Integral Diagnostics PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Integral Diagnostics—concise yet sharply focused on political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists seeking actionable intelligence. Purchase the full report to unlock detailed insights and ready-to-use recommendations.

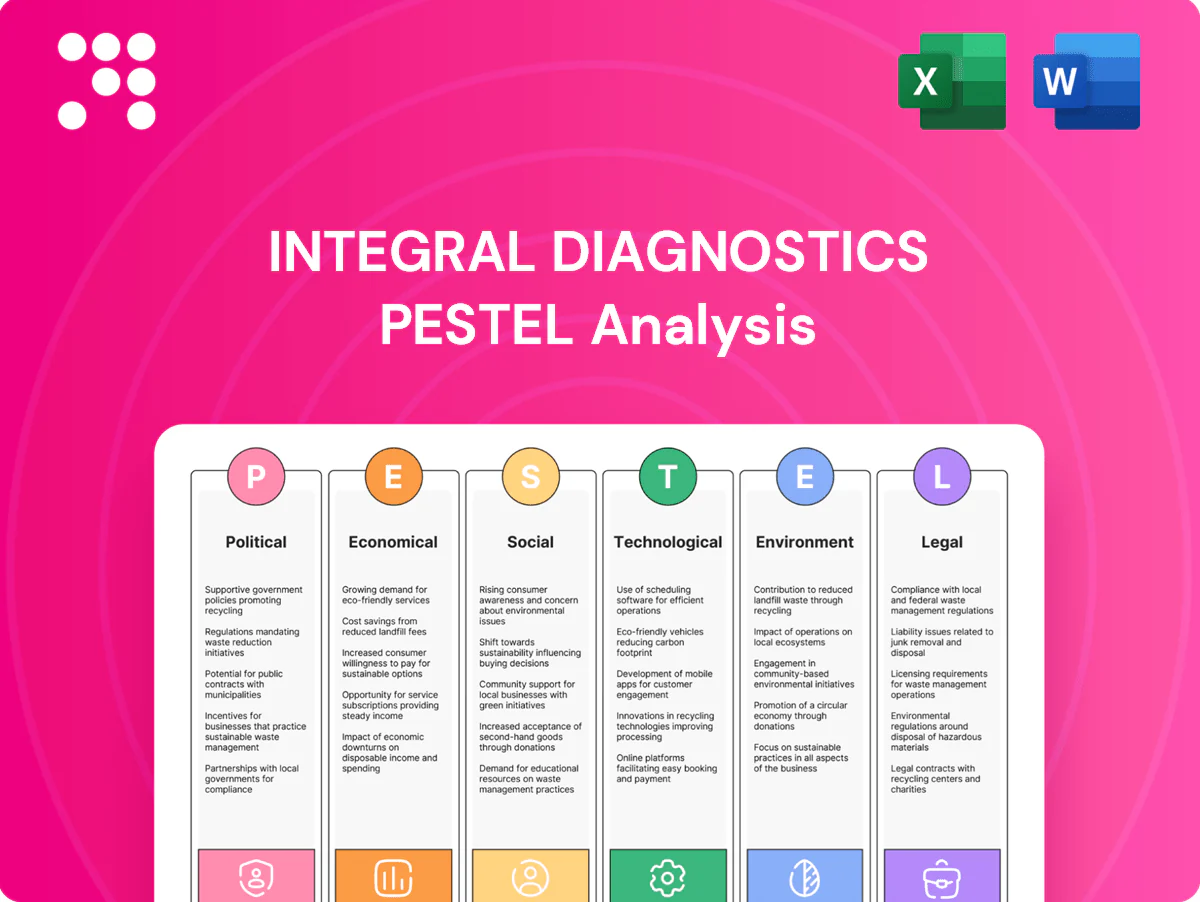

Political factors

Government imaging rebates

AU Medicare MBS and NZ public funding determine scan volumes and set prices, directly anchoring Integral Diagnostics’ reimbursement base; any MBS indexation change immediately shifts margins and alters capital planning timeframes. Sustained advocacy and strict compliance alignment with Commonwealth and DHB rules are required to secure long-term reimbursement stability. Scenario planning should model rebate freezes, 0% indexation, and targeted increases to stress-test cash flow and capex.

