ING Groep Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

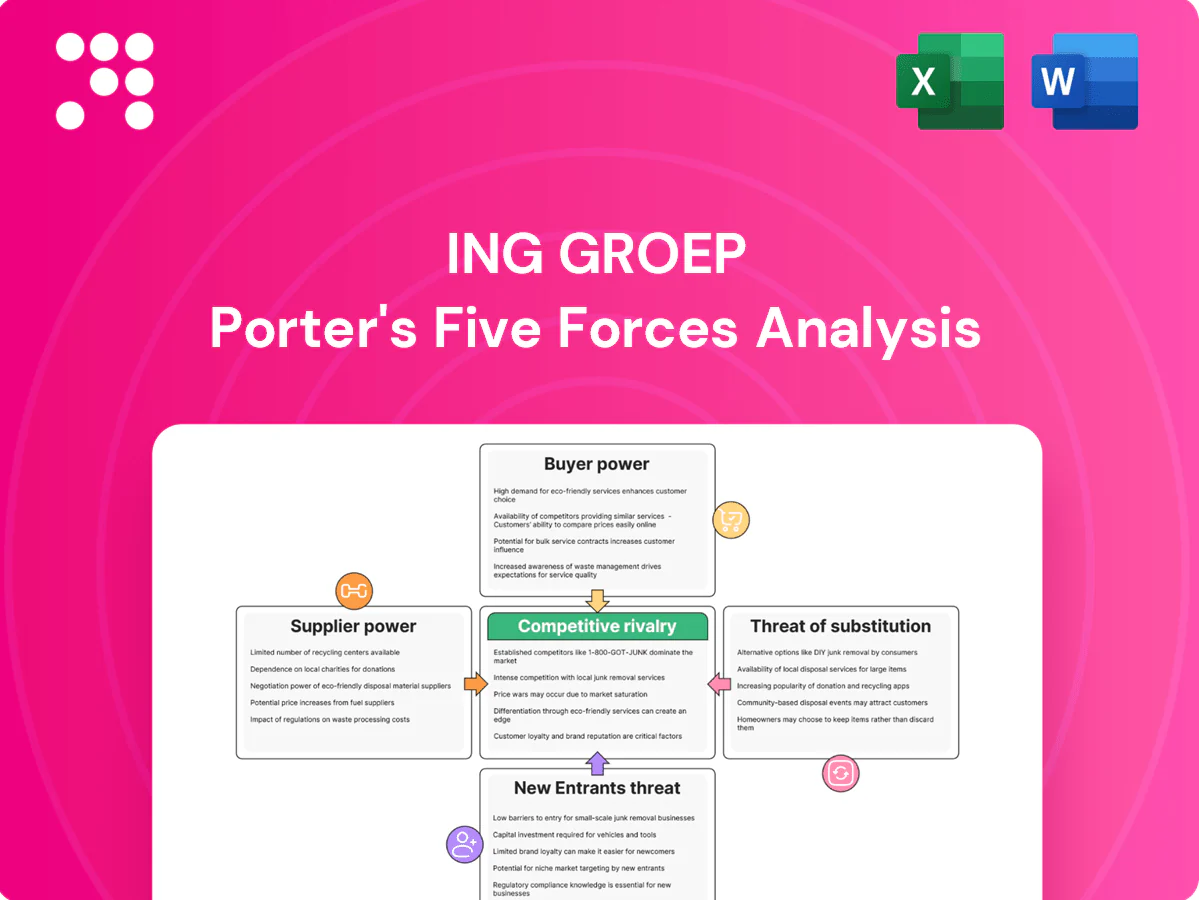

ING Groep faces moderate buyer power, strong regulatory barriers, and mounting fintech substitution that together pressure margins and strategic positioning. This snapshot highlights key competitive levers and risk vectors shaping the bank’s future. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ING Groep’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated wholesale funding sources

ING relies partly on wholesale markets for liquidity, issuing covered bonds and senior debt via EMTN programmes; wholesale funding accounted for roughly one-third of term funding in 2024. Large institutional investors can demand higher spreads in stress, raising funding costs and prompting basis-point widening seen in 2022–24 market episodes. Diversified issuance mitigates single-source risk, while ECB facilities (TLTRO/Deposit Facility) can temper spikes but have eligibility constraints.

Critical technology and cloud vendors

Core banking platforms, cloud providers and cybersecurity vendors are mission-critical and the top three cloud providers hold roughly 66% of the IaaS/PaaS market, amplifying supplier leverage. High switching costs and deep integration complexity raise lock-in and pricing power. ING mitigates this by multi-vendor strategies and selective in-house development to lower dependency. EU rules such as DORA (effective 2025) further shape vendor negotiation and contractual resilience requirements.

