Integer Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

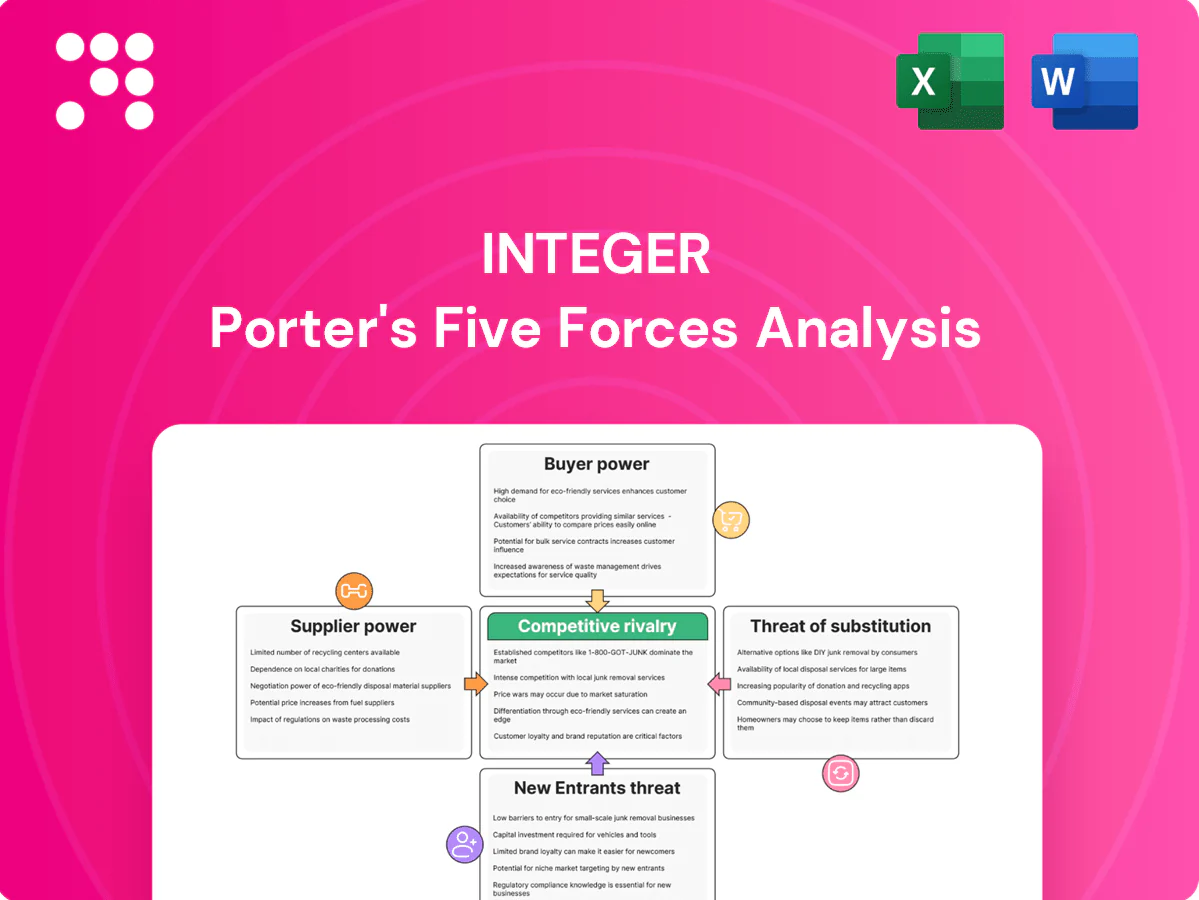

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Integer’s competitive dynamics, market pressures, and strategic advantages in detail. The full report reveals force-by-force ratings, visuals, and actionable implications to inform investment or strategic decisions—get instant access to a consultant-grade Excel and Word deliverable.

Suppliers Bargaining Power

Specialized materials concentration

Many critical inputs—nitinol, cobalt-chrome, platinum-iridium and implant-grade polymers—are supplied by a highly concentrated base, often fewer than 10 qualified vendors per material, giving suppliers pricing and allocation leverage. Scarcity and stringent qualification processes limit true substitutes, forcing Integer to pursue multi-sourcing where feasible. This concentration raises exposure during demand spikes or disruptions, historically causing material lead-time extensions and cost volatility.

