Iluka Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

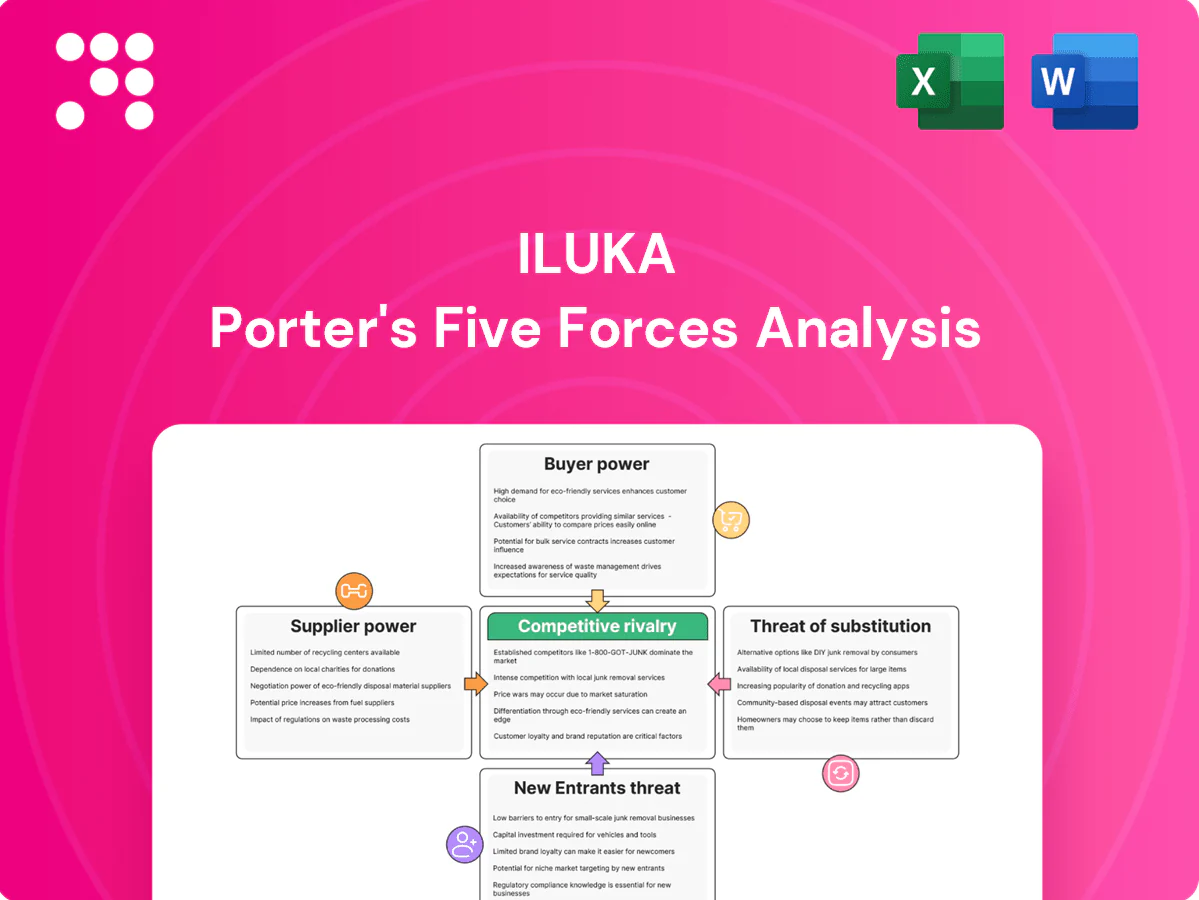

Iluka’s Porter's Five Forces snapshot highlights competitive intensity from miners, shifting buyer power, and substitution risks tied to alternative minerals and recycling; regulatory and capital barriers further shape strategic choices. This brief overview teases key pressure points and growth levers for Iluka’s zircon and titanium dioxide businesses. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Iluka’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Reagents, consumables and specialized equipment for mineral sands processing are sourced from a limited set of global suppliers, so outages of chlorinators, caustic or specialty parts can force higher costs or plant downtime; this supplier concentration raises switching costs and gives vendors pricing leverage, while long-term framework agreements reduce but do not eliminate that risk.