Payment networks and rails

Card schemes and cross-border networks set fees and technical standards, and their network effects sustain supplier leverage despite alternatives; SEPA covers 36 countries and ECB TIPS (launched 2018) enables instant settlement. EU regulatory caps on interchange (0.2% for debit, 0.3% for credit) constrain fees materially. Volume-based pricing and co‑brand partnerships can partially offset scheme costs for issuers.

Data, analytics, and credit bureaus

Access to high-quality data from credit bureaus and AML/KYC providers directly impacts ING’s underwriting accuracy and compliance; with ING serving ~37 million customers (2024), enterprise contracts help lower per-unit costs. Leading bureaus can command premium pricing, but open banking and PSD2-driven data aggregation have expanded alternative sources, diluting individual supplier power.

- Scale: enterprise contracts reduce unit cost

- Supplier pricing: premium for top bureaus

- Open banking: increases data sources

Specialized talent and outsourcing partners

Engineering, risk and compliance talent is scarce, driving wage inflation and tight hiring: ING employed about 56,000 staff in 2024, leveraging its global brand but facing local market gaps that raise compensation and contractor spend. Niche KYC remediation and model-validation vendors command premium fees, while automation and regional centres of excellence gradually lower supplier dependence.

- Wage pressure: high demand for engineers/compliance

- Premium vendors: costly KYC/model validation

- Brand helps recruitment, local variance persists

- Automation/Centres of excellence reduce reliance

Suppliers moderate: 33% funding, 66% cloud, 56k staff

Suppliers exert moderate power: wholesale investors funded ~33% of ING term funding in 2024, raising spread risk in stress. Top three cloud providers hold ~66% IaaS/PaaS, creating supplier leverage despite multi‑vendor use. ING served ~37m customers (2024) so bureaus and card schemes retain pricing power. Staff 56,000 (2024) keeps talent suppliers strong.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Wholesale funding | 33% term funding | Spread risk |

| Cloud providers | 66% IaaS/PaaS | Lock‑in |

| Customers/bureaus | 37m | Data costs |

| Labor | 56,000 staff | Wage pressure |

What is included in the product

Tailored Porter’s Five Forces analysis for ING Groep that uncovers competitive intensity, customer and supplier influence, entry barriers, substitute threats and regulatory/digital disruptions shaping profitability.

One-sheet Porter's Five Forces for ING Groep that visualizes competitive pressure with an interactive spider chart and customizable force levels for swift strategic decisions. Clean, slide-ready layout—no macros, swap in your data and integrate instantly into reports or dashboards to relieve analysis bottlenecks.

Customers Bargaining Power

High retail switching ease via digital channels

High retail switching ease via digital channels means ING, which serves over 50 million customers, faces heightened customer bargaining power as digital account opening and switching remove friction; visible price transparency on deposits and mortgages increases sensitivity to rates and fees, ING responds with improved UX, bundled services and loyalty features, yet churn risk spikes when competitors lift savings rates significantly.

SME and corporate multi-banking

Larger SME and corporate clients routinely maintain 3+ banking relationships to optimize pricing and service, using multi-banking to bargain on lending spreads, transaction fees and ancillaries. Deep relationship coverage and cross-sell of cash management and trade finance reduce pure price-driven negotiations. Treasury integration and API connectivity materially strengthen stickiness by embedding services into clients’ workflows.

Open banking-enabled portability

PSD2, in force since January 2018, and standardized APIs let customers aggregate accounts and initiate payments via third-party apps, lowering switching friction and increasing buyer power; by 2024 there were over 3,000 licensed PSD2 TPPs in the EU. ING can use its own APIs to remain embedded in customer journeys and ecosystems, while selling value-added analytics and personalized insights to protect margins despite portability.

Rate sensitivity in a changing cycle

Service quality and trust as negotiation levers

Outages in digital banking prompt rapid switching; ING reported app uptime of 99.98% in 2024 and a retail NPS near 30, which reduces buyer leverage by raising satisfaction and trust. Financial education and health tools (used by ~4M customers in 2024) increase perceived value, while transparent fees cut dispute-driven concessions.

- uptime: 99.98%

- nps: ~30 (2024)

- digital users: ~12.8M (2024)

- education tools: ~4M users

High digital switching and PSD2 pressure NIM; UX, bundles and uptime defend customer share

High digital switching (50M customers, 12.8M digital users) and price transparency raise retail bargaining power; ING counters with UX, bundles and personalization.

