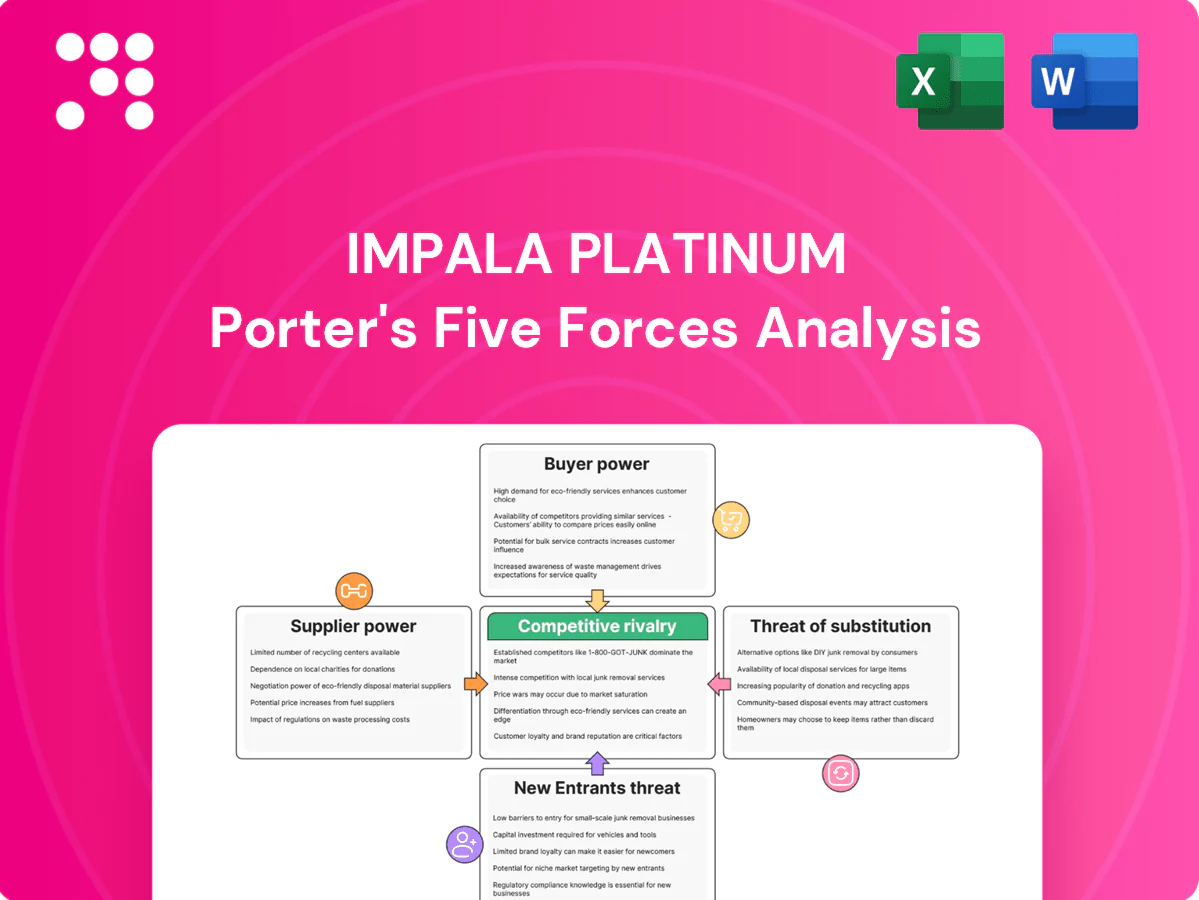

Impala Platinum Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Impala Platinum faces intense competitive rivalry and commodity-driven price swings, while supplier concentration and regulatory risks elevate input and operational pressures; buyer power and substitutes remain moderate but growing with recycling and EV demand shifts. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Impala Platinum’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Concentrated critical inputs

PGM mining depends on concentrated suppliers for electricity, explosives, reagents and OEM heavy equipment; Eskom supplies about 95% of South Africa's power, giving it outsized leverage. Load-shedding and tariff pressure in 2024 tightened margins as energy can account for 20–30% of mining opex. OEMs such as Sandvik and Epiroc dominate underground fleets, creating switching costs via proprietary systems. This concentration raises input costs and downtime risk.

