Infinity Natural Resources Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

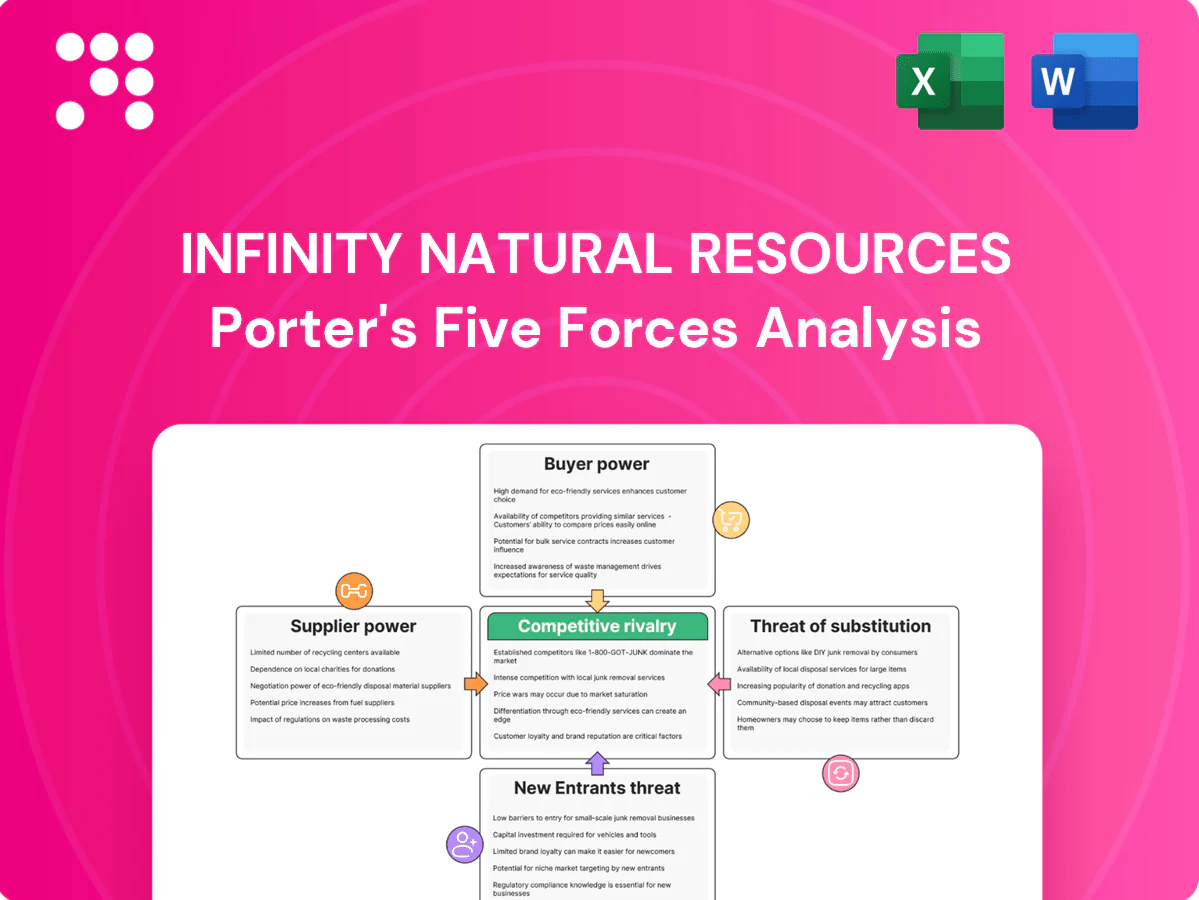

Infinity Natural Resources’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, entrant threats, and substitution risks shaping profitability. This brief teases strategic implications and gaps that matter to investors and executives. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated oilfield services and rigs

Drilling, completion and rig providers are concentrated, giving suppliers pricing leverage in busy cycles; Baker Hughes reported the U.S. rig count reached about 687 by Dec 2024, supporting stronger service demand. For an Appalachian unconventional operator, specialized frac crews and horizontal rigs are critical and not easily substitutable, driving double‑digit day‑rate inflation in upcycles. During upcycles service costs can spike and compress margins; in downturns capacity loosens and discounts reappear.