Corporate clients multi-bank to squeeze spreads; treasury APIs and cash management embed services, reducing pure price pressure.

PSD2 (~3,000 TPPs) and ~25% deposit beta (2024) compress NIM; uptime 99.98% and NPS ~30 support retention.

| Metric | 2024 |

|---|---|

| Customers | 50M |

| Digital users | 12.8M |

| Deposit beta | ~25% |

| Uptime | 99.98% |

| NPS | ~30 |

| PSD2 TPPs | ~3,000 |

Preview Before You Purchase

ING Groep Porter's Five Forces Analysis

This preview shows the exact ING Groep Porter's Five Forces analysis you'll receive instantly after purchase—fully formatted and ready for use. It contains the complete competitive assessment, force-by-force evaluation, and strategic implications. No placeholders or mockups—this is the final deliverable.

A Must-Have Tool for Decision-Makers

ING Groep faces moderate buyer power, strong regulatory barriers, and mounting fintech substitution that together pressure margins and strategic positioning. This snapshot highlights key competitive levers and risk vectors shaping the bank’s future. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ING Groep’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated wholesale funding sources

ING relies partly on wholesale markets for liquidity, issuing covered bonds and senior debt via EMTN programmes; wholesale funding accounted for roughly one-third of term funding in 2024. Large institutional investors can demand higher spreads in stress, raising funding costs and prompting basis-point widening seen in 2022–24 market episodes. Diversified issuance mitigates single-source risk, while ECB facilities (TLTRO/Deposit Facility) can temper spikes but have eligibility constraints.

Critical technology and cloud vendors

Core banking platforms, cloud providers and cybersecurity vendors are mission-critical and the top three cloud providers hold roughly 66% of the IaaS/PaaS market, amplifying supplier leverage. High switching costs and deep integration complexity raise lock-in and pricing power. ING mitigates this by multi-vendor strategies and selective in-house development to lower dependency. EU rules such as DORA (effective 2025) further shape vendor negotiation and contractual resilience requirements.

Payment networks and rails

Card schemes and cross-border networks set fees and technical standards, and their network effects sustain supplier leverage despite alternatives; SEPA covers 36 countries and ECB TIPS (launched 2018) enables instant settlement. EU regulatory caps on interchange (0.2% for debit, 0.3% for credit) constrain fees materially. Volume-based pricing and co‑brand partnerships can partially offset scheme costs for issuers.

Data, analytics, and credit bureaus

Access to high-quality data from credit bureaus and AML/KYC providers directly impacts ING’s underwriting accuracy and compliance; with ING serving ~37 million customers (2024), enterprise contracts help lower per-unit costs. Leading bureaus can command premium pricing, but open banking and PSD2-driven data aggregation have expanded alternative sources, diluting individual supplier power.

- Scale: enterprise contracts reduce unit cost

- Supplier pricing: premium for top bureaus

- Open banking: increases data sources

Specialized talent and outsourcing partners

Engineering, risk and compliance talent is scarce, driving wage inflation and tight hiring: ING employed about 56,000 staff in 2024, leveraging its global brand but facing local market gaps that raise compensation and contractor spend. Niche KYC remediation and model-validation vendors command premium fees, while automation and regional centres of excellence gradually lower supplier dependence.

- Wage pressure: high demand for engineers/compliance

- Premium vendors: costly KYC/model validation

- Brand helps recruitment, local variance persists

- Automation/Centres of excellence reduce reliance

Suppliers moderate: 33% funding, 66% cloud, 56k staff

Suppliers exert moderate power: wholesale investors funded ~33% of ING term funding in 2024, raising spread risk in stress. Top three cloud providers hold ~66% IaaS/PaaS, creating supplier leverage despite multi‑vendor use. ING served ~37m customers (2024) so bureaus and card schemes retain pricing power. Staff 56,000 (2024) keeps talent suppliers strong.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Wholesale funding | 33% term funding | Spread risk |

| Cloud providers | 66% IaaS/PaaS | Lock‑in |

| Customers/bureaus | 37m | Data costs |

| Labor | 56,000 staff | Wage pressure |

What is included in the product

Tailored Porter’s Five Forces analysis for ING Groep that uncovers competitive intensity, customer and supplier influence, entry barriers, substitute threats and regulatory/digital disruptions shaping profitability.

One-sheet Porter's Five Forces for ING Groep that visualizes competitive pressure with an interactive spider chart and customizable force levels for swift strategic decisions. Clean, slide-ready layout—no macros, swap in your data and integrate instantly into reports or dashboards to relieve analysis bottlenecks.

