IMA Klessmann GmbH Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

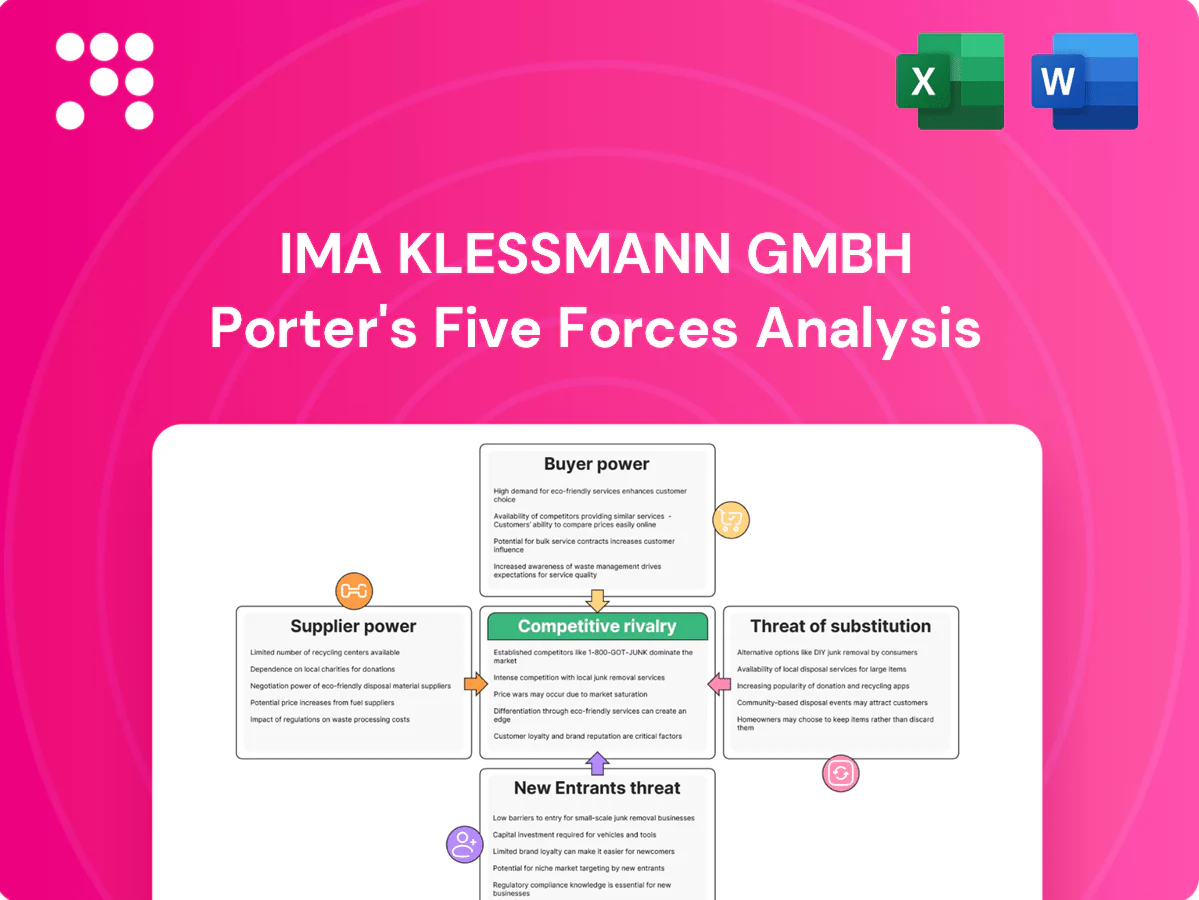

IMA Klessmann GmbH faces intense competitive dynamics across supplier leverage, buyer demands, and innovation-driven substitutes, with moderate barriers to entry and focused rivalry among OEMs and automation players. This snapshot outlines key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Concentrated automation suppliers

Core CNC controls, servomotors and linear guides are concentrated among a few global suppliers, with the top 5 vendors holding roughly 70–80% of market share in 2024, increasing supplier leverage on pricing and lead times (often 16–24 weeks). Dual-sourcing is feasible but typically demands engineering redesign and 6–18 months of requalification, so long qualification cycles entrench incumbents.

