capabilities reduce dependency, while vendor SLAs (commonly 99.9% uptime) and interoperability standards strengthen IIFL’s negotiating position.

- Critical inputs: lending platforms, analytics, bureaus

- Vendor power: switching costs, integration

- Mitigants: multi-vendor, in-house

- Levers: SLAs (99.9%), interoperability

Distribution partners and DSAs

Direct selling agents and fintech originators drove significant lead flow for IIFL, contributing about 40% of sourced loans in FY2024, allowing top partners to command premium payouts tied to conversion rates.

Building owned branches and digital funnels has reduced reliance on external suppliers, with branch expansion and online sourcing lowering variable acquisition costs.

Performance-linked contracts and tiered commissions align incentives and cap supplier bargaining power while preserving volume from high-performers.

- DSA/fintech share: ~40% (FY2024)

- Owned channels: lower acquisition cost

- Contracts: performance-linked, tiered payouts

Funding spreads: repo 6.5%, 10y 7.3%, DSAs 40%

IIFL faces moderate supplier power: wholesale lenders and rating sensitivity drive funding spreads (repo ~6.5% and 10y G‑Sec ~7.3% in 2024), making refinancing costly in tight markets. DSAs/fintech provided ~40% of originations in FY2024, giving top partners pricing leverage. Vendor switching costs and 99.9% SLA expectations increase dependency; diversification and in‑house buildout mitigate risks.

| Metric | 2024 |

|---|---|

| Repo rate | ~6.5% |

| 10y G‑Sec | ~7.3% |

| DSA/fintech share | ~40% (FY2024) |

| Vendor SLA | 99.9% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to IIFL Finance, evaluating supplier and buyer power, substitutes, and rival intensity to highlight pricing and profitability pressures.

A concise one-sheet Porter's Five Forces for IIFL Finance that pinpoints competitive pressures to relieve decision-making pain—ready to drop into decks, customize with your data, compare scenarios, and use without macros.

Customers Bargaining Power

Price sensitivity and comparison

Loan products are highly price-competitive and easily compared online, with over 50% of urban borrowers in 2024 using comparison tools to shortlist lenders. Customers routinely negotiate rates, fees and turnaround time across NBFCs and banks, elevating buyer power in cities. Transparent marketplaces and rating platforms amplify this effect, while tailored bundles and faster disbursals (same‑day vs 3–7 days) help IIFL retain customers.

Switching costs by product

Gold loans exhibit low switching costs—tenors are typically 3–12 months in 2024 and closures are simple, driving higher churn risk. Home loans carry higher switching costs from refinancing fees (commonly 0.25–0.5%) and extensive documentation, reducing elasticity. Business and microfinance borrower switching varies with formalization and collateral; informal microloans show higher churn. Step-down rate schedules (eg, 25–50 bps over time) are used to curb churn.

Service speed and convenience

Service speed and convenience drive customer bargaining: turnaround times (TAT) and doorstep service plus digital KYC now weigh as heavily as rate in negotiations, with IIFL Finance reporting faster digital onboarding in 2024 and AUM near Rs 55,000 crore, strengthening its positioning. Buyers leverage written service promises to extract fee or rate concessions, while strong omnichannel processes blunt buyer power by delivering superior experience. Missed SLAs rapidly trigger switching in competitive retail lending markets.

Credit access alternatives

Prime customers face strong bargaining power as banks and an estimated 75 million credit cards in India by 2024 give them alternative credit channels, while new-to-credit and rural borrowers—with roughly 40% formal credit penetration in many rural districts in 2024—have limited leverage; growing formalization will raise buyer power, making responsible pricing key to long-term retention.

- Prime alternatives: banks, ~75m credit cards (2024)

- Rural/new-to-credit: ~40% formal penetration (2024)

- Trend: formalization → rising buyer power

- Action: responsible pricing for retention

Collateral-driven negotiations

High-LTV collateral (gold often up to 75% LTV) strengthens borrower confidence to negotiate pricing and tenure, shifting bargaining power toward customers; IIFL can offer sharper rates to lower-risk, high-collateral profiles while protecting margin via haircuts and tenor limits. Dynamic risk-based pricing links quoted rates to credit metrics and LTV bands, and transparent collateral policies reduce disputes and collection costs.

- High-LTV up to 75% reinforces borrower leverage

- Lower-risk profiles justify tighter IIFL pricing

- Risk-based pricing ties rate to LTV/score

- Clear collateral rules cut disputes and recovery time

Customers' pricing power: >50% compare rates; speed drives retention

Customers wield strong bargaining power in urban lending—>50% use comparison tools in 2024 and prime borrowers have 75m card alternatives, forcing rate and fee negotiation; IIFL’s faster digital onboarding and AUM ~Rs 55,000 crore mitigate this. Gold loans (LTV up to 75%) and short tenors increase churn risk; rural/formal penetration ~40% limits leverage but is rising. Service speed (same‑day vs 3–7 days) and risk‑based pricing are key retention levers.

| Metric | 2024 Value |

|---|---|

| Urban comparison tool use | >50% |

| IIFL AUM | ~Rs 55,000 crore |

| Credit cards (India) | ~75 million |

| Rural formal credit penetration | ~40% |

| Gold loan LTV | Up to 75% |

Full Version Awaits

IIFL Finance Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of IIFL Finance you'll receive after purchase—no placeholders or mockups. The document is professionally formatted, comprehensive, and ready for immediate download and use. Once you buy, you’ll get instant access to this same complete file.