Inter&Co PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of Inter&Co—concise, data-driven insights into political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it's ready to use and editable. Buy the full report to get the complete deep-dive instantly.

Political factors

Regulatory stance of Brazil’s Central Bank

Brazil’s Central Bank is proactive on innovation, having launched PIX in 2020 and rolled out Open Finance from 2021. Supportive BCB policy through 2024 has enabled rapid fintech growth, aiding Inter&Co’s user and product expansion. Tighter supervisory cycles increase compliance costs and capital buffers. Continuous engagement with the BCB is essential to anticipate rule changes.

Government priorities on financial inclusion

Brazilian administrations emphasize inclusion and competition, favoring digital-first banks as population (~214 million in 2023) shifts to digital rails; Nubank reached about 80 million customers by 2024, illustrating scale. Public programs and Pix-led payment rails channel more users into the formal system, boosting onboarding. Post-election policy shifts can reallocate subsidies or regulatory support. Inter&Co must align its super app narrative with inclusion goals to retain goodwill.

Fiscal stability and sovereign risk

Brazil’s fiscal path—with gross public debt near 75% of GDP and an EMBI sovereign spread around 300 bps in 2024—directly shapes macro stability, policy rates and investor sentiment. Rising sovereign risk premia can widen funding costs and tighten credit for banks and nonbank lenders. Fiscal stability supports credit growth and higher fintech equity multiples. Inter&Co should recalibrate risk appetite and provisioning in line with fiscal newsflow.

Trade and geopolitical dynamics

Global tensions in 2024–25 have intermittently tightened capital flows to emerging markets such as Brazil, triggering risk-off episodes that can weaken the real and raise corporate funding costs.

Nearshoring and revived cross-border commerce present revenue and user-growth opportunities a super app can capture by facilitating payments, logistics and B2B services across the region.

Inter&Co should build optionality for regional expansion—cash buffers, modular product stacks and contingent funding lines—to scale quickly when conditions improve.

- Tag: risk-off — episodic FX pressure on BRL

- Tag: funding — higher short-term borrowing costs in stress

- Tag: opportunity — nearshoring-driven trade growth 2024–25

- Tag: strategy — preserve optionality for regional rollouts

Public digital infrastructure and state-owned competitors

PIX and other government-led instant-payment platforms set baseline expectations for near-instant settlement and near-zero fees, pushing private players to match speed and cost while PIX adoption scaled rapidly across Brazil.

State-owned banks such as Caixa and Banco do Brasil—which together control roughly 40% of retail deposits—can shape pricing and credit availability, affecting market dynamics for Inter&Co.

Inter&Co can differentiate through superior UX and bundled ecosystem services, but must stay ready to pivot quickly when policy changes to public platforms alter fee structures or technical requirements.

- PIX-like platforms: baseline expectations on speed/cost

- State banks: ~40% retail deposit influence

- Inter&Co edge: UX + ecosystem services

- Risk: rapid product changes after policy shifts

PIX/Open Finance scaled fintech; fiscal strain (debt ~75% GDP) raises funding risk

BCB-led innovation (PIX 2020; Open Finance 2021) and supportive policy through 2024 fueled fintech scale (Brazil pop ~214m; Nubank ~80m customers in 2024), but tighter supervision raises compliance costs. Fiscal stress (gross public debt ~75% of GDP; EMBI ~300bps in 2024) elevates funding risk; state banks hold ~40% retail deposits. Inter&Co must preserve optionality for regional expansion and adjust provisioning to fiscal/newsflow.