High switching and qualification costs

Requalifying critical parts in Klessmann woodworking machines typically takes 4–12 weeks, risking prolonged downtime and variability in cycle times. Safety and compliance recertifications often incur direct costs in the range of €10,000–€75,000 per line and add administrative lead time. Software and PLC integrations are tightly coupled to hardware ecosystems, creating vendor lock-in that affects up to 60% of control-layer decisions. These frictions elevate supplier bargaining power during price and lead-time negotiations.

Lead-time volatility and capacity constraints

Semiconductor and precision component bottlenecks—with chip lead times having peaked near 26 weeks in 2021—can still stretch delivery schedules and force IMA Klessmann to absorb delays. Suppliers commonly prioritize larger customers or higher-margin sectors, constraining available capacity for smaller OEMs. Extended lead times cascade into project delays and potential penalty exposure under OEM contracts. This scarcity strengthens suppliers’ bargaining positions in tight cycles.

Commodity inputs and price pass-through

Steel HRC averaged about 800 EUR/ton and LME aluminum near 2,300 USD/ton in 2024, while industrial energy prices remained elevated, directly raising machine frame and subsystem costs.

Suppliers typically pass cost rises within weeks, whereas OEMs often face a 3–9 month lag before customers accept higher prices, squeezing margins.

Hedging and long‑term frame agreements mitigate but do not eliminate volatility; persistent 2024 inflation sustained supplier‑OEM margin tension.

Specialized subsystems and IP

Proprietary spindles, gluing units and vacuum technologies embed supplier know-how, creating black-box modules that reduce interchangeability and increase vendor lock-in; joint development projects yield performance advantages while deepening dependence on those suppliers. Negotiation leverage therefore shifts toward vendors of unique, high-performance modules, raising switching costs and lengthening contract cycles.

- Vendor lock-in: black-box modules limit third-party replacements

- Joint R&D: boosts performance but increases reliance

- Bargaining shift: suppliers of proprietary tech hold pricing power

Supplier concentration, long lead times and commodity shocks squeeze OEM margins

Suppliers hold strong leverage: core CNC, servomotor and linear-guide vendors account for ~70–80% share in 2024, with critical lead times of 16–26 weeks and requalification often 4–18 months, creating lock-in and price power. Commodity cost pressure (steel ~800 EUR/t; aluminum ~2,300 USD/t in 2024) and fast supplier pass‑through (weeks) vs OEM price lag (3–9 months) squeeze margins. Proprietary modules and software integrations amplify switching costs.

| Metric | 2024 Value |

|---|---|

| Top-5 supplier share | 70–80% |

| Chip/lead times | 16–26 weeks |

| Steel | ~800 EUR/t |

| Aluminum | ~2,300 USD/t |

| Price pass-through | Suppliers: weeks; OEMs: 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to IMA Klessmann GmbH's position in industrial automation and packaging/labeling markets. Evaluates supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and strategic responses for pricing and profitability.

A concise one-sheet Porter's Five Forces for IMA Klessmann GmbH—instantly pinpoints supplier, buyer, competitive, entrant and substitute pressures to ease strategic decision‑making and prioritize mitigation actions.

Customers Bargaining Power

Consolidated industrial buyers

Large furniture and panel processors often buy full production lines and multi-plant programs, leveraging scale to drive competitive tenders and price pressure; in 2024 the global furniture market exceeded $600 billion, concentrating purchasing power. They routinely demand product customization, vendor financing and strict service SLAs. Ongoing consolidation of buyers across regions further amplifies their bargaining power versus suppliers like IMA Klessmann.

High ticket, long-cycle purchases

Capital equipment decisions at IMA Klessmann involve multi-year horizons (typically 3–7 years) and rigorous ROI scrutiny, with 2024 procurement teams demanding detailed payback models. Buyers use total cost of ownership analyses to extract discounts and service commitments, pushing for 95%+ uptime guarantees. Post-warranty service and spare-part costs drive negotiation leverage, and the infrequency of purchases magnifies each deal’s stakes.

Demand for turnkey integration

Customers increasingly demand turnkey integration—end-to-end lines including automation, software and material handling—shifting integration risk to OEMs and raising their accountability. Buyers leverage scope and interface complexity to extract performance guarantees; in 2024 the global industrial automation market (~$192B) magnifies buyer leverage on terms and acceptance criteria.

