Impinj Porter's Five Forces Analysis

Don't Miss the Bigger Picture

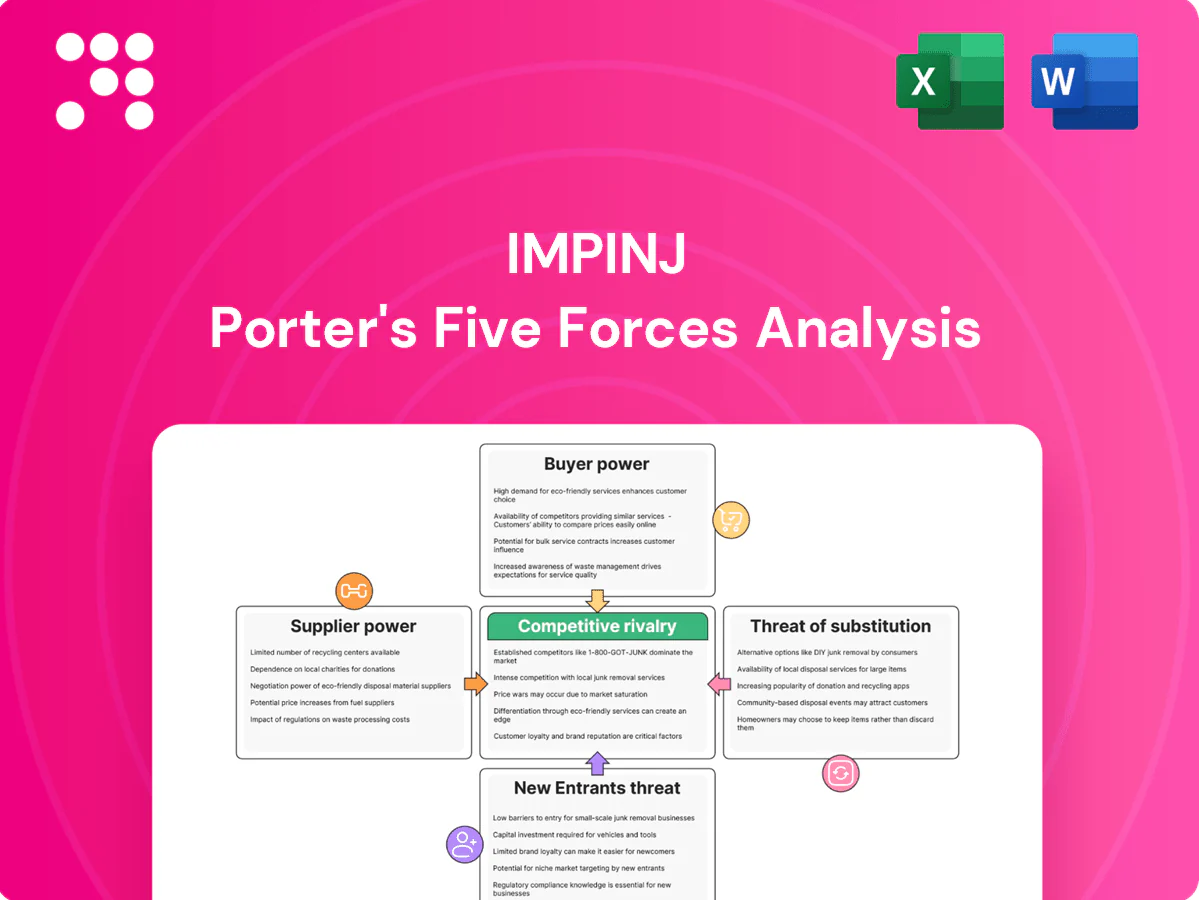

Impinj faces moderate supplier power, strong buyer expectations for integration, and ongoing pressure from semiconductor rivals and alternative tagging technologies, while barriers for new entrants remain significant but evolving. This snapshot highlights key tensions shaping Impinj’s strategy and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Foundry concentration

Impinj depends on a small set of advanced semiconductor foundries for endpoint ICs and RF components, and in 2024 TSMC remained the dominant advanced-node foundry, concentrating supply. Limited alternative capacity gives foundries pricing and allocation leverage, especially in tight cycles. Long lead times and qualification hurdles raise switching costs. Multi-year supply agreements can mitigate but do not eliminate this power.