Energy and fuel dependency

Iluka’s operations are energy-intensive, relying on electricity, gas and diesel for mining and upgrading, including synthetic rutile kilns. Volatile energy prices and constrained regional grids compress margins and raise supplier leverage. Remote sites have limited interchangeable energy sources, increasing exposure to supplier power. Hedging programs and on-site efficiency projects partially mitigate that reliance.

Skilled labor and contractors

Geologists, metallurgists and mine contractors are scarce in key mining regions, with around 60% of operators in 2024 reporting critical skills shortages; tight regional labor markets and stricter safety compliance have driven mining services wage inflation and higher contractor rates. Project ramp-ups often coincide with regional booms, intensifying bidding pressure on staff and equipment. Training pipelines and multi-year service contracts (typically 3–7 years) mitigate but do not eliminate this supplier power.

Land, water, and permits

Access to leases, water rights and environmental permits functions as a quasi-supplier constraint for Iluka: in 2024 Iluka held about 2.1 million hectares of tenements, while project approvals in Australia commonly add 1–3 years to timelines, increasing carrying costs and reducing flexibility. Government agencies and communities can impose conditions, royalties or stricter standards that raise operating costs; delays strengthen external negotiating power and can erode project NPV. Early stakeholder engagement smooths approvals but increases pre-production lead time and up-front expenditure.

- Leases: ~2.1m ha tenements (2024)

- Approval delays: 12–36 months

- Impact: higher capex, longer lead times

- Mitigation: early stakeholder engagement

Logistics and ports

Vendors gain pricing leverage as supply, energy and logistics concentrate; top-3 ~60%, skills ~60%

Supplier concentration in reagents, energy and logistics gives vendors pricing leverage; 2024 saw top-3 carriers control ~60% capacity and global skills shortages hit ~60% of operators. Energy price volatility and remote-site dependencies raise switching costs and downtime risk. Long-term contracts, hedging and multi-port/contractor agreements partially mitigate but do not eliminate supplier power.

| Metric | 2024 |

|---|---|

| Tenements | ~2.1m ha |

| Top-3 carriers | ~60% capacity |

| Skills shortage | ~60% operators |

What is included in the product

Tailored Porter's Five Forces analysis for Iluka that uncovers competitive drivers, supplier and buyer bargaining power, threats from substitutes and new entrants, and industry rivalry; includes strategic implications and emerging risks to Iluka's pricing and profitability.

Compact one-sheet Porter's Five Forces for Iluka—clarifies supplier, buyer, substitute, entrant, and rivalry pressures for quick strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Buyer concentration

Major TiO2 pigment producers and large ceramics manufacturers handle outsized volumes in a roughly 6 million tonne global TiO2 market (2024), giving buyers strong negotiating leverage. Consolidation—top five producers supplying over half capacity—intensifies pressure. Iluka mitigates this via consistent product quality, supply reliability and optionality across zircon and high‑grade TiO2 feedstocks.

Price sensitivity and cycles

End-use demand for Iluka's products tracks construction, automotive and consumer durables cycles, with 2024 weakness in automotive production and housing activity pushing buyers to demand discounts. Buyers press for concessions in downturns and resist increases when markets are soft; spot exposure can drive intra-year price swings of 15–25%. Multi-year contracts and index-linked formulas (common in heavy-minerals offtakes) help balance producer and buyer interests.

Product qualification stickiness

Pigment and ceramics lines demand rigorous feedstock qualification, often taking 6–18 months, which raises switching costs and can lock in supply once approved. That stickiness enables suppliers to command premiums for consistent chemistry and low impurities. Buyers frequently dual-source after qualification to preserve leverage and mitigate supply risk. Strong impurity control supports sustained pricing power in 2024 markets.

Backward integration options

Some pigment players such as Tronox (which merged with Cristal in 2019) are vertically integrated into mineral sands, reducing reliance on external ilmenite/rutile suppliers; integration is used as a bargaining lever even when external purchases continue. Iluka must differentiate on reliability and value-in-use, not only price, while strategic offtakes and partnerships align incentives across the value chain in 2024.

- Integrated players: Tronox (integrated since 2019)

- Bargaining lever: integration + external buying

- Iluka focus: reliability, value-in-use

- Alignment: strategic offtake and partnerships

Substitutability within feedstocks

Buyers can blend natural rutile, synthetic rutile and chloride slag for TiO2 and partially substitute zircon in some ceramics, giving purchasers leverage in negotiations; however process and quality constraints prevent full substitution without yield or performance penalties. Iluka preserves pricing and share through technical support, tailored specifications and supply reliability.