Public–private partnerships

Hospital contracts and outsourcing policies directly shape Integral Diagnostics site footprint through awarded service agreements with public hospitals and outpatient networks. Tender outcomes increasingly hinge on demonstrable service quality, geographic access and cost-efficiency. Strong relationship management with regional health districts and Te Whatu Ora (est. 2022) is essential. Election cycles (eg NZ Oct 14 2023, AU May 2022) can reset PPP priorities and funding.

Workforce immigration settings

Radiologist and technologist shortages hinge on visa pathways: slower processing restricts throughput and forces locum hires, raising operational costs; Australia set its 2023–24 migration planning level at 195,000, underscoring policy shifts that affect supply. Faster credentialing enables regional expansion and utilisation of overseas specialists, so monitor Skilled Occupation Lists and bilateral recognition agreements for capacity and cost impact.

Regional health policy shifts

State and New Zealand regional directives increasingly shape modality mix and clinic locations, with many jurisdictions emphasizing MRI and CT access to meet diagnostic standards. Screening programs and waitlist targets, such as Category 1 treated within 30 days, can lift demand for imaging services and extend revenue streams. Budget reallocations sometimes prioritize public capacity, pressuring private providers to partner or compete; engage early in policy consultations to influence placement and funding decisions.

- Policy drivers: state/NZ directives

- Demand lift: screening + 30‑day Cat 1 targets

- Risk: public budget shift vs private

- Action: early engagement in consultations

Health infrastructure investment

Government capital programs for hospitals shape colocations for Integral Diagnostics, as public investment can determine where demand concentrates and whether private imaging is viable. Grants and regional uplift funds reduce site-level greenfield risk and can accelerate rollouts of new clinics. New public scanners in hospitals can cannibalize private outpatient volumes, so IDX must track the public capital pipeline to time openings and equipment upgrades.

- Tag: colocations

- Tag: de-risking

- Tag: public-cannibalisation

- Tag: pipeline-timing

Medicare indexation, NZ funding and visa caps dictate imaging margins, capacity and site access

AU Medicare MBS indexation and NZ public funding directly set reimbursement and scan volumes; any MBS change shifts margins and capex timing. Hospital tenders and Te Whatu Ora (est. 2022) rules determine site access; election cycles (NZ Oct 14 2023; AU May 2022) reset PPP priorities. Workforce hinges on visa policy (AU 2023–24 migration cap 195,000). Monitor public capital pipelines for cannibalisation risk.

| Factor | Key data |

|---|---|

| Migrant cap | 195,000 (AU 2023–24) |

| Te Whatu Ora | Established 2022 |

| NZ election | Oct 14 2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect Integral Diagnostics across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific context. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios in clean, presentation-ready format.

A concise, shareable PESTLE summary for Integral Diagnostics that’s visually segmented for quick interpretation, ideal for meetings, slides, and cross-team alignment, and editable for region-specific notes.

Economic factors

Procedure volume cycles

Procedure volumes at Integral Diagnostics track macro growth and labor markets: Australia’s unemployment was 4.1% (ABS, June 2025) and Westpac–Melbourne Institute consumer confidence hovered near 82 in mid‑2025, both moderating self‑pay and insured scan demand. Elective imaging follows economic cycles, with pipeline swings amplifying during downturns and recoveries. Public elective surgery backlogs (hundreds of thousands in 2024) can create sudden surges. Flexible staffing models are essential to absorb this volatility.

Inflation and wage pressure

Skilled imaging labor costs have risen faster than Australia’s CPI (around 4.1% in 2024), squeezing margins as technician and sonographer wage growth outpaces general inflation. Service contracts, energy and consumables—driven by supply-chain and energy volatility—continue to inflate OPEX. Price pass-through is constrained by fixed private and government rebates, so lean operations and automation investments are critical to protect margins.

Capex intensity and rates

MRI replacements typically cost around AUD 2–4m and CT upgrades AUD 0.5–2m, creating large, recurring capex for Integral Diagnostics. RBA cash rate was ~4.35% in 2024, lifting WACC and internal hurdle rates for capital projects. Vendor financing and multi‑year service packs (commonly 3–7 years) smooth cash flow and capex timing. Optimizing fleet lifecycle (7–10 year refreshes) and maintaining 95–98% uptime maximizes ROI.