Specialty RF inputs

High-performance RF substrates, antennas and packaging materials are niche and vendor-limited, with supplier concentration exceeding 60% in 2024 for advanced RF substrates. Performance specs (sensitivity, transmit power) tightly constrain substitution, forcing designers to accept specific materials. Suppliers influence cost and timelines through MOQs often in the 5,000–50,000 unit range and formal change notices. Dual-sourcing is feasible but typically requires 3–6 months of requalification and testing.

Tooling and test equipment

RADIO test rigs, wafer probers and calibration systems are highly specialized capital equipment, with wafer probers typically costing $1–5 million and test rigs/calibration systems often ranging from $100k–2 million, creating strong supplier leverage. Proprietary interfaces and software cause vendor lock-in, making tool swaps risky as upgrades or replacements can reduce yield and throughput during qualification. Customers often commit to volume or long-term service contracts to gain priority support and spare parts, accepting higher fixed costs in return for reduced downtime.

Software and cloud dependencies

Reader firmware stacks, SDKs, and cloud services underpin Impinj’s platform; in 2024 the three largest cloud providers (AWS, Azure, GCP) still held over 60% market share, concentrating supplier power. License or pricing shifts from these providers can compress margins, while compliance updates and security patches create ongoing operational reliance. Building in-house alternatives cuts dependency but raises R&D and OpEx.

- Concentration: >60% market share by top-3 clouds (2024)

- Risk: licensing/pricing can squeeze margins

- Ongoing: compliance/security patch cadence

- Trade-off: in-house reduces risk but increases costs

Logistics and OSAT capacity

Outsourced assembly and test providers (OSATs) control critical packaging throughput, and during peak seasons they often reallocate capacity toward larger contracts, squeezing smaller lots and ramp schedules. Disruptions at key OSATs cascade directly into Impinj customer delivery SLAs, raising fulfillment risk despite hedging. Buffer inventory and a diversified OSAT base reduce but do not eliminate this exposure.

- OSAT control of throughput

- Peak-season reallocation risk

- Disruptions → SLA impact

- Diversification lowers but not removes exposure

High supplier power: foundry dominance, RF substrates >60%, requalification 3-6 months

Impinj faces high supplier power: TSMC dominance and niche RF substrate suppliers (top-3 >60% in 2024) limit pricing leverage and capacity. Capital test equipment and OSAT bottlenecks raise switching costs and lead times, while cloud dependence (top-3 >60% share in 2024) risks margin pressure. Long requalification (3–6 months) sustains supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Foundries | TSMC dominant | High pricing/allocation |

| RF substrates | Top-3 >60% | Low substitution |

| Cloud | Top-3 >60% | Margin risk |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks specific to Impinj, identifying substitutes and disruptive threats that could erode RFID market share while evaluating dynamics that protect incumbency and influence pricing and profitability.

A concise Porter's Five Forces one-sheet for Impinj that highlights competitor, supplier, buyer, substitute, and entry pressures—ready to drop into decks to speed strategic decisions and reduce research time.

Customers Bargaining Power

Large enterprise buyers

Large enterprise buyers such as retailers, logistics firms and airlines purchase RFID at scale and negotiate aggressively, leveraging order sizes to extract price concessions and bespoke SLAs; in 2024 Impinj disclosed its top 10 customers represented roughly 45% of revenue, underscoring concentration risk. Consolidated buying via systems integrators amplifies leverage, and losing a key account can materially reduce revenue visibility and forecasting certainty.

Price sensitivity of tags

Tag ICs are high-volume, low-ASP components—by 2024 typical passive UHF IC ASPs ran in the cent range—so buyers relentlessly benchmark suppliers and drive cost reductions; even $0.01–$0.03 price deltas can flip share in multi-million-unit rollouts. Procurement demands proven read rates, reliability and lower TCO, making performance metrics (read rates >99% in trials) as decisive as unit price.