Global service and uptime expectations

Buyers demand global service reach, spare parts availability and digital diagnostics—2024 industry benchmarks cite ~98% uptime expectations and 60–70% adoption of remote diagnostics among industrial buyers. Customers negotiate bundled service contracts with strict response-time commitments and common downtime penalties of 1–5% of contract value, tightening vendor obligations. Strong SLAs shift negotiating power toward buyers by making lifecycle costs a primary bargaining lever.

- Service reach: global 24/7 expectations

- Spare parts: same‑day/next‑day availability drives selection

- Digital diagnostics: 60–70% adoption raises monitoring demands

- SLA penalties: 1–5% of contract value enforce uptime

Alternative sourcing and refurb options

Buyers increasingly use rival brands or certified used machinery and refurb options to lower capex; refurbished lines and modular upgrades emerged as credible 2024 alternatives that discipline pricing for new equipment. Integration complexity and warranty limits keep substitution weak for highly engineered lines, preserving some pricing power for IMA Klessmann.

- 2024: certified used/refurb options rose as procurement levers

- Disciplines new-equipment pricing

- Integration/warranty limit substitution for complex lines

Buyers in > $600B furniture market demand 98%+ uptime, 60–70% remote diagnostics

Large furniture/panel buyers (> $600B global market in 2024) concentrate purchasing power and extract price concessions; multi-year capex cycles (3–7 years) and rigorous TCO/ROI models push for deep discounts. Buyers demand 98%+ uptime, 60–70% remote diagnostics adoption and 1–5% SLA penalties, shifting lifecycle costs to suppliers. Certified refurbished options in 2024 materially discipline new-equipment pricing while complex integrations preserve some OEM pricing power.

| Metric | 2024 Value |

|---|---|

| Global furniture market | > $600B |

| Industrial automation market | ~ $192B |

| Uptime expectation | ~98%+ |

| Remote diagnostics adoption | 60–70% |

| SLA penalties | 1–5% contract value |

Preview Before You Purchase

IMA Klessmann GmbH Porter's Five Forces Analysis

This preview shows the exact IMA Klessmann GmbH Porter's Five Forces Analysis you'll receive—fully written, professionally formatted, and ready for use. There are no samples, placeholders, or mockups; the content here is the final deliverable. Purchase grants instant access to this same file for immediate download. Use it as-is for strategic insight and decision-making.

A Must-Have Tool for Decision-Makers

IMA Klessmann GmbH faces intense competitive dynamics across supplier leverage, buyer demands, and innovation-driven substitutes, with moderate barriers to entry and focused rivalry among OEMs and automation players. This snapshot outlines key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Concentrated automation suppliers

Core CNC controls, servomotors and linear guides are concentrated among a few global suppliers, with the top 5 vendors holding roughly 70–80% of market share in 2024, increasing supplier leverage on pricing and lead times (often 16–24 weeks). Dual-sourcing is feasible but typically demands engineering redesign and 6–18 months of requalification, so long qualification cycles entrench incumbents.

High switching and qualification costs

Requalifying critical parts in Klessmann woodworking machines typically takes 4–12 weeks, risking prolonged downtime and variability in cycle times. Safety and compliance recertifications often incur direct costs in the range of €10,000–€75,000 per line and add administrative lead time. Software and PLC integrations are tightly coupled to hardware ecosystems, creating vendor lock-in that affects up to 60% of control-layer decisions. These frictions elevate supplier bargaining power during price and lead-time negotiations.

Lead-time volatility and capacity constraints

Semiconductor and precision component bottlenecks—with chip lead times having peaked near 26 weeks in 2021—can still stretch delivery schedules and force IMA Klessmann to absorb delays. Suppliers commonly prioritize larger customers or higher-margin sectors, constraining available capacity for smaller OEMs. Extended lead times cascade into project delays and potential penalty exposure under OEM contracts. This scarcity strengthens suppliers’ bargaining positions in tight cycles.

Commodity inputs and price pass-through

Steel HRC averaged about 800 EUR/ton and LME aluminum near 2,300 USD/ton in 2024, while industrial energy prices remained elevated, directly raising machine frame and subsystem costs.

Suppliers typically pass cost rises within weeks, whereas OEMs often face a 3–9 month lag before customers accept higher prices, squeezing margins.