Battery cells and power components

Implantable-grade lithium cells and advanced power modules are produced by a very limited set of FDA-compliant manufacturers, concentrating supply and raising supplier bargaining power. Validation and safety cycles commonly run 12–24 months, locking OEM programs to specific cells and increasing switching costs. In tight markets suppliers have secured stronger commercial terms, while multi-year offtake contracts (common in 2024) stabilize cost and supply but reduce short-term flexibility.

Regulatory-grade process equipment/services

Regulatory-grade process equipment and services—sterilization, ISO 14644 cleanroom compliance, and validated vendors under FDA 21 CFR Part 820—exert strong supplier power because noncompliance risks DHF changes and OEM re-approvals. Requalification timelines commonly involve extensive validation runs and documentation updates, tying procurement to incumbent suppliers. Any supplier swap can trigger formal design history file amendments and regulatory submissions. This entrenches dependence on current certified vendors.

Quality and traceability requirements

ISO 13485:2016 and FDA 21 CFR 820 quality requirements elevate supplier documentation and lot-traceability burdens, narrowing the eligible vendor pool; suppliers that maintain robust documentation and electronic traceability therefore gain leverage. Integer's supplier development programs aim to expand qualified sources, but regulatory audits and CAPA processes still slow rapid supplier switching.

- ISO 13485:2016 / FDA QSR increase supplier compliance

- Traceability-capable suppliers hold higher bargaining power

- Integer invests in supplier development to widen pool

- Audits and CAPAs constrain fast switching

Logistics and geopolitical exposure

Global metals and electronic components face tariff and export-control pressures—US Section 232 tariffs remain 25% on steel and 10% on aluminum—and freight and export controls (eg, semiconductor curbs amid the CHIPS Act era, $52 billion US support) let suppliers pass surcharges and extend lead times; buffer stocks and nearshoring reduce risk but raise costs, while disruptions force expedited, costly buys.

- Tariffs: 25% steel / 10% aluminum

- Export controls: semiconductor restrictions driving reshoring

- Mitigation: buffer stocks + nearshoring = higher capex/Opex

- Risk: expedited purchases at unfavorable terms

Concentrated supplier power, long validation cycles and tariffs tighten supply chains

Supplier bases are highly concentrated (often <10 qualified vendors per critical material), creating pricing and allocation leverage; validation cycles of 12–24 months raise switching costs. Multi-year offtake contracts (common in 2024) and tariffs (25% steel / 10% aluminum) add cost rigidity; CHIPS Act support ($52B) and export controls tighten electronics supply, increasing reliance on incumbent, qualified suppliers.

| Metric | Value |

|---|---|

| Qualified vendors per material | <10 |

| Validation cycle | 12–24 months |

| Tariffs | 25% steel / 10% aluminum |

| CHIPS Act funding | $52B |

What is included in the product

Tailored Porter’s Five Forces analysis for Integer that uncovers competitive drivers, buyer and supplier power, substitutes, and entry threats, identifying disruptive forces and defensive barriers to protect market share; delivered in fully editable Word format for use in investor decks, strategy reports, or academic projects.

One-sheet Porter's Five Forces for Integer simplifies competitive assessment into a single, customizable summary—ideal for fast strategic decisions and slide-ready reporting.

Customers Bargaining Power

OEM concentration

Large OEM concentration drives buyer power: Medtronic, Abbott and Boston Scientific together accounted for roughly two-thirds of implantable device procurement in 2024 (~65%), with Medtronic holding about a 40% share in CRM devices in 2023–24; their scale enforces aggressive pricing, service-level and liability terms, and losing a top program can cut an outsourced supplier’s volumes by double digits, materially affecting revenue and margins.

Dual sourcing strategies

OEMs increasingly dual-source critical components, commonly maintaining 2 suppliers to de-risk supply and continuity. Competitive bidding from dual sourcing squeezes margins and accelerates 5–10% annual cost-down roadmaps in many programs. Integer must differentiate on quality, yield, and engineering support to resist commoditization. Preferred-supplier status can temper price pressure but remains contestable.