Customers Bargaining Power

High retail switching ease via digital channels

High retail switching ease via digital channels means ING, which serves over 50 million customers, faces heightened customer bargaining power as digital account opening and switching remove friction; visible price transparency on deposits and mortgages increases sensitivity to rates and fees, ING responds with improved UX, bundled services and loyalty features, yet churn risk spikes when competitors lift savings rates significantly.

SME and corporate multi-banking

Larger SME and corporate clients routinely maintain 3+ banking relationships to optimize pricing and service, using multi-banking to bargain on lending spreads, transaction fees and ancillaries. Deep relationship coverage and cross-sell of cash management and trade finance reduce pure price-driven negotiations. Treasury integration and API connectivity materially strengthen stickiness by embedding services into clients’ workflows.

Open banking-enabled portability

PSD2, in force since January 2018, and standardized APIs let customers aggregate accounts and initiate payments via third-party apps, lowering switching friction and increasing buyer power; by 2024 there were over 3,000 licensed PSD2 TPPs in the EU. ING can use its own APIs to remain embedded in customer journeys and ecosystems, while selling value-added analytics and personalized insights to protect margins despite portability.

Rate sensitivity in a changing cycle

Service quality and trust as negotiation levers

Outages in digital banking prompt rapid switching; ING reported app uptime of 99.98% in 2024 and a retail NPS near 30, which reduces buyer leverage by raising satisfaction and trust. Financial education and health tools (used by ~4M customers in 2024) increase perceived value, while transparent fees cut dispute-driven concessions.

- uptime: 99.98%

- nps: ~30 (2024)

- digital users: ~12.8M (2024)

- education tools: ~4M users

High digital switching and PSD2 pressure NIM; UX, bundles and uptime defend customer share

High digital switching (50M customers, 12.8M digital users) and price transparency raise retail bargaining power; ING counters with UX, bundles and personalization.

Corporate clients multi-bank to squeeze spreads; treasury APIs and cash management embed services, reducing pure price pressure.

PSD2 (~3,000 TPPs) and ~25% deposit beta (2024) compress NIM; uptime 99.98% and NPS ~30 support retention.

| Metric | 2024 |

|---|---|

| Customers | 50M |

| Digital users | 12.8M |

| Deposit beta | ~25% |

| Uptime | 99.98% |

| NPS | ~30 |

| PSD2 TPPs | ~3,000 |

Preview Before You Purchase

ING Groep Porter's Five Forces Analysis

This preview shows the exact ING Groep Porter's Five Forces analysis you'll receive instantly after purchase—fully formatted and ready for use. It contains the complete competitive assessment, force-by-force evaluation, and strategic implications. No placeholders or mockups—this is the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

ING Groep faces moderate buyer power, strong regulatory barriers, and mounting fintech substitution that together pressure margins and strategic positioning. This snapshot highlights key competitive levers and risk vectors shaping the bank’s future. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ING Groep’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated wholesale funding sources

ING relies partly on wholesale markets for liquidity, issuing covered bonds and senior debt via EMTN programmes; wholesale funding accounted for roughly one-third of term funding in 2024. Large institutional investors can demand higher spreads in stress, raising funding costs and prompting basis-point widening seen in 2022–24 market episodes. Diversified issuance mitigates single-source risk, while ECB facilities (TLTRO/Deposit Facility) can temper spikes but have eligibility constraints.

Critical technology and cloud vendors

Core banking platforms, cloud providers and cybersecurity vendors are mission-critical and the top three cloud providers hold roughly 66% of the IaaS/PaaS market, amplifying supplier leverage. High switching costs and deep integration complexity raise lock-in and pricing power. ING mitigates this by multi-vendor strategies and selective in-house development to lower dependency. EU rules such as DORA (effective 2025) further shape vendor negotiation and contractual resilience requirements.

Payment networks and rails

Card schemes and cross-border networks set fees and technical standards, and their network effects sustain supplier leverage despite alternatives; SEPA covers 36 countries and ECB TIPS (launched 2018) enables instant settlement. EU regulatory caps on interchange (0.2% for debit, 0.3% for credit) constrain fees materially. Volume-based pricing and co‑brand partnerships can partially offset scheme costs for issuers.

Data, analytics, and credit bureaus

Access to high-quality data from credit bureaus and AML/KYC providers directly impacts ING’s underwriting accuracy and compliance; with ING serving ~37 million customers (2024), enterprise contracts help lower per-unit costs. Leading bureaus can command premium pricing, but open banking and PSD2-driven data aggregation have expanded alternative sources, diluting individual supplier power.