Proppant, water, and chemicals logistics

Frac sand, water sourcing/disposal, and chemicals are critical inputs with regional logistics bottlenecks; in 2024 spot frac sand traded broadly between 40–80 USD/ton and water disposal ranged roughly 0.50–4.00 USD/bbl, raising delivered costs when trucking is constrained. Local supply or truck shortages can add 10–25% to delivered cost and delay completions. Long-term contracts and in-basin sand supply reduce price volatility but lock operators into volume commitments. Tight environmental rules on water handling (permits, disposal limits) further strengthen supplier leverage.

Midstream gathering and processing dependency

Appalachian production (Marcellus+Utica ~35 Bcf/d in 2024 per EIA) depends on a limited set of gatherers/processors, giving midstream firms strong leverage; take‑or‑pay and fixed‑fee contracts often comprise a majority of near‑term transport costs, locking expenses regardless of commodity prices. Capacity tightness or outages sharply raise midstream bargaining power, while securing optionality across two or more systems can partially rebalance negotiations.

Landowners and lease terms

Landowner and broker leverage is high for Infinity Natural Resources where access to core-tier acreage drives value; royalty rates commonly range 12.5–25% and 2024 lease bonuses in core U.S. basins reached several thousand dollars per acre, squeezing project IRRs. Stringent surface-use and environmental clauses and competitive leasing rounds increase lessor power, while early leasing programs and strong landowner relations help moderate cost escalation.

- Royalty range: 12.5–25%

- 2024 bonuses: several thousand $/acre in core tiers

- Mitigation: early leasing, broker relationships, structured clauses

Technology and data vendors

Advanced drilling, geosteering and subsurface analytics are core to Infinity’s efficiency drive; specialized software, telemetry and proprietary tools create measurable switching friction and implementation timelines of 6–12 months. In 2024 more than 60% of upstream firms increased digital budgets, enabling vendors to bundle services and raise dependency, widening negotiating asymmetry.

- Key frictions: proprietary formats, 6–12 month integrations

- Risk: vendor bundling increases dependence

- Mitigation: standard APIs, dual-sourcing

Suppliers tighten leverage: rig count, sand & water costs, midstream control

Suppliers hold meaningful leverage: U.S. rig count ~687 (Dec 2024) tightens service pricing; frac sand 40–80 USD/ton and water disposal 0.50–4.00 USD/bbl raise completion costs; Appalachian midstream (Marcellus+Utica ~35 Bcf/d in 2024) and royalty rates 12.5–25%/bonuses several thousand USD/acre concentrate bargaining power, partially mitigated by long‑term contracts, dual‑sourcing and early leasing.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Service rigs | Rig count 687 | Higher day rates |

| Frac sand | 40–80 USD/ton | Completion cost volatility |

| Midstream | 35 Bcf/d | Transport leverage |

What is included in the product

Tailored Porter's Five Forces analysis for Infinity Natural Resources that uncovers key competitive drivers, supplier and buyer power, substitutes and entry risks, and highlights disruptive threats and barriers protecting incumbency to inform pricing, strategic positioning, and investor decision-making.

A one-sheet Porter's Five Forces summary for Infinity Natural Resources that clarifies competitive pressure at a glance and exports cleanly into pitch decks; customize force levels, swap in your data, and visualize strategic risk instantly with an integrated spider chart.

Customers Bargaining Power

Concentrated marketers and refiners

Sales often channel to a concentrated pool of gas marketers, utilities and refiners; in the US the top four refiners held roughly 55% of refining capacity in 2024, giving large offtakers significant leverage. These buyers press pricing and contract terms, especially during regional oversupply when basis differentials can widen. Creditworthy offtakers demand strict quality specs and delivery flexibility. Diversifying counterparties reduces single-buyer concentration risk.

Commodity benchmark pricing

Oil and gas are priced off benchmarks (WTI, Henry Hub), with 2024 benchmark ranges roughly WTI $70–90/bbl and Henry Hub $2–5/MMBtu, leaving limited producer pricing discretion. Buyers gain from transparent pricing and deep NYMEX liquidity, enabling broad hedging. Appalachian basis differentials often subtract $1–3/MMBtu from realized prices, further favoring buyers. Hedging smooths cash flows but cannot remove benchmark-driven buyer power.

