Insteel Industries Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

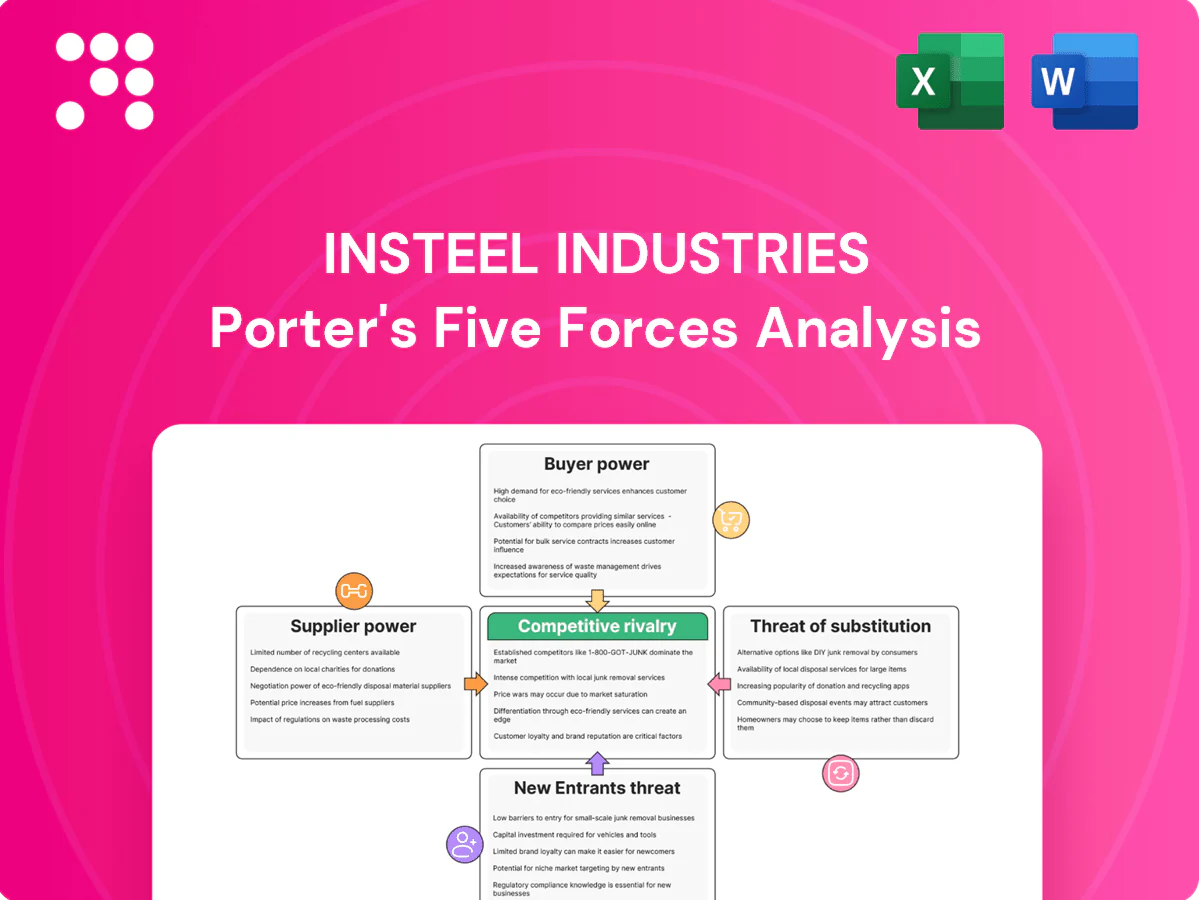

Insteel Industries faces moderate supplier power due to specialized steel inputs, while buyer power is tempered by construction demand cycles and distributor relationships; rivalry is intense among steel and rebar producers, and threats from new entrants and substitutes remain low-to-moderate. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated rod suppliers

Wire rod inputs are sourced from a relatively concentrated set of North American mini-mills—notably Nucor, Steel Dynamics and Cleveland-Cliffs—which remained primary rod suppliers in 2024, increasing supplier leverage. Fewer qualified mills meeting ASTM/PCI specs heighten dependence and let consolidation tighten terms and delivery windows. Insteel must balance dual-sourcing against quality control and freight economics to manage cost and continuity.