- Scale: enterprise contracts reduce unit cost

- Supplier pricing: premium for top bureaus

- Open banking: increases data sources

Specialized talent and outsourcing partners

Engineering, risk and compliance talent is scarce, driving wage inflation and tight hiring: ING employed about 56,000 staff in 2024, leveraging its global brand but facing local market gaps that raise compensation and contractor spend. Niche KYC remediation and model-validation vendors command premium fees, while automation and regional centres of excellence gradually lower supplier dependence.

- Wage pressure: high demand for engineers/compliance

- Premium vendors: costly KYC/model validation

- Brand helps recruitment, local variance persists

- Automation/Centres of excellence reduce reliance

Suppliers moderate: 33% funding, 66% cloud, 56k staff

Suppliers exert moderate power: wholesale investors funded ~33% of ING term funding in 2024, raising spread risk in stress. Top three cloud providers hold ~66% IaaS/PaaS, creating supplier leverage despite multi‑vendor use. ING served ~37m customers (2024) so bureaus and card schemes retain pricing power. Staff 56,000 (2024) keeps talent suppliers strong.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Wholesale funding | 33% term funding | Spread risk |

| Cloud providers | 66% IaaS/PaaS | Lock‑in |

| Customers/bureaus | 37m | Data costs |

| Labor | 56,000 staff | Wage pressure |

What is included in the product

Tailored Porter’s Five Forces analysis for ING Groep that uncovers competitive intensity, customer and supplier influence, entry barriers, substitute threats and regulatory/digital disruptions shaping profitability.

One-sheet Porter's Five Forces for ING Groep that visualizes competitive pressure with an interactive spider chart and customizable force levels for swift strategic decisions. Clean, slide-ready layout—no macros, swap in your data and integrate instantly into reports or dashboards to relieve analysis bottlenecks.

Customers Bargaining Power

High retail switching ease via digital channels

High retail switching ease via digital channels means ING, which serves over 50 million customers, faces heightened customer bargaining power as digital account opening and switching remove friction; visible price transparency on deposits and mortgages increases sensitivity to rates and fees, ING responds with improved UX, bundled services and loyalty features, yet churn risk spikes when competitors lift savings rates significantly.

SME and corporate multi-banking

Larger SME and corporate clients routinely maintain 3+ banking relationships to optimize pricing and service, using multi-banking to bargain on lending spreads, transaction fees and ancillaries. Deep relationship coverage and cross-sell of cash management and trade finance reduce pure price-driven negotiations. Treasury integration and API connectivity materially strengthen stickiness by embedding services into clients’ workflows.

Open banking-enabled portability

PSD2, in force since January 2018, and standardized APIs let customers aggregate accounts and initiate payments via third-party apps, lowering switching friction and increasing buyer power; by 2024 there were over 3,000 licensed PSD2 TPPs in the EU. ING can use its own APIs to remain embedded in customer journeys and ecosystems, while selling value-added analytics and personalized insights to protect margins despite portability.

Rate sensitivity in a changing cycle

Service quality and trust as negotiation levers

Outages in digital banking prompt rapid switching; ING reported app uptime of 99.98% in 2024 and a retail NPS near 30, which reduces buyer leverage by raising satisfaction and trust. Financial education and health tools (used by ~4M customers in 2024) increase perceived value, while transparent fees cut dispute-driven concessions.

- uptime: 99.98%

- nps: ~30 (2024)

- digital users: ~12.8M (2024)

- education tools: ~4M users

High digital switching and PSD2 pressure NIM; UX, bundles and uptime defend customer share

High digital switching (50M customers, 12.8M digital users) and price transparency raise retail bargaining power; ING counters with UX, bundles and personalization.

Corporate clients multi-bank to squeeze spreads; treasury APIs and cash management embed services, reducing pure price pressure.

PSD2 (~3,000 TPPs) and ~25% deposit beta (2024) compress NIM; uptime 99.98% and NPS ~30 support retention.

| Metric | 2024 |

|---|---|

| Customers | 50M |

| Digital users | 12.8M |

| Deposit beta | ~25% |

| Uptime | 99.98% |

| NPS | ~30 |

| PSD2 TPPs | ~3,000 |

Preview Before You Purchase

ING Groep Porter's Five Forces Analysis

This preview shows the exact ING Groep Porter's Five Forces analysis you'll receive instantly after purchase—fully formatted and ready for use. It contains the complete competitive assessment, force-by-force evaluation, and strategic implications. No placeholders or mockups—this is the final deliverable.