Standards-based comparability

RAIN/EPC Gen2 compliance enables apples-to-apples comparisons; with over 90% of enterprise RAIN deployments using Gen2, customers can multi-source readers and tags with minimal redesign, moderating switching costs and squeezing margin. Differentiation must come from read performance, software ecosystems and service—areas where Impinj emphasized software subscription growth in 2024.

Solution integration demands

Enterprises demand turnkey outcomes across hardware, middleware and analytics, driving systems integrators to influence vendor selection; pilots and performance SLAs commonly extend sales cycles to 3–6 months and increase discount pressure, while strong partner ecosystems help recapture bargaining balance for vendors.

- Enterprise turnkey demand

- Integrators steer vendor choice

- Pilots 3–6 months, higher discounts

- Partner ecosystems mitigate pressure

Data and platform expectations

Buyers now demand item-level intelligence, robust APIs, and enterprise-grade security, pushing Impinj to provide roadmap access and premium support as negotiating levers; enterprise customers often secure multi-year SLAs and feature roadmaps tied to purchases. Failure to meet these data needs drives customers to rivals or software substitutes, increasing churn risk. Ongoing service quality and support responsiveness directly affect renewal leverage, with enterprise renewal rates generally exceeding 80% in 2024.

- Data-first buyers

- API and security demands

- Roadmap & SLA negotiation

- Service quality = renewal leverage

Enterprise buyers hold leverage; top clients ~45%, pilots 3–6m

Enterprise buyers hold strong leverage: Impinj's top 10 customers ~45% of 2024 revenue, procurement drives aggressive price concessions and bespoke SLAs. Passive UHF IC ASPs typically $0.01–$0.03 in 2024, so minute price deltas shift multi-million unit deals; pilots take 3–6 months and renewal rates exceed 80%. RAIN Gen2 compatibility (>90% deployments) lowers switching costs, forcing differentiation via software and SLAs.

| Metric | 2024 Value |

|---|---|

| Top-10 revenue share | ~45% |

| Passive UHF IC ASP | $0.01–$0.03 |

| RAIN Gen2 adoption | >90% |

| Pilot length | 3–6 months |

| Enterprise renewal rate | >80% |

Preview Before You Purchase

Impinj Porter's Five Forces Analysis

This preview shows the exact Impinj Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or excerpts. It is the full, professionally formatted document ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.

Don't Miss the Bigger Picture

Impinj faces moderate supplier power, strong buyer expectations for integration, and ongoing pressure from semiconductor rivals and alternative tagging technologies, while barriers for new entrants remain significant but evolving. This snapshot highlights key tensions shaping Impinj’s strategy and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Foundry concentration

Impinj depends on a small set of advanced semiconductor foundries for endpoint ICs and RF components, and in 2024 TSMC remained the dominant advanced-node foundry, concentrating supply. Limited alternative capacity gives foundries pricing and allocation leverage, especially in tight cycles. Long lead times and qualification hurdles raise switching costs. Multi-year supply agreements can mitigate but do not eliminate this power.

Specialty RF inputs

High-performance RF substrates, antennas and packaging materials are niche and vendor-limited, with supplier concentration exceeding 60% in 2024 for advanced RF substrates. Performance specs (sensitivity, transmit power) tightly constrain substitution, forcing designers to accept specific materials. Suppliers influence cost and timelines through MOQs often in the 5,000–50,000 unit range and formal change notices. Dual-sourcing is feasible but typically requires 3–6 months of requalification and testing.

Tooling and test equipment

RADIO test rigs, wafer probers and calibration systems are highly specialized capital equipment, with wafer probers typically costing $1–5 million and test rigs/calibration systems often ranging from $100k–2 million, creating strong supplier leverage. Proprietary interfaces and software cause vendor lock-in, making tool swaps risky as upgrades or replacements can reduce yield and throughput during qualification. Customers often commit to volume or long-term service contracts to gain priority support and spare parts, accepting higher fixed costs in return for reduced downtime.

