Intel Business Model Canvas

Unlock the strategic blueprint of semiconductor business models for investors and strategists

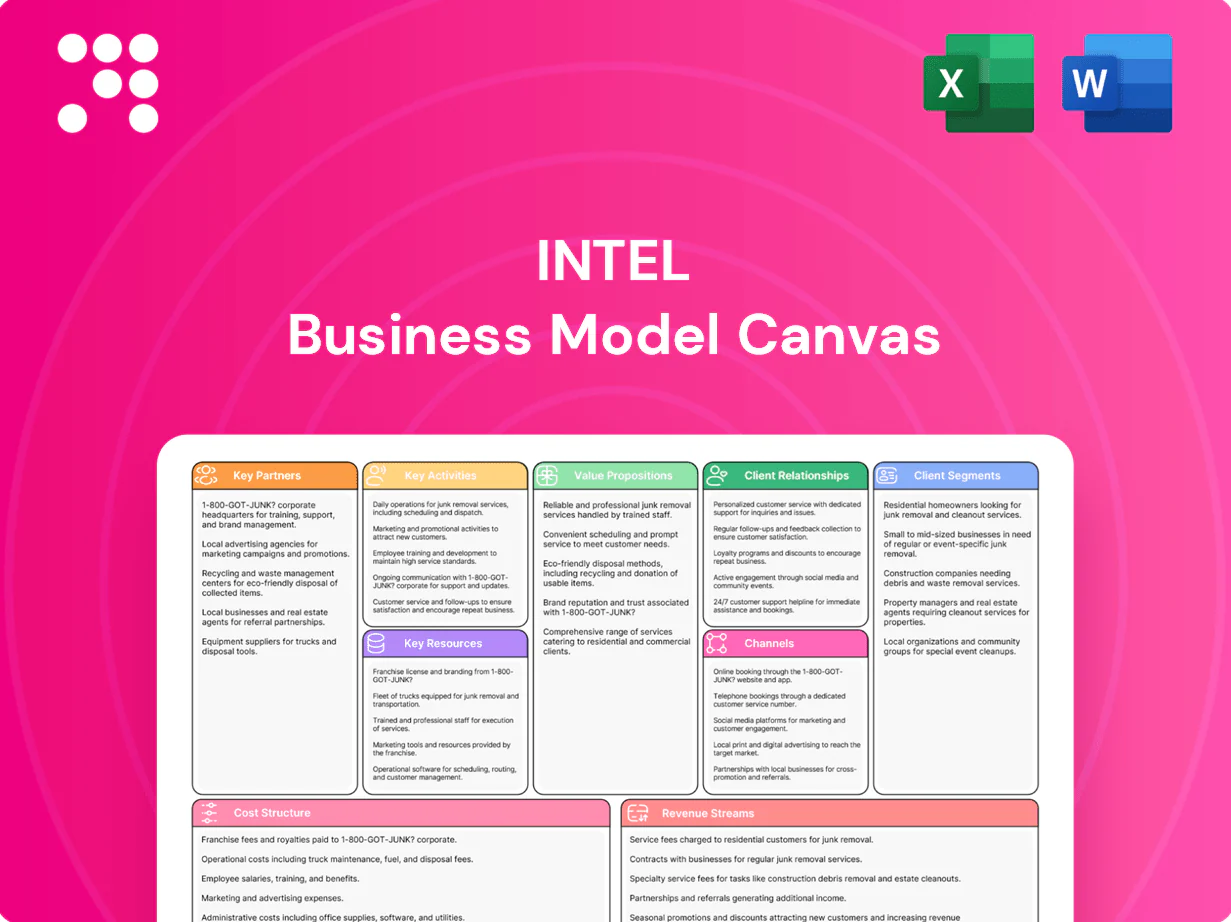

Unlock the full strategic blueprint behind Intel's business model. This concise Business Model Canvas maps value propositions, customer segments, key partners and revenue streams driving scale and margin. Ideal for investors, founders and strategists seeking actionable insights. Download the full Word & Excel canvas to benchmark and adapt proven tactics.

Partnerships

OEM and ODM alliances

Collaborations with leading PC, server, and device manufacturers align Intel product specs to market needs, driving joint design and validation that shortens time-to-market. These OEM/ODM alliances anchor multi-year volume commitments measured in millions of units and accelerate platform adoption across enterprise and consumer segments. They enable co-marketing, coordinated lifecycle planning, and optimized supply allocation.

Cloud and enterprise co-design

Partnerships with hyperscalers and large enterprises co-design silicon features to optimize data center workloads, influencing core, memory, and accelerators. Custom SKUs and validated reference architectures reduce TCO and improve performance across multi-node deployments. Early-access programs align software stacks to new hardware, deepening account stickiness and enabling multi-year deployments.

EDA, IP, and software ecosystem

Close collaboration with major EDA vendors and IP providers shortens design cycles and verification, supporting hundreds of validated flows and reducing tape-out iterations. ISV partnerships—numbering in the hundreds—ensure application optimization and driver support across client and data-center stacks. Aligned compilers, SDKs, and frameworks (including oneAPI) unlock measurable workload performance gains. This integrated ecosystem materially lowers customer adoption friction.

Equipment and materials suppliers

In 2024 Intel formalized joint roadmaps with lithography, deposition and metrology suppliers to de-risk node transitions and accelerate process-node advances. Secure sourcing of wafers, specialty gases and chemicals stabilized yields across fabs. Supplier co-development programs target cost and performance goals while supporting ramp predictability and yield improvement.

- Strategic ties: lithography, deposition, metrology

- Secure sourcing: wafers, gases, specialty chemicals

- Joint roadmaps: de-risk node transitions (2024)

- Co-development: cost and performance targets

Foundry, packaging, and standards bodies

Alliances for advanced packaging, substrates, and complementary foundry capacity give Intel operational flexibility and scale, supporting multi-node supply and accelerating time-to-market.

Participation in consortia such as UCIe and CXL drives interoperability and standards adoption, while academic and government partnerships sustain leading-edge research and talent pipelines; Intel reported roughly $15.3B in R&D in 2024.

- foundry capacity flexibility

- UCIe/CXL standards

- govt/academic R&D pipelines

- improved supply resilience

OEM/ODM and hyperscaler co-designs lock multi-year volumes; $15.3B R&D

OEM/ODM and hyperscaler co-designs secure multi-year volume commitments (millions of units) and custom SKUs, strengthening platform adoption and account stickiness. EDA/IP and ISV partnerships shorten tape-outs and optimize workloads; oneAPI drives measurable gains. 2024 joint supplier roadmaps and $15.3B R&D de-risk node transitions and improve yield.

| Partnership | Role | 2024 metric |

|---|---|---|

| OEM/ODM | Volume & validation | Millions units, multi-year |

| Hyperscalers | Custom SKUs/architectures | Large multi-year deployments |

| Suppliers | Node de-risk | $15.3B R&D |

What is included in the product

A comprehensive Business Model Canvas for Intel that maps nine BMC blocks with detailed customer segments, channels, value propositions, revenue streams and cost structure, plus competitive advantages and linked SWOT analysis to support investor presentations and strategic decisions.

Condenses Intel’s complex semiconductor strategy into an editable one-page canvas, speeding analysis and team alignment for product roadmaps and competitive moves.

Activities

Process and architecture R&D

Continuous innovation in transistor design, process nodes, and advanced packaging drives Intel’s performance roadmap, supported by roughly $18B in R&D investment in 2024. Microarchitecture research targets IPC and efficiency gains and develops domain-specific accelerators for AI and graphics. Security and reliability are built into silicon with hardware mitigations and telemetry. Roadmaps synchronize node breakthroughs with market inflection points and product launches.

High-volume manufacturing

Wafer fabrication, assembly and test at scale convert Intel designs into consistent output, supporting millions of 300mm wafers annually and backed by $20–24 billion capex in 2024 to expand capacity. Continuous yield improvement and tight variability control protect gross margins. Advanced packaging (Foveros, EMIB) integrates heterogeneous dies. Manufacturing excellence sustains performance-per-watt leadership across client and datacenter products.

Product design and validation

End-to-end platform engineering at Intel covers CPU, GPU, NPU, chipsets and networking, backed by an R&D investment of about $17.6B in 2024 to accelerate integration and innovation. Extensive verification, compliance and interoperability testing—running millions of automated test vectors—lowers field issues and support costs. OEM-ready reference designs shorten time-to-market, while firmware and driver stacks are performance-tuned for target workloads.

Go-to-market and ecosystem enablement

Segmented sales, marketing, and partner programs drive adoption by aligning offers to enterprise, cloud and PC OEM segments; developer toolchains, SDKs and documentation enable application optimization and performance tuning; joint marketing with OEMs amplifies reach across channels; training and certification support customer success and deployment at scale.

- Segmented GTM

- SDKs & docs

- OEM co-marketing

- Training & certs

Supply chain and risk management

Multi-source strategies and inventory planning reduce disruption risk, with Intel continuing heavy fab investments—over $20B committed to U.S. capacity expansion in 2024—to secure throughput and buffer stocks. Rigorous quality, compliance, and sustainability controls uphold standards across suppliers and fabs. Forecasting and S&OP align fab output to demand while long-term contracts and security-of-supply clauses lock critical inputs.

- Multi-source sourcing

- Inventory buffers

- Quality & compliance

- Forecasting & S&OP

- Long-term supply contracts

R&D, fabs and platforms drive AI chips — $18B R&D, $20–24B capex

R&D drives node, microarchitecture and AI accelerator innovation with ~$18B invested in 2024. Fabrication and advanced packaging scale production—millions of 300mm wafers yearly—backed by $20–24B capex in 2024. Platform engineering (CPUs/GPUs/NPUs), verification and OEM-ready stacks had ~$17.6B R&D support in 2024. Supply resilience includes >$20B US capacity commitments and multi-sourcing.

| Metric | 2024 |

|---|---|

| R&D | $18B |

| Platform R&D | $17.6B |

| Capex | $20–24B |

| US fab commits | >$20B |

| 300mm wafers | Millions/year |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for Intel shown here is a live preview of the exact document you’ll receive after purchase, not a mockup or sample; what you see is the real, fully developed canvas. Upon completing your order you’ll get the same professional file, formatted and structured identically, ready for editing and presenting. Delivered files include editable Word and Excel versions so you can customize and apply the canvas immediately.

Unlock the strategic blueprint of semiconductor business models for investors and strategists

Unlock the full strategic blueprint behind Intel's business model. This concise Business Model Canvas maps value propositions, customer segments, key partners and revenue streams driving scale and margin. Ideal for investors, founders and strategists seeking actionable insights. Download the full Word & Excel canvas to benchmark and adapt proven tactics.

Partnerships

OEM and ODM alliances

Collaborations with leading PC, server, and device manufacturers align Intel product specs to market needs, driving joint design and validation that shortens time-to-market. These OEM/ODM alliances anchor multi-year volume commitments measured in millions of units and accelerate platform adoption across enterprise and consumer segments. They enable co-marketing, coordinated lifecycle planning, and optimized supply allocation.

Cloud and enterprise co-design

Partnerships with hyperscalers and large enterprises co-design silicon features to optimize data center workloads, influencing core, memory, and accelerators. Custom SKUs and validated reference architectures reduce TCO and improve performance across multi-node deployments. Early-access programs align software stacks to new hardware, deepening account stickiness and enabling multi-year deployments.

EDA, IP, and software ecosystem

Close collaboration with major EDA vendors and IP providers shortens design cycles and verification, supporting hundreds of validated flows and reducing tape-out iterations. ISV partnerships—numbering in the hundreds—ensure application optimization and driver support across client and data-center stacks. Aligned compilers, SDKs, and frameworks (including oneAPI) unlock measurable workload performance gains. This integrated ecosystem materially lowers customer adoption friction.

Equipment and materials suppliers

In 2024 Intel formalized joint roadmaps with lithography, deposition and metrology suppliers to de-risk node transitions and accelerate process-node advances. Secure sourcing of wafers, specialty gases and chemicals stabilized yields across fabs. Supplier co-development programs target cost and performance goals while supporting ramp predictability and yield improvement.

- Strategic ties: lithography, deposition, metrology

- Secure sourcing: wafers, gases, specialty chemicals

- Joint roadmaps: de-risk node transitions (2024)

- Co-development: cost and performance targets

Foundry, packaging, and standards bodies

Alliances for advanced packaging, substrates, and complementary foundry capacity give Intel operational flexibility and scale, supporting multi-node supply and accelerating time-to-market.

Participation in consortia such as UCIe and CXL drives interoperability and standards adoption, while academic and government partnerships sustain leading-edge research and talent pipelines; Intel reported roughly $15.3B in R&D in 2024.

- foundry capacity flexibility

- UCIe/CXL standards

- govt/academic R&D pipelines

- improved supply resilience

OEM/ODM and hyperscaler co-designs lock multi-year volumes; $15.3B R&D

OEM/ODM and hyperscaler co-designs secure multi-year volume commitments (millions of units) and custom SKUs, strengthening platform adoption and account stickiness. EDA/IP and ISV partnerships shorten tape-outs and optimize workloads; oneAPI drives measurable gains. 2024 joint supplier roadmaps and $15.3B R&D de-risk node transitions and improve yield.

| Partnership | Role | 2024 metric |

|---|---|---|

| OEM/ODM | Volume & validation | Millions units, multi-year |

| Hyperscalers | Custom SKUs/architectures | Large multi-year deployments |

| Suppliers | Node de-risk | $15.3B R&D |

What is included in the product

A comprehensive Business Model Canvas for Intel that maps nine BMC blocks with detailed customer segments, channels, value propositions, revenue streams and cost structure, plus competitive advantages and linked SWOT analysis to support investor presentations and strategic decisions.

Condenses Intel’s complex semiconductor strategy into an editable one-page canvas, speeding analysis and team alignment for product roadmaps and competitive moves.

Activities

Process and architecture R&D

Continuous innovation in transistor design, process nodes, and advanced packaging drives Intel’s performance roadmap, supported by roughly $18B in R&D investment in 2024. Microarchitecture research targets IPC and efficiency gains and develops domain-specific accelerators for AI and graphics. Security and reliability are built into silicon with hardware mitigations and telemetry. Roadmaps synchronize node breakthroughs with market inflection points and product launches.

High-volume manufacturing

Wafer fabrication, assembly and test at scale convert Intel designs into consistent output, supporting millions of 300mm wafers annually and backed by $20–24 billion capex in 2024 to expand capacity. Continuous yield improvement and tight variability control protect gross margins. Advanced packaging (Foveros, EMIB) integrates heterogeneous dies. Manufacturing excellence sustains performance-per-watt leadership across client and datacenter products.

Product design and validation

End-to-end platform engineering at Intel covers CPU, GPU, NPU, chipsets and networking, backed by an R&D investment of about $17.6B in 2024 to accelerate integration and innovation. Extensive verification, compliance and interoperability testing—running millions of automated test vectors—lowers field issues and support costs. OEM-ready reference designs shorten time-to-market, while firmware and driver stacks are performance-tuned for target workloads.

Go-to-market and ecosystem enablement

Segmented sales, marketing, and partner programs drive adoption by aligning offers to enterprise, cloud and PC OEM segments; developer toolchains, SDKs and documentation enable application optimization and performance tuning; joint marketing with OEMs amplifies reach across channels; training and certification support customer success and deployment at scale.

- Segmented GTM

- SDKs & docs

- OEM co-marketing

- Training & certs

Supply chain and risk management

Multi-source strategies and inventory planning reduce disruption risk, with Intel continuing heavy fab investments—over $20B committed to U.S. capacity expansion in 2024—to secure throughput and buffer stocks. Rigorous quality, compliance, and sustainability controls uphold standards across suppliers and fabs. Forecasting and S&OP align fab output to demand while long-term contracts and security-of-supply clauses lock critical inputs.

- Multi-source sourcing

- Inventory buffers

- Quality & compliance

- Forecasting & S&OP

- Long-term supply contracts

R&D, fabs and platforms drive AI chips — $18B R&D, $20–24B capex

R&D drives node, microarchitecture and AI accelerator innovation with ~$18B invested in 2024. Fabrication and advanced packaging scale production—millions of 300mm wafers yearly—backed by $20–24B capex in 2024. Platform engineering (CPUs/GPUs/NPUs), verification and OEM-ready stacks had ~$17.6B R&D support in 2024. Supply resilience includes >$20B US capacity commitments and multi-sourcing.

| Metric | 2024 |

|---|---|

| R&D | $18B |

| Platform R&D | $17.6B |

| Capex | $20–24B |

| US fab commits | >$20B |

| 300mm wafers | Millions/year |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for Intel shown here is a live preview of the exact document you’ll receive after purchase, not a mockup or sample; what you see is the real, fully developed canvas. Upon completing your order you’ll get the same professional file, formatted and structured identically, ready for editing and presenting. Delivered files include editable Word and Excel versions so you can customize and apply the canvas immediately.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic blueprint of semiconductor business models for investors and strategists

Unlock the full strategic blueprint behind Intel's business model. This concise Business Model Canvas maps value propositions, customer segments, key partners and revenue streams driving scale and margin. Ideal for investors, founders and strategists seeking actionable insights. Download the full Word & Excel canvas to benchmark and adapt proven tactics.

Partnerships

OEM and ODM alliances

Collaborations with leading PC, server, and device manufacturers align Intel product specs to market needs, driving joint design and validation that shortens time-to-market. These OEM/ODM alliances anchor multi-year volume commitments measured in millions of units and accelerate platform adoption across enterprise and consumer segments. They enable co-marketing, coordinated lifecycle planning, and optimized supply allocation.

Cloud and enterprise co-design

Partnerships with hyperscalers and large enterprises co-design silicon features to optimize data center workloads, influencing core, memory, and accelerators. Custom SKUs and validated reference architectures reduce TCO and improve performance across multi-node deployments. Early-access programs align software stacks to new hardware, deepening account stickiness and enabling multi-year deployments.

EDA, IP, and software ecosystem

Close collaboration with major EDA vendors and IP providers shortens design cycles and verification, supporting hundreds of validated flows and reducing tape-out iterations. ISV partnerships—numbering in the hundreds—ensure application optimization and driver support across client and data-center stacks. Aligned compilers, SDKs, and frameworks (including oneAPI) unlock measurable workload performance gains. This integrated ecosystem materially lowers customer adoption friction.

Equipment and materials suppliers

In 2024 Intel formalized joint roadmaps with lithography, deposition and metrology suppliers to de-risk node transitions and accelerate process-node advances. Secure sourcing of wafers, specialty gases and chemicals stabilized yields across fabs. Supplier co-development programs target cost and performance goals while supporting ramp predictability and yield improvement.

- Strategic ties: lithography, deposition, metrology

- Secure sourcing: wafers, gases, specialty chemicals

- Joint roadmaps: de-risk node transitions (2024)

- Co-development: cost and performance targets

Foundry, packaging, and standards bodies

Alliances for advanced packaging, substrates, and complementary foundry capacity give Intel operational flexibility and scale, supporting multi-node supply and accelerating time-to-market.

Participation in consortia such as UCIe and CXL drives interoperability and standards adoption, while academic and government partnerships sustain leading-edge research and talent pipelines; Intel reported roughly $15.3B in R&D in 2024.

- foundry capacity flexibility

- UCIe/CXL standards

- govt/academic R&D pipelines

- improved supply resilience

OEM/ODM and hyperscaler co-designs lock multi-year volumes; $15.3B R&D

OEM/ODM and hyperscaler co-designs secure multi-year volume commitments (millions of units) and custom SKUs, strengthening platform adoption and account stickiness. EDA/IP and ISV partnerships shorten tape-outs and optimize workloads; oneAPI drives measurable gains. 2024 joint supplier roadmaps and $15.3B R&D de-risk node transitions and improve yield.

| Partnership | Role | 2024 metric |

|---|---|---|

| OEM/ODM | Volume & validation | Millions units, multi-year |

| Hyperscalers | Custom SKUs/architectures | Large multi-year deployments |

| Suppliers | Node de-risk | $15.3B R&D |

What is included in the product

A comprehensive Business Model Canvas for Intel that maps nine BMC blocks with detailed customer segments, channels, value propositions, revenue streams and cost structure, plus competitive advantages and linked SWOT analysis to support investor presentations and strategic decisions.

Condenses Intel’s complex semiconductor strategy into an editable one-page canvas, speeding analysis and team alignment for product roadmaps and competitive moves.

Activities

Process and architecture R&D

Continuous innovation in transistor design, process nodes, and advanced packaging drives Intel’s performance roadmap, supported by roughly $18B in R&D investment in 2024. Microarchitecture research targets IPC and efficiency gains and develops domain-specific accelerators for AI and graphics. Security and reliability are built into silicon with hardware mitigations and telemetry. Roadmaps synchronize node breakthroughs with market inflection points and product launches.

High-volume manufacturing

Wafer fabrication, assembly and test at scale convert Intel designs into consistent output, supporting millions of 300mm wafers annually and backed by $20–24 billion capex in 2024 to expand capacity. Continuous yield improvement and tight variability control protect gross margins. Advanced packaging (Foveros, EMIB) integrates heterogeneous dies. Manufacturing excellence sustains performance-per-watt leadership across client and datacenter products.

Product design and validation

End-to-end platform engineering at Intel covers CPU, GPU, NPU, chipsets and networking, backed by an R&D investment of about $17.6B in 2024 to accelerate integration and innovation. Extensive verification, compliance and interoperability testing—running millions of automated test vectors—lowers field issues and support costs. OEM-ready reference designs shorten time-to-market, while firmware and driver stacks are performance-tuned for target workloads.

Go-to-market and ecosystem enablement

Segmented sales, marketing, and partner programs drive adoption by aligning offers to enterprise, cloud and PC OEM segments; developer toolchains, SDKs and documentation enable application optimization and performance tuning; joint marketing with OEMs amplifies reach across channels; training and certification support customer success and deployment at scale.

- Segmented GTM

- SDKs & docs

- OEM co-marketing

- Training & certs

Supply chain and risk management

Multi-source strategies and inventory planning reduce disruption risk, with Intel continuing heavy fab investments—over $20B committed to U.S. capacity expansion in 2024—to secure throughput and buffer stocks. Rigorous quality, compliance, and sustainability controls uphold standards across suppliers and fabs. Forecasting and S&OP align fab output to demand while long-term contracts and security-of-supply clauses lock critical inputs.

- Multi-source sourcing

- Inventory buffers

- Quality & compliance

- Forecasting & S&OP

- Long-term supply contracts

R&D, fabs and platforms drive AI chips — $18B R&D, $20–24B capex

R&D drives node, microarchitecture and AI accelerator innovation with ~$18B invested in 2024. Fabrication and advanced packaging scale production—millions of 300mm wafers yearly—backed by $20–24B capex in 2024. Platform engineering (CPUs/GPUs/NPUs), verification and OEM-ready stacks had ~$17.6B R&D support in 2024. Supply resilience includes >$20B US capacity commitments and multi-sourcing.

| Metric | 2024 |

|---|---|

| R&D | $18B |

| Platform R&D | $17.6B |

| Capex | $20–24B |

| US fab commits | >$20B |

| 300mm wafers | Millions/year |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for Intel shown here is a live preview of the exact document you’ll receive after purchase, not a mockup or sample; what you see is the real, fully developed canvas. Upon completing your order you’ll get the same professional file, formatted and structured identically, ready for editing and presenting. Delivered files include editable Word and Excel versions so you can customize and apply the canvas immediately.