Labor and unions leverage

Skilled underground labor is scarce and heavily unionized in South Africa, giving unions like NUM and AMCU strong leverage; Implats reported around 45,000 employees and contractors in 2024. Wage negotiations and strike risks drive material bargaining power, raising retention premiums and safety-related costs that pressurize unit costs and can sharply reduce output.

Energy and water dependence

Continuous mining, smelting and refining at Implats require high baseload power and significant water; reliance on Eskom as the primary grid supplier remained critical through 2024 as loadshedding persisted. Supply interruptions in 2024 forced deployment of costly diesel and curtailed furnace schedules, raising unit costs. Tighter water licensing and scarcity in key regions increased compliance and abstraction charges, giving suppliers and municipalities greater negotiating leverage over service terms.

Technical services and consumables

Specialist services for shafts, ventilation, geology and assay are hard to substitute, and chemical reagents/catalysts for PGM refining have a concentrated supplier base, often yielding long qualification cycles of 12–24 months and tight quality controls that lock in vendors. These factors raise switching costs and give suppliers measurable influence over pricing and delivery risk, increasing procurement vulnerability for Impala Platinum.

- Concentrated vendors for key reagents

- Qualification cycles commonly 12–24 months

- High switching costs from technical lock-in

Mitigants via integration and scale

In 2024 Implats’ in-house smelting and refining capacity, plus a multi-shaft footprint, strengthened countervailing power versus input suppliers; this vertical integration supports internal flexibility and quality control. Volume commitments, vendor development and dual-sourcing reduced single-supplier exposure, while long-term contracts hedged price volatility and ensured continuity. Scale-based bargaining in 2024 enabled renegotiation of terms and recovery of service levels, improving procurement leverage and cost resilience.

- Integration: in-house smelting/refining boosts supply security

- Risk reduction: volume commitments, vendor development, dual-sourcing

- Hedging: long-term contracts mitigate price swings

- Scale: bargaining power reclaims terms and service levels

Supply squeeze: 95% grid reliance, energy 20-30% opex

Suppliers hold significant leverage: Eskom provided ~95% of SA power in 2024 and energy is 20–30% of mining opex, raising cost and interruption risk. OEMs and reagent vendors are concentrated with 12–24 month qualification cycles and high switching costs. Implats' vertical integration and long-term contracts partially offset supplier power but exposure remains material.

| Metric | 2024 |

|---|---|

| Eskom share of grid | ≈95% |

| Energy share of opex | 20–30% |

| Employees & contractors | ≈45,000 |

| Qualification cycle | 12–24 months |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Impala Platinum, uncovering competitive rivalry, supplier and buyer power, entry barriers, substitutes and regulatory threats to pricing and profitability, with strategic commentary and editable insights for reports, investor materials or internal strategy decks.

A clear, one-sheet Porter's Five Forces summary for Impala Platinum—perfect for quick decision-making and boardroom use, with customizable pressure levels to reflect commodity cycles, regulation changes, or new entrants.

Customers Bargaining Power

Few large industrial buyers

Autocatalyst fabricators and OEM-linked firms account for roughly 45% of PGM demand, and their scale plus tight technical specifications enable hard price negotiations. Consolidated buying—top 10 automakers produce about 40% of global vehicle output (~82 million vehicles in 2024)—amplifies volume leverage and pressures premiums and contract terms.

Global pricing benchmarks

Spot and benchmark prices — 2024 averages near platinum 1,050 USD/oz, palladium ~1,250 USD/oz and rhodium volatile with intrayear spikes above 10,000 USD/oz — constrain bilateral pricing and limit deep discounts. Transparent LBMA-style markets curb buyer-negotiated markdowns, but off-take terms, payment timing and penalty clauses remain negotiable. Basket pricing exposes Implats to buyer mix optimization and margin dilution if purchasers favor higher-value metals in settlements.