Steel price volatility

Raw steel costs remain cyclical and volatile, with US hot-rolled coil averaging about $820 per short ton in 2024 and spot swings exceeding 25% intra-year, often outpacing finished-goods pricing. Suppliers routinely apply surcharges that compress Insteel Industries margins when demand cools, and timing mismatches between input spikes and customer price resets intensify pressure. Hedging and index-linked contracts partially mitigate exposure but do not eliminate residual basis and timing risk.

Logistics and freight

Freight is a material cost for heavy, low-value-density rod and mesh, often representing roughly 10–15% of landed cost. U.S. diesel averaged about $4.17/gal in 2024 (EIA), and fuel spikes or rail/truck capacity constraints can add 5–20% to delivered cost, amplifying supplier power. Regional proximity to mills materially affects landed economics, and disruptions frequently force premium expedited freight or higher-priced alternate sourcing.

Quality/spec compliance

PCS and WWR demand tight mechanical and weld properties, narrowing acceptable suppliers and concentrating sourcing risk; failures risk customer rejection and costly rework, so Insteel in 2024 prioritizes proven mills and long-term relationships. This raises switching costs on the supply side, while mill certifications and audits give certified suppliers measurable negotiating leverage.

- Supplier pool: constrained by PCS/WWR specs

- Cost impact: failures→rework/customer rejection

- Leverage: certifications/audits increase supplier bargaining power

Trade policy and imports

Tariffs, quotas and AD/CVD rulings have curtailed rod imports and strengthened domestic pricing power, causing fast shifts in mill order books and lead times; when imports ebb, U.S. mills capture margin and Insteel’s negotiating leverage tightens. Insteel’s options remain constrained until trade flows and enforcement normalize, pressuring near-term cost pass-through and utilization decisions.

- Trade barriers lift domestic pricing

- Rapid ripple into lead times

- Domestic mills capture margin

- Insteel constrained until normalization

Concentrated rod supply and tight PCS/WWR specs boost mill pricing amid volatile HRC

Concentrated rod supply (Nucor, Steel Dynamics, Cleveland-Cliffs) and tight PCS/WWR specs raised supplier leverage in 2024; HRC averaged ~$820/st with >25% spot swings, compressing margins. Freight (10–15% of landed cost) and diesel at ~$4.17/gal amplified delivery risk. Trade barriers reduced imports, tightening domestic mill lead times and pricing power.

| Metric | 2024 |

|---|---|

| HRC price | $820/short ton |

| Diesel | $4.17/gal |

| Freight share | 10–15% |

| Spot volatility | >25% |

What is included in the product

Tailored Porter's Five Forces analysis for Insteel Industries uncovering key drivers of competition, customer influence, and market entry risks specific to steel reinforcement products. Evaluates supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces shaping pricing, margins, and competitive positioning.

A concise Porter's Five Forces snapshot for Insteel Industries—one-sheet clarity that visualizes competitive pressure with an editable radar chart, customizable scores for evolving market data, and a clean layout ready for pitch decks or integration into broader reports.

Customers Bargaining Power

Large, knowledgeable buyers

Large precast/prestressed producers and major contractors buy steel in scale, benchmark suppliers via multiple quotes and indices, and their professional procurement teams drive price pressure; Insteel's 2024 net sales (~$695 million) underscore customer concentration and volume-based leverage. Relationship value helps but rarely fully offsets buyers' ability to demand lower margins.

Price sensitivity

Reinforcement is a significant cost in many concrete projects, often comprising a sizeable share of structural budgets and driving tight margins for contractors in 2024 as U.S. construction spending rose about 3.4% year-over-year.

Project bid environments favor lowest delivered price, so buyers leverage competitive bids and push for index-based or spot discounts when steel prices soften.