Payer mix dynamics

Payer mix—balance among Medicare/public, private insurers and out-of-pocket patients—directly drives yields; private-pay cases typically generate higher margins while public-funded cases offer volume stability. Insurer contract terms and prior‑authorization requirements shape exam protocols and throughput, affecting per‑case revenue and volumes. With ~45% of Australians covered by private health insurance (APRA 2024), shifts toward public funding compress prices but stabilize demand; diversifying referrers reduces concentration risk.

- Medicare/public: price stability, lower yield

- Private insurers: higher yield, contract risk

- Out‑of‑pocket: margin upside, volume sensitivity

- Action: diversify referrers to cut concentration risk

FX and supply chain

Imported imaging equipment ties Integral Diagnostics' procurement costs to USD/EUR; AUD/USD was ~0.66 and EUR/AUD ~1.55 in June 2025, so currency swings materially affect purchase timing and spare-parts pricing. Global logistics disruptions continue to cause 4–12 week delays, extending service downtime. Hedge key orders and hold 3–6 months of critical spares to reduce interruption risk.

- FX exposure: USD/EUR pricing

- Rates: AUD/USD ~0.66 (Jun 2025)

- Delays: 4–12 week shipping impact

- Mitigation: hedge orders, 3–6 months spares

Medicare indexation, NZ funding and visa caps dictate imaging margins, capacity and site access

Procedure volumes tied to macro: unemployment 4.1% (ABS Jun 2025) and consumer confidence ~82 compress elective demand; private cover ~45% (APRA 2024) shapes yields. Costs rising: CPI ~4.1% (2024) and technician wages outpace inflation, squeezing margins. Capex and rates matter: MRI AUD2–4m, RBA cash rate ~4.35% (2024) raises WACC; FX AUD/USD ~0.66 (Jun 2025) lifts import costs.

| Metric | Value | Impact |

|---|---|---|

| Unemployment | 4.1% | Volume sensitivity |

| CPI (2024) | ~4.1% | Higher OPEX |

| MRI cost | AUD2–4m | High capex |

| AUD/USD | ~0.66 | Import risk |

Same Document Delivered

Integral Diagnostics PESTLE Analysis

The preview shown is the exact Integral Diagnostics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file is the final version with complete political, economic, social, technological, legal and environmental insights. No placeholders, no surprises; download it immediately after checkout.

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Integral Diagnostics—concise yet sharply focused on political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists seeking actionable intelligence. Purchase the full report to unlock detailed insights and ready-to-use recommendations.

Political factors

Government imaging rebates

AU Medicare MBS and NZ public funding determine scan volumes and set prices, directly anchoring Integral Diagnostics’ reimbursement base; any MBS indexation change immediately shifts margins and alters capital planning timeframes. Sustained advocacy and strict compliance alignment with Commonwealth and DHB rules are required to secure long-term reimbursement stability. Scenario planning should model rebate freezes, 0% indexation, and targeted increases to stress-test cash flow and capex.

Public–private partnerships

Hospital contracts and outsourcing policies directly shape Integral Diagnostics site footprint through awarded service agreements with public hospitals and outpatient networks. Tender outcomes increasingly hinge on demonstrable service quality, geographic access and cost-efficiency. Strong relationship management with regional health districts and Te Whatu Ora (est. 2022) is essential. Election cycles (eg NZ Oct 14 2023, AU May 2022) can reset PPP priorities and funding.

Workforce immigration settings

Radiologist and technologist shortages hinge on visa pathways: slower processing restricts throughput and forces locum hires, raising operational costs; Australia set its 2023–24 migration planning level at 195,000, underscoring policy shifts that affect supply. Faster credentialing enables regional expansion and utilisation of overseas specialists, so monitor Skilled Occupation Lists and bilateral recognition agreements for capacity and cost impact.

Regional health policy shifts

State and New Zealand regional directives increasingly shape modality mix and clinic locations, with many jurisdictions emphasizing MRI and CT access to meet diagnostic standards. Screening programs and waitlist targets, such as Category 1 treated within 30 days, can lift demand for imaging services and extend revenue streams. Budget reallocations sometimes prioritize public capacity, pressuring private providers to partner or compete; engage early in policy consultations to influence placement and funding decisions.

