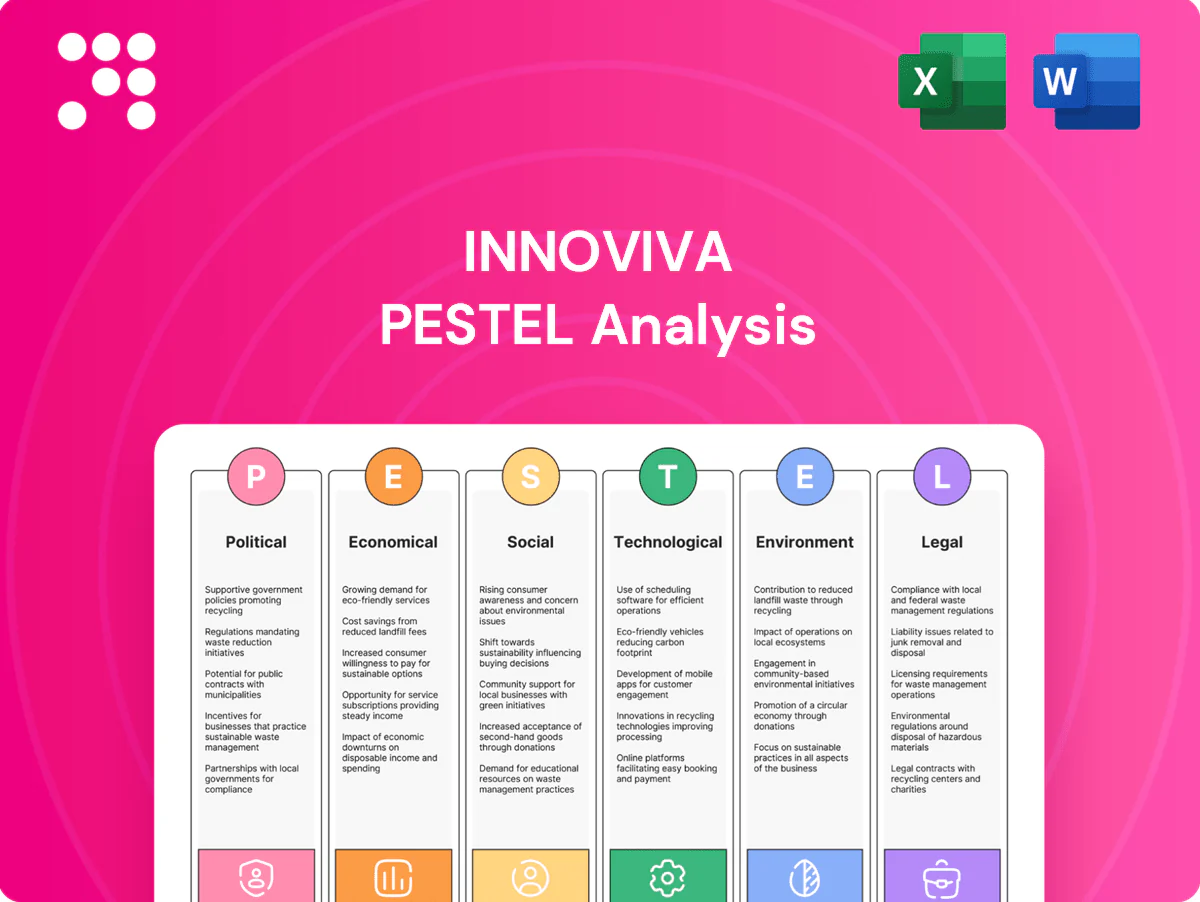

Innoviva PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping Innoviva’s strategic outlook in our targeted PESTLE snapshot. This concise analysis highlights key external risks and opportunities to inform investment or corporate strategy. Ready-made and research-backed, the full PESTLE provides in-depth insights and actionable recommendations—purchase now to access the complete report.

Political factors

Healthcare policy stability

Changes in national health priorities and funding directly affect respiratory drug uptake: US National Health Expenditure hit about $4.5 trillion in 2023 (CMS) while COPD affects ~16 million diagnosed Americans (CDC), linking spending to demand. Government support for chronic disease management can expand formularies—Medicare Part D covers inhalers for roughly 50 million beneficiaries. Policy volatility raises forecasting risk for royalty streams; Innoviva’s partner-led model amplifies exposure to country-level decisions.