To defend premiums, Insteel must quantify and market clear value-add services—just-in-time delivery, fabrication accuracy, and warranty metrics—that justify higher per-ton prices.

Low switching costs

WWR and PCS are standardized to ASTM A1064/A1064M and ACI 318, so once a supplier meets specs switching on future orders is straightforward. Regional freight variability and lead times—often 2–6 weeks in 2024 logistics reports—pose larger hurdles than technical changeover. That keeps buyer power elevated, pressuring margins and enabling price-driven switching for repeat orders.

Demand cyclicality

Construction cycles shift volume bargaining power: Insteel (net sales ~1.05 billion in 2023) faces stronger buyer leverage in downturns as customers consolidate purchases and demand price or lead-time concessions; conversely 2024 US housing starts near 1.3M units and tighter allocation in upcycles reduce buyer leverage.

- Downturns: buyers consolidate spend, win concessions

- Upcycles: allocation tightness limits buyer leverage

- Mix shift: residential vs non-residential alters negotiating dynamics

Specification influence

Engineers and owners set reinforcement specs, creating supplier lock-in when drawings name products or basis-of-design; this can force mid-project sourcing shifts and margin pressure. Securing basis-of-design or approved-list status limits buyer options, while many specs retain or equal language that preserved competition. Submittal control offers defense but does not provide immunity against substitution or change orders; U.S. construction spending topped $1.6 trillion in 2023.

- Specification control increases switching costs

- Approved-list status reduces buyer options mid-project

- or equal clauses preserve competition

- Submittal control mitigates but does not eliminate risk

Buyers drive down delivered steel prices via index benchmarking and short lead-time leverage

Buyers exert high price pressure: large contractors and precast producers benchmark via indices and quotes, with Insteel 2024 net sales ~695 million reflecting volume-driven leverage. Project bids favor lowest delivered price; buyers push index/spot discounts when steel softens. Specification control and logistics (lead times 2–6 weeks) temper switching but do not eliminate buyer leverage.

| Metric | 2024 Value |

|---|---|

| Insteel net sales | $695M |

| US housing starts | ~1.3M units |

| Lead times | 2–6 weeks |

Preview the Actual Deliverable

Insteel Industries Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for Insteel Industries you’ll receive after purchase—no placeholders or samples. The full document is fully formatted, ready for immediate download and use. What you see here is precisely the deliverable available upon payment.

A Must-Have Tool for Decision-Makers

Insteel Industries faces moderate supplier power due to specialized steel inputs, while buyer power is tempered by construction demand cycles and distributor relationships; rivalry is intense among steel and rebar producers, and threats from new entrants and substitutes remain low-to-moderate. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated rod suppliers

Wire rod inputs are sourced from a relatively concentrated set of North American mini-mills—notably Nucor, Steel Dynamics and Cleveland-Cliffs—which remained primary rod suppliers in 2024, increasing supplier leverage. Fewer qualified mills meeting ASTM/PCI specs heighten dependence and let consolidation tighten terms and delivery windows. Insteel must balance dual-sourcing against quality control and freight economics to manage cost and continuity.

Steel price volatility

Raw steel costs remain cyclical and volatile, with US hot-rolled coil averaging about $820 per short ton in 2024 and spot swings exceeding 25% intra-year, often outpacing finished-goods pricing. Suppliers routinely apply surcharges that compress Insteel Industries margins when demand cools, and timing mismatches between input spikes and customer price resets intensify pressure. Hedging and index-linked contracts partially mitigate exposure but do not eliminate residual basis and timing risk.

Logistics and freight

Freight is a material cost for heavy, low-value-density rod and mesh, often representing roughly 10–15% of landed cost. U.S. diesel averaged about $4.17/gal in 2024 (EIA), and fuel spikes or rail/truck capacity constraints can add 5–20% to delivered cost, amplifying supplier power. Regional proximity to mills materially affects landed economics, and disruptions frequently force premium expedited freight or higher-priced alternate sourcing.