- Policy drivers: state/NZ directives

- Demand lift: screening + 30‑day Cat 1 targets

- Risk: public budget shift vs private

- Action: early engagement in consultations

Health infrastructure investment

Government capital programs for hospitals shape colocations for Integral Diagnostics, as public investment can determine where demand concentrates and whether private imaging is viable. Grants and regional uplift funds reduce site-level greenfield risk and can accelerate rollouts of new clinics. New public scanners in hospitals can cannibalize private outpatient volumes, so IDX must track the public capital pipeline to time openings and equipment upgrades.

- Tag: colocations

- Tag: de-risking

- Tag: public-cannibalisation

- Tag: pipeline-timing

Medicare indexation, NZ funding and visa caps dictate imaging margins, capacity and site access

AU Medicare MBS indexation and NZ public funding directly set reimbursement and scan volumes; any MBS change shifts margins and capex timing. Hospital tenders and Te Whatu Ora (est. 2022) rules determine site access; election cycles (NZ Oct 14 2023; AU May 2022) reset PPP priorities. Workforce hinges on visa policy (AU 2023–24 migration cap 195,000). Monitor public capital pipelines for cannibalisation risk.

| Factor | Key data |

|---|---|

| Migrant cap | 195,000 (AU 2023–24) |

| Te Whatu Ora | Established 2022 |

| NZ election | Oct 14 2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect Integral Diagnostics across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific context. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios in clean, presentation-ready format.

A concise, shareable PESTLE summary for Integral Diagnostics that’s visually segmented for quick interpretation, ideal for meetings, slides, and cross-team alignment, and editable for region-specific notes.

Economic factors

Procedure volume cycles

Procedure volumes at Integral Diagnostics track macro growth and labor markets: Australia’s unemployment was 4.1% (ABS, June 2025) and Westpac–Melbourne Institute consumer confidence hovered near 82 in mid‑2025, both moderating self‑pay and insured scan demand. Elective imaging follows economic cycles, with pipeline swings amplifying during downturns and recoveries. Public elective surgery backlogs (hundreds of thousands in 2024) can create sudden surges. Flexible staffing models are essential to absorb this volatility.

Inflation and wage pressure

Skilled imaging labor costs have risen faster than Australia’s CPI (around 4.1% in 2024), squeezing margins as technician and sonographer wage growth outpaces general inflation. Service contracts, energy and consumables—driven by supply-chain and energy volatility—continue to inflate OPEX. Price pass-through is constrained by fixed private and government rebates, so lean operations and automation investments are critical to protect margins.

Capex intensity and rates

MRI replacements typically cost around AUD 2–4m and CT upgrades AUD 0.5–2m, creating large, recurring capex for Integral Diagnostics. RBA cash rate was ~4.35% in 2024, lifting WACC and internal hurdle rates for capital projects. Vendor financing and multi‑year service packs (commonly 3–7 years) smooth cash flow and capex timing. Optimizing fleet lifecycle (7–10 year refreshes) and maintaining 95–98% uptime maximizes ROI.

Payer mix dynamics

Payer mix—balance among Medicare/public, private insurers and out-of-pocket patients—directly drives yields; private-pay cases typically generate higher margins while public-funded cases offer volume stability. Insurer contract terms and prior‑authorization requirements shape exam protocols and throughput, affecting per‑case revenue and volumes. With ~45% of Australians covered by private health insurance (APRA 2024), shifts toward public funding compress prices but stabilize demand; diversifying referrers reduces concentration risk.

- Medicare/public: price stability, lower yield

- Private insurers: higher yield, contract risk

- Out‑of‑pocket: margin upside, volume sensitivity

- Action: diversify referrers to cut concentration risk

FX and supply chain

Imported imaging equipment ties Integral Diagnostics' procurement costs to USD/EUR; AUD/USD was ~0.66 and EUR/AUD ~1.55 in June 2025, so currency swings materially affect purchase timing and spare-parts pricing. Global logistics disruptions continue to cause 4–12 week delays, extending service downtime. Hedge key orders and hold 3–6 months of critical spares to reduce interruption risk.