Hedging and long‑term frame agreements mitigate but do not eliminate volatility; persistent 2024 inflation sustained supplier‑OEM margin tension.

Specialized subsystems and IP

Proprietary spindles, gluing units and vacuum technologies embed supplier know-how, creating black-box modules that reduce interchangeability and increase vendor lock-in; joint development projects yield performance advantages while deepening dependence on those suppliers. Negotiation leverage therefore shifts toward vendors of unique, high-performance modules, raising switching costs and lengthening contract cycles.

- Vendor lock-in: black-box modules limit third-party replacements

- Joint R&D: boosts performance but increases reliance

- Bargaining shift: suppliers of proprietary tech hold pricing power

Supplier concentration, long lead times and commodity shocks squeeze OEM margins

Suppliers hold strong leverage: core CNC, servomotor and linear-guide vendors account for ~70–80% share in 2024, with critical lead times of 16–26 weeks and requalification often 4–18 months, creating lock-in and price power. Commodity cost pressure (steel ~800 EUR/t; aluminum ~2,300 USD/t in 2024) and fast supplier pass‑through (weeks) vs OEM price lag (3–9 months) squeeze margins. Proprietary modules and software integrations amplify switching costs.

| Metric | 2024 Value |

|---|---|

| Top-5 supplier share | 70–80% |

| Chip/lead times | 16–26 weeks |

| Steel | ~800 EUR/t |

| Aluminum | ~2,300 USD/t |

| Price pass-through | Suppliers: weeks; OEMs: 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to IMA Klessmann GmbH's position in industrial automation and packaging/labeling markets. Evaluates supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and strategic responses for pricing and profitability.

A concise one-sheet Porter's Five Forces for IMA Klessmann GmbH—instantly pinpoints supplier, buyer, competitive, entrant and substitute pressures to ease strategic decision‑making and prioritize mitigation actions.

Customers Bargaining Power

Consolidated industrial buyers

Large furniture and panel processors often buy full production lines and multi-plant programs, leveraging scale to drive competitive tenders and price pressure; in 2024 the global furniture market exceeded $600 billion, concentrating purchasing power. They routinely demand product customization, vendor financing and strict service SLAs. Ongoing consolidation of buyers across regions further amplifies their bargaining power versus suppliers like IMA Klessmann.

High ticket, long-cycle purchases

Capital equipment decisions at IMA Klessmann involve multi-year horizons (typically 3–7 years) and rigorous ROI scrutiny, with 2024 procurement teams demanding detailed payback models. Buyers use total cost of ownership analyses to extract discounts and service commitments, pushing for 95%+ uptime guarantees. Post-warranty service and spare-part costs drive negotiation leverage, and the infrequency of purchases magnifies each deal’s stakes.

Demand for turnkey integration

Customers increasingly demand turnkey integration—end-to-end lines including automation, software and material handling—shifting integration risk to OEMs and raising their accountability. Buyers leverage scope and interface complexity to extract performance guarantees; in 2024 the global industrial automation market (~$192B) magnifies buyer leverage on terms and acceptance criteria.

Global service and uptime expectations

Buyers demand global service reach, spare parts availability and digital diagnostics—2024 industry benchmarks cite ~98% uptime expectations and 60–70% adoption of remote diagnostics among industrial buyers. Customers negotiate bundled service contracts with strict response-time commitments and common downtime penalties of 1–5% of contract value, tightening vendor obligations. Strong SLAs shift negotiating power toward buyers by making lifecycle costs a primary bargaining lever.

- Service reach: global 24/7 expectations

- Spare parts: same‑day/next‑day availability drives selection

- Digital diagnostics: 60–70% adoption raises monitoring demands

- SLA penalties: 1–5% of contract value enforce uptime

Alternative sourcing and refurb options

Buyers increasingly use rival brands or certified used machinery and refurb options to lower capex; refurbished lines and modular upgrades emerged as credible 2024 alternatives that discipline pricing for new equipment. Integration complexity and warranty limits keep substitution weak for highly engineered lines, preserving some pricing power for IMA Klessmann.