Quality/spec compliance

PCS and WWR demand tight mechanical and weld properties, narrowing acceptable suppliers and concentrating sourcing risk; failures risk customer rejection and costly rework, so Insteel in 2024 prioritizes proven mills and long-term relationships. This raises switching costs on the supply side, while mill certifications and audits give certified suppliers measurable negotiating leverage.

- Supplier pool: constrained by PCS/WWR specs

- Cost impact: failures→rework/customer rejection

- Leverage: certifications/audits increase supplier bargaining power

Trade policy and imports

Tariffs, quotas and AD/CVD rulings have curtailed rod imports and strengthened domestic pricing power, causing fast shifts in mill order books and lead times; when imports ebb, U.S. mills capture margin and Insteel’s negotiating leverage tightens. Insteel’s options remain constrained until trade flows and enforcement normalize, pressuring near-term cost pass-through and utilization decisions.

- Trade barriers lift domestic pricing

- Rapid ripple into lead times

- Domestic mills capture margin

- Insteel constrained until normalization

Concentrated rod supply and tight PCS/WWR specs boost mill pricing amid volatile HRC

Concentrated rod supply (Nucor, Steel Dynamics, Cleveland-Cliffs) and tight PCS/WWR specs raised supplier leverage in 2024; HRC averaged ~$820/st with >25% spot swings, compressing margins. Freight (10–15% of landed cost) and diesel at ~$4.17/gal amplified delivery risk. Trade barriers reduced imports, tightening domestic mill lead times and pricing power.

| Metric | 2024 |

|---|---|

| HRC price | $820/short ton |

| Diesel | $4.17/gal |

| Freight share | 10–15% |

| Spot volatility | >25% |

What is included in the product

Tailored Porter's Five Forces analysis for Insteel Industries uncovering key drivers of competition, customer influence, and market entry risks specific to steel reinforcement products. Evaluates supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces shaping pricing, margins, and competitive positioning.

A concise Porter's Five Forces snapshot for Insteel Industries—one-sheet clarity that visualizes competitive pressure with an editable radar chart, customizable scores for evolving market data, and a clean layout ready for pitch decks or integration into broader reports.

Customers Bargaining Power

Large, knowledgeable buyers

Large precast/prestressed producers and major contractors buy steel in scale, benchmark suppliers via multiple quotes and indices, and their professional procurement teams drive price pressure; Insteel's 2024 net sales (~$695 million) underscore customer concentration and volume-based leverage. Relationship value helps but rarely fully offsets buyers' ability to demand lower margins.

Price sensitivity

Reinforcement is a significant cost in many concrete projects, often comprising a sizeable share of structural budgets and driving tight margins for contractors in 2024 as U.S. construction spending rose about 3.4% year-over-year.

Project bid environments favor lowest delivered price, so buyers leverage competitive bids and push for index-based or spot discounts when steel prices soften.

To defend premiums, Insteel must quantify and market clear value-add services—just-in-time delivery, fabrication accuracy, and warranty metrics—that justify higher per-ton prices.

Low switching costs

WWR and PCS are standardized to ASTM A1064/A1064M and ACI 318, so once a supplier meets specs switching on future orders is straightforward. Regional freight variability and lead times—often 2–6 weeks in 2024 logistics reports—pose larger hurdles than technical changeover. That keeps buyer power elevated, pressuring margins and enabling price-driven switching for repeat orders.

Demand cyclicality

Construction cycles shift volume bargaining power: Insteel (net sales ~1.05 billion in 2023) faces stronger buyer leverage in downturns as customers consolidate purchases and demand price or lead-time concessions; conversely 2024 US housing starts near 1.3M units and tighter allocation in upcycles reduce buyer leverage.

- Downturns: buyers consolidate spend, win concessions

- Upcycles: allocation tightness limits buyer leverage

- Mix shift: residential vs non-residential alters negotiating dynamics

Specification influence

Engineers and owners set reinforcement specs, creating supplier lock-in when drawings name products or basis-of-design; this can force mid-project sourcing shifts and margin pressure. Securing basis-of-design or approved-list status limits buyer options, while many specs retain or equal language that preserved competition. Submittal control offers defense but does not provide immunity against substitution or change orders; U.S. construction spending topped $1.6 trillion in 2023.