High switching costs yet enforced

Design validations and regulatory file transfer create high switching costs—requalification typically takes 12–24 months—ordinarily favoring Integer, but OEMs plan multi-year supplier transitions to extract concessions. Despite lock-in, OEMs press for price reductions, PPV and VAVE targets (commonly 2–5% annually) and use staged transitions as leverage. Service failures can immediately trigger costly requalification initiatives and supplier audits.

Total cost and time-to-market focus

Buyers prioritize total cost of ownership, speed and reliability over unit price, demanding DFM support, rapid prototyping and stable ramp-to-volume; meeting those needs can justify premium pricing and reduces churn, while failure to deliver invites resourcing threats and supply-switching risk.

- Lifecycle focus: TCO over unit price

- Speed: rapid prototyping required

- Reliability: stable ramp-to-volume

- Outcome: premium pricing or churn

Compliance and liability pass-through

OEMs enforce stringent quality metrics, audit rights, and chargebacks for nonconformance, and routinely flow down warranty and field-action liabilities to suppliers, shifting operational and financial risk onto Integer. This pass-through increases exposure to retrospective chargebacks and recall costs, making tight supplier controls and traceability critical. Strong process controls and documented compliance reduce audit findings and limit liability leakage to Integer.

- OEM audit rights: enforced compliance

- Chargebacks: financial risk transferred

- Warranty/field actions: liability pass-through

- Mitigation: robust process controls & traceability

High OEM concentration and dual-sourcing squeeze supplier margins

High OEM concentration (Medtronic/Abbott/Boston Scientific ≈65% of implantable procurement in 2024; Medtronic ~40% CRM share in 2023–24) gives buyers strong price and term leverage. Dual-sourcing (commonly 2 suppliers) and 5–10% program cost-downs pressure margins; preferred-supplier status mitigates but is contestable. Requalification (12–24 months) raises switching costs yet OEMs use staged transitions to extract 2–5% annual PPV/VAVE. Stringent audits, chargebacks and liability pass-through amplify supplier risk.

| Metric | Value |

|---|---|

| OEM top-3 share (2024) | ~65% |

| Medtronic CRM share (2023–24) | ~40% |

| Dual sourcing | 2 suppliers |

| Requalification | 12–24 months |

| Annual cost-down | 2–10% |

Same Document Delivered

Integer Porter's Five Forces Analysis

This preview shows the exact Integer Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The file is the professionally written, fully formatted document ready for download and use the moment you buy. What you see is precisely what you’ll get.

A Must-Have Tool for Decision-Makers

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Integer’s competitive dynamics, market pressures, and strategic advantages in detail. The full report reveals force-by-force ratings, visuals, and actionable implications to inform investment or strategic decisions—get instant access to a consultant-grade Excel and Word deliverable.

Suppliers Bargaining Power

Specialized materials concentration

Many critical inputs—nitinol, cobalt-chrome, platinum-iridium and implant-grade polymers—are supplied by a highly concentrated base, often fewer than 10 qualified vendors per material, giving suppliers pricing and allocation leverage. Scarcity and stringent qualification processes limit true substitutes, forcing Integer to pursue multi-sourcing where feasible. This concentration raises exposure during demand spikes or disruptions, historically causing material lead-time extensions and cost volatility.

Battery cells and power components

Implantable-grade lithium cells and advanced power modules are produced by a very limited set of FDA-compliant manufacturers, concentrating supply and raising supplier bargaining power. Validation and safety cycles commonly run 12–24 months, locking OEM programs to specific cells and increasing switching costs. In tight markets suppliers have secured stronger commercial terms, while multi-year offtake contracts (common in 2024) stabilize cost and supply but reduce short-term flexibility.

Regulatory-grade process equipment/services

Regulatory-grade process equipment and services—sterilization, ISO 14644 cleanroom compliance, and validated vendors under FDA 21 CFR Part 820—exert strong supplier power because noncompliance risks DHF changes and OEM re-approvals. Requalification timelines commonly involve extensive validation runs and documentation updates, tying procurement to incumbent suppliers. Any supplier swap can trigger formal design history file amendments and regulatory submissions. This entrenches dependence on current certified vendors.

Quality and traceability requirements

ISO 13485:2016 and FDA 21 CFR 820 quality requirements elevate supplier documentation and lot-traceability burdens, narrowing the eligible vendor pool; suppliers that maintain robust documentation and electronic traceability therefore gain leverage. Integer's supplier development programs aim to expand qualified sources, but regulatory audits and CAPA processes still slow rapid supplier switching.