- 2024: certified used/refurb options rose as procurement levers

- Disciplines new-equipment pricing

- Integration/warranty limit substitution for complex lines

Buyers in > $600B furniture market demand 98%+ uptime, 60–70% remote diagnostics

Large furniture/panel buyers (> $600B global market in 2024) concentrate purchasing power and extract price concessions; multi-year capex cycles (3–7 years) and rigorous TCO/ROI models push for deep discounts. Buyers demand 98%+ uptime, 60–70% remote diagnostics adoption and 1–5% SLA penalties, shifting lifecycle costs to suppliers. Certified refurbished options in 2024 materially discipline new-equipment pricing while complex integrations preserve some OEM pricing power.

| Metric | 2024 Value |

|---|---|

| Global furniture market | > $600B |

| Industrial automation market | ~ $192B |

| Uptime expectation | ~98%+ |

| Remote diagnostics adoption | 60–70% |

| SLA penalties | 1–5% contract value |

Preview Before You Purchase

IMA Klessmann GmbH Porter's Five Forces Analysis

This preview shows the exact IMA Klessmann GmbH Porter's Five Forces Analysis you'll receive—fully written, professionally formatted, and ready for use. There are no samples, placeholders, or mockups; the content here is the final deliverable. Purchase grants instant access to this same file for immediate download. Use it as-is for strategic insight and decision-making.

Description

A Must-Have Tool for Decision-Makers

IMA Klessmann GmbH faces intense competitive dynamics across supplier leverage, buyer demands, and innovation-driven substitutes, with moderate barriers to entry and focused rivalry among OEMs and automation players. This snapshot outlines key pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Concentrated automation suppliers

Core CNC controls, servomotors and linear guides are concentrated among a few global suppliers, with the top 5 vendors holding roughly 70–80% of market share in 2024, increasing supplier leverage on pricing and lead times (often 16–24 weeks). Dual-sourcing is feasible but typically demands engineering redesign and 6–18 months of requalification, so long qualification cycles entrench incumbents.

High switching and qualification costs

Requalifying critical parts in Klessmann woodworking machines typically takes 4–12 weeks, risking prolonged downtime and variability in cycle times. Safety and compliance recertifications often incur direct costs in the range of €10,000–€75,000 per line and add administrative lead time. Software and PLC integrations are tightly coupled to hardware ecosystems, creating vendor lock-in that affects up to 60% of control-layer decisions. These frictions elevate supplier bargaining power during price and lead-time negotiations.

Lead-time volatility and capacity constraints

Semiconductor and precision component bottlenecks—with chip lead times having peaked near 26 weeks in 2021—can still stretch delivery schedules and force IMA Klessmann to absorb delays. Suppliers commonly prioritize larger customers or higher-margin sectors, constraining available capacity for smaller OEMs. Extended lead times cascade into project delays and potential penalty exposure under OEM contracts. This scarcity strengthens suppliers’ bargaining positions in tight cycles.

Commodity inputs and price pass-through

Steel HRC averaged about 800 EUR/ton and LME aluminum near 2,300 USD/ton in 2024, while industrial energy prices remained elevated, directly raising machine frame and subsystem costs.

Suppliers typically pass cost rises within weeks, whereas OEMs often face a 3–9 month lag before customers accept higher prices, squeezing margins.

Hedging and long‑term frame agreements mitigate but do not eliminate volatility; persistent 2024 inflation sustained supplier‑OEM margin tension.

Specialized subsystems and IP

Proprietary spindles, gluing units and vacuum technologies embed supplier know-how, creating black-box modules that reduce interchangeability and increase vendor lock-in; joint development projects yield performance advantages while deepening dependence on those suppliers. Negotiation leverage therefore shifts toward vendors of unique, high-performance modules, raising switching costs and lengthening contract cycles.

- Vendor lock-in: black-box modules limit third-party replacements

- Joint R&D: boosts performance but increases reliance

- Bargaining shift: suppliers of proprietary tech hold pricing power

Supplier concentration, long lead times and commodity shocks squeeze OEM margins

Suppliers hold strong leverage: core CNC, servomotor and linear-guide vendors account for ~70–80% share in 2024, with critical lead times of 16–26 weeks and requalification often 4–18 months, creating lock-in and price power. Commodity cost pressure (steel ~800 EUR/t; aluminum ~2,300 USD/t in 2024) and fast supplier pass‑through (weeks) vs OEM price lag (3–9 months) squeeze margins. Proprietary modules and software integrations amplify switching costs.

| Metric | 2024 Value |

|---|---|

| Top-5 supplier share | 70–80% |

| Chip/lead times | 16–26 weeks |

| Steel | ~800 EUR/t |

| Aluminum | ~2,300 USD/t |

| Price pass-through | Suppliers: weeks; OEMs: 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to IMA Klessmann GmbH's position in industrial automation and packaging/labeling markets. Evaluates supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and strategic responses for pricing and profitability.

A concise one-sheet Porter's Five Forces for IMA Klessmann GmbH—instantly pinpoints supplier, buyer, competitive, entrant and substitute pressures to ease strategic decision‑making and prioritize mitigation actions.

Customers Bargaining Power

Consolidated industrial buyers

Large furniture and panel processors often buy full production lines and multi-plant programs, leveraging scale to drive competitive tenders and price pressure; in 2024 the global furniture market exceeded $600 billion, concentrating purchasing power. They routinely demand product customization, vendor financing and strict service SLAs. Ongoing consolidation of buyers across regions further amplifies their bargaining power versus suppliers like IMA Klessmann.

High ticket, long-cycle purchases

Capital equipment decisions at IMA Klessmann involve multi-year horizons (typically 3–7 years) and rigorous ROI scrutiny, with 2024 procurement teams demanding detailed payback models. Buyers use total cost of ownership analyses to extract discounts and service commitments, pushing for 95%+ uptime guarantees. Post-warranty service and spare-part costs drive negotiation leverage, and the infrequency of purchases magnifies each deal’s stakes.

Demand for turnkey integration

Customers increasingly demand turnkey integration—end-to-end lines including automation, software and material handling—shifting integration risk to OEMs and raising their accountability. Buyers leverage scope and interface complexity to extract performance guarantees; in 2024 the global industrial automation market (~$192B) magnifies buyer leverage on terms and acceptance criteria.

Global service and uptime expectations

Buyers demand global service reach, spare parts availability and digital diagnostics—2024 industry benchmarks cite ~98% uptime expectations and 60–70% adoption of remote diagnostics among industrial buyers. Customers negotiate bundled service contracts with strict response-time commitments and common downtime penalties of 1–5% of contract value, tightening vendor obligations. Strong SLAs shift negotiating power toward buyers by making lifecycle costs a primary bargaining lever.

- Service reach: global 24/7 expectations

- Spare parts: same‑day/next‑day availability drives selection

- Digital diagnostics: 60–70% adoption raises monitoring demands

- SLA penalties: 1–5% of contract value enforce uptime

Alternative sourcing and refurb options

Buyers increasingly use rival brands or certified used machinery and refurb options to lower capex; refurbished lines and modular upgrades emerged as credible 2024 alternatives that discipline pricing for new equipment. Integration complexity and warranty limits keep substitution weak for highly engineered lines, preserving some pricing power for IMA Klessmann.

- 2024: certified used/refurb options rose as procurement levers

- Disciplines new-equipment pricing

- Integration/warranty limit substitution for complex lines

Buyers in > $600B furniture market demand 98%+ uptime, 60–70% remote diagnostics

Large furniture/panel buyers (> $600B global market in 2024) concentrate purchasing power and extract price concessions; multi-year capex cycles (3–7 years) and rigorous TCO/ROI models push for deep discounts. Buyers demand 98%+ uptime, 60–70% remote diagnostics adoption and 1–5% SLA penalties, shifting lifecycle costs to suppliers. Certified refurbished options in 2024 materially discipline new-equipment pricing while complex integrations preserve some OEM pricing power.

| Metric | 2024 Value |

|---|---|

| Global furniture market | > $600B |

| Industrial automation market | ~ $192B |

| Uptime expectation | ~98%+ |

| Remote diagnostics adoption | 60–70% |

| SLA penalties | 1–5% contract value |

Preview Before You Purchase

IMA Klessmann GmbH Porter's Five Forces Analysis

This preview shows the exact IMA Klessmann GmbH Porter's Five Forces Analysis you'll receive—fully written, professionally formatted, and ready for use. There are no samples, placeholders, or mockups; the content here is the final deliverable. Purchase grants instant access to this same file for immediate download. Use it as-is for strategic insight and decision-making.