Software and cloud dependencies

Reader firmware stacks, SDKs, and cloud services underpin Impinj’s platform; in 2024 the three largest cloud providers (AWS, Azure, GCP) still held over 60% market share, concentrating supplier power. License or pricing shifts from these providers can compress margins, while compliance updates and security patches create ongoing operational reliance. Building in-house alternatives cuts dependency but raises R&D and OpEx.

- Concentration: >60% market share by top-3 clouds (2024)

- Risk: licensing/pricing can squeeze margins

- Ongoing: compliance/security patch cadence

- Trade-off: in-house reduces risk but increases costs

Logistics and OSAT capacity

Outsourced assembly and test providers (OSATs) control critical packaging throughput, and during peak seasons they often reallocate capacity toward larger contracts, squeezing smaller lots and ramp schedules. Disruptions at key OSATs cascade directly into Impinj customer delivery SLAs, raising fulfillment risk despite hedging. Buffer inventory and a diversified OSAT base reduce but do not eliminate this exposure.

- OSAT control of throughput

- Peak-season reallocation risk

- Disruptions → SLA impact

- Diversification lowers but not removes exposure

High supplier power: foundry dominance, RF substrates >60%, requalification 3-6 months

Impinj faces high supplier power: TSMC dominance and niche RF substrate suppliers (top-3 >60% in 2024) limit pricing leverage and capacity. Capital test equipment and OSAT bottlenecks raise switching costs and lead times, while cloud dependence (top-3 >60% share in 2024) risks margin pressure. Long requalification (3–6 months) sustains supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Foundries | TSMC dominant | High pricing/allocation |

| RF substrates | Top-3 >60% | Low substitution |

| Cloud | Top-3 >60% | Margin risk |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks specific to Impinj, identifying substitutes and disruptive threats that could erode RFID market share while evaluating dynamics that protect incumbency and influence pricing and profitability.

A concise Porter's Five Forces one-sheet for Impinj that highlights competitor, supplier, buyer, substitute, and entry pressures—ready to drop into decks to speed strategic decisions and reduce research time.

Customers Bargaining Power

Large enterprise buyers

Large enterprise buyers such as retailers, logistics firms and airlines purchase RFID at scale and negotiate aggressively, leveraging order sizes to extract price concessions and bespoke SLAs; in 2024 Impinj disclosed its top 10 customers represented roughly 45% of revenue, underscoring concentration risk. Consolidated buying via systems integrators amplifies leverage, and losing a key account can materially reduce revenue visibility and forecasting certainty.

Price sensitivity of tags

Tag ICs are high-volume, low-ASP components—by 2024 typical passive UHF IC ASPs ran in the cent range—so buyers relentlessly benchmark suppliers and drive cost reductions; even $0.01–$0.03 price deltas can flip share in multi-million-unit rollouts. Procurement demands proven read rates, reliability and lower TCO, making performance metrics (read rates >99% in trials) as decisive as unit price.

Standards-based comparability

RAIN/EPC Gen2 compliance enables apples-to-apples comparisons; with over 90% of enterprise RAIN deployments using Gen2, customers can multi-source readers and tags with minimal redesign, moderating switching costs and squeezing margin. Differentiation must come from read performance, software ecosystems and service—areas where Impinj emphasized software subscription growth in 2024.

Solution integration demands

Enterprises demand turnkey outcomes across hardware, middleware and analytics, driving systems integrators to influence vendor selection; pilots and performance SLAs commonly extend sales cycles to 3–6 months and increase discount pressure, while strong partner ecosystems help recapture bargaining balance for vendors.

- Enterprise turnkey demand

- Integrators steer vendor choice

- Pilots 3–6 months, higher discounts

- Partner ecosystems mitigate pressure

Data and platform expectations

Buyers now demand item-level intelligence, robust APIs, and enterprise-grade security, pushing Impinj to provide roadmap access and premium support as negotiating levers; enterprise customers often secure multi-year SLAs and feature roadmaps tied to purchases. Failure to meet these data needs drives customers to rivals or software substitutes, increasing churn risk. Ongoing service quality and support responsiveness directly affect renewal leverage, with enterprise renewal rates generally exceeding 80% in 2024.