- ISO 13485:2016 / FDA QSR increase supplier compliance

- Traceability-capable suppliers hold higher bargaining power

- Integer invests in supplier development to widen pool

- Audits and CAPAs constrain fast switching

Logistics and geopolitical exposure

Global metals and electronic components face tariff and export-control pressures—US Section 232 tariffs remain 25% on steel and 10% on aluminum—and freight and export controls (eg, semiconductor curbs amid the CHIPS Act era, $52 billion US support) let suppliers pass surcharges and extend lead times; buffer stocks and nearshoring reduce risk but raise costs, while disruptions force expedited, costly buys.

- Tariffs: 25% steel / 10% aluminum

- Export controls: semiconductor restrictions driving reshoring

- Mitigation: buffer stocks + nearshoring = higher capex/Opex

- Risk: expedited purchases at unfavorable terms

Concentrated supplier power, long validation cycles and tariffs tighten supply chains

Supplier bases are highly concentrated (often <10 qualified vendors per critical material), creating pricing and allocation leverage; validation cycles of 12–24 months raise switching costs. Multi-year offtake contracts (common in 2024) and tariffs (25% steel / 10% aluminum) add cost rigidity; CHIPS Act support ($52B) and export controls tighten electronics supply, increasing reliance on incumbent, qualified suppliers.

| Metric | Value |

|---|---|

| Qualified vendors per material | <10 |

| Validation cycle | 12–24 months |

| Tariffs | 25% steel / 10% aluminum |

| CHIPS Act funding | $52B |

What is included in the product

Tailored Porter’s Five Forces analysis for Integer that uncovers competitive drivers, buyer and supplier power, substitutes, and entry threats, identifying disruptive forces and defensive barriers to protect market share; delivered in fully editable Word format for use in investor decks, strategy reports, or academic projects.

One-sheet Porter's Five Forces for Integer simplifies competitive assessment into a single, customizable summary—ideal for fast strategic decisions and slide-ready reporting.

Customers Bargaining Power

OEM concentration

Large OEM concentration drives buyer power: Medtronic, Abbott and Boston Scientific together accounted for roughly two-thirds of implantable device procurement in 2024 (~65%), with Medtronic holding about a 40% share in CRM devices in 2023–24; their scale enforces aggressive pricing, service-level and liability terms, and losing a top program can cut an outsourced supplier’s volumes by double digits, materially affecting revenue and margins.

Dual sourcing strategies

OEMs increasingly dual-source critical components, commonly maintaining 2 suppliers to de-risk supply and continuity. Competitive bidding from dual sourcing squeezes margins and accelerates 5–10% annual cost-down roadmaps in many programs. Integer must differentiate on quality, yield, and engineering support to resist commoditization. Preferred-supplier status can temper price pressure but remains contestable.

High switching costs yet enforced

Design validations and regulatory file transfer create high switching costs—requalification typically takes 12–24 months—ordinarily favoring Integer, but OEMs plan multi-year supplier transitions to extract concessions. Despite lock-in, OEMs press for price reductions, PPV and VAVE targets (commonly 2–5% annually) and use staged transitions as leverage. Service failures can immediately trigger costly requalification initiatives and supplier audits.

Total cost and time-to-market focus

Buyers prioritize total cost of ownership, speed and reliability over unit price, demanding DFM support, rapid prototyping and stable ramp-to-volume; meeting those needs can justify premium pricing and reduces churn, while failure to deliver invites resourcing threats and supply-switching risk.

- Lifecycle focus: TCO over unit price

- Speed: rapid prototyping required

- Reliability: stable ramp-to-volume

- Outcome: premium pricing or churn

Compliance and liability pass-through

OEMs enforce stringent quality metrics, audit rights, and chargebacks for nonconformance, and routinely flow down warranty and field-action liabilities to suppliers, shifting operational and financial risk onto Integer. This pass-through increases exposure to retrospective chargebacks and recall costs, making tight supplier controls and traceability critical. Strong process controls and documented compliance reduce audit findings and limit liability leakage to Integer.