Pricing and reimbursement politics

Public pressure and policies such as the US Inflation Reduction Act (negotiation from 2026) are tightening reimbursement for inhaled therapies, raising payer leverage. Reference pricing and tendering in EU and emerging markets commonly cut net prices 30–60%, lowering volumes. Political scrutiny of pharma margins forces partners to adjust pricing and contracting; with US list-to-net discounts near 40–50% in 2023, Innoviva royalty income may compress if spreads widen further.

Trade and supply geopolitics

Cross-border rules on APIs and inhaler components matter as China supplies roughly 40% of global APIs, affecting Innoviva-linked inhaler production and distribution. Export controls, tariffs and 2024 trade frictions have disrupted partner supply chains and raised risks to supply continuity. Geopolitical tensions pushed logistics costs (global container rates averaged near $2,000/FEU in 2024) and lead times up, increasing uncertainty for ex-US royalties.

Public health initiatives

Government screening programs raise COPD/asthma detection—WHO estimates 251 million COPD cases (2019) with many undiagnosed—driving higher treatment rates. Anti-smoking policies and vaccination campaigns (US adult smoking 12.5% in 2022) shift prevalence and drug demand, while pandemic preparedness can divert budgets from chronic care. Policy-driven adherence programs increase persistence and royalty flows for Innoviva.

- Screening↑ detection → treatment↑

- Smoking rates↓, vaccination↑ → demand shift

- Pandemic prep → budget reallocation risk

- Adherence programs → better persistence, higher royalties

State procurement and HTA influence

Health Technology Assessment outcomes determine national formulary access, and negative HTA decisions can sharply reduce addressable market even after regulatory approval. Centralized procurement in some countries exerts downward price pressure—WHO estimates pooled procurement can lower prices by up to 30%. Innoviva depends on partners to prepare and defend HTA submissions and responses.

- HTA drives formulary access

- Negative HTA can cut market share significantly

- Pooled procurement may reduce prices up to 30%

- Innoviva relies on partner-led HTA strategies

Policy shifts compress drug pricing, reimbursement and supply-chain risks for respiratory meds

Policy shifts reshape demand and pricing: US NHE ~$4.5T (2023) and ~16M diagnosed COPD link funding to uptake; Medicare Part D ~50M beneficiaries affect formulary access. IRA negotiations from 2026 and US list-to-net discounts 40–50% (2023) raise reimbursement risk. China supplies ~40% APIs and 2024 container rates ~$2,000/FEU heighten supply-chain risk.

| Metric | Value |

|---|---|

| US NHE | $4.5T (2023) |

| COPD diagnosed (US) | ~16M |

| Medicare Part D | ~50M beneficiaries |

| API share (China) | ~40% |

| Container rate | $2,000/FEU (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Innoviva across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section supported by current data and trend analysis. Designed to help executives, investors and entrepreneurs identify threats, opportunities and forward‑looking scenarios ready for reports, decks and strategy sessions.

Innoviva PESTLE Analysis presents a clean, visually segmented summary of external risks and opportunities, easily drop‑in ready for presentations and team alignment.

Economic factors

Macroeconomic cycles

Macroeconomic downturns pressure healthcare budgets and patient co-pay affordability, reducing elasticity for nonurgent therapies. Global growth was 3.2% in 2024 (IMF), while US inflation averaged 3.4% in 2024, raising partners' manufacturing and distribution costs. Currency swings compress ex-US royalty conversions when the dollar strengthens. Strong, stable volumes in chronic respiratory care partially offset price headwinds.

Interest rates and capital costs

Higher policy rates — about 5.25% (mid-2025) — and a 10-year Treasury near 4.3% push up discount rates applied to royalty valuations, lowering present values. Elevated borrowing costs and investment-grade yields around 5–6% raise debt servicing for leveraged post-acquisition structures. Under tighter capital, partners may reprioritize pipelines and delay spend. Future deal-making and royalty monetizations become more expensive and less frequent.

Payer mix and affordability

Shifts from public to private coverage materially change net pricing dynamics for Innoviva, as US payer mix in 2024 showed roughly 49% employer-sponsored, ~20% Medicaid/CHIP and ~17% Medicare, altering rebate and copay exposure. Rising high-deductible plan enrollment (about 45% of covered workers in 2024) can depress adherence among price-sensitive patients, lowering real-world sales. Patient assistance programs limit access barriers but increase administrative costs and contracting complexity. Royalty receipts therefore vary with utilization and persistence observed in claims and Rx data, driving quarter-to-quarter volatility.

Portfolio concentration risk

Innoviva relies on a small set of respiratory royalties, concentrating cash‑flow risk as generic or new‑entrant competition can rapidly erode volumes and pricing; geographic diversification mitigates market risk but introduces FX and policy complexity; active portfolio management and new deals are required to smooth revenue cycles.

- Concentration: respiratory royalties

- Competition: generics/new entrants

- Countermeasures: diversification, active deals

M&A and royalty market dynamics

Competition for royalty assets pushed acquisition multiples higher in 2024, with buyer sets led by specialist platforms and strategics; private equity participation increased, prioritizing cash yield and portfolio efficiency. Secondary royalty trades continued to provide liquidity but commonly executed at market-driven discounts of roughly 10–30%. Macroeconomic shocks in 2022–24 widened bid-ask spreads (often 5–15%) and delayed deal timelines into 2025.

- Competition raises multiples

- Secondary trades: ~10–30% discounts

- PE focus: cash yield & efficiency

- Shocks widen spreads ~5–15% and delay deals

Policy shifts compress drug pricing, reimbursement and supply-chain risks for respiratory meds

Macroeconomic slowdown and 2024 global growth of 3.2% (IMF) plus US inflation 3.4% in 2024 compress demand and raise partner costs; mid‑2025 policy rates ~5.25% and 10y Treasury ~4.3% lift discount rates, lowering royalty PVs. Dollar strength and FX volatility reduce ex‑US royalty conversions while high‑deductible plan prevalence (~45% of covered workers, 2024) and payer mix (49% employer, 20% Medicaid, 17% Medicare) pressure utilization. Secondary trades show ~10–30% discounts and bid‑ask spreads widened ~5–15%, making acquisitions costlier.

| Metric | Value |

|---|---|

| Global GDP 2024 (IMF) | 3.2% |

| US inflation 2024 | 3.4% |

| Policy rate mid‑2025 | ~5.25% |

| 10y Treasury | ~4.3% |

| High‑deductible enrollment 2024 | ~45% |

| Secondary trade discounts | ~10–30% |

Preview Before You Purchase

Innoviva PESTLE Analysis

The Innoviva PESTLE Analysis shown here provides a concise, actionable review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Everything displayed is the final, professionally structured file available for immediate download.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping Innoviva’s strategic outlook in our targeted PESTLE snapshot. This concise analysis highlights key external risks and opportunities to inform investment or corporate strategy. Ready-made and research-backed, the full PESTLE provides in-depth insights and actionable recommendations—purchase now to access the complete report.

Political factors

Healthcare policy stability

Changes in national health priorities and funding directly affect respiratory drug uptake: US National Health Expenditure hit about $4.5 trillion in 2023 (CMS) while COPD affects ~16 million diagnosed Americans (CDC), linking spending to demand. Government support for chronic disease management can expand formularies—Medicare Part D covers inhalers for roughly 50 million beneficiaries. Policy volatility raises forecasting risk for royalty streams; Innoviva’s partner-led model amplifies exposure to country-level decisions.

Pricing and reimbursement politics

Public pressure and policies such as the US Inflation Reduction Act (negotiation from 2026) are tightening reimbursement for inhaled therapies, raising payer leverage. Reference pricing and tendering in EU and emerging markets commonly cut net prices 30–60%, lowering volumes. Political scrutiny of pharma margins forces partners to adjust pricing and contracting; with US list-to-net discounts near 40–50% in 2023, Innoviva royalty income may compress if spreads widen further.

Trade and supply geopolitics

Cross-border rules on APIs and inhaler components matter as China supplies roughly 40% of global APIs, affecting Innoviva-linked inhaler production and distribution. Export controls, tariffs and 2024 trade frictions have disrupted partner supply chains and raised risks to supply continuity. Geopolitical tensions pushed logistics costs (global container rates averaged near $2,000/FEU in 2024) and lead times up, increasing uncertainty for ex-US royalties.

Public health initiatives

Government screening programs raise COPD/asthma detection—WHO estimates 251 million COPD cases (2019) with many undiagnosed—driving higher treatment rates. Anti-smoking policies and vaccination campaigns (US adult smoking 12.5% in 2022) shift prevalence and drug demand, while pandemic preparedness can divert budgets from chronic care. Policy-driven adherence programs increase persistence and royalty flows for Innoviva.

- Screening↑ detection → treatment↑

- Smoking rates↓, vaccination↑ → demand shift

- Pandemic prep → budget reallocation risk

- Adherence programs → better persistence, higher royalties

State procurement and HTA influence

Health Technology Assessment outcomes determine national formulary access, and negative HTA decisions can sharply reduce addressable market even after regulatory approval. Centralized procurement in some countries exerts downward price pressure—WHO estimates pooled procurement can lower prices by up to 30%. Innoviva depends on partners to prepare and defend HTA submissions and responses.

- HTA drives formulary access

- Negative HTA can cut market share significantly

- Pooled procurement may reduce prices up to 30%

- Innoviva relies on partner-led HTA strategies

Policy shifts compress drug pricing, reimbursement and supply-chain risks for respiratory meds

Policy shifts reshape demand and pricing: US NHE ~$4.5T (2023) and ~16M diagnosed COPD link funding to uptake; Medicare Part D ~50M beneficiaries affect formulary access. IRA negotiations from 2026 and US list-to-net discounts 40–50% (2023) raise reimbursement risk. China supplies ~40% APIs and 2024 container rates ~$2,000/FEU heighten supply-chain risk.

| Metric | Value |

|---|---|

| US NHE | $4.5T (2023) |

| COPD diagnosed (US) | ~16M |

| Medicare Part D | ~50M beneficiaries |

| API share (China) | ~40% |

| Container rate | $2,000/FEU (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Innoviva across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section supported by current data and trend analysis. Designed to help executives, investors and entrepreneurs identify threats, opportunities and forward‑looking scenarios ready for reports, decks and strategy sessions.

Innoviva PESTLE Analysis presents a clean, visually segmented summary of external risks and opportunities, easily drop‑in ready for presentations and team alignment.

Economic factors

Macroeconomic cycles

Macroeconomic downturns pressure healthcare budgets and patient co-pay affordability, reducing elasticity for nonurgent therapies. Global growth was 3.2% in 2024 (IMF), while US inflation averaged 3.4% in 2024, raising partners' manufacturing and distribution costs. Currency swings compress ex-US royalty conversions when the dollar strengthens. Strong, stable volumes in chronic respiratory care partially offset price headwinds.

Interest rates and capital costs

Higher policy rates — about 5.25% (mid-2025) — and a 10-year Treasury near 4.3% push up discount rates applied to royalty valuations, lowering present values. Elevated borrowing costs and investment-grade yields around 5–6% raise debt servicing for leveraged post-acquisition structures. Under tighter capital, partners may reprioritize pipelines and delay spend. Future deal-making and royalty monetizations become more expensive and less frequent.

Payer mix and affordability

Shifts from public to private coverage materially change net pricing dynamics for Innoviva, as US payer mix in 2024 showed roughly 49% employer-sponsored, ~20% Medicaid/CHIP and ~17% Medicare, altering rebate and copay exposure. Rising high-deductible plan enrollment (about 45% of covered workers in 2024) can depress adherence among price-sensitive patients, lowering real-world sales. Patient assistance programs limit access barriers but increase administrative costs and contracting complexity. Royalty receipts therefore vary with utilization and persistence observed in claims and Rx data, driving quarter-to-quarter volatility.

Portfolio concentration risk

Innoviva relies on a small set of respiratory royalties, concentrating cash‑flow risk as generic or new‑entrant competition can rapidly erode volumes and pricing; geographic diversification mitigates market risk but introduces FX and policy complexity; active portfolio management and new deals are required to smooth revenue cycles.

- Concentration: respiratory royalties

- Competition: generics/new entrants

- Countermeasures: diversification, active deals

M&A and royalty market dynamics

Competition for royalty assets pushed acquisition multiples higher in 2024, with buyer sets led by specialist platforms and strategics; private equity participation increased, prioritizing cash yield and portfolio efficiency. Secondary royalty trades continued to provide liquidity but commonly executed at market-driven discounts of roughly 10–30%. Macroeconomic shocks in 2022–24 widened bid-ask spreads (often 5–15%) and delayed deal timelines into 2025.

- Competition raises multiples

- Secondary trades: ~10–30% discounts

- PE focus: cash yield & efficiency

- Shocks widen spreads ~5–15% and delay deals

Policy shifts compress drug pricing, reimbursement and supply-chain risks for respiratory meds

Macroeconomic slowdown and 2024 global growth of 3.2% (IMF) plus US inflation 3.4% in 2024 compress demand and raise partner costs; mid‑2025 policy rates ~5.25% and 10y Treasury ~4.3% lift discount rates, lowering royalty PVs. Dollar strength and FX volatility reduce ex‑US royalty conversions while high‑deductible plan prevalence (~45% of covered workers, 2024) and payer mix (49% employer, 20% Medicaid, 17% Medicare) pressure utilization. Secondary trades show ~10–30% discounts and bid‑ask spreads widened ~5–15%, making acquisitions costlier.

| Metric | Value |

|---|---|

| Global GDP 2024 (IMF) | 3.2% |

| US inflation 2024 | 3.4% |

| Policy rate mid‑2025 | ~5.25% |

| 10y Treasury | ~4.3% |

| High‑deductible enrollment 2024 | ~45% |

| Secondary trade discounts | ~10–30% |

Preview Before You Purchase

Innoviva PESTLE Analysis

The Innoviva PESTLE Analysis shown here provides a concise, actionable review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Everything displayed is the final, professionally structured file available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping Innoviva’s strategic outlook in our targeted PESTLE snapshot. This concise analysis highlights key external risks and opportunities to inform investment or corporate strategy. Ready-made and research-backed, the full PESTLE provides in-depth insights and actionable recommendations—purchase now to access the complete report.

Political factors

Healthcare policy stability

Changes in national health priorities and funding directly affect respiratory drug uptake: US National Health Expenditure hit about $4.5 trillion in 2023 (CMS) while COPD affects ~16 million diagnosed Americans (CDC), linking spending to demand. Government support for chronic disease management can expand formularies—Medicare Part D covers inhalers for roughly 50 million beneficiaries. Policy volatility raises forecasting risk for royalty streams; Innoviva’s partner-led model amplifies exposure to country-level decisions.

Pricing and reimbursement politics

Public pressure and policies such as the US Inflation Reduction Act (negotiation from 2026) are tightening reimbursement for inhaled therapies, raising payer leverage. Reference pricing and tendering in EU and emerging markets commonly cut net prices 30–60%, lowering volumes. Political scrutiny of pharma margins forces partners to adjust pricing and contracting; with US list-to-net discounts near 40–50% in 2023, Innoviva royalty income may compress if spreads widen further.

Trade and supply geopolitics

Cross-border rules on APIs and inhaler components matter as China supplies roughly 40% of global APIs, affecting Innoviva-linked inhaler production and distribution. Export controls, tariffs and 2024 trade frictions have disrupted partner supply chains and raised risks to supply continuity. Geopolitical tensions pushed logistics costs (global container rates averaged near $2,000/FEU in 2024) and lead times up, increasing uncertainty for ex-US royalties.

Public health initiatives

Government screening programs raise COPD/asthma detection—WHO estimates 251 million COPD cases (2019) with many undiagnosed—driving higher treatment rates. Anti-smoking policies and vaccination campaigns (US adult smoking 12.5% in 2022) shift prevalence and drug demand, while pandemic preparedness can divert budgets from chronic care. Policy-driven adherence programs increase persistence and royalty flows for Innoviva.

- Screening↑ detection → treatment↑

- Smoking rates↓, vaccination↑ → demand shift

- Pandemic prep → budget reallocation risk

- Adherence programs → better persistence, higher royalties

State procurement and HTA influence

Health Technology Assessment outcomes determine national formulary access, and negative HTA decisions can sharply reduce addressable market even after regulatory approval. Centralized procurement in some countries exerts downward price pressure—WHO estimates pooled procurement can lower prices by up to 30%. Innoviva depends on partners to prepare and defend HTA submissions and responses.

- HTA drives formulary access

- Negative HTA can cut market share significantly

- Pooled procurement may reduce prices up to 30%

- Innoviva relies on partner-led HTA strategies

Policy shifts compress drug pricing, reimbursement and supply-chain risks for respiratory meds

Policy shifts reshape demand and pricing: US NHE ~$4.5T (2023) and ~16M diagnosed COPD link funding to uptake; Medicare Part D ~50M beneficiaries affect formulary access. IRA negotiations from 2026 and US list-to-net discounts 40–50% (2023) raise reimbursement risk. China supplies ~40% APIs and 2024 container rates ~$2,000/FEU heighten supply-chain risk.

| Metric | Value |

|---|---|

| US NHE | $4.5T (2023) |

| COPD diagnosed (US) | ~16M |

| Medicare Part D | ~50M beneficiaries |

| API share (China) | ~40% |

| Container rate | $2,000/FEU (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Innoviva across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section supported by current data and trend analysis. Designed to help executives, investors and entrepreneurs identify threats, opportunities and forward‑looking scenarios ready for reports, decks and strategy sessions.

Innoviva PESTLE Analysis presents a clean, visually segmented summary of external risks and opportunities, easily drop‑in ready for presentations and team alignment.

Economic factors

Macroeconomic cycles

Macroeconomic downturns pressure healthcare budgets and patient co-pay affordability, reducing elasticity for nonurgent therapies. Global growth was 3.2% in 2024 (IMF), while US inflation averaged 3.4% in 2024, raising partners' manufacturing and distribution costs. Currency swings compress ex-US royalty conversions when the dollar strengthens. Strong, stable volumes in chronic respiratory care partially offset price headwinds.

Interest rates and capital costs

Higher policy rates — about 5.25% (mid-2025) — and a 10-year Treasury near 4.3% push up discount rates applied to royalty valuations, lowering present values. Elevated borrowing costs and investment-grade yields around 5–6% raise debt servicing for leveraged post-acquisition structures. Under tighter capital, partners may reprioritize pipelines and delay spend. Future deal-making and royalty monetizations become more expensive and less frequent.

Payer mix and affordability

Shifts from public to private coverage materially change net pricing dynamics for Innoviva, as US payer mix in 2024 showed roughly 49% employer-sponsored, ~20% Medicaid/CHIP and ~17% Medicare, altering rebate and copay exposure. Rising high-deductible plan enrollment (about 45% of covered workers in 2024) can depress adherence among price-sensitive patients, lowering real-world sales. Patient assistance programs limit access barriers but increase administrative costs and contracting complexity. Royalty receipts therefore vary with utilization and persistence observed in claims and Rx data, driving quarter-to-quarter volatility.

Portfolio concentration risk

Innoviva relies on a small set of respiratory royalties, concentrating cash‑flow risk as generic or new‑entrant competition can rapidly erode volumes and pricing; geographic diversification mitigates market risk but introduces FX and policy complexity; active portfolio management and new deals are required to smooth revenue cycles.

- Concentration: respiratory royalties

- Competition: generics/new entrants

- Countermeasures: diversification, active deals

M&A and royalty market dynamics

Competition for royalty assets pushed acquisition multiples higher in 2024, with buyer sets led by specialist platforms and strategics; private equity participation increased, prioritizing cash yield and portfolio efficiency. Secondary royalty trades continued to provide liquidity but commonly executed at market-driven discounts of roughly 10–30%. Macroeconomic shocks in 2022–24 widened bid-ask spreads (often 5–15%) and delayed deal timelines into 2025.

- Competition raises multiples

- Secondary trades: ~10–30% discounts

- PE focus: cash yield & efficiency

- Shocks widen spreads ~5–15% and delay deals

Policy shifts compress drug pricing, reimbursement and supply-chain risks for respiratory meds

Macroeconomic slowdown and 2024 global growth of 3.2% (IMF) plus US inflation 3.4% in 2024 compress demand and raise partner costs; mid‑2025 policy rates ~5.25% and 10y Treasury ~4.3% lift discount rates, lowering royalty PVs. Dollar strength and FX volatility reduce ex‑US royalty conversions while high‑deductible plan prevalence (~45% of covered workers, 2024) and payer mix (49% employer, 20% Medicaid, 17% Medicare) pressure utilization. Secondary trades show ~10–30% discounts and bid‑ask spreads widened ~5–15%, making acquisitions costlier.

| Metric | Value |

|---|---|

| Global GDP 2024 (IMF) | 3.2% |

| US inflation 2024 | 3.4% |

| Policy rate mid‑2025 | ~5.25% |

| 10y Treasury | ~4.3% |

| High‑deductible enrollment 2024 | ~45% |

| Secondary trade discounts | ~10–30% |

Preview Before You Purchase

Innoviva PESTLE Analysis

The Innoviva PESTLE Analysis shown here provides a concise, actionable review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Everything displayed is the final, professionally structured file available for immediate download.