| Tag | Metric | 2024/25 |

|---|---|---|

| innovation | PIX launch / Open Finance | 2020 / 2021 |

| scale | Population / Nubank users | 214M / ~80M (2024) |

| fiscal | Debt / EMBI | ~75% GDP / ~300bps (2024) |

| competition | State bank deposit share | ~40% |

What is included in the product

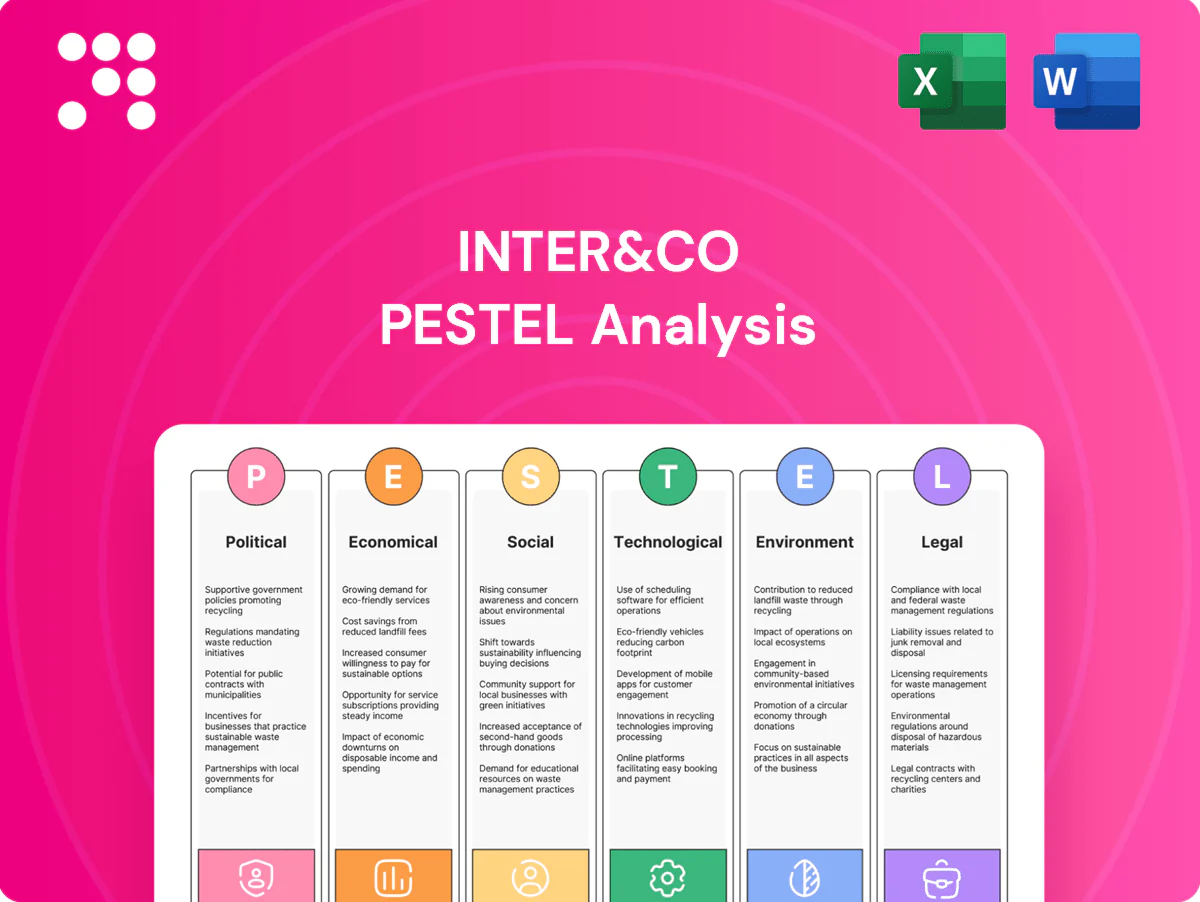

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Inter&Co, with data-driven, region- and industry-specific insights and forward-looking scenarios to identify risks and opportunities for executives, investors and strategists.

Inter&Co's PESTLE delivers a visually segmented, concise summary of external risks and opportunities that’s easily dropped into presentations or shared across teams, with editable notes for region- or business-specific context to speed decision-making.

Economic factors

Interest rate cycle and credit demand

Selic at 13.75% (Dec 2023) directly boosts net interest margins but can restrain loan growth when tightened; easing phases historically support origination and improve asset quality. Tightening increases borrower stress and NPL risk, requiring active pricing and duration management. Inter&Co should align product mix to rate trajectories, favoring floating-rate and shorter-duration assets during hikes and origination-heavy strategies when cuts resume.

Inflation and consumer spending

Inflation erodes real incomes and drove higher consumer loan delinquencies as credit-card 90+ day delinquencies rose toward 3.2% in 2024, pressuring Inter&Co’s receivables. Elevated prices compressed discretionary spend across super app verticals, with US PCE spending growth slowing to about 2.6% in 2024. Disinflation into 2025 (CPI ~3.4% in 2024) supports fee income and cross-selling, while dynamic risk-based pricing protects margins.

Exchange rate volatility

BRL swings (~15% vs USD in 2023–24) pressure Inter&Co funding costs, lift imported tech prices and dampen investor appetite after sharper volatility episodes. If Inter&Co carries USD-linked capex or partner payouts, hedging (forwards/options) is critical to cap FX-driven margin erosion. Currency moves also reshaped cross-border e-commerce flows—Brazilian cross-border sales grew ~16% in 2024—so transparent FX pass-through helps stabilize unit economics.