- OEM audit rights: enforced compliance

- Chargebacks: financial risk transferred

- Warranty/field actions: liability pass-through

- Mitigation: robust process controls & traceability

High OEM concentration and dual-sourcing squeeze supplier margins

High OEM concentration (Medtronic/Abbott/Boston Scientific ≈65% of implantable procurement in 2024; Medtronic ~40% CRM share in 2023–24) gives buyers strong price and term leverage. Dual-sourcing (commonly 2 suppliers) and 5–10% program cost-downs pressure margins; preferred-supplier status mitigates but is contestable. Requalification (12–24 months) raises switching costs yet OEMs use staged transitions to extract 2–5% annual PPV/VAVE. Stringent audits, chargebacks and liability pass-through amplify supplier risk.

| Metric | Value |

|---|---|

| OEM top-3 share (2024) | ~65% |

| Medtronic CRM share (2023–24) | ~40% |

| Dual sourcing | 2 suppliers |

| Requalification | 12–24 months |

| Annual cost-down | 2–10% |

Same Document Delivered

Integer Porter's Five Forces Analysis

This preview shows the exact Integer Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The file is the professionally written, fully formatted document ready for download and use the moment you buy. What you see is precisely what you’ll get.

Description

A Must-Have Tool for Decision-Makers

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Integer’s competitive dynamics, market pressures, and strategic advantages in detail. The full report reveals force-by-force ratings, visuals, and actionable implications to inform investment or strategic decisions—get instant access to a consultant-grade Excel and Word deliverable.

Suppliers Bargaining Power

Specialized materials concentration

Many critical inputs—nitinol, cobalt-chrome, platinum-iridium and implant-grade polymers—are supplied by a highly concentrated base, often fewer than 10 qualified vendors per material, giving suppliers pricing and allocation leverage. Scarcity and stringent qualification processes limit true substitutes, forcing Integer to pursue multi-sourcing where feasible. This concentration raises exposure during demand spikes or disruptions, historically causing material lead-time extensions and cost volatility.

Battery cells and power components

Implantable-grade lithium cells and advanced power modules are produced by a very limited set of FDA-compliant manufacturers, concentrating supply and raising supplier bargaining power. Validation and safety cycles commonly run 12–24 months, locking OEM programs to specific cells and increasing switching costs. In tight markets suppliers have secured stronger commercial terms, while multi-year offtake contracts (common in 2024) stabilize cost and supply but reduce short-term flexibility.

Regulatory-grade process equipment/services

Regulatory-grade process equipment and services—sterilization, ISO 14644 cleanroom compliance, and validated vendors under FDA 21 CFR Part 820—exert strong supplier power because noncompliance risks DHF changes and OEM re-approvals. Requalification timelines commonly involve extensive validation runs and documentation updates, tying procurement to incumbent suppliers. Any supplier swap can trigger formal design history file amendments and regulatory submissions. This entrenches dependence on current certified vendors.

Quality and traceability requirements

ISO 13485:2016 and FDA 21 CFR 820 quality requirements elevate supplier documentation and lot-traceability burdens, narrowing the eligible vendor pool; suppliers that maintain robust documentation and electronic traceability therefore gain leverage. Integer's supplier development programs aim to expand qualified sources, but regulatory audits and CAPA processes still slow rapid supplier switching.

- ISO 13485:2016 / FDA QSR increase supplier compliance

- Traceability-capable suppliers hold higher bargaining power

- Integer invests in supplier development to widen pool

- Audits and CAPAs constrain fast switching

Logistics and geopolitical exposure

Global metals and electronic components face tariff and export-control pressures—US Section 232 tariffs remain 25% on steel and 10% on aluminum—and freight and export controls (eg, semiconductor curbs amid the CHIPS Act era, $52 billion US support) let suppliers pass surcharges and extend lead times; buffer stocks and nearshoring reduce risk but raise costs, while disruptions force expedited, costly buys.

- Tariffs: 25% steel / 10% aluminum

- Export controls: semiconductor restrictions driving reshoring

- Mitigation: buffer stocks + nearshoring = higher capex/Opex

- Risk: expedited purchases at unfavorable terms

Concentrated supplier power, long validation cycles and tariffs tighten supply chains

Supplier bases are highly concentrated (often <10 qualified vendors per critical material), creating pricing and allocation leverage; validation cycles of 12–24 months raise switching costs. Multi-year offtake contracts (common in 2024) and tariffs (25% steel / 10% aluminum) add cost rigidity; CHIPS Act support ($52B) and export controls tighten electronics supply, increasing reliance on incumbent, qualified suppliers.

| Metric | Value |

|---|---|

| Qualified vendors per material | <10 |

| Validation cycle | 12–24 months |

| Tariffs | 25% steel / 10% aluminum |

| CHIPS Act funding | $52B |

What is included in the product

Tailored Porter’s Five Forces analysis for Integer that uncovers competitive drivers, buyer and supplier power, substitutes, and entry threats, identifying disruptive forces and defensive barriers to protect market share; delivered in fully editable Word format for use in investor decks, strategy reports, or academic projects.

One-sheet Porter's Five Forces for Integer simplifies competitive assessment into a single, customizable summary—ideal for fast strategic decisions and slide-ready reporting.

Customers Bargaining Power

OEM concentration

Large OEM concentration drives buyer power: Medtronic, Abbott and Boston Scientific together accounted for roughly two-thirds of implantable device procurement in 2024 (~65%), with Medtronic holding about a 40% share in CRM devices in 2023–24; their scale enforces aggressive pricing, service-level and liability terms, and losing a top program can cut an outsourced supplier’s volumes by double digits, materially affecting revenue and margins.

Dual sourcing strategies

OEMs increasingly dual-source critical components, commonly maintaining 2 suppliers to de-risk supply and continuity. Competitive bidding from dual sourcing squeezes margins and accelerates 5–10% annual cost-down roadmaps in many programs. Integer must differentiate on quality, yield, and engineering support to resist commoditization. Preferred-supplier status can temper price pressure but remains contestable.

High switching costs yet enforced

Design validations and regulatory file transfer create high switching costs—requalification typically takes 12–24 months—ordinarily favoring Integer, but OEMs plan multi-year supplier transitions to extract concessions. Despite lock-in, OEMs press for price reductions, PPV and VAVE targets (commonly 2–5% annually) and use staged transitions as leverage. Service failures can immediately trigger costly requalification initiatives and supplier audits.

Total cost and time-to-market focus

Buyers prioritize total cost of ownership, speed and reliability over unit price, demanding DFM support, rapid prototyping and stable ramp-to-volume; meeting those needs can justify premium pricing and reduces churn, while failure to deliver invites resourcing threats and supply-switching risk.

- Lifecycle focus: TCO over unit price

- Speed: rapid prototyping required

- Reliability: stable ramp-to-volume

- Outcome: premium pricing or churn

Compliance and liability pass-through

OEMs enforce stringent quality metrics, audit rights, and chargebacks for nonconformance, and routinely flow down warranty and field-action liabilities to suppliers, shifting operational and financial risk onto Integer. This pass-through increases exposure to retrospective chargebacks and recall costs, making tight supplier controls and traceability critical. Strong process controls and documented compliance reduce audit findings and limit liability leakage to Integer.

- OEM audit rights: enforced compliance

- Chargebacks: financial risk transferred

- Warranty/field actions: liability pass-through

- Mitigation: robust process controls & traceability

High OEM concentration and dual-sourcing squeeze supplier margins

High OEM concentration (Medtronic/Abbott/Boston Scientific ≈65% of implantable procurement in 2024; Medtronic ~40% CRM share in 2023–24) gives buyers strong price and term leverage. Dual-sourcing (commonly 2 suppliers) and 5–10% program cost-downs pressure margins; preferred-supplier status mitigates but is contestable. Requalification (12–24 months) raises switching costs yet OEMs use staged transitions to extract 2–5% annual PPV/VAVE. Stringent audits, chargebacks and liability pass-through amplify supplier risk.

| Metric | Value |

|---|---|

| OEM top-3 share (2024) | ~65% |

| Medtronic CRM share (2023–24) | ~40% |

| Dual sourcing | 2 suppliers |

| Requalification | 12–24 months |

| Annual cost-down | 2–10% |

Same Document Delivered

Integer Porter's Five Forces Analysis

This preview shows the exact Integer Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The file is the professionally written, fully formatted document ready for download and use the moment you buy. What you see is precisely what you’ll get.