Buyers hold leverage as top-5 supply >50% of ~6Mt TiO2; spot swings 15-25%

Buyers hold strong leverage in the ~6 Mt TiO2 market (2024); top five producers supply >50% of capacity, amplifying bargaining power. 2024 autos/housing weakness drives discounting and spot volatility of 15–25% intra‑year. Long 6–18 month feedstock qualification and limited zircon substitution support Iluka premiums via quality, reliability and technical service.

| Metric | 2024 Value |

|---|---|

| Global TiO2 market | ~6,000,000 t |

| Top‑5 producer share | >50% |

| Spot price volatility | 15–25% |

| Feedstock qualification | 6–18 months |

Full Version Awaits

Iluka Porter's Five Forces Analysis

This preview shows the exact Iluka Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Iluka’s Porter's Five Forces snapshot highlights competitive intensity from miners, shifting buyer power, and substitution risks tied to alternative minerals and recycling; regulatory and capital barriers further shape strategic choices. This brief overview teases key pressure points and growth levers for Iluka’s zircon and titanium dioxide businesses. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Iluka’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Reagents, consumables and specialized equipment for mineral sands processing are sourced from a limited set of global suppliers, so outages of chlorinators, caustic or specialty parts can force higher costs or plant downtime; this supplier concentration raises switching costs and gives vendors pricing leverage, while long-term framework agreements reduce but do not eliminate that risk.

Energy and fuel dependency

Iluka’s operations are energy-intensive, relying on electricity, gas and diesel for mining and upgrading, including synthetic rutile kilns. Volatile energy prices and constrained regional grids compress margins and raise supplier leverage. Remote sites have limited interchangeable energy sources, increasing exposure to supplier power. Hedging programs and on-site efficiency projects partially mitigate that reliance.

Skilled labor and contractors

Geologists, metallurgists and mine contractors are scarce in key mining regions, with around 60% of operators in 2024 reporting critical skills shortages; tight regional labor markets and stricter safety compliance have driven mining services wage inflation and higher contractor rates. Project ramp-ups often coincide with regional booms, intensifying bidding pressure on staff and equipment. Training pipelines and multi-year service contracts (typically 3–7 years) mitigate but do not eliminate this supplier power.

Land, water, and permits

Access to leases, water rights and environmental permits functions as a quasi-supplier constraint for Iluka: in 2024 Iluka held about 2.1 million hectares of tenements, while project approvals in Australia commonly add 1–3 years to timelines, increasing carrying costs and reducing flexibility. Government agencies and communities can impose conditions, royalties or stricter standards that raise operating costs; delays strengthen external negotiating power and can erode project NPV. Early stakeholder engagement smooths approvals but increases pre-production lead time and up-front expenditure.

- Leases: ~2.1m ha tenements (2024)

- Approval delays: 12–36 months

- Impact: higher capex, longer lead times

- Mitigation: early stakeholder engagement

Logistics and ports

Vendors gain pricing leverage as supply, energy and logistics concentrate; top-3 ~60%, skills ~60%

Supplier concentration in reagents, energy and logistics gives vendors pricing leverage; 2024 saw top-3 carriers control ~60% capacity and global skills shortages hit ~60% of operators. Energy price volatility and remote-site dependencies raise switching costs and downtime risk. Long-term contracts, hedging and multi-port/contractor agreements partially mitigate but do not eliminate supplier power.

| Metric | 2024 |

|---|---|

| Tenements | ~2.1m ha |

| Top-3 carriers | ~60% capacity |

| Skills shortage | ~60% operators |

What is included in the product

Tailored Porter's Five Forces analysis for Iluka that uncovers competitive drivers, supplier and buyer bargaining power, threats from substitutes and new entrants, and industry rivalry; includes strategic implications and emerging risks to Iluka's pricing and profitability.

Compact one-sheet Porter's Five Forces for Iluka—clarifies supplier, buyer, substitute, entrant, and rivalry pressures for quick strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Buyer concentration

Major TiO2 pigment producers and large ceramics manufacturers handle outsized volumes in a roughly 6 million tonne global TiO2 market (2024), giving buyers strong negotiating leverage. Consolidation—top five producers supplying over half capacity—intensifies pressure. Iluka mitigates this via consistent product quality, supply reliability and optionality across zircon and high‑grade TiO2 feedstocks.