- Specification control increases switching costs

- Approved-list status reduces buyer options mid-project

- or equal clauses preserve competition

- Submittal control mitigates but does not eliminate risk

Buyers drive down delivered steel prices via index benchmarking and short lead-time leverage

Buyers exert high price pressure: large contractors and precast producers benchmark via indices and quotes, with Insteel 2024 net sales ~695 million reflecting volume-driven leverage. Project bids favor lowest delivered price; buyers push index/spot discounts when steel softens. Specification control and logistics (lead times 2–6 weeks) temper switching but do not eliminate buyer leverage.

| Metric | 2024 Value |

|---|---|

| Insteel net sales | $695M |

| US housing starts | ~1.3M units |

| Lead times | 2–6 weeks |

Preview the Actual Deliverable

Insteel Industries Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for Insteel Industries you’ll receive after purchase—no placeholders or samples. The full document is fully formatted, ready for immediate download and use. What you see here is precisely the deliverable available upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Insteel Industries faces moderate supplier power due to specialized steel inputs, while buyer power is tempered by construction demand cycles and distributor relationships; rivalry is intense among steel and rebar producers, and threats from new entrants and substitutes remain low-to-moderate. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated rod suppliers

Wire rod inputs are sourced from a relatively concentrated set of North American mini-mills—notably Nucor, Steel Dynamics and Cleveland-Cliffs—which remained primary rod suppliers in 2024, increasing supplier leverage. Fewer qualified mills meeting ASTM/PCI specs heighten dependence and let consolidation tighten terms and delivery windows. Insteel must balance dual-sourcing against quality control and freight economics to manage cost and continuity.

Steel price volatility

Raw steel costs remain cyclical and volatile, with US hot-rolled coil averaging about $820 per short ton in 2024 and spot swings exceeding 25% intra-year, often outpacing finished-goods pricing. Suppliers routinely apply surcharges that compress Insteel Industries margins when demand cools, and timing mismatches between input spikes and customer price resets intensify pressure. Hedging and index-linked contracts partially mitigate exposure but do not eliminate residual basis and timing risk.

Logistics and freight

Freight is a material cost for heavy, low-value-density rod and mesh, often representing roughly 10–15% of landed cost. U.S. diesel averaged about $4.17/gal in 2024 (EIA), and fuel spikes or rail/truck capacity constraints can add 5–20% to delivered cost, amplifying supplier power. Regional proximity to mills materially affects landed economics, and disruptions frequently force premium expedited freight or higher-priced alternate sourcing.

Quality/spec compliance

PCS and WWR demand tight mechanical and weld properties, narrowing acceptable suppliers and concentrating sourcing risk; failures risk customer rejection and costly rework, so Insteel in 2024 prioritizes proven mills and long-term relationships. This raises switching costs on the supply side, while mill certifications and audits give certified suppliers measurable negotiating leverage.

- Supplier pool: constrained by PCS/WWR specs

- Cost impact: failures→rework/customer rejection

- Leverage: certifications/audits increase supplier bargaining power

Trade policy and imports

Tariffs, quotas and AD/CVD rulings have curtailed rod imports and strengthened domestic pricing power, causing fast shifts in mill order books and lead times; when imports ebb, U.S. mills capture margin and Insteel’s negotiating leverage tightens. Insteel’s options remain constrained until trade flows and enforcement normalize, pressuring near-term cost pass-through and utilization decisions.