Substitution within PGMs

OEMs can redesign catalysts to favor cheaper PGMs, enabling a platinum-for-palladium swing that shifts demand and bargaining power across cycles; the auto sector represented about 40% of PGM demand in 2024. Engineers also thrift loadings—reducing PGM intensity by as much as 10–15% on some platforms—giving buyers leverage to blunt supplier pricing power and compress margins for producers like Impala Platinum.

Quality, reliability, and ESG

Automotive and industrial customers demand consistent purity, on-time delivery and full traceability; failures can trigger penalties or immediate re-sourcing, giving buyers leverage via performance clauses. Supplier ESG credentials now shape sourcing decisions, reflected in Implats 2024 Sustainable Development Report and tighter OEM contracts. This raises the bar for suppliers and increases buyer negotiating power.

- purity, delivery, traceability

- ESG credentials matter (Implats 2024 report)

- penalties/re-sourcing elevate buyer leverage

Long-term contracts as a buffer

Multi-year off-takes stabilise volumes and align product specifications for Impala Platinum, with take-or-pay clauses and formula pricing materially reducing mutual exposure to spot volatility, though large renegotiations have produced major price swings in recent years. Contract structures therefore dampen but do not eliminate buyer bargaining power.

- Multi-year offtakes: volume/spec alignment

- Take-or-pay & formula pricing: lower spot exposure

- Renegotiations: persistent price swing risk

- Net effect: partial mitigation of buyer power

Top10 OEMs (≈82m) & cat fabs (~45% PGM) squeeze premiums, Pt ≈1,050

Large OEMs (top 10 ≈82m vehicles in 2024) and autocatalyst fabricators (~45% PGM demand) exert strong volume and technical-spec leverage, pressuring premiums and terms. 2024 avg prices — Pt ≈1,050 USD/oz, Pd ≈1,250 USD/oz, Rh volatile >10,000 USD/oz — cap deep discounts; multi-year offtakes and formula pricing partly blunt but do not remove buyer power. ESG, purity and traceability clauses increase re‑sourcing risk for Implats.

| Metric | 2024 Value |

|---|---|

| Auto share of PGM demand | ≈40–45% |

| Top10 auto output | ≈82m vehicles |

| Pt/Pd avg prices | Pt 1,050 / Pd 1,250 USD/oz |

What You See Is What You Get

Impala Platinum Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Impala Platinum you'll receive after purchase—no placeholders, no samples. It delivers a comprehensive assessment of competitive rivalry, supplier and buyer power, and threats of entry and substitutes, plus strategic implications. The file is fully formatted and available for immediate download upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Impala Platinum faces intense competitive rivalry and commodity-driven price swings, while supplier concentration and regulatory risks elevate input and operational pressures; buyer power and substitutes remain moderate but growing with recycling and EV demand shifts. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Impala Platinum’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Concentrated critical inputs

PGM mining depends on concentrated suppliers for electricity, explosives, reagents and OEM heavy equipment; Eskom supplies about 95% of South Africa's power, giving it outsized leverage. Load-shedding and tariff pressure in 2024 tightened margins as energy can account for 20–30% of mining opex. OEMs such as Sandvik and Epiroc dominate underground fleets, creating switching costs via proprietary systems. This concentration raises input costs and downtime risk.

Labor and unions leverage

Skilled underground labor is scarce and heavily unionized in South Africa, giving unions like NUM and AMCU strong leverage; Implats reported around 45,000 employees and contractors in 2024. Wage negotiations and strike risks drive material bargaining power, raising retention premiums and safety-related costs that pressurize unit costs and can sharply reduce output.

Energy and water dependence

Continuous mining, smelting and refining at Implats require high baseload power and significant water; reliance on Eskom as the primary grid supplier remained critical through 2024 as loadshedding persisted. Supply interruptions in 2024 forced deployment of costly diesel and curtailed furnace schedules, raising unit costs. Tighter water licensing and scarcity in key regions increased compliance and abstraction charges, giving suppliers and municipalities greater negotiating leverage over service terms.

Technical services and consumables

Specialist services for shafts, ventilation, geology and assay are hard to substitute, and chemical reagents/catalysts for PGM refining have a concentrated supplier base, often yielding long qualification cycles of 12–24 months and tight quality controls that lock in vendors. These factors raise switching costs and give suppliers measurable influence over pricing and delivery risk, increasing procurement vulnerability for Impala Platinum.