High product substitutability for buyers

Hydrocarbons from different producers are largely fungible once specs are met, and buyers can switch among suppliers with minimal switching costs; in 2024 global crude production averaged about 82.5 million barrels per day, keeping supply options broad. This fosters strong buyer leverage in balanced or oversupplied markets where inventories rose in parts of 2024. Differentiation through reliable delivery schedules and spare capacity access can modestly offset buyer power.

Contractual terms and penalties

Contractual terms like take-or-pay, firm transport and tight delivery windows shift volumetric and price risk onto producers; 2024 industry surveys show over 50% of long-term gas contracts retain take-or-pay exposure. Buyers increasingly secure penalties for non-delivery or off-spec volumes while term contracts stabilize cash flows but often embed 5–15% effective discounts. Flexibility in nominations and multi-point delivery materially strengthens a producer’s bargaining stance.

- Take-or-pay >50% in 2024 long-term contracts

- Penalty clauses common; discounts 5–15%

- Flexible nominations/multi-point delivery = higher producer leverage

ESG and certification pressures

Some buyers now prefer responsibly sourced gas and lower-emission barrels; the 2024 rollout of Europe’s CSRD has intensified demand for verified ESG credentials and methane monitoring, raising producers’ compliance costs while buyers with ESG mandates steer procurement toward certified suppliers.

- Certification can unlock price premiums and cut buyer leverage

- CSRD 2024 raises reporting expectations

- Global sustainable assets were $35.3tn (2020) showing market ESG weight

Concentrated buyers wield pricing leverage; take-or-pay shifts volume risk to producers

Concentrated offtakers (top-4 refiners ~55% US capacity in 2024) and fungible benchmarks (WTI $70–90/bbl; Henry Hub $2–5/MMBtu in 2024) give buyers strong pricing leverage. Take-or-pay exposure >50% of long-term gas contracts shifts volume risk to producers; Appalachian basis -$1–3/MMBtu further weakens realized prices. ESG demand (CSRD 2024) nudges procurement toward certified suppliers, slightly reducing buyer power.

| Metric | 2024 Value |

|---|---|

| Top-4 refiners (US) | ~55% capacity |

| WTI | $70–90/bbl |

| Henry Hub | $2–5/MMBtu |

| Take-or-pay contracts | >50% |

| Appalachian basis | -$1–3/MMBtu |

What You See Is What You Get

Infinity Natural Resources Porter's Five Forces Analysis

This preview shows the exact Infinity Natural Resources Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable.

Go Beyond the Preview—Access the Full Strategic Report

Infinity Natural Resources’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, entrant threats, and substitution risks shaping profitability. This brief teases strategic implications and gaps that matter to investors and executives. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated oilfield services and rigs

Drilling, completion and rig providers are concentrated, giving suppliers pricing leverage in busy cycles; Baker Hughes reported the U.S. rig count reached about 687 by Dec 2024, supporting stronger service demand. For an Appalachian unconventional operator, specialized frac crews and horizontal rigs are critical and not easily substitutable, driving double‑digit day‑rate inflation in upcycles. During upcycles service costs can spike and compress margins; in downturns capacity loosens and discounts reappear.

Proppant, water, and chemicals logistics

Frac sand, water sourcing/disposal, and chemicals are critical inputs with regional logistics bottlenecks; in 2024 spot frac sand traded broadly between 40–80 USD/ton and water disposal ranged roughly 0.50–4.00 USD/bbl, raising delivered costs when trucking is constrained. Local supply or truck shortages can add 10–25% to delivered cost and delay completions. Long-term contracts and in-basin sand supply reduce price volatility but lock operators into volume commitments. Tight environmental rules on water handling (permits, disposal limits) further strengthen supplier leverage.

Midstream gathering and processing dependency

Appalachian production (Marcellus+Utica ~35 Bcf/d in 2024 per EIA) depends on a limited set of gatherers/processors, giving midstream firms strong leverage; take‑or‑pay and fixed‑fee contracts often comprise a majority of near‑term transport costs, locking expenses regardless of commodity prices. Capacity tightness or outages sharply raise midstream bargaining power, while securing optionality across two or more systems can partially rebalance negotiations.

Landowners and lease terms

Landowner and broker leverage is high for Infinity Natural Resources where access to core-tier acreage drives value; royalty rates commonly range 12.5–25% and 2024 lease bonuses in core U.S. basins reached several thousand dollars per acre, squeezing project IRRs. Stringent surface-use and environmental clauses and competitive leasing rounds increase lessor power, while early leasing programs and strong landowner relations help moderate cost escalation.