- Trade barriers lift domestic pricing

- Rapid ripple into lead times

- Domestic mills capture margin

- Insteel constrained until normalization

Concentrated rod supply and tight PCS/WWR specs boost mill pricing amid volatile HRC

Concentrated rod supply (Nucor, Steel Dynamics, Cleveland-Cliffs) and tight PCS/WWR specs raised supplier leverage in 2024; HRC averaged ~$820/st with >25% spot swings, compressing margins. Freight (10–15% of landed cost) and diesel at ~$4.17/gal amplified delivery risk. Trade barriers reduced imports, tightening domestic mill lead times and pricing power.

| Metric | 2024 |

|---|---|

| HRC price | $820/short ton |

| Diesel | $4.17/gal |

| Freight share | 10–15% |

| Spot volatility | >25% |

What is included in the product

Tailored Porter's Five Forces analysis for Insteel Industries uncovering key drivers of competition, customer influence, and market entry risks specific to steel reinforcement products. Evaluates supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces shaping pricing, margins, and competitive positioning.

A concise Porter's Five Forces snapshot for Insteel Industries—one-sheet clarity that visualizes competitive pressure with an editable radar chart, customizable scores for evolving market data, and a clean layout ready for pitch decks or integration into broader reports.

Customers Bargaining Power

Large, knowledgeable buyers

Large precast/prestressed producers and major contractors buy steel in scale, benchmark suppliers via multiple quotes and indices, and their professional procurement teams drive price pressure; Insteel's 2024 net sales (~$695 million) underscore customer concentration and volume-based leverage. Relationship value helps but rarely fully offsets buyers' ability to demand lower margins.

Price sensitivity

Reinforcement is a significant cost in many concrete projects, often comprising a sizeable share of structural budgets and driving tight margins for contractors in 2024 as U.S. construction spending rose about 3.4% year-over-year.

Project bid environments favor lowest delivered price, so buyers leverage competitive bids and push for index-based or spot discounts when steel prices soften.

To defend premiums, Insteel must quantify and market clear value-add services—just-in-time delivery, fabrication accuracy, and warranty metrics—that justify higher per-ton prices.

Low switching costs

WWR and PCS are standardized to ASTM A1064/A1064M and ACI 318, so once a supplier meets specs switching on future orders is straightforward. Regional freight variability and lead times—often 2–6 weeks in 2024 logistics reports—pose larger hurdles than technical changeover. That keeps buyer power elevated, pressuring margins and enabling price-driven switching for repeat orders.

Demand cyclicality

Construction cycles shift volume bargaining power: Insteel (net sales ~1.05 billion in 2023) faces stronger buyer leverage in downturns as customers consolidate purchases and demand price or lead-time concessions; conversely 2024 US housing starts near 1.3M units and tighter allocation in upcycles reduce buyer leverage.

- Downturns: buyers consolidate spend, win concessions

- Upcycles: allocation tightness limits buyer leverage

- Mix shift: residential vs non-residential alters negotiating dynamics

Specification influence

Engineers and owners set reinforcement specs, creating supplier lock-in when drawings name products or basis-of-design; this can force mid-project sourcing shifts and margin pressure. Securing basis-of-design or approved-list status limits buyer options, while many specs retain or equal language that preserved competition. Submittal control offers defense but does not provide immunity against substitution or change orders; U.S. construction spending topped $1.6 trillion in 2023.

- Specification control increases switching costs

- Approved-list status reduces buyer options mid-project

- or equal clauses preserve competition

- Submittal control mitigates but does not eliminate risk

Buyers drive down delivered steel prices via index benchmarking and short lead-time leverage

Buyers exert high price pressure: large contractors and precast producers benchmark via indices and quotes, with Insteel 2024 net sales ~695 million reflecting volume-driven leverage. Project bids favor lowest delivered price; buyers push index/spot discounts when steel softens. Specification control and logistics (lead times 2–6 weeks) temper switching but do not eliminate buyer leverage.

| Metric | 2024 Value |

|---|---|

| Insteel net sales | $695M |

| US housing starts | ~1.3M units |

| Lead times | 2–6 weeks |

Preview the Actual Deliverable

Insteel Industries Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for Insteel Industries you’ll receive after purchase—no placeholders or samples. The full document is fully formatted, ready for immediate download and use. What you see here is precisely the deliverable available upon payment.