- Concentrated vendors for key reagents

- Qualification cycles commonly 12–24 months

- High switching costs from technical lock-in

Mitigants via integration and scale

In 2024 Implats’ in-house smelting and refining capacity, plus a multi-shaft footprint, strengthened countervailing power versus input suppliers; this vertical integration supports internal flexibility and quality control. Volume commitments, vendor development and dual-sourcing reduced single-supplier exposure, while long-term contracts hedged price volatility and ensured continuity. Scale-based bargaining in 2024 enabled renegotiation of terms and recovery of service levels, improving procurement leverage and cost resilience.

- Integration: in-house smelting/refining boosts supply security

- Risk reduction: volume commitments, vendor development, dual-sourcing

- Hedging: long-term contracts mitigate price swings

- Scale: bargaining power reclaims terms and service levels

Supply squeeze: 95% grid reliance, energy 20-30% opex

Suppliers hold significant leverage: Eskom provided ~95% of SA power in 2024 and energy is 20–30% of mining opex, raising cost and interruption risk. OEMs and reagent vendors are concentrated with 12–24 month qualification cycles and high switching costs. Implats' vertical integration and long-term contracts partially offset supplier power but exposure remains material.

| Metric | 2024 |

|---|---|

| Eskom share of grid | ≈95% |

| Energy share of opex | 20–30% |

| Employees & contractors | ≈45,000 |

| Qualification cycle | 12–24 months |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Impala Platinum, uncovering competitive rivalry, supplier and buyer power, entry barriers, substitutes and regulatory threats to pricing and profitability, with strategic commentary and editable insights for reports, investor materials or internal strategy decks.

A clear, one-sheet Porter's Five Forces summary for Impala Platinum—perfect for quick decision-making and boardroom use, with customizable pressure levels to reflect commodity cycles, regulation changes, or new entrants.

Customers Bargaining Power

Few large industrial buyers

Autocatalyst fabricators and OEM-linked firms account for roughly 45% of PGM demand, and their scale plus tight technical specifications enable hard price negotiations. Consolidated buying—top 10 automakers produce about 40% of global vehicle output (~82 million vehicles in 2024)—amplifies volume leverage and pressures premiums and contract terms.

Global pricing benchmarks

Spot and benchmark prices — 2024 averages near platinum 1,050 USD/oz, palladium ~1,250 USD/oz and rhodium volatile with intrayear spikes above 10,000 USD/oz — constrain bilateral pricing and limit deep discounts. Transparent LBMA-style markets curb buyer-negotiated markdowns, but off-take terms, payment timing and penalty clauses remain negotiable. Basket pricing exposes Implats to buyer mix optimization and margin dilution if purchasers favor higher-value metals in settlements.

Substitution within PGMs

OEMs can redesign catalysts to favor cheaper PGMs, enabling a platinum-for-palladium swing that shifts demand and bargaining power across cycles; the auto sector represented about 40% of PGM demand in 2024. Engineers also thrift loadings—reducing PGM intensity by as much as 10–15% on some platforms—giving buyers leverage to blunt supplier pricing power and compress margins for producers like Impala Platinum.

Quality, reliability, and ESG

Automotive and industrial customers demand consistent purity, on-time delivery and full traceability; failures can trigger penalties or immediate re-sourcing, giving buyers leverage via performance clauses. Supplier ESG credentials now shape sourcing decisions, reflected in Implats 2024 Sustainable Development Report and tighter OEM contracts. This raises the bar for suppliers and increases buyer negotiating power.

- purity, delivery, traceability

- ESG credentials matter (Implats 2024 report)

- penalties/re-sourcing elevate buyer leverage

Long-term contracts as a buffer

Multi-year off-takes stabilise volumes and align product specifications for Impala Platinum, with take-or-pay clauses and formula pricing materially reducing mutual exposure to spot volatility, though large renegotiations have produced major price swings in recent years. Contract structures therefore dampen but do not eliminate buyer bargaining power.

- Multi-year offtakes: volume/spec alignment

- Take-or-pay & formula pricing: lower spot exposure

- Renegotiations: persistent price swing risk

- Net effect: partial mitigation of buyer power

Top10 OEMs (≈82m) & cat fabs (~45% PGM) squeeze premiums, Pt ≈1,050

Large OEMs (top 10 ≈82m vehicles in 2024) and autocatalyst fabricators (~45% PGM demand) exert strong volume and technical-spec leverage, pressuring premiums and terms. 2024 avg prices — Pt ≈1,050 USD/oz, Pd ≈1,250 USD/oz, Rh volatile >10,000 USD/oz — cap deep discounts; multi-year offtakes and formula pricing partly blunt but do not remove buyer power. ESG, purity and traceability clauses increase re‑sourcing risk for Implats.

| Metric | 2024 Value |

|---|---|

| Auto share of PGM demand | ≈40–45% |

| Top10 auto output | ≈82m vehicles |

| Pt/Pd avg prices | Pt 1,050 / Pd 1,250 USD/oz |

What You See Is What You Get

Impala Platinum Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Impala Platinum you'll receive after purchase—no placeholders, no samples. It delivers a comprehensive assessment of competitive rivalry, supplier and buyer power, and threats of entry and substitutes, plus strategic implications. The file is fully formatted and available for immediate download upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Impala Platinum faces intense competitive rivalry and commodity-driven price swings, while supplier concentration and regulatory risks elevate input and operational pressures; buyer power and substitutes remain moderate but growing with recycling and EV demand shifts. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Impala Platinum’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Concentrated critical inputs

PGM mining depends on concentrated suppliers for electricity, explosives, reagents and OEM heavy equipment; Eskom supplies about 95% of South Africa's power, giving it outsized leverage. Load-shedding and tariff pressure in 2024 tightened margins as energy can account for 20–30% of mining opex. OEMs such as Sandvik and Epiroc dominate underground fleets, creating switching costs via proprietary systems. This concentration raises input costs and downtime risk.

Labor and unions leverage

Skilled underground labor is scarce and heavily unionized in South Africa, giving unions like NUM and AMCU strong leverage; Implats reported around 45,000 employees and contractors in 2024. Wage negotiations and strike risks drive material bargaining power, raising retention premiums and safety-related costs that pressurize unit costs and can sharply reduce output.

Energy and water dependence

Continuous mining, smelting and refining at Implats require high baseload power and significant water; reliance on Eskom as the primary grid supplier remained critical through 2024 as loadshedding persisted. Supply interruptions in 2024 forced deployment of costly diesel and curtailed furnace schedules, raising unit costs. Tighter water licensing and scarcity in key regions increased compliance and abstraction charges, giving suppliers and municipalities greater negotiating leverage over service terms.

Technical services and consumables

Specialist services for shafts, ventilation, geology and assay are hard to substitute, and chemical reagents/catalysts for PGM refining have a concentrated supplier base, often yielding long qualification cycles of 12–24 months and tight quality controls that lock in vendors. These factors raise switching costs and give suppliers measurable influence over pricing and delivery risk, increasing procurement vulnerability for Impala Platinum.

- Concentrated vendors for key reagents

- Qualification cycles commonly 12–24 months

- High switching costs from technical lock-in

Mitigants via integration and scale

In 2024 Implats’ in-house smelting and refining capacity, plus a multi-shaft footprint, strengthened countervailing power versus input suppliers; this vertical integration supports internal flexibility and quality control. Volume commitments, vendor development and dual-sourcing reduced single-supplier exposure, while long-term contracts hedged price volatility and ensured continuity. Scale-based bargaining in 2024 enabled renegotiation of terms and recovery of service levels, improving procurement leverage and cost resilience.

- Integration: in-house smelting/refining boosts supply security

- Risk reduction: volume commitments, vendor development, dual-sourcing

- Hedging: long-term contracts mitigate price swings

- Scale: bargaining power reclaims terms and service levels

Supply squeeze: 95% grid reliance, energy 20-30% opex

Suppliers hold significant leverage: Eskom provided ~95% of SA power in 2024 and energy is 20–30% of mining opex, raising cost and interruption risk. OEMs and reagent vendors are concentrated with 12–24 month qualification cycles and high switching costs. Implats' vertical integration and long-term contracts partially offset supplier power but exposure remains material.

| Metric | 2024 |

|---|---|

| Eskom share of grid | ≈95% |

| Energy share of opex | 20–30% |

| Employees & contractors | ≈45,000 |

| Qualification cycle | 12–24 months |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Impala Platinum, uncovering competitive rivalry, supplier and buyer power, entry barriers, substitutes and regulatory threats to pricing and profitability, with strategic commentary and editable insights for reports, investor materials or internal strategy decks.

A clear, one-sheet Porter's Five Forces summary for Impala Platinum—perfect for quick decision-making and boardroom use, with customizable pressure levels to reflect commodity cycles, regulation changes, or new entrants.

Customers Bargaining Power

Few large industrial buyers

Autocatalyst fabricators and OEM-linked firms account for roughly 45% of PGM demand, and their scale plus tight technical specifications enable hard price negotiations. Consolidated buying—top 10 automakers produce about 40% of global vehicle output (~82 million vehicles in 2024)—amplifies volume leverage and pressures premiums and contract terms.

Global pricing benchmarks

Spot and benchmark prices — 2024 averages near platinum 1,050 USD/oz, palladium ~1,250 USD/oz and rhodium volatile with intrayear spikes above 10,000 USD/oz — constrain bilateral pricing and limit deep discounts. Transparent LBMA-style markets curb buyer-negotiated markdowns, but off-take terms, payment timing and penalty clauses remain negotiable. Basket pricing exposes Implats to buyer mix optimization and margin dilution if purchasers favor higher-value metals in settlements.

Substitution within PGMs

OEMs can redesign catalysts to favor cheaper PGMs, enabling a platinum-for-palladium swing that shifts demand and bargaining power across cycles; the auto sector represented about 40% of PGM demand in 2024. Engineers also thrift loadings—reducing PGM intensity by as much as 10–15% on some platforms—giving buyers leverage to blunt supplier pricing power and compress margins for producers like Impala Platinum.

Quality, reliability, and ESG

Automotive and industrial customers demand consistent purity, on-time delivery and full traceability; failures can trigger penalties or immediate re-sourcing, giving buyers leverage via performance clauses. Supplier ESG credentials now shape sourcing decisions, reflected in Implats 2024 Sustainable Development Report and tighter OEM contracts. This raises the bar for suppliers and increases buyer negotiating power.

- purity, delivery, traceability

- ESG credentials matter (Implats 2024 report)

- penalties/re-sourcing elevate buyer leverage

Long-term contracts as a buffer

Multi-year off-takes stabilise volumes and align product specifications for Impala Platinum, with take-or-pay clauses and formula pricing materially reducing mutual exposure to spot volatility, though large renegotiations have produced major price swings in recent years. Contract structures therefore dampen but do not eliminate buyer bargaining power.

- Multi-year offtakes: volume/spec alignment

- Take-or-pay & formula pricing: lower spot exposure

- Renegotiations: persistent price swing risk

- Net effect: partial mitigation of buyer power

Top10 OEMs (≈82m) & cat fabs (~45% PGM) squeeze premiums, Pt ≈1,050

Large OEMs (top 10 ≈82m vehicles in 2024) and autocatalyst fabricators (~45% PGM demand) exert strong volume and technical-spec leverage, pressuring premiums and terms. 2024 avg prices — Pt ≈1,050 USD/oz, Pd ≈1,250 USD/oz, Rh volatile >10,000 USD/oz — cap deep discounts; multi-year offtakes and formula pricing partly blunt but do not remove buyer power. ESG, purity and traceability clauses increase re‑sourcing risk for Implats.

| Metric | 2024 Value |

|---|---|

| Auto share of PGM demand | ≈40–45% |

| Top10 auto output | ≈82m vehicles |

| Pt/Pd avg prices | Pt 1,050 / Pd 1,250 USD/oz |

What You See Is What You Get

Impala Platinum Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Impala Platinum you'll receive after purchase—no placeholders, no samples. It delivers a comprehensive assessment of competitive rivalry, supplier and buyer power, and threats of entry and substitutes, plus strategic implications. The file is fully formatted and available for immediate download upon payment.