- Data-first buyers

- API and security demands

- Roadmap & SLA negotiation

- Service quality = renewal leverage

Enterprise buyers hold leverage; top clients ~45%, pilots 3–6m

Enterprise buyers hold strong leverage: Impinj's top 10 customers ~45% of 2024 revenue, procurement drives aggressive price concessions and bespoke SLAs. Passive UHF IC ASPs typically $0.01–$0.03 in 2024, so minute price deltas shift multi-million unit deals; pilots take 3–6 months and renewal rates exceed 80%. RAIN Gen2 compatibility (>90% deployments) lowers switching costs, forcing differentiation via software and SLAs.

| Metric | 2024 Value |

|---|---|

| Top-10 revenue share | ~45% |

| Passive UHF IC ASP | $0.01–$0.03 |

| RAIN Gen2 adoption | >90% |

| Pilot length | 3–6 months |

| Enterprise renewal rate | >80% |

Preview Before You Purchase

Impinj Porter's Five Forces Analysis

This preview shows the exact Impinj Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or excerpts. It is the full, professionally formatted document ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Impinj faces moderate supplier power, strong buyer expectations for integration, and ongoing pressure from semiconductor rivals and alternative tagging technologies, while barriers for new entrants remain significant but evolving. This snapshot highlights key tensions shaping Impinj’s strategy and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Foundry concentration

Impinj depends on a small set of advanced semiconductor foundries for endpoint ICs and RF components, and in 2024 TSMC remained the dominant advanced-node foundry, concentrating supply. Limited alternative capacity gives foundries pricing and allocation leverage, especially in tight cycles. Long lead times and qualification hurdles raise switching costs. Multi-year supply agreements can mitigate but do not eliminate this power.

Specialty RF inputs

High-performance RF substrates, antennas and packaging materials are niche and vendor-limited, with supplier concentration exceeding 60% in 2024 for advanced RF substrates. Performance specs (sensitivity, transmit power) tightly constrain substitution, forcing designers to accept specific materials. Suppliers influence cost and timelines through MOQs often in the 5,000–50,000 unit range and formal change notices. Dual-sourcing is feasible but typically requires 3–6 months of requalification and testing.

Tooling and test equipment

RADIO test rigs, wafer probers and calibration systems are highly specialized capital equipment, with wafer probers typically costing $1–5 million and test rigs/calibration systems often ranging from $100k–2 million, creating strong supplier leverage. Proprietary interfaces and software cause vendor lock-in, making tool swaps risky as upgrades or replacements can reduce yield and throughput during qualification. Customers often commit to volume or long-term service contracts to gain priority support and spare parts, accepting higher fixed costs in return for reduced downtime.

Software and cloud dependencies

Reader firmware stacks, SDKs, and cloud services underpin Impinj’s platform; in 2024 the three largest cloud providers (AWS, Azure, GCP) still held over 60% market share, concentrating supplier power. License or pricing shifts from these providers can compress margins, while compliance updates and security patches create ongoing operational reliance. Building in-house alternatives cuts dependency but raises R&D and OpEx.

- Concentration: >60% market share by top-3 clouds (2024)

- Risk: licensing/pricing can squeeze margins

- Ongoing: compliance/security patch cadence

- Trade-off: in-house reduces risk but increases costs

Logistics and OSAT capacity

Outsourced assembly and test providers (OSATs) control critical packaging throughput, and during peak seasons they often reallocate capacity toward larger contracts, squeezing smaller lots and ramp schedules. Disruptions at key OSATs cascade directly into Impinj customer delivery SLAs, raising fulfillment risk despite hedging. Buffer inventory and a diversified OSAT base reduce but do not eliminate this exposure.

- OSAT control of throughput

- Peak-season reallocation risk

- Disruptions → SLA impact

- Diversification lowers but not removes exposure

High supplier power: foundry dominance, RF substrates >60%, requalification 3-6 months

Impinj faces high supplier power: TSMC dominance and niche RF substrate suppliers (top-3 >60% in 2024) limit pricing leverage and capacity. Capital test equipment and OSAT bottlenecks raise switching costs and lead times, while cloud dependence (top-3 >60% share in 2024) risks margin pressure. Long requalification (3–6 months) sustains supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Foundries | TSMC dominant | High pricing/allocation |

| RF substrates | Top-3 >60% | Low substitution |

| Cloud | Top-3 >60% | Margin risk |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks specific to Impinj, identifying substitutes and disruptive threats that could erode RFID market share while evaluating dynamics that protect incumbency and influence pricing and profitability.

A concise Porter's Five Forces one-sheet for Impinj that highlights competitor, supplier, buyer, substitute, and entry pressures—ready to drop into decks to speed strategic decisions and reduce research time.

Customers Bargaining Power

Large enterprise buyers

Large enterprise buyers such as retailers, logistics firms and airlines purchase RFID at scale and negotiate aggressively, leveraging order sizes to extract price concessions and bespoke SLAs; in 2024 Impinj disclosed its top 10 customers represented roughly 45% of revenue, underscoring concentration risk. Consolidated buying via systems integrators amplifies leverage, and losing a key account can materially reduce revenue visibility and forecasting certainty.

Price sensitivity of tags

Tag ICs are high-volume, low-ASP components—by 2024 typical passive UHF IC ASPs ran in the cent range—so buyers relentlessly benchmark suppliers and drive cost reductions; even $0.01–$0.03 price deltas can flip share in multi-million-unit rollouts. Procurement demands proven read rates, reliability and lower TCO, making performance metrics (read rates >99% in trials) as decisive as unit price.

Standards-based comparability

RAIN/EPC Gen2 compliance enables apples-to-apples comparisons; with over 90% of enterprise RAIN deployments using Gen2, customers can multi-source readers and tags with minimal redesign, moderating switching costs and squeezing margin. Differentiation must come from read performance, software ecosystems and service—areas where Impinj emphasized software subscription growth in 2024.

Solution integration demands

Enterprises demand turnkey outcomes across hardware, middleware and analytics, driving systems integrators to influence vendor selection; pilots and performance SLAs commonly extend sales cycles to 3–6 months and increase discount pressure, while strong partner ecosystems help recapture bargaining balance for vendors.

- Enterprise turnkey demand

- Integrators steer vendor choice

- Pilots 3–6 months, higher discounts

- Partner ecosystems mitigate pressure

Data and platform expectations

Buyers now demand item-level intelligence, robust APIs, and enterprise-grade security, pushing Impinj to provide roadmap access and premium support as negotiating levers; enterprise customers often secure multi-year SLAs and feature roadmaps tied to purchases. Failure to meet these data needs drives customers to rivals or software substitutes, increasing churn risk. Ongoing service quality and support responsiveness directly affect renewal leverage, with enterprise renewal rates generally exceeding 80% in 2024.

- Data-first buyers

- API and security demands

- Roadmap & SLA negotiation

- Service quality = renewal leverage

Enterprise buyers hold leverage; top clients ~45%, pilots 3–6m

Enterprise buyers hold strong leverage: Impinj's top 10 customers ~45% of 2024 revenue, procurement drives aggressive price concessions and bespoke SLAs. Passive UHF IC ASPs typically $0.01–$0.03 in 2024, so minute price deltas shift multi-million unit deals; pilots take 3–6 months and renewal rates exceed 80%. RAIN Gen2 compatibility (>90% deployments) lowers switching costs, forcing differentiation via software and SLAs.

| Metric | 2024 Value |

|---|---|

| Top-10 revenue share | ~45% |

| Passive UHF IC ASP | $0.01–$0.03 |

| RAIN Gen2 adoption | >90% |

| Pilot length | 3–6 months |

| Enterprise renewal rate | >80% |

Preview Before You Purchase

Impinj Porter's Five Forces Analysis

This preview shows the exact Impinj Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or excerpts. It is the full, professionally formatted document ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.