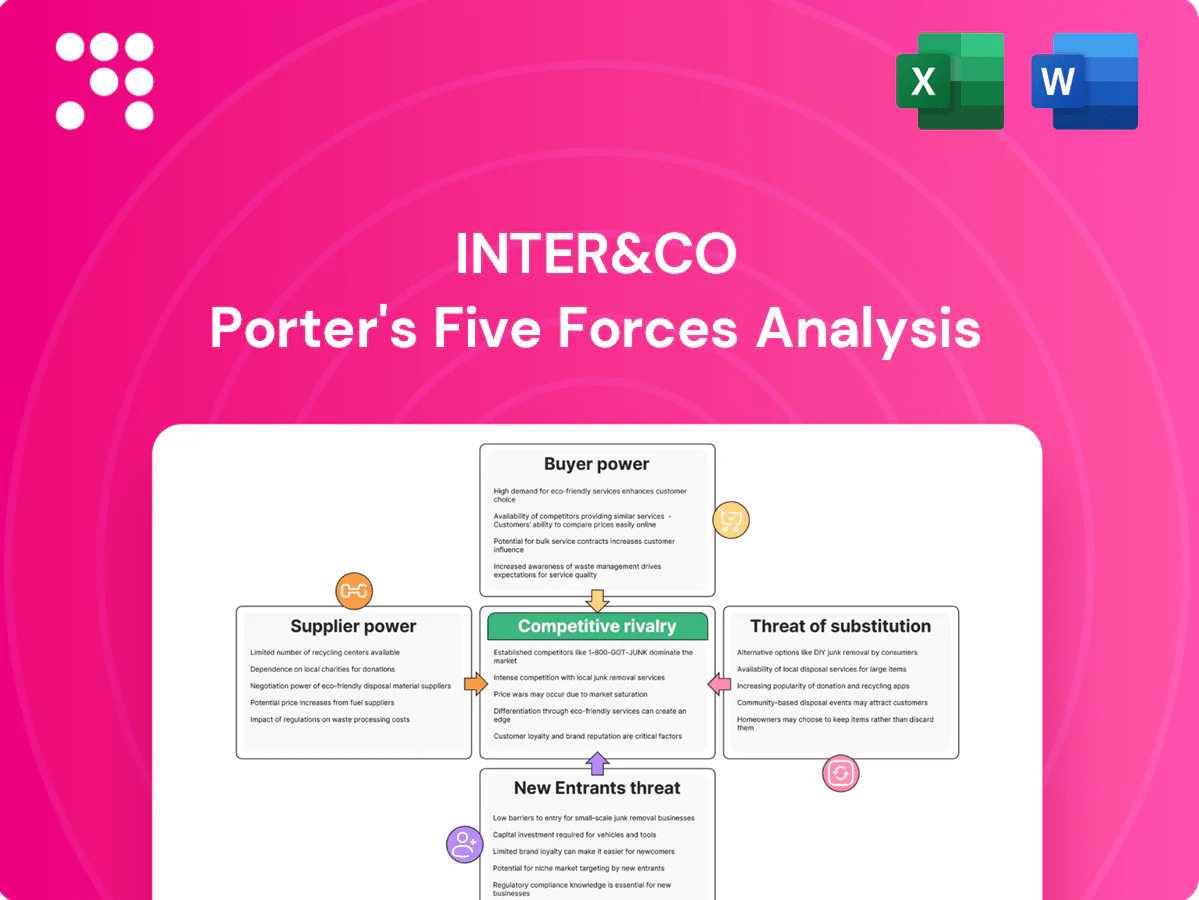

Inter&Co Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Inter&Co faces moderate buyer power, concentrated suppliers in key inputs, and rising substitute risks that compress margins; barriers to entry remain mixed while rivalry intensifies in core segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Inter&Co’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud and infrastructure dependence

Inter&Co relies on hyperscale cloud providers and CDNs to deliver app performance and security; AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 11% of the global cloud market in 2024, while CDNs like Cloudflare reported $1.67B revenue in 2024, underscoring vendor concentration and leverage on pricing and SLAs. High migration costs and compliance complexity raise switching friction and operational risk. Building multi-cloud and selective in-house infrastructure can materially moderate supplier power.

Payment networks and rails

Visa and Mastercard dominate card rails with roughly 70–80% market share globally, while acquiring banks and partners capture 1–3% of transaction value in fees, shaping Inter&Co’s margins; certification and partner onboarding often take 3–6 months. Brazil’s Pix has cut merchant costs substantially and handled billions of instant payments by 2024, but still requires compliance and ops readiness. Diversifying rails and shifting volume reduces dependence on any single network.

Core banking and data providers

Core systems, KYC/AML vendors, bureaus and analytics partners are critical for risk/compliance, especially after Brazil's open banking rollout in 2021–2022; many banks rely on a small set of specialist vendors, raising switching costs. Multi-year contracts (commonly 3–7 years) and deep integrations amplify supplier leverage. Limited interchangeable vendors in Brazil elevate vendor power. Building proprietary modules and APIs reduces exposure.

App stores and device ecosystems

Apple and Google control app distribution, policies, and fees—standard cuts are up to 30% with 15% tiers for developers earning under $1M (Small Business Program, 2024). Policy shifts can rapidly change acquisition costs and engagement mechanics; store visibility acts as a quasi-gatekeeper given Android ~70% and iOS ~30% global share (2024).

- Platform fees: up to 30%, 15% for <1M revenue (2024)

- OS share: Android ~70%, iOS ~30% (2024)

- Store visibility = gatekeeper for discovery

- Web/direct channels lower dependence

Capital and liquidity sources

Wholesale funding, securitization partners and investors determine Inter&Co’s growth capacity and cost of capital; with the US federal funds rate near 5.25% in 2024, market funding costs remain elevated and spreads widened after 2023 stress episodes, strengthening supplier leverage. Deposit growth eases but does not remove wholesale reliance; diversified funding and strong credit metrics improve bargaining power.

- Wholesale funding material to liquidity

- Higher spreads/covenants in tight cycles

- Deposits mitigate, not eliminate risk

- Diversification + credit quality = better terms

Concentrated supplier power: hyperscalers, CDNs, card rails and app-store fees squeeze margins

Inter&Co faces concentrated supplier power: hyperscale cloud (AWS 32%, Azure 23%, GCP 11% in 2024) and CDNs (Cloudflare $1.67B revenue 2024) drive pricing and SLAs, while Visa/Mastercard control ~70–80% of card rails. App stores levy up to 30% (15% tier for <1M revenue, 2024). Diversification, multi-cloud and proprietary stacks reduce leverage.

| Supplier | Metric (2024) | Impact |

|---|---|---|

| Hyperscale cloud | AWS 32%/Azure 23%/GCP 11% | High pricing/SLA power |

| CDN | Cloudflare $1.67B | Performance dependency |

| Card rails | Visa/Mastercard 70–80% | Fee pressure |

| App stores | Fees up to 30% (15% <1M) | Acquisition/monetization risk |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, substitutes, new entrants, and rivalry—specific to Inter&Co, highlighting disruptive threats, pricing pressures, and strategic implications with editable output for reports and presentations.

Inter&Co Porter's Five Forces condenses complex competitive dynamics into a single, customizable one-sheet with spider charts, duplicate scenario tabs, no macros, and deck-ready layout—relieving strategic analysis pain by making pressure levels instantly actionable and easy to share.

Customers Bargaining Power

Low switching costs in digital banking

Low switching costs let consumers open accounts and move balances within hours, and in 2024 roughly 60% of retail customers said they would switch providers for better rates or experience. Feature parity across fintechs amplifies price and UX sensitivity, increasing churn when incentives or yields shift. Deep loyalty programs and multi-product ecosystems (wallets, payments, lending) can still raise switching frictions and retain high-value segments.

Open Finance and data portability

Brazil’s Open Finance lets users port data and initiate payments across providers, and by 2024 over 100 institutions were connected to the ecosystem per Banco Central. This transparency increases comparison shopping and strengthens rate negotiation as aggregators serving millions press fees and benefits. Inter&Co must compete on tangible value, superior UX, and deep personalization to retain customers.

SME bargaining on payments and credit

SMEs intensely negotiate acquiring fees, settlement times and working-capital rates, with a 2024 industry survey showing 68% multi-homing across PSPs and banks, which strengthens their leverage. Bundled banking, e-commerce and credit offers can win share but prompt rapid price-matching; service reliability and API integration remain decisive tie-breakers for switching decisions.

Price sensitivity to yields and fees

Retail customers in Brazil chase higher CDI and lower fees, favoring funds with low expense ratios and cashback; digital-bank users exceeded 100 million in 2024, amplifying rapid repricing that spreads instantly via social and fintech channels. Fee-free expectations remain entrenched in the digital segment, forcing any monetization to be justified by clear value-added services.

- High price sensitivity

- Instant repricing via fintech/social

- 100M+ digital users (2024)

- Monetization must add measurable value

Platform expectations and service quality

Users demand super-app convenience — payments, shopping, investing and insurance in one flow — and 2024 data shows platforms with integrated stacks report up to 30% higher engagement; outages or slow support trigger immediate backlash and migration, with app-rating drops raising CAC materially.

- NPS shifts can change CAC by ~15–25% (2024 industry trend); transparent policies and proactive support cut churn and blunt buyer power.

Low switching: 60% would switch; 100M+ users speed repricing

Low switching costs and feature parity keep customer power high: 60% of retail users would switch for better rates or UX in 2024, and 100M+ digital users amplify rapid repricing. SMEs multi-home (68% in 2024) and fiercely negotiate fees and settlement terms. Integrated stacks raise engagement ~30%, but NPS shifts can change CAC by ~15–25%.

| Metric | 2024 | Impact |

|---|---|---|

| Retail switch intent | 60% | Higher churn |

| Digital users | 100M+ | Fast repricing |

| SME multi-homing | 68% | Stronger negotiation |

| Integrated engagement | +30% | Better retention |

Same Document Delivered

Inter&Co Porter's Five Forces Analysis

This preview shows the exact Inter&Co Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download the moment you buy. You're getting the same complete, ready-to-use file shown here.

Don't Miss the Bigger Picture

Inter&Co faces moderate buyer power, concentrated suppliers in key inputs, and rising substitute risks that compress margins; barriers to entry remain mixed while rivalry intensifies in core segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Inter&Co’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud and infrastructure dependence

Inter&Co relies on hyperscale cloud providers and CDNs to deliver app performance and security; AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 11% of the global cloud market in 2024, while CDNs like Cloudflare reported $1.67B revenue in 2024, underscoring vendor concentration and leverage on pricing and SLAs. High migration costs and compliance complexity raise switching friction and operational risk. Building multi-cloud and selective in-house infrastructure can materially moderate supplier power.

Payment networks and rails

Visa and Mastercard dominate card rails with roughly 70–80% market share globally, while acquiring banks and partners capture 1–3% of transaction value in fees, shaping Inter&Co’s margins; certification and partner onboarding often take 3–6 months. Brazil’s Pix has cut merchant costs substantially and handled billions of instant payments by 2024, but still requires compliance and ops readiness. Diversifying rails and shifting volume reduces dependence on any single network.

Core banking and data providers

Core systems, KYC/AML vendors, bureaus and analytics partners are critical for risk/compliance, especially after Brazil's open banking rollout in 2021–2022; many banks rely on a small set of specialist vendors, raising switching costs. Multi-year contracts (commonly 3–7 years) and deep integrations amplify supplier leverage. Limited interchangeable vendors in Brazil elevate vendor power. Building proprietary modules and APIs reduces exposure.

App stores and device ecosystems

Apple and Google control app distribution, policies, and fees—standard cuts are up to 30% with 15% tiers for developers earning under $1M (Small Business Program, 2024). Policy shifts can rapidly change acquisition costs and engagement mechanics; store visibility acts as a quasi-gatekeeper given Android ~70% and iOS ~30% global share (2024).

- Platform fees: up to 30%, 15% for <1M revenue (2024)

- OS share: Android ~70%, iOS ~30% (2024)

- Store visibility = gatekeeper for discovery

- Web/direct channels lower dependence

Capital and liquidity sources

Wholesale funding, securitization partners and investors determine Inter&Co’s growth capacity and cost of capital; with the US federal funds rate near 5.25% in 2024, market funding costs remain elevated and spreads widened after 2023 stress episodes, strengthening supplier leverage. Deposit growth eases but does not remove wholesale reliance; diversified funding and strong credit metrics improve bargaining power.

- Wholesale funding material to liquidity

- Higher spreads/covenants in tight cycles

- Deposits mitigate, not eliminate risk

- Diversification + credit quality = better terms

Concentrated supplier power: hyperscalers, CDNs, card rails and app-store fees squeeze margins

Inter&Co faces concentrated supplier power: hyperscale cloud (AWS 32%, Azure 23%, GCP 11% in 2024) and CDNs (Cloudflare $1.67B revenue 2024) drive pricing and SLAs, while Visa/Mastercard control ~70–80% of card rails. App stores levy up to 30% (15% tier for <1M revenue, 2024). Diversification, multi-cloud and proprietary stacks reduce leverage.

| Supplier | Metric (2024) | Impact |

|---|---|---|

| Hyperscale cloud | AWS 32%/Azure 23%/GCP 11% | High pricing/SLA power |

| CDN | Cloudflare $1.67B | Performance dependency |

| Card rails | Visa/Mastercard 70–80% | Fee pressure |

| App stores | Fees up to 30% (15% <1M) | Acquisition/monetization risk |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, substitutes, new entrants, and rivalry—specific to Inter&Co, highlighting disruptive threats, pricing pressures, and strategic implications with editable output for reports and presentations.

Inter&Co Porter's Five Forces condenses complex competitive dynamics into a single, customizable one-sheet with spider charts, duplicate scenario tabs, no macros, and deck-ready layout—relieving strategic analysis pain by making pressure levels instantly actionable and easy to share.

Customers Bargaining Power

Low switching costs in digital banking

Low switching costs let consumers open accounts and move balances within hours, and in 2024 roughly 60% of retail customers said they would switch providers for better rates or experience. Feature parity across fintechs amplifies price and UX sensitivity, increasing churn when incentives or yields shift. Deep loyalty programs and multi-product ecosystems (wallets, payments, lending) can still raise switching frictions and retain high-value segments.

Open Finance and data portability

Brazil’s Open Finance lets users port data and initiate payments across providers, and by 2024 over 100 institutions were connected to the ecosystem per Banco Central. This transparency increases comparison shopping and strengthens rate negotiation as aggregators serving millions press fees and benefits. Inter&Co must compete on tangible value, superior UX, and deep personalization to retain customers.

SME bargaining on payments and credit

SMEs intensely negotiate acquiring fees, settlement times and working-capital rates, with a 2024 industry survey showing 68% multi-homing across PSPs and banks, which strengthens their leverage. Bundled banking, e-commerce and credit offers can win share but prompt rapid price-matching; service reliability and API integration remain decisive tie-breakers for switching decisions.

Price sensitivity to yields and fees

Retail customers in Brazil chase higher CDI and lower fees, favoring funds with low expense ratios and cashback; digital-bank users exceeded 100 million in 2024, amplifying rapid repricing that spreads instantly via social and fintech channels. Fee-free expectations remain entrenched in the digital segment, forcing any monetization to be justified by clear value-added services.

- High price sensitivity

- Instant repricing via fintech/social

- 100M+ digital users (2024)

- Monetization must add measurable value

Platform expectations and service quality

Users demand super-app convenience — payments, shopping, investing and insurance in one flow — and 2024 data shows platforms with integrated stacks report up to 30% higher engagement; outages or slow support trigger immediate backlash and migration, with app-rating drops raising CAC materially.

- NPS shifts can change CAC by ~15–25% (2024 industry trend); transparent policies and proactive support cut churn and blunt buyer power.

Low switching: 60% would switch; 100M+ users speed repricing

Low switching costs and feature parity keep customer power high: 60% of retail users would switch for better rates or UX in 2024, and 100M+ digital users amplify rapid repricing. SMEs multi-home (68% in 2024) and fiercely negotiate fees and settlement terms. Integrated stacks raise engagement ~30%, but NPS shifts can change CAC by ~15–25%.

| Metric | 2024 | Impact |

|---|---|---|

| Retail switch intent | 60% | Higher churn |

| Digital users | 100M+ | Fast repricing |

| SME multi-homing | 68% | Stronger negotiation |

| Integrated engagement | +30% | Better retention |

Same Document Delivered

Inter&Co Porter's Five Forces Analysis

This preview shows the exact Inter&Co Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download the moment you buy. You're getting the same complete, ready-to-use file shown here.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Inter&Co faces moderate buyer power, concentrated suppliers in key inputs, and rising substitute risks that compress margins; barriers to entry remain mixed while rivalry intensifies in core segments. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Inter&Co’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud and infrastructure dependence

Inter&Co relies on hyperscale cloud providers and CDNs to deliver app performance and security; AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 11% of the global cloud market in 2024, while CDNs like Cloudflare reported $1.67B revenue in 2024, underscoring vendor concentration and leverage on pricing and SLAs. High migration costs and compliance complexity raise switching friction and operational risk. Building multi-cloud and selective in-house infrastructure can materially moderate supplier power.

Payment networks and rails

Visa and Mastercard dominate card rails with roughly 70–80% market share globally, while acquiring banks and partners capture 1–3% of transaction value in fees, shaping Inter&Co’s margins; certification and partner onboarding often take 3–6 months. Brazil’s Pix has cut merchant costs substantially and handled billions of instant payments by 2024, but still requires compliance and ops readiness. Diversifying rails and shifting volume reduces dependence on any single network.

Core banking and data providers

Core systems, KYC/AML vendors, bureaus and analytics partners are critical for risk/compliance, especially after Brazil's open banking rollout in 2021–2022; many banks rely on a small set of specialist vendors, raising switching costs. Multi-year contracts (commonly 3–7 years) and deep integrations amplify supplier leverage. Limited interchangeable vendors in Brazil elevate vendor power. Building proprietary modules and APIs reduces exposure.

App stores and device ecosystems

Apple and Google control app distribution, policies, and fees—standard cuts are up to 30% with 15% tiers for developers earning under $1M (Small Business Program, 2024). Policy shifts can rapidly change acquisition costs and engagement mechanics; store visibility acts as a quasi-gatekeeper given Android ~70% and iOS ~30% global share (2024).

- Platform fees: up to 30%, 15% for <1M revenue (2024)

- OS share: Android ~70%, iOS ~30% (2024)

- Store visibility = gatekeeper for discovery

- Web/direct channels lower dependence

Capital and liquidity sources

Wholesale funding, securitization partners and investors determine Inter&Co’s growth capacity and cost of capital; with the US federal funds rate near 5.25% in 2024, market funding costs remain elevated and spreads widened after 2023 stress episodes, strengthening supplier leverage. Deposit growth eases but does not remove wholesale reliance; diversified funding and strong credit metrics improve bargaining power.

- Wholesale funding material to liquidity

- Higher spreads/covenants in tight cycles

- Deposits mitigate, not eliminate risk

- Diversification + credit quality = better terms

Concentrated supplier power: hyperscalers, CDNs, card rails and app-store fees squeeze margins

Inter&Co faces concentrated supplier power: hyperscale cloud (AWS 32%, Azure 23%, GCP 11% in 2024) and CDNs (Cloudflare $1.67B revenue 2024) drive pricing and SLAs, while Visa/Mastercard control ~70–80% of card rails. App stores levy up to 30% (15% tier for <1M revenue, 2024). Diversification, multi-cloud and proprietary stacks reduce leverage.

| Supplier | Metric (2024) | Impact |

|---|---|---|

| Hyperscale cloud | AWS 32%/Azure 23%/GCP 11% | High pricing/SLA power |

| CDN | Cloudflare $1.67B | Performance dependency |

| Card rails | Visa/Mastercard 70–80% | Fee pressure |

| App stores | Fees up to 30% (15% <1M) | Acquisition/monetization risk |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, substitutes, new entrants, and rivalry—specific to Inter&Co, highlighting disruptive threats, pricing pressures, and strategic implications with editable output for reports and presentations.

Inter&Co Porter's Five Forces condenses complex competitive dynamics into a single, customizable one-sheet with spider charts, duplicate scenario tabs, no macros, and deck-ready layout—relieving strategic analysis pain by making pressure levels instantly actionable and easy to share.

Customers Bargaining Power

Low switching costs in digital banking

Low switching costs let consumers open accounts and move balances within hours, and in 2024 roughly 60% of retail customers said they would switch providers for better rates or experience. Feature parity across fintechs amplifies price and UX sensitivity, increasing churn when incentives or yields shift. Deep loyalty programs and multi-product ecosystems (wallets, payments, lending) can still raise switching frictions and retain high-value segments.

Open Finance and data portability

Brazil’s Open Finance lets users port data and initiate payments across providers, and by 2024 over 100 institutions were connected to the ecosystem per Banco Central. This transparency increases comparison shopping and strengthens rate negotiation as aggregators serving millions press fees and benefits. Inter&Co must compete on tangible value, superior UX, and deep personalization to retain customers.

SME bargaining on payments and credit

SMEs intensely negotiate acquiring fees, settlement times and working-capital rates, with a 2024 industry survey showing 68% multi-homing across PSPs and banks, which strengthens their leverage. Bundled banking, e-commerce and credit offers can win share but prompt rapid price-matching; service reliability and API integration remain decisive tie-breakers for switching decisions.

Price sensitivity to yields and fees

Retail customers in Brazil chase higher CDI and lower fees, favoring funds with low expense ratios and cashback; digital-bank users exceeded 100 million in 2024, amplifying rapid repricing that spreads instantly via social and fintech channels. Fee-free expectations remain entrenched in the digital segment, forcing any monetization to be justified by clear value-added services.

- High price sensitivity

- Instant repricing via fintech/social

- 100M+ digital users (2024)

- Monetization must add measurable value

Platform expectations and service quality

Users demand super-app convenience — payments, shopping, investing and insurance in one flow — and 2024 data shows platforms with integrated stacks report up to 30% higher engagement; outages or slow support trigger immediate backlash and migration, with app-rating drops raising CAC materially.

- NPS shifts can change CAC by ~15–25% (2024 industry trend); transparent policies and proactive support cut churn and blunt buyer power.

Low switching: 60% would switch; 100M+ users speed repricing

Low switching costs and feature parity keep customer power high: 60% of retail users would switch for better rates or UX in 2024, and 100M+ digital users amplify rapid repricing. SMEs multi-home (68% in 2024) and fiercely negotiate fees and settlement terms. Integrated stacks raise engagement ~30%, but NPS shifts can change CAC by ~15–25%.

| Metric | 2024 | Impact |

|---|---|---|

| Retail switch intent | 60% | Higher churn |

| Digital users | 100M+ | Fast repricing |

| SME multi-homing | 68% | Stronger negotiation |

| Integrated engagement | +30% | Better retention |

Same Document Delivered

Inter&Co Porter's Five Forces Analysis

This preview shows the exact Inter&Co Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download the moment you buy. You're getting the same complete, ready-to-use file shown here.