Price sensitivity and cycles

End-use demand for Iluka's products tracks construction, automotive and consumer durables cycles, with 2024 weakness in automotive production and housing activity pushing buyers to demand discounts. Buyers press for concessions in downturns and resist increases when markets are soft; spot exposure can drive intra-year price swings of 15–25%. Multi-year contracts and index-linked formulas (common in heavy-minerals offtakes) help balance producer and buyer interests.

Product qualification stickiness

Pigment and ceramics lines demand rigorous feedstock qualification, often taking 6–18 months, which raises switching costs and can lock in supply once approved. That stickiness enables suppliers to command premiums for consistent chemistry and low impurities. Buyers frequently dual-source after qualification to preserve leverage and mitigate supply risk. Strong impurity control supports sustained pricing power in 2024 markets.

Backward integration options

Some pigment players such as Tronox (which merged with Cristal in 2019) are vertically integrated into mineral sands, reducing reliance on external ilmenite/rutile suppliers; integration is used as a bargaining lever even when external purchases continue. Iluka must differentiate on reliability and value-in-use, not only price, while strategic offtakes and partnerships align incentives across the value chain in 2024.

- Integrated players: Tronox (integrated since 2019)

- Bargaining lever: integration + external buying

- Iluka focus: reliability, value-in-use

- Alignment: strategic offtake and partnerships

Substitutability within feedstocks

Buyers can blend natural rutile, synthetic rutile and chloride slag for TiO2 and partially substitute zircon in some ceramics, giving purchasers leverage in negotiations; however process and quality constraints prevent full substitution without yield or performance penalties. Iluka preserves pricing and share through technical support, tailored specifications and supply reliability.

Buyers hold leverage as top-5 supply >50% of ~6Mt TiO2; spot swings 15-25%

Buyers hold strong leverage in the ~6 Mt TiO2 market (2024); top five producers supply >50% of capacity, amplifying bargaining power. 2024 autos/housing weakness drives discounting and spot volatility of 15–25% intra‑year. Long 6–18 month feedstock qualification and limited zircon substitution support Iluka premiums via quality, reliability and technical service.

| Metric | 2024 Value |

|---|---|

| Global TiO2 market | ~6,000,000 t |

| Top‑5 producer share | >50% |

| Spot price volatility | 15–25% |

| Feedstock qualification | 6–18 months |

Full Version Awaits

Iluka Porter's Five Forces Analysis

This preview shows the exact Iluka Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Iluka’s Porter's Five Forces snapshot highlights competitive intensity from miners, shifting buyer power, and substitution risks tied to alternative minerals and recycling; regulatory and capital barriers further shape strategic choices. This brief overview teases key pressure points and growth levers for Iluka’s zircon and titanium dioxide businesses. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Iluka’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Reagents, consumables and specialized equipment for mineral sands processing are sourced from a limited set of global suppliers, so outages of chlorinators, caustic or specialty parts can force higher costs or plant downtime; this supplier concentration raises switching costs and gives vendors pricing leverage, while long-term framework agreements reduce but do not eliminate that risk.

Energy and fuel dependency

Iluka’s operations are energy-intensive, relying on electricity, gas and diesel for mining and upgrading, including synthetic rutile kilns. Volatile energy prices and constrained regional grids compress margins and raise supplier leverage. Remote sites have limited interchangeable energy sources, increasing exposure to supplier power. Hedging programs and on-site efficiency projects partially mitigate that reliance.

Skilled labor and contractors

Geologists, metallurgists and mine contractors are scarce in key mining regions, with around 60% of operators in 2024 reporting critical skills shortages; tight regional labor markets and stricter safety compliance have driven mining services wage inflation and higher contractor rates. Project ramp-ups often coincide with regional booms, intensifying bidding pressure on staff and equipment. Training pipelines and multi-year service contracts (typically 3–7 years) mitigate but do not eliminate this supplier power.