Labor market and income formalization

Gig and informal work account for roughly 40% of Brazil's workforce (IBGE, 2024), concentrating credit risk in variable-income segments; improving formalization raises KYC data quality and measurable repayment capacity. Inter&Co can underwrite variable incomes using granular cash-flow signals from bank and app data, while employment cycles and an unemployment rate near 8–9% (IBGE, 2024) will drive portfolio performance.

- Informal share ~40% (IBGE 2024)

- Unemployment ~8–9% (IBGE 2024)

- Formalization → better KYC, higher repayment predictability

- Underwrite via granular cash-flow, adapt to employment cycles

Capital markets access and cost of capital

Equity and debt market windows determine Inter&Co growth funding; with benchmark policy rates around 5.25-5.50% (US mid-2024) access shifts timing and pricing of raises. Risk sentiment to fintech drives valuation multiples and IPO activity, affecting cost of equity. Lower capital costs expand spend on customer acquisition and R&D; Inter&Co should keep diversified funding and 6–12 months cash buffers.

- Market rate: 5.25–5.50%

- Liquidity buffer: 6–12 months

- Strategy: diversify equity, debt, revolving credit

PIX/Open Finance scaled fintech; fiscal strain (debt ~75% GDP) raises funding risk

High Selic (13.75% Dec 2023) lifts NIMs but caps loan growth; shift to floating-rate and short-duration assets during hikes is prudent.

Inflation easing (CPI ~3.4% in 2024) and 90+ card delinquencies ~3.2% improve fee income prospects while requiring dynamic risk pricing.

BRL volatility (~15% vs USD 2023–24), informal labor ~40% and unemployment 8–9% (IBGE 2024) mandate granular underwriting and FX hedges.

| Metric | Value |

|---|---|

| Selic (Dec 2023) | 13.75% |

| CPI (2024) | ~3.4% |

| Card 90+ DLQ (2024) | ~3.2% |

| BRL vol (2023–24) | ~15% vs USD |

| Informal labor (IBGE 2024) | ~40% |

| Unemployment (IBGE 2024) | 8–9% |

What You See Is What You Get

Inter&Co PESTLE Analysis

The preview shown here is the exact Inter&Co PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly what you’ll download immediately after buying.

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of Inter&Co—concise, data-driven insights into political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it's ready to use and editable. Buy the full report to get the complete deep-dive instantly.

Political factors

Regulatory stance of Brazil’s Central Bank

Brazil’s Central Bank is proactive on innovation, having launched PIX in 2020 and rolled out Open Finance from 2021. Supportive BCB policy through 2024 has enabled rapid fintech growth, aiding Inter&Co’s user and product expansion. Tighter supervisory cycles increase compliance costs and capital buffers. Continuous engagement with the BCB is essential to anticipate rule changes.

Government priorities on financial inclusion

Brazilian administrations emphasize inclusion and competition, favoring digital-first banks as population (~214 million in 2023) shifts to digital rails; Nubank reached about 80 million customers by 2024, illustrating scale. Public programs and Pix-led payment rails channel more users into the formal system, boosting onboarding. Post-election policy shifts can reallocate subsidies or regulatory support. Inter&Co must align its super app narrative with inclusion goals to retain goodwill.

Fiscal stability and sovereign risk

Brazil’s fiscal path—with gross public debt near 75% of GDP and an EMBI sovereign spread around 300 bps in 2024—directly shapes macro stability, policy rates and investor sentiment. Rising sovereign risk premia can widen funding costs and tighten credit for banks and nonbank lenders. Fiscal stability supports credit growth and higher fintech equity multiples. Inter&Co should recalibrate risk appetite and provisioning in line with fiscal newsflow.

Trade and geopolitical dynamics

Global tensions in 2024–25 have intermittently tightened capital flows to emerging markets such as Brazil, triggering risk-off episodes that can weaken the real and raise corporate funding costs.

Nearshoring and revived cross-border commerce present revenue and user-growth opportunities a super app can capture by facilitating payments, logistics and B2B services across the region.

Inter&Co should build optionality for regional expansion—cash buffers, modular product stacks and contingent funding lines—to scale quickly when conditions improve.

- Tag: risk-off — episodic FX pressure on BRL

- Tag: funding — higher short-term borrowing costs in stress

- Tag: opportunity — nearshoring-driven trade growth 2024–25

- Tag: strategy — preserve optionality for regional rollouts

Public digital infrastructure and state-owned competitors

PIX and other government-led instant-payment platforms set baseline expectations for near-instant settlement and near-zero fees, pushing private players to match speed and cost while PIX adoption scaled rapidly across Brazil.

State-owned banks such as Caixa and Banco do Brasil—which together control roughly 40% of retail deposits—can shape pricing and credit availability, affecting market dynamics for Inter&Co.

Inter&Co can differentiate through superior UX and bundled ecosystem services, but must stay ready to pivot quickly when policy changes to public platforms alter fee structures or technical requirements.

- PIX-like platforms: baseline expectations on speed/cost

- State banks: ~40% retail deposit influence

- Inter&Co edge: UX + ecosystem services

- Risk: rapid product changes after policy shifts

PIX/Open Finance scaled fintech; fiscal strain (debt ~75% GDP) raises funding risk

BCB-led innovation (PIX 2020; Open Finance 2021) and supportive policy through 2024 fueled fintech scale (Brazil pop ~214m; Nubank ~80m customers in 2024), but tighter supervision raises compliance costs. Fiscal stress (gross public debt ~75% of GDP; EMBI ~300bps in 2024) elevates funding risk; state banks hold ~40% retail deposits. Inter&Co must preserve optionality for regional expansion and adjust provisioning to fiscal/newsflow.

| Tag | Metric | 2024/25 |

|---|---|---|

| innovation | PIX launch / Open Finance | 2020 / 2021 |

| scale | Population / Nubank users | 214M / ~80M (2024) |

| fiscal | Debt / EMBI | ~75% GDP / ~300bps (2024) |

| competition | State bank deposit share | ~40% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Inter&Co, with data-driven, region- and industry-specific insights and forward-looking scenarios to identify risks and opportunities for executives, investors and strategists.

Inter&Co's PESTLE delivers a visually segmented, concise summary of external risks and opportunities that’s easily dropped into presentations or shared across teams, with editable notes for region- or business-specific context to speed decision-making.

Economic factors

Interest rate cycle and credit demand

Selic at 13.75% (Dec 2023) directly boosts net interest margins but can restrain loan growth when tightened; easing phases historically support origination and improve asset quality. Tightening increases borrower stress and NPL risk, requiring active pricing and duration management. Inter&Co should align product mix to rate trajectories, favoring floating-rate and shorter-duration assets during hikes and origination-heavy strategies when cuts resume.

Inflation and consumer spending

Inflation erodes real incomes and drove higher consumer loan delinquencies as credit-card 90+ day delinquencies rose toward 3.2% in 2024, pressuring Inter&Co’s receivables. Elevated prices compressed discretionary spend across super app verticals, with US PCE spending growth slowing to about 2.6% in 2024. Disinflation into 2025 (CPI ~3.4% in 2024) supports fee income and cross-selling, while dynamic risk-based pricing protects margins.

Exchange rate volatility

BRL swings (~15% vs USD in 2023–24) pressure Inter&Co funding costs, lift imported tech prices and dampen investor appetite after sharper volatility episodes. If Inter&Co carries USD-linked capex or partner payouts, hedging (forwards/options) is critical to cap FX-driven margin erosion. Currency moves also reshaped cross-border e-commerce flows—Brazilian cross-border sales grew ~16% in 2024—so transparent FX pass-through helps stabilize unit economics.

Labor market and income formalization

Gig and informal work account for roughly 40% of Brazil's workforce (IBGE, 2024), concentrating credit risk in variable-income segments; improving formalization raises KYC data quality and measurable repayment capacity. Inter&Co can underwrite variable incomes using granular cash-flow signals from bank and app data, while employment cycles and an unemployment rate near 8–9% (IBGE, 2024) will drive portfolio performance.

- Informal share ~40% (IBGE 2024)

- Unemployment ~8–9% (IBGE 2024)

- Formalization → better KYC, higher repayment predictability

- Underwrite via granular cash-flow, adapt to employment cycles

Capital markets access and cost of capital

Equity and debt market windows determine Inter&Co growth funding; with benchmark policy rates around 5.25-5.50% (US mid-2024) access shifts timing and pricing of raises. Risk sentiment to fintech drives valuation multiples and IPO activity, affecting cost of equity. Lower capital costs expand spend on customer acquisition and R&D; Inter&Co should keep diversified funding and 6–12 months cash buffers.

- Market rate: 5.25–5.50%

- Liquidity buffer: 6–12 months

- Strategy: diversify equity, debt, revolving credit

PIX/Open Finance scaled fintech; fiscal strain (debt ~75% GDP) raises funding risk

High Selic (13.75% Dec 2023) lifts NIMs but caps loan growth; shift to floating-rate and short-duration assets during hikes is prudent.

Inflation easing (CPI ~3.4% in 2024) and 90+ card delinquencies ~3.2% improve fee income prospects while requiring dynamic risk pricing.

BRL volatility (~15% vs USD 2023–24), informal labor ~40% and unemployment 8–9% (IBGE 2024) mandate granular underwriting and FX hedges.

| Metric | Value |

|---|---|

| Selic (Dec 2023) | 13.75% |

| CPI (2024) | ~3.4% |

| Card 90+ DLQ (2024) | ~3.2% |

| BRL vol (2023–24) | ~15% vs USD |

| Informal labor (IBGE 2024) | ~40% |

| Unemployment (IBGE 2024) | 8–9% |

What You See Is What You Get

Inter&Co PESTLE Analysis

The preview shown here is the exact Inter&Co PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly what you’ll download immediately after buying.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of Inter&Co—concise, data-driven insights into political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it's ready to use and editable. Buy the full report to get the complete deep-dive instantly.

Political factors

Regulatory stance of Brazil’s Central Bank

Brazil’s Central Bank is proactive on innovation, having launched PIX in 2020 and rolled out Open Finance from 2021. Supportive BCB policy through 2024 has enabled rapid fintech growth, aiding Inter&Co’s user and product expansion. Tighter supervisory cycles increase compliance costs and capital buffers. Continuous engagement with the BCB is essential to anticipate rule changes.

Government priorities on financial inclusion

Brazilian administrations emphasize inclusion and competition, favoring digital-first banks as population (~214 million in 2023) shifts to digital rails; Nubank reached about 80 million customers by 2024, illustrating scale. Public programs and Pix-led payment rails channel more users into the formal system, boosting onboarding. Post-election policy shifts can reallocate subsidies or regulatory support. Inter&Co must align its super app narrative with inclusion goals to retain goodwill.

Fiscal stability and sovereign risk

Brazil’s fiscal path—with gross public debt near 75% of GDP and an EMBI sovereign spread around 300 bps in 2024—directly shapes macro stability, policy rates and investor sentiment. Rising sovereign risk premia can widen funding costs and tighten credit for banks and nonbank lenders. Fiscal stability supports credit growth and higher fintech equity multiples. Inter&Co should recalibrate risk appetite and provisioning in line with fiscal newsflow.

Trade and geopolitical dynamics

Global tensions in 2024–25 have intermittently tightened capital flows to emerging markets such as Brazil, triggering risk-off episodes that can weaken the real and raise corporate funding costs.

Nearshoring and revived cross-border commerce present revenue and user-growth opportunities a super app can capture by facilitating payments, logistics and B2B services across the region.

Inter&Co should build optionality for regional expansion—cash buffers, modular product stacks and contingent funding lines—to scale quickly when conditions improve.

- Tag: risk-off — episodic FX pressure on BRL

- Tag: funding — higher short-term borrowing costs in stress

- Tag: opportunity — nearshoring-driven trade growth 2024–25

- Tag: strategy — preserve optionality for regional rollouts

Public digital infrastructure and state-owned competitors

PIX and other government-led instant-payment platforms set baseline expectations for near-instant settlement and near-zero fees, pushing private players to match speed and cost while PIX adoption scaled rapidly across Brazil.

State-owned banks such as Caixa and Banco do Brasil—which together control roughly 40% of retail deposits—can shape pricing and credit availability, affecting market dynamics for Inter&Co.

Inter&Co can differentiate through superior UX and bundled ecosystem services, but must stay ready to pivot quickly when policy changes to public platforms alter fee structures or technical requirements.

- PIX-like platforms: baseline expectations on speed/cost

- State banks: ~40% retail deposit influence

- Inter&Co edge: UX + ecosystem services

- Risk: rapid product changes after policy shifts

PIX/Open Finance scaled fintech; fiscal strain (debt ~75% GDP) raises funding risk

BCB-led innovation (PIX 2020; Open Finance 2021) and supportive policy through 2024 fueled fintech scale (Brazil pop ~214m; Nubank ~80m customers in 2024), but tighter supervision raises compliance costs. Fiscal stress (gross public debt ~75% of GDP; EMBI ~300bps in 2024) elevates funding risk; state banks hold ~40% retail deposits. Inter&Co must preserve optionality for regional expansion and adjust provisioning to fiscal/newsflow.

| Tag | Metric | 2024/25 |

|---|---|---|

| innovation | PIX launch / Open Finance | 2020 / 2021 |

| scale | Population / Nubank users | 214M / ~80M (2024) |

| fiscal | Debt / EMBI | ~75% GDP / ~300bps (2024) |

| competition | State bank deposit share | ~40% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Inter&Co, with data-driven, region- and industry-specific insights and forward-looking scenarios to identify risks and opportunities for executives, investors and strategists.

Inter&Co's PESTLE delivers a visually segmented, concise summary of external risks and opportunities that’s easily dropped into presentations or shared across teams, with editable notes for region- or business-specific context to speed decision-making.

Economic factors

Interest rate cycle and credit demand

Selic at 13.75% (Dec 2023) directly boosts net interest margins but can restrain loan growth when tightened; easing phases historically support origination and improve asset quality. Tightening increases borrower stress and NPL risk, requiring active pricing and duration management. Inter&Co should align product mix to rate trajectories, favoring floating-rate and shorter-duration assets during hikes and origination-heavy strategies when cuts resume.

Inflation and consumer spending

Inflation erodes real incomes and drove higher consumer loan delinquencies as credit-card 90+ day delinquencies rose toward 3.2% in 2024, pressuring Inter&Co’s receivables. Elevated prices compressed discretionary spend across super app verticals, with US PCE spending growth slowing to about 2.6% in 2024. Disinflation into 2025 (CPI ~3.4% in 2024) supports fee income and cross-selling, while dynamic risk-based pricing protects margins.

Exchange rate volatility

BRL swings (~15% vs USD in 2023–24) pressure Inter&Co funding costs, lift imported tech prices and dampen investor appetite after sharper volatility episodes. If Inter&Co carries USD-linked capex or partner payouts, hedging (forwards/options) is critical to cap FX-driven margin erosion. Currency moves also reshaped cross-border e-commerce flows—Brazilian cross-border sales grew ~16% in 2024—so transparent FX pass-through helps stabilize unit economics.

Labor market and income formalization

Gig and informal work account for roughly 40% of Brazil's workforce (IBGE, 2024), concentrating credit risk in variable-income segments; improving formalization raises KYC data quality and measurable repayment capacity. Inter&Co can underwrite variable incomes using granular cash-flow signals from bank and app data, while employment cycles and an unemployment rate near 8–9% (IBGE, 2024) will drive portfolio performance.

- Informal share ~40% (IBGE 2024)

- Unemployment ~8–9% (IBGE 2024)

- Formalization → better KYC, higher repayment predictability

- Underwrite via granular cash-flow, adapt to employment cycles

Capital markets access and cost of capital

Equity and debt market windows determine Inter&Co growth funding; with benchmark policy rates around 5.25-5.50% (US mid-2024) access shifts timing and pricing of raises. Risk sentiment to fintech drives valuation multiples and IPO activity, affecting cost of equity. Lower capital costs expand spend on customer acquisition and R&D; Inter&Co should keep diversified funding and 6–12 months cash buffers.

- Market rate: 5.25–5.50%

- Liquidity buffer: 6–12 months

- Strategy: diversify equity, debt, revolving credit

PIX/Open Finance scaled fintech; fiscal strain (debt ~75% GDP) raises funding risk

High Selic (13.75% Dec 2023) lifts NIMs but caps loan growth; shift to floating-rate and short-duration assets during hikes is prudent.

Inflation easing (CPI ~3.4% in 2024) and 90+ card delinquencies ~3.2% improve fee income prospects while requiring dynamic risk pricing.

BRL volatility (~15% vs USD 2023–24), informal labor ~40% and unemployment 8–9% (IBGE 2024) mandate granular underwriting and FX hedges.

| Metric | Value |

|---|---|

| Selic (Dec 2023) | 13.75% |

| CPI (2024) | ~3.4% |

| Card 90+ DLQ (2024) | ~3.2% |

| BRL vol (2023–24) | ~15% vs USD |

| Informal labor (IBGE 2024) | ~40% |

| Unemployment (IBGE 2024) | 8–9% |

What You See Is What You Get

Inter&Co PESTLE Analysis

The preview shown here is the exact Inter&Co PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly what you’ll download immediately after buying.