- FX exposure: USD/EUR pricing

- Rates: AUD/USD ~0.66 (Jun 2025)

- Delays: 4–12 week shipping impact

- Mitigation: hedge orders, 3–6 months spares

Medicare indexation, NZ funding and visa caps dictate imaging margins, capacity and site access

Procedure volumes tied to macro: unemployment 4.1% (ABS Jun 2025) and consumer confidence ~82 compress elective demand; private cover ~45% (APRA 2024) shapes yields. Costs rising: CPI ~4.1% (2024) and technician wages outpace inflation, squeezing margins. Capex and rates matter: MRI AUD2–4m, RBA cash rate ~4.35% (2024) raises WACC; FX AUD/USD ~0.66 (Jun 2025) lifts import costs.

| Metric | Value | Impact |

|---|---|---|

| Unemployment | 4.1% | Volume sensitivity |

| CPI (2024) | ~4.1% | Higher OPEX |

| MRI cost | AUD2–4m | High capex |

| AUD/USD | ~0.66 | Import risk |

Same Document Delivered

Integral Diagnostics PESTLE Analysis

The preview shown is the exact Integral Diagnostics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file is the final version with complete political, economic, social, technological, legal and environmental insights. No placeholders, no surprises; download it immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Integral Diagnostics—concise yet sharply focused on political, economic, social, technological, legal, and environmental forces shaping its future. Ideal for investors and strategists seeking actionable intelligence. Purchase the full report to unlock detailed insights and ready-to-use recommendations.

Political factors

Government imaging rebates

AU Medicare MBS and NZ public funding determine scan volumes and set prices, directly anchoring Integral Diagnostics’ reimbursement base; any MBS indexation change immediately shifts margins and alters capital planning timeframes. Sustained advocacy and strict compliance alignment with Commonwealth and DHB rules are required to secure long-term reimbursement stability. Scenario planning should model rebate freezes, 0% indexation, and targeted increases to stress-test cash flow and capex.

Public–private partnerships

Hospital contracts and outsourcing policies directly shape Integral Diagnostics site footprint through awarded service agreements with public hospitals and outpatient networks. Tender outcomes increasingly hinge on demonstrable service quality, geographic access and cost-efficiency. Strong relationship management with regional health districts and Te Whatu Ora (est. 2022) is essential. Election cycles (eg NZ Oct 14 2023, AU May 2022) can reset PPP priorities and funding.

Workforce immigration settings

Radiologist and technologist shortages hinge on visa pathways: slower processing restricts throughput and forces locum hires, raising operational costs; Australia set its 2023–24 migration planning level at 195,000, underscoring policy shifts that affect supply. Faster credentialing enables regional expansion and utilisation of overseas specialists, so monitor Skilled Occupation Lists and bilateral recognition agreements for capacity and cost impact.

Regional health policy shifts

State and New Zealand regional directives increasingly shape modality mix and clinic locations, with many jurisdictions emphasizing MRI and CT access to meet diagnostic standards. Screening programs and waitlist targets, such as Category 1 treated within 30 days, can lift demand for imaging services and extend revenue streams. Budget reallocations sometimes prioritize public capacity, pressuring private providers to partner or compete; engage early in policy consultations to influence placement and funding decisions.

- Policy drivers: state/NZ directives

- Demand lift: screening + 30‑day Cat 1 targets

- Risk: public budget shift vs private

- Action: early engagement in consultations

Health infrastructure investment

Government capital programs for hospitals shape colocations for Integral Diagnostics, as public investment can determine where demand concentrates and whether private imaging is viable. Grants and regional uplift funds reduce site-level greenfield risk and can accelerate rollouts of new clinics. New public scanners in hospitals can cannibalize private outpatient volumes, so IDX must track the public capital pipeline to time openings and equipment upgrades.

- Tag: colocations

- Tag: de-risking

- Tag: public-cannibalisation

- Tag: pipeline-timing

Medicare indexation, NZ funding and visa caps dictate imaging margins, capacity and site access

AU Medicare MBS indexation and NZ public funding directly set reimbursement and scan volumes; any MBS change shifts margins and capex timing. Hospital tenders and Te Whatu Ora (est. 2022) rules determine site access; election cycles (NZ Oct 14 2023; AU May 2022) reset PPP priorities. Workforce hinges on visa policy (AU 2023–24 migration cap 195,000). Monitor public capital pipelines for cannibalisation risk.

| Factor | Key data |

|---|---|

| Migrant cap | 195,000 (AU 2023–24) |

| Te Whatu Ora | Established 2022 |

| NZ election | Oct 14 2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect Integral Diagnostics across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific context. Designed for executives and investors, it highlights threats, opportunities and forward-looking scenarios in clean, presentation-ready format.

A concise, shareable PESTLE summary for Integral Diagnostics that’s visually segmented for quick interpretation, ideal for meetings, slides, and cross-team alignment, and editable for region-specific notes.

Economic factors

Procedure volume cycles

Procedure volumes at Integral Diagnostics track macro growth and labor markets: Australia’s unemployment was 4.1% (ABS, June 2025) and Westpac–Melbourne Institute consumer confidence hovered near 82 in mid‑2025, both moderating self‑pay and insured scan demand. Elective imaging follows economic cycles, with pipeline swings amplifying during downturns and recoveries. Public elective surgery backlogs (hundreds of thousands in 2024) can create sudden surges. Flexible staffing models are essential to absorb this volatility.

Inflation and wage pressure

Skilled imaging labor costs have risen faster than Australia’s CPI (around 4.1% in 2024), squeezing margins as technician and sonographer wage growth outpaces general inflation. Service contracts, energy and consumables—driven by supply-chain and energy volatility—continue to inflate OPEX. Price pass-through is constrained by fixed private and government rebates, so lean operations and automation investments are critical to protect margins.

Capex intensity and rates

MRI replacements typically cost around AUD 2–4m and CT upgrades AUD 0.5–2m, creating large, recurring capex for Integral Diagnostics. RBA cash rate was ~4.35% in 2024, lifting WACC and internal hurdle rates for capital projects. Vendor financing and multi‑year service packs (commonly 3–7 years) smooth cash flow and capex timing. Optimizing fleet lifecycle (7–10 year refreshes) and maintaining 95–98% uptime maximizes ROI.

Payer mix dynamics

Payer mix—balance among Medicare/public, private insurers and out-of-pocket patients—directly drives yields; private-pay cases typically generate higher margins while public-funded cases offer volume stability. Insurer contract terms and prior‑authorization requirements shape exam protocols and throughput, affecting per‑case revenue and volumes. With ~45% of Australians covered by private health insurance (APRA 2024), shifts toward public funding compress prices but stabilize demand; diversifying referrers reduces concentration risk.

- Medicare/public: price stability, lower yield

- Private insurers: higher yield, contract risk

- Out‑of‑pocket: margin upside, volume sensitivity

- Action: diversify referrers to cut concentration risk

FX and supply chain

Imported imaging equipment ties Integral Diagnostics' procurement costs to USD/EUR; AUD/USD was ~0.66 and EUR/AUD ~1.55 in June 2025, so currency swings materially affect purchase timing and spare-parts pricing. Global logistics disruptions continue to cause 4–12 week delays, extending service downtime. Hedge key orders and hold 3–6 months of critical spares to reduce interruption risk.

- FX exposure: USD/EUR pricing

- Rates: AUD/USD ~0.66 (Jun 2025)

- Delays: 4–12 week shipping impact

- Mitigation: hedge orders, 3–6 months spares

Medicare indexation, NZ funding and visa caps dictate imaging margins, capacity and site access

Procedure volumes tied to macro: unemployment 4.1% (ABS Jun 2025) and consumer confidence ~82 compress elective demand; private cover ~45% (APRA 2024) shapes yields. Costs rising: CPI ~4.1% (2024) and technician wages outpace inflation, squeezing margins. Capex and rates matter: MRI AUD2–4m, RBA cash rate ~4.35% (2024) raises WACC; FX AUD/USD ~0.66 (Jun 2025) lifts import costs.

| Metric | Value | Impact |

|---|---|---|

| Unemployment | 4.1% | Volume sensitivity |

| CPI (2024) | ~4.1% | Higher OPEX |

| MRI cost | AUD2–4m | High capex |

| AUD/USD | ~0.66 | Import risk |

Same Document Delivered

Integral Diagnostics PESTLE Analysis

The preview shown is the exact Integral Diagnostics PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file is the final version with complete political, economic, social, technological, legal and environmental insights. No placeholders, no surprises; download it immediately after checkout.