- Royalty range: 12.5–25%

- 2024 bonuses: several thousand $/acre in core tiers

- Mitigation: early leasing, broker relationships, structured clauses

Technology and data vendors

Advanced drilling, geosteering and subsurface analytics are core to Infinity’s efficiency drive; specialized software, telemetry and proprietary tools create measurable switching friction and implementation timelines of 6–12 months. In 2024 more than 60% of upstream firms increased digital budgets, enabling vendors to bundle services and raise dependency, widening negotiating asymmetry.

- Key frictions: proprietary formats, 6–12 month integrations

- Risk: vendor bundling increases dependence

- Mitigation: standard APIs, dual-sourcing

Suppliers tighten leverage: rig count, sand & water costs, midstream control

Suppliers hold meaningful leverage: U.S. rig count ~687 (Dec 2024) tightens service pricing; frac sand 40–80 USD/ton and water disposal 0.50–4.00 USD/bbl raise completion costs; Appalachian midstream (Marcellus+Utica ~35 Bcf/d in 2024) and royalty rates 12.5–25%/bonuses several thousand USD/acre concentrate bargaining power, partially mitigated by long‑term contracts, dual‑sourcing and early leasing.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Service rigs | Rig count 687 | Higher day rates |

| Frac sand | 40–80 USD/ton | Completion cost volatility |

| Midstream | 35 Bcf/d | Transport leverage |

What is included in the product

Tailored Porter's Five Forces analysis for Infinity Natural Resources that uncovers key competitive drivers, supplier and buyer power, substitutes and entry risks, and highlights disruptive threats and barriers protecting incumbency to inform pricing, strategic positioning, and investor decision-making.

A one-sheet Porter's Five Forces summary for Infinity Natural Resources that clarifies competitive pressure at a glance and exports cleanly into pitch decks; customize force levels, swap in your data, and visualize strategic risk instantly with an integrated spider chart.

Customers Bargaining Power

Concentrated marketers and refiners

Sales often channel to a concentrated pool of gas marketers, utilities and refiners; in the US the top four refiners held roughly 55% of refining capacity in 2024, giving large offtakers significant leverage. These buyers press pricing and contract terms, especially during regional oversupply when basis differentials can widen. Creditworthy offtakers demand strict quality specs and delivery flexibility. Diversifying counterparties reduces single-buyer concentration risk.

Commodity benchmark pricing

Oil and gas are priced off benchmarks (WTI, Henry Hub), with 2024 benchmark ranges roughly WTI $70–90/bbl and Henry Hub $2–5/MMBtu, leaving limited producer pricing discretion. Buyers gain from transparent pricing and deep NYMEX liquidity, enabling broad hedging. Appalachian basis differentials often subtract $1–3/MMBtu from realized prices, further favoring buyers. Hedging smooths cash flows but cannot remove benchmark-driven buyer power.

High product substitutability for buyers

Hydrocarbons from different producers are largely fungible once specs are met, and buyers can switch among suppliers with minimal switching costs; in 2024 global crude production averaged about 82.5 million barrels per day, keeping supply options broad. This fosters strong buyer leverage in balanced or oversupplied markets where inventories rose in parts of 2024. Differentiation through reliable delivery schedules and spare capacity access can modestly offset buyer power.

Contractual terms and penalties

Contractual terms like take-or-pay, firm transport and tight delivery windows shift volumetric and price risk onto producers; 2024 industry surveys show over 50% of long-term gas contracts retain take-or-pay exposure. Buyers increasingly secure penalties for non-delivery or off-spec volumes while term contracts stabilize cash flows but often embed 5–15% effective discounts. Flexibility in nominations and multi-point delivery materially strengthens a producer’s bargaining stance.

- Take-or-pay >50% in 2024 long-term contracts

- Penalty clauses common; discounts 5–15%

- Flexible nominations/multi-point delivery = higher producer leverage

ESG and certification pressures

Some buyers now prefer responsibly sourced gas and lower-emission barrels; the 2024 rollout of Europe’s CSRD has intensified demand for verified ESG credentials and methane monitoring, raising producers’ compliance costs while buyers with ESG mandates steer procurement toward certified suppliers.