Land, water, and permits

Access to leases, water rights and environmental permits functions as a quasi-supplier constraint for Iluka: in 2024 Iluka held about 2.1 million hectares of tenements, while project approvals in Australia commonly add 1–3 years to timelines, increasing carrying costs and reducing flexibility. Government agencies and communities can impose conditions, royalties or stricter standards that raise operating costs; delays strengthen external negotiating power and can erode project NPV. Early stakeholder engagement smooths approvals but increases pre-production lead time and up-front expenditure.

- Leases: ~2.1m ha tenements (2024)

- Approval delays: 12–36 months

- Impact: higher capex, longer lead times

- Mitigation: early stakeholder engagement

Logistics and ports

Vendors gain pricing leverage as supply, energy and logistics concentrate; top-3 ~60%, skills ~60%

Supplier concentration in reagents, energy and logistics gives vendors pricing leverage; 2024 saw top-3 carriers control ~60% capacity and global skills shortages hit ~60% of operators. Energy price volatility and remote-site dependencies raise switching costs and downtime risk. Long-term contracts, hedging and multi-port/contractor agreements partially mitigate but do not eliminate supplier power.

| Metric | 2024 |

|---|---|

| Tenements | ~2.1m ha |

| Top-3 carriers | ~60% capacity |

| Skills shortage | ~60% operators |

What is included in the product

Tailored Porter's Five Forces analysis for Iluka that uncovers competitive drivers, supplier and buyer bargaining power, threats from substitutes and new entrants, and industry rivalry; includes strategic implications and emerging risks to Iluka's pricing and profitability.

Compact one-sheet Porter's Five Forces for Iluka—clarifies supplier, buyer, substitute, entrant, and rivalry pressures for quick strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Buyer concentration

Major TiO2 pigment producers and large ceramics manufacturers handle outsized volumes in a roughly 6 million tonne global TiO2 market (2024), giving buyers strong negotiating leverage. Consolidation—top five producers supplying over half capacity—intensifies pressure. Iluka mitigates this via consistent product quality, supply reliability and optionality across zircon and high‑grade TiO2 feedstocks.

Price sensitivity and cycles

End-use demand for Iluka's products tracks construction, automotive and consumer durables cycles, with 2024 weakness in automotive production and housing activity pushing buyers to demand discounts. Buyers press for concessions in downturns and resist increases when markets are soft; spot exposure can drive intra-year price swings of 15–25%. Multi-year contracts and index-linked formulas (common in heavy-minerals offtakes) help balance producer and buyer interests.

Product qualification stickiness

Pigment and ceramics lines demand rigorous feedstock qualification, often taking 6–18 months, which raises switching costs and can lock in supply once approved. That stickiness enables suppliers to command premiums for consistent chemistry and low impurities. Buyers frequently dual-source after qualification to preserve leverage and mitigate supply risk. Strong impurity control supports sustained pricing power in 2024 markets.

Backward integration options

Some pigment players such as Tronox (which merged with Cristal in 2019) are vertically integrated into mineral sands, reducing reliance on external ilmenite/rutile suppliers; integration is used as a bargaining lever even when external purchases continue. Iluka must differentiate on reliability and value-in-use, not only price, while strategic offtakes and partnerships align incentives across the value chain in 2024.

- Integrated players: Tronox (integrated since 2019)

- Bargaining lever: integration + external buying

- Iluka focus: reliability, value-in-use

- Alignment: strategic offtake and partnerships

Substitutability within feedstocks

Buyers can blend natural rutile, synthetic rutile and chloride slag for TiO2 and partially substitute zircon in some ceramics, giving purchasers leverage in negotiations; however process and quality constraints prevent full substitution without yield or performance penalties. Iluka preserves pricing and share through technical support, tailored specifications and supply reliability.

Buyers hold leverage as top-5 supply >50% of ~6Mt TiO2; spot swings 15-25%

Buyers hold strong leverage in the ~6 Mt TiO2 market (2024); top five producers supply >50% of capacity, amplifying bargaining power. 2024 autos/housing weakness drives discounting and spot volatility of 15–25% intra‑year. Long 6–18 month feedstock qualification and limited zircon substitution support Iluka premiums via quality, reliability and technical service.

| Metric | 2024 Value |

|---|---|

| Global TiO2 market | ~6,000,000 t |

| Top‑5 producer share | >50% |

| Spot price volatility | 15–25% |

| Feedstock qualification | 6–18 months |

Full Version Awaits

Iluka Porter's Five Forces Analysis

This preview shows the exact Iluka Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable.