Innoviva SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Explore Innoviva’s strategic position with our concise SWOT snapshot—highlighting licensing strengths, royalty dependencies, and pipeline risks in three clear insights. Want the full picture? Purchase the complete SWOT report for research-backed analysis, investor-ready Word and Excel deliverables, and actionable recommendations to inform decisions.

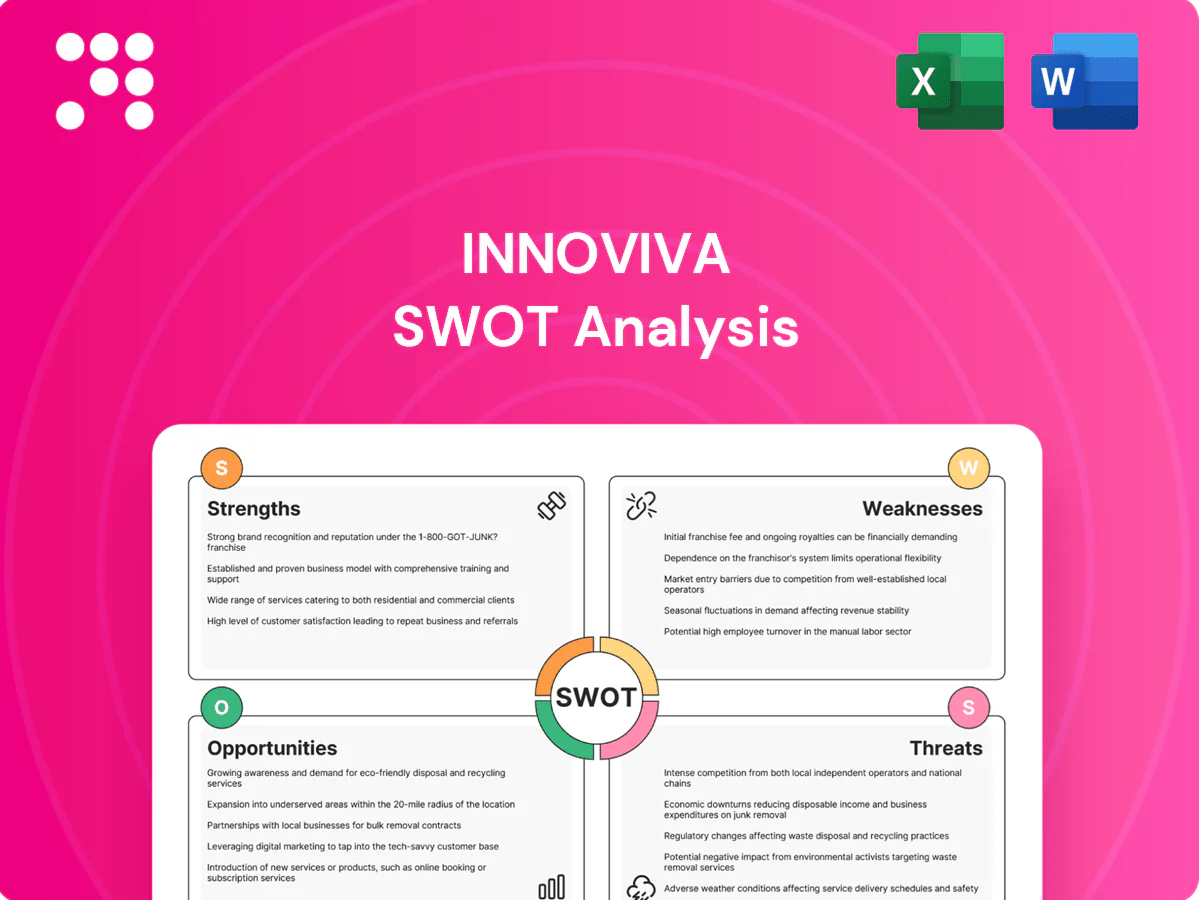

Strengths

Recurring royalty cash flows

Innoviva (ticker INVA) generates steady, contractually defined royalties from partnered respiratory products, producing predictable cash inflows that support operating stability and capital allocation. These royalty streams have historically shown resilience through modest market fluctuations, cushioning volatility in other revenue sources. The predictability of royalties enables disciplined portfolio decisions following acquisitions.

Leverage of partner commercialization

By relying on partner commercialization, Innoviva captures value without building large commercial infrastructures, lowering fixed costs and execution risk; partners handle sales/marketing, accelerating time to market via established channels and enabling the model to scale with partner performance across key geographies.

Focused respiratory domain expertise

Focused respiratory expertise sharpens Innoviva’s asset selection and deal-making, particularly in a therapeutic area that accounted for roughly $50B in global market activity in 2023 and faces high unmet need (COPD caused ~3.23M deaths in 2019; asthma affected ~262M people in 2019). Clinical and regulatory familiarity streamlines diligence and lifecycle input, improving negotiating leverage and credibility with specialist partners and prescribers.

Capital-light operating model

Innoviva’s capital-light operating model, driven by limited internal R&D and lean operations, preserves gross margins and operating flexibility.

Consistent cash generation is redeployable into new royalty agreements or milestone-driven investments, reducing dilution pressure.

Lower cash burn cuts financing risk across cycles and sustains optionality through market volatility.

- royalty-focused model

- low opex, preserved margins

- cash redeployable to deals

- reduced financing risk

Strategic partnership track record

Innoviva's established collaborations with biopharma licensors reinforce its reliability to prospective partners, supported by a consistent track record of executed royalty and asset transactions. Historical milestone achievements validate its deal structures and commercialization timelines. Repeat partner engagement lowers sourcing friction and increases leverage to secure favorable terms on future assets.

- Established collaborator signal: reliability to licensors

- Milestone validation: deal structures proven in practice

- Repeat partners: reduced sourcing friction

- Negotiation leverage: better terms on future assets

Predictable royalty cashflows and capital-light model enable disciplined capital redeployment

Innoviva generates predictable royalty cashflows from partnered respiratory products, supporting disciplined capital allocation and low operating leverage. The capital-light model reduces financing risk and preserves margins, enabling cash redeployment into new royalties or milestone investments. Established partner relationships and repeat transactions strengthen sourcing and negotiation leverage.

| Metric | Value |

|---|---|

| Global respiratory market (2023) | $50B |

| COPD deaths (2019) | 3.23M |

| Asthma prevalence (2019) | 262M people |

What is included in the product

Delivers a strategic overview of Innoviva’s internal and external business factors, outlining its strengths, weaknesses, opportunities and threats to assess competitive position, growth drivers and key risks shaping the company’s future.

Provides a compact Innoviva-specific SWOT matrix that relieves analysis bottlenecks by turning licensing, royalty and portfolio risks into a clear visual overview for rapid strategic alignment and stakeholder briefings.

Weaknesses

Product and partner concentration

Revenue remained heavily weighted toward a narrow set of respiratory products and a small number of counterparties, concentrating cash flow risk. This concentration magnifies exposure to single-asset demand shifts and patent or competitive setbacks. Any partner-specific operational or commercial issues can disproportionately reduce royalty receipts and free cash flow. Strategic diversification is structurally limited by Innoviva’s focused licensing portfolio and modest balance-sheet scale.

Limited control over commercialization

Dependence on partners such as GSK and Theravance means Innoviva cannot set pricing, promotion or market access; its royalties derive from partner-led sales. Innoviva’s influence on sales execution is indirect, constrained to contractual remedies rather than day-to-day commercialization. Misalignment of incentives between Innoviva and partners can damp peak sales, and SEC disclosures highlight that course corrections may be slow or partial.

Finite royalty duration and IP cliffs

Royalties fall to zero as patents expire or agreements terminate; patents have a statutory term of 20 years but effective exclusivity for drugs often ranges 8–12 years post-approval. As exclusivities erode, generic entry commonly compresses prices by 70–90% and volumes materially decline. Without continual replenishment of new royalty assets, license revenue decays and firms must plan for step-downs and long tail effects in cash-flow modeling.

Constrained internal pipeline

Innoviva's model remains royalty-centric, prioritizing external licensing over in-house drug discovery; as of 2024 this limits owned R&D and reduces future growth self-sufficiency. Reliance on third-party deal flow creates timing unpredictability, and gaps can form between steady legacy royalty cash flows and the timing of new asset contributions.

- royalty-heavy model

- limited owned R&D

- deal-flow timing risk

- legacy vs new-asset cash gaps

Post-acquisition and delisting constraints

Following acquisition and delisting, transparency and liquidity may decline for stakeholders; trading volume often falls >90% post-delisting, constraining exit options. Private control can narrow funding to sponsor support and limit access to public capital markets. Strategic shifts after buyout create interim uncertainty, while governance changes can alter risk appetite and extend execution timelines.

- Liquidity impact: trading volume down >90%

- Funding narrowed: sponsor-dependent

- Short-term uncertainty from strategy shifts

- Governance change risks timelines and risk appetite

Concentrated respiratory revenue, partner dependence, and 8–12yr exclusivity risk

Revenue concentrated in a narrow respiratory portfolio and few partners, creating cash-flow risk and dependence on partner execution. Royalties cease as exclusivity erodes (effective exclusivity 8–12 years), with generic entry commonly compressing prices 70–90%. Post-acquisition delisting often cuts trading volume by >90%, narrowing funding to sponsor support.

| Metric | Value |

|---|---|

| Effective exclusivity | 8–12 years |

| Generic price compression | 70–90% |

| Post-delist volume change | >90% decline |

Full Version Awaits

Innoviva SWOT Analysis

This is the actual Innoviva SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the complete, editable version unlocked after checkout. You’re viewing a live excerpt of the real file, ready for immediate download once purchased.

Elevate Your Analysis with the Complete SWOT Report

Explore Innoviva’s strategic position with our concise SWOT snapshot—highlighting licensing strengths, royalty dependencies, and pipeline risks in three clear insights. Want the full picture? Purchase the complete SWOT report for research-backed analysis, investor-ready Word and Excel deliverables, and actionable recommendations to inform decisions.

Strengths

Recurring royalty cash flows

Innoviva (ticker INVA) generates steady, contractually defined royalties from partnered respiratory products, producing predictable cash inflows that support operating stability and capital allocation. These royalty streams have historically shown resilience through modest market fluctuations, cushioning volatility in other revenue sources. The predictability of royalties enables disciplined portfolio decisions following acquisitions.

Leverage of partner commercialization

By relying on partner commercialization, Innoviva captures value without building large commercial infrastructures, lowering fixed costs and execution risk; partners handle sales/marketing, accelerating time to market via established channels and enabling the model to scale with partner performance across key geographies.

Focused respiratory domain expertise

Focused respiratory expertise sharpens Innoviva’s asset selection and deal-making, particularly in a therapeutic area that accounted for roughly $50B in global market activity in 2023 and faces high unmet need (COPD caused ~3.23M deaths in 2019; asthma affected ~262M people in 2019). Clinical and regulatory familiarity streamlines diligence and lifecycle input, improving negotiating leverage and credibility with specialist partners and prescribers.

Capital-light operating model

Innoviva’s capital-light operating model, driven by limited internal R&D and lean operations, preserves gross margins and operating flexibility.

Consistent cash generation is redeployable into new royalty agreements or milestone-driven investments, reducing dilution pressure.

Lower cash burn cuts financing risk across cycles and sustains optionality through market volatility.

- royalty-focused model

- low opex, preserved margins

- cash redeployable to deals

- reduced financing risk

Strategic partnership track record

Innoviva's established collaborations with biopharma licensors reinforce its reliability to prospective partners, supported by a consistent track record of executed royalty and asset transactions. Historical milestone achievements validate its deal structures and commercialization timelines. Repeat partner engagement lowers sourcing friction and increases leverage to secure favorable terms on future assets.

- Established collaborator signal: reliability to licensors

- Milestone validation: deal structures proven in practice

- Repeat partners: reduced sourcing friction

- Negotiation leverage: better terms on future assets

Predictable royalty cashflows and capital-light model enable disciplined capital redeployment

Innoviva generates predictable royalty cashflows from partnered respiratory products, supporting disciplined capital allocation and low operating leverage. The capital-light model reduces financing risk and preserves margins, enabling cash redeployment into new royalties or milestone investments. Established partner relationships and repeat transactions strengthen sourcing and negotiation leverage.

| Metric | Value |

|---|---|

| Global respiratory market (2023) | $50B |

| COPD deaths (2019) | 3.23M |

| Asthma prevalence (2019) | 262M people |

What is included in the product

Delivers a strategic overview of Innoviva’s internal and external business factors, outlining its strengths, weaknesses, opportunities and threats to assess competitive position, growth drivers and key risks shaping the company’s future.

Provides a compact Innoviva-specific SWOT matrix that relieves analysis bottlenecks by turning licensing, royalty and portfolio risks into a clear visual overview for rapid strategic alignment and stakeholder briefings.

Weaknesses

Product and partner concentration

Revenue remained heavily weighted toward a narrow set of respiratory products and a small number of counterparties, concentrating cash flow risk. This concentration magnifies exposure to single-asset demand shifts and patent or competitive setbacks. Any partner-specific operational or commercial issues can disproportionately reduce royalty receipts and free cash flow. Strategic diversification is structurally limited by Innoviva’s focused licensing portfolio and modest balance-sheet scale.

Limited control over commercialization

Dependence on partners such as GSK and Theravance means Innoviva cannot set pricing, promotion or market access; its royalties derive from partner-led sales. Innoviva’s influence on sales execution is indirect, constrained to contractual remedies rather than day-to-day commercialization. Misalignment of incentives between Innoviva and partners can damp peak sales, and SEC disclosures highlight that course corrections may be slow or partial.

Finite royalty duration and IP cliffs

Royalties fall to zero as patents expire or agreements terminate; patents have a statutory term of 20 years but effective exclusivity for drugs often ranges 8–12 years post-approval. As exclusivities erode, generic entry commonly compresses prices by 70–90% and volumes materially decline. Without continual replenishment of new royalty assets, license revenue decays and firms must plan for step-downs and long tail effects in cash-flow modeling.

Constrained internal pipeline

Innoviva's model remains royalty-centric, prioritizing external licensing over in-house drug discovery; as of 2024 this limits owned R&D and reduces future growth self-sufficiency. Reliance on third-party deal flow creates timing unpredictability, and gaps can form between steady legacy royalty cash flows and the timing of new asset contributions.

- royalty-heavy model

- limited owned R&D

- deal-flow timing risk

- legacy vs new-asset cash gaps

Post-acquisition and delisting constraints

Following acquisition and delisting, transparency and liquidity may decline for stakeholders; trading volume often falls >90% post-delisting, constraining exit options. Private control can narrow funding to sponsor support and limit access to public capital markets. Strategic shifts after buyout create interim uncertainty, while governance changes can alter risk appetite and extend execution timelines.

- Liquidity impact: trading volume down >90%

- Funding narrowed: sponsor-dependent

- Short-term uncertainty from strategy shifts

- Governance change risks timelines and risk appetite

Concentrated respiratory revenue, partner dependence, and 8–12yr exclusivity risk

Revenue concentrated in a narrow respiratory portfolio and few partners, creating cash-flow risk and dependence on partner execution. Royalties cease as exclusivity erodes (effective exclusivity 8–12 years), with generic entry commonly compressing prices 70–90%. Post-acquisition delisting often cuts trading volume by >90%, narrowing funding to sponsor support.

| Metric | Value |

|---|---|

| Effective exclusivity | 8–12 years |

| Generic price compression | 70–90% |

| Post-delist volume change | >90% decline |

Full Version Awaits

Innoviva SWOT Analysis

This is the actual Innoviva SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the complete, editable version unlocked after checkout. You’re viewing a live excerpt of the real file, ready for immediate download once purchased.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Explore Innoviva’s strategic position with our concise SWOT snapshot—highlighting licensing strengths, royalty dependencies, and pipeline risks in three clear insights. Want the full picture? Purchase the complete SWOT report for research-backed analysis, investor-ready Word and Excel deliverables, and actionable recommendations to inform decisions.

Strengths

Recurring royalty cash flows

Innoviva (ticker INVA) generates steady, contractually defined royalties from partnered respiratory products, producing predictable cash inflows that support operating stability and capital allocation. These royalty streams have historically shown resilience through modest market fluctuations, cushioning volatility in other revenue sources. The predictability of royalties enables disciplined portfolio decisions following acquisitions.

Leverage of partner commercialization

By relying on partner commercialization, Innoviva captures value without building large commercial infrastructures, lowering fixed costs and execution risk; partners handle sales/marketing, accelerating time to market via established channels and enabling the model to scale with partner performance across key geographies.

Focused respiratory domain expertise

Focused respiratory expertise sharpens Innoviva’s asset selection and deal-making, particularly in a therapeutic area that accounted for roughly $50B in global market activity in 2023 and faces high unmet need (COPD caused ~3.23M deaths in 2019; asthma affected ~262M people in 2019). Clinical and regulatory familiarity streamlines diligence and lifecycle input, improving negotiating leverage and credibility with specialist partners and prescribers.

Capital-light operating model

Innoviva’s capital-light operating model, driven by limited internal R&D and lean operations, preserves gross margins and operating flexibility.

Consistent cash generation is redeployable into new royalty agreements or milestone-driven investments, reducing dilution pressure.

Lower cash burn cuts financing risk across cycles and sustains optionality through market volatility.

- royalty-focused model

- low opex, preserved margins

- cash redeployable to deals

- reduced financing risk

Strategic partnership track record

Innoviva's established collaborations with biopharma licensors reinforce its reliability to prospective partners, supported by a consistent track record of executed royalty and asset transactions. Historical milestone achievements validate its deal structures and commercialization timelines. Repeat partner engagement lowers sourcing friction and increases leverage to secure favorable terms on future assets.

- Established collaborator signal: reliability to licensors

- Milestone validation: deal structures proven in practice

- Repeat partners: reduced sourcing friction

- Negotiation leverage: better terms on future assets

Predictable royalty cashflows and capital-light model enable disciplined capital redeployment

Innoviva generates predictable royalty cashflows from partnered respiratory products, supporting disciplined capital allocation and low operating leverage. The capital-light model reduces financing risk and preserves margins, enabling cash redeployment into new royalties or milestone investments. Established partner relationships and repeat transactions strengthen sourcing and negotiation leverage.

| Metric | Value |

|---|---|

| Global respiratory market (2023) | $50B |

| COPD deaths (2019) | 3.23M |

| Asthma prevalence (2019) | 262M people |

What is included in the product

Delivers a strategic overview of Innoviva’s internal and external business factors, outlining its strengths, weaknesses, opportunities and threats to assess competitive position, growth drivers and key risks shaping the company’s future.

Provides a compact Innoviva-specific SWOT matrix that relieves analysis bottlenecks by turning licensing, royalty and portfolio risks into a clear visual overview for rapid strategic alignment and stakeholder briefings.

Weaknesses

Product and partner concentration

Revenue remained heavily weighted toward a narrow set of respiratory products and a small number of counterparties, concentrating cash flow risk. This concentration magnifies exposure to single-asset demand shifts and patent or competitive setbacks. Any partner-specific operational or commercial issues can disproportionately reduce royalty receipts and free cash flow. Strategic diversification is structurally limited by Innoviva’s focused licensing portfolio and modest balance-sheet scale.

Limited control over commercialization

Dependence on partners such as GSK and Theravance means Innoviva cannot set pricing, promotion or market access; its royalties derive from partner-led sales. Innoviva’s influence on sales execution is indirect, constrained to contractual remedies rather than day-to-day commercialization. Misalignment of incentives between Innoviva and partners can damp peak sales, and SEC disclosures highlight that course corrections may be slow or partial.

Finite royalty duration and IP cliffs

Royalties fall to zero as patents expire or agreements terminate; patents have a statutory term of 20 years but effective exclusivity for drugs often ranges 8–12 years post-approval. As exclusivities erode, generic entry commonly compresses prices by 70–90% and volumes materially decline. Without continual replenishment of new royalty assets, license revenue decays and firms must plan for step-downs and long tail effects in cash-flow modeling.

Constrained internal pipeline

Innoviva's model remains royalty-centric, prioritizing external licensing over in-house drug discovery; as of 2024 this limits owned R&D and reduces future growth self-sufficiency. Reliance on third-party deal flow creates timing unpredictability, and gaps can form between steady legacy royalty cash flows and the timing of new asset contributions.

- royalty-heavy model

- limited owned R&D

- deal-flow timing risk

- legacy vs new-asset cash gaps

Post-acquisition and delisting constraints

Following acquisition and delisting, transparency and liquidity may decline for stakeholders; trading volume often falls >90% post-delisting, constraining exit options. Private control can narrow funding to sponsor support and limit access to public capital markets. Strategic shifts after buyout create interim uncertainty, while governance changes can alter risk appetite and extend execution timelines.

- Liquidity impact: trading volume down >90%

- Funding narrowed: sponsor-dependent

- Short-term uncertainty from strategy shifts

- Governance change risks timelines and risk appetite

Concentrated respiratory revenue, partner dependence, and 8–12yr exclusivity risk

Revenue concentrated in a narrow respiratory portfolio and few partners, creating cash-flow risk and dependence on partner execution. Royalties cease as exclusivity erodes (effective exclusivity 8–12 years), with generic entry commonly compressing prices 70–90%. Post-acquisition delisting often cuts trading volume by >90%, narrowing funding to sponsor support.

| Metric | Value |

|---|---|

| Effective exclusivity | 8–12 years |

| Generic price compression | 70–90% |

| Post-delist volume change | >90% decline |

Full Version Awaits

Innoviva SWOT Analysis

This is the actual Innoviva SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, with the complete, editable version unlocked after checkout. You’re viewing a live excerpt of the real file, ready for immediate download once purchased.