- Certification can unlock price premiums and cut buyer leverage

- CSRD 2024 raises reporting expectations

- Global sustainable assets were $35.3tn (2020) showing market ESG weight

Concentrated buyers wield pricing leverage; take-or-pay shifts volume risk to producers

Concentrated offtakers (top-4 refiners ~55% US capacity in 2024) and fungible benchmarks (WTI $70–90/bbl; Henry Hub $2–5/MMBtu in 2024) give buyers strong pricing leverage. Take-or-pay exposure >50% of long-term gas contracts shifts volume risk to producers; Appalachian basis -$1–3/MMBtu further weakens realized prices. ESG demand (CSRD 2024) nudges procurement toward certified suppliers, slightly reducing buyer power.

| Metric | 2024 Value |

|---|---|

| Top-4 refiners (US) | ~55% capacity |

| WTI | $70–90/bbl |

| Henry Hub | $2–5/MMBtu |

| Take-or-pay contracts | >50% |

| Appalachian basis | -$1–3/MMBtu |

What You See Is What You Get

Infinity Natural Resources Porter's Five Forces Analysis

This preview shows the exact Infinity Natural Resources Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Infinity Natural Resources’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, entrant threats, and substitution risks shaping profitability. This brief teases strategic implications and gaps that matter to investors and executives. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated oilfield services and rigs

Drilling, completion and rig providers are concentrated, giving suppliers pricing leverage in busy cycles; Baker Hughes reported the U.S. rig count reached about 687 by Dec 2024, supporting stronger service demand. For an Appalachian unconventional operator, specialized frac crews and horizontal rigs are critical and not easily substitutable, driving double‑digit day‑rate inflation in upcycles. During upcycles service costs can spike and compress margins; in downturns capacity loosens and discounts reappear.

Proppant, water, and chemicals logistics

Frac sand, water sourcing/disposal, and chemicals are critical inputs with regional logistics bottlenecks; in 2024 spot frac sand traded broadly between 40–80 USD/ton and water disposal ranged roughly 0.50–4.00 USD/bbl, raising delivered costs when trucking is constrained. Local supply or truck shortages can add 10–25% to delivered cost and delay completions. Long-term contracts and in-basin sand supply reduce price volatility but lock operators into volume commitments. Tight environmental rules on water handling (permits, disposal limits) further strengthen supplier leverage.

Midstream gathering and processing dependency

Appalachian production (Marcellus+Utica ~35 Bcf/d in 2024 per EIA) depends on a limited set of gatherers/processors, giving midstream firms strong leverage; take‑or‑pay and fixed‑fee contracts often comprise a majority of near‑term transport costs, locking expenses regardless of commodity prices. Capacity tightness or outages sharply raise midstream bargaining power, while securing optionality across two or more systems can partially rebalance negotiations.

Landowners and lease terms

Landowner and broker leverage is high for Infinity Natural Resources where access to core-tier acreage drives value; royalty rates commonly range 12.5–25% and 2024 lease bonuses in core U.S. basins reached several thousand dollars per acre, squeezing project IRRs. Stringent surface-use and environmental clauses and competitive leasing rounds increase lessor power, while early leasing programs and strong landowner relations help moderate cost escalation.

- Royalty range: 12.5–25%

- 2024 bonuses: several thousand $/acre in core tiers

- Mitigation: early leasing, broker relationships, structured clauses

Technology and data vendors

Advanced drilling, geosteering and subsurface analytics are core to Infinity’s efficiency drive; specialized software, telemetry and proprietary tools create measurable switching friction and implementation timelines of 6–12 months. In 2024 more than 60% of upstream firms increased digital budgets, enabling vendors to bundle services and raise dependency, widening negotiating asymmetry.

- Key frictions: proprietary formats, 6–12 month integrations

- Risk: vendor bundling increases dependence

- Mitigation: standard APIs, dual-sourcing

Suppliers tighten leverage: rig count, sand & water costs, midstream control

Suppliers hold meaningful leverage: U.S. rig count ~687 (Dec 2024) tightens service pricing; frac sand 40–80 USD/ton and water disposal 0.50–4.00 USD/bbl raise completion costs; Appalachian midstream (Marcellus+Utica ~35 Bcf/d in 2024) and royalty rates 12.5–25%/bonuses several thousand USD/acre concentrate bargaining power, partially mitigated by long‑term contracts, dual‑sourcing and early leasing.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Service rigs | Rig count 687 | Higher day rates |

| Frac sand | 40–80 USD/ton | Completion cost volatility |

| Midstream | 35 Bcf/d | Transport leverage |

What is included in the product

Tailored Porter's Five Forces analysis for Infinity Natural Resources that uncovers key competitive drivers, supplier and buyer power, substitutes and entry risks, and highlights disruptive threats and barriers protecting incumbency to inform pricing, strategic positioning, and investor decision-making.

A one-sheet Porter's Five Forces summary for Infinity Natural Resources that clarifies competitive pressure at a glance and exports cleanly into pitch decks; customize force levels, swap in your data, and visualize strategic risk instantly with an integrated spider chart.

Customers Bargaining Power

Concentrated marketers and refiners

Sales often channel to a concentrated pool of gas marketers, utilities and refiners; in the US the top four refiners held roughly 55% of refining capacity in 2024, giving large offtakers significant leverage. These buyers press pricing and contract terms, especially during regional oversupply when basis differentials can widen. Creditworthy offtakers demand strict quality specs and delivery flexibility. Diversifying counterparties reduces single-buyer concentration risk.

Commodity benchmark pricing

Oil and gas are priced off benchmarks (WTI, Henry Hub), with 2024 benchmark ranges roughly WTI $70–90/bbl and Henry Hub $2–5/MMBtu, leaving limited producer pricing discretion. Buyers gain from transparent pricing and deep NYMEX liquidity, enabling broad hedging. Appalachian basis differentials often subtract $1–3/MMBtu from realized prices, further favoring buyers. Hedging smooths cash flows but cannot remove benchmark-driven buyer power.

High product substitutability for buyers

Hydrocarbons from different producers are largely fungible once specs are met, and buyers can switch among suppliers with minimal switching costs; in 2024 global crude production averaged about 82.5 million barrels per day, keeping supply options broad. This fosters strong buyer leverage in balanced or oversupplied markets where inventories rose in parts of 2024. Differentiation through reliable delivery schedules and spare capacity access can modestly offset buyer power.

Contractual terms and penalties

Contractual terms like take-or-pay, firm transport and tight delivery windows shift volumetric and price risk onto producers; 2024 industry surveys show over 50% of long-term gas contracts retain take-or-pay exposure. Buyers increasingly secure penalties for non-delivery or off-spec volumes while term contracts stabilize cash flows but often embed 5–15% effective discounts. Flexibility in nominations and multi-point delivery materially strengthens a producer’s bargaining stance.

- Take-or-pay >50% in 2024 long-term contracts

- Penalty clauses common; discounts 5–15%

- Flexible nominations/multi-point delivery = higher producer leverage

ESG and certification pressures

Some buyers now prefer responsibly sourced gas and lower-emission barrels; the 2024 rollout of Europe’s CSRD has intensified demand for verified ESG credentials and methane monitoring, raising producers’ compliance costs while buyers with ESG mandates steer procurement toward certified suppliers.

- Certification can unlock price premiums and cut buyer leverage

- CSRD 2024 raises reporting expectations

- Global sustainable assets were $35.3tn (2020) showing market ESG weight

Concentrated buyers wield pricing leverage; take-or-pay shifts volume risk to producers

Concentrated offtakers (top-4 refiners ~55% US capacity in 2024) and fungible benchmarks (WTI $70–90/bbl; Henry Hub $2–5/MMBtu in 2024) give buyers strong pricing leverage. Take-or-pay exposure >50% of long-term gas contracts shifts volume risk to producers; Appalachian basis -$1–3/MMBtu further weakens realized prices. ESG demand (CSRD 2024) nudges procurement toward certified suppliers, slightly reducing buyer power.

| Metric | 2024 Value |

|---|---|

| Top-4 refiners (US) | ~55% capacity |

| WTI | $70–90/bbl |

| Henry Hub | $2–5/MMBtu |

| Take-or-pay contracts | >50% |

| Appalachian basis | -$1–3/MMBtu |

What You See Is What You Get

Infinity Natural Resources Porter's Five Forces Analysis

This preview shows the exact Infinity Natural Resources Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable.