InterDigital Porter's Five Forces Analysis

From Overview to Strategy Blueprint

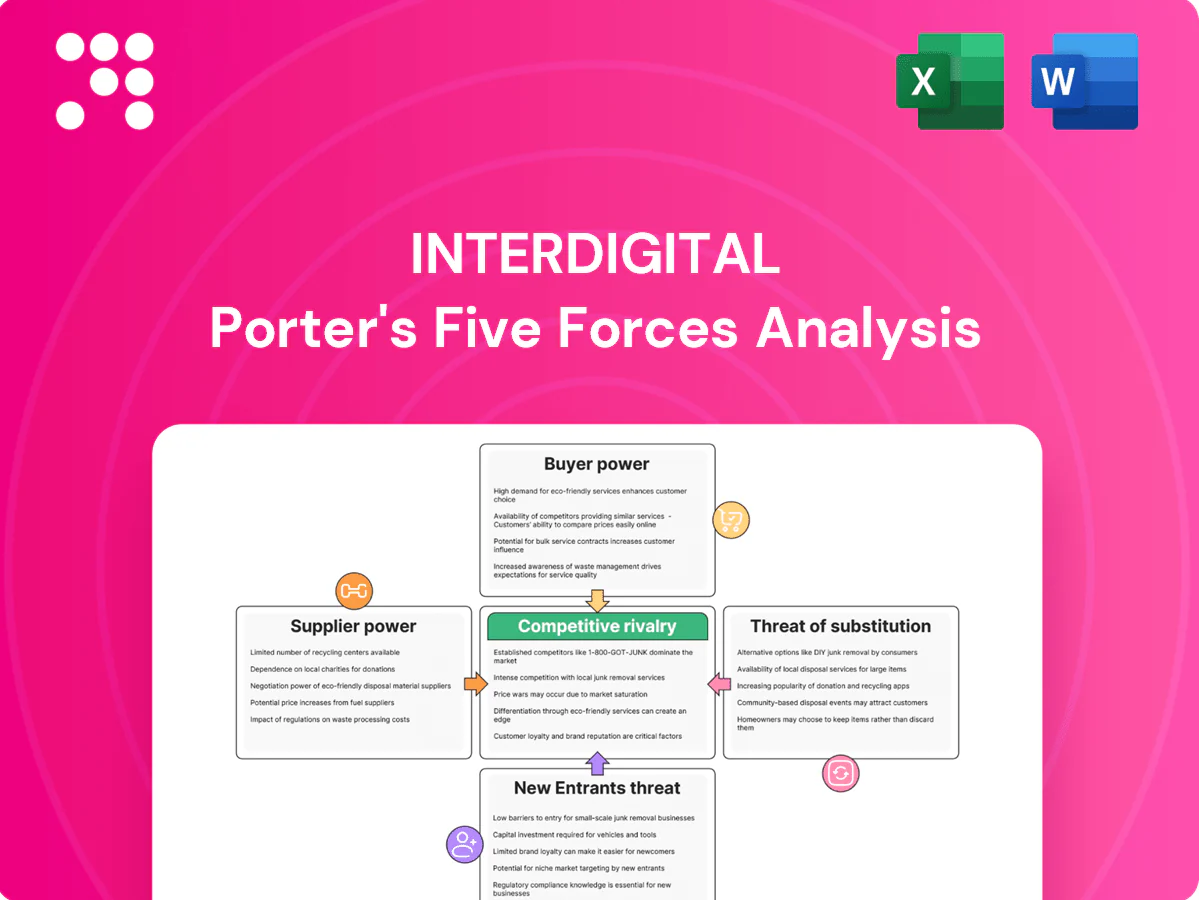

InterDigital operates in a patent-heavy, licensing-driven ecosystem where supplier power is moderate, buyer negotiations are pivotal, and rivalry hinges on IP strength and cross-licensing; substitutes and new entrants face high barriers yet technological shifts pose risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore InterDigital’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce deep-tech talent

InterDigital depends on a scarce global pool of PhD-level engineers and scientists in wireless and video, giving these suppliers strong bargaining power through wage and retention pressure. Visa constraints—notably the US H-1B cap of 85,000—plus location and hybrid-work dynamics further tighten supply. The company’s long-term incentives and research culture mitigate turnover but do not eliminate talent leverage. Recruitment costs and premium compensation remain material.

Standards participation inputs

Access to standards bodies, testbeds and academic partners (eg 3GPP, ETSI, IEEE) is critical; 3GPP involved over 700 contributors in 2024, concentrating influence among leading labs. Influential contributors can secure funding, co-authorship or IP-sharing terms, giving selective upstream partners negotiation leverage. Multi-partner consortia dilute single-source dependence and lower supplier bargaining power.

Specialized tools and IP

Simulation software, test equipment and complementary IP for wireless systems are supplied mainly by a small set of vendors—Synopsys, Cadence, Siemens EDA for simulation and Keysight, Rohde & Schwarz, Anritsu for test gear—concentration among roughly 3–5 leaders elevates supplier leverage.

Vendor dominance increases switching costs and pricing power, especially given multi-year licensing and interoperability requirements that lock in toolchains.

Long contracts and certified IP bundles (codecs, FEC) further entrench relationships and can raise renewal prices.

Open-source stacks and in-house emulation efforts partially offset supplier power but typically cover only a minority of high-end needs.

Cloud and compute resources

Training, simulation and video workloads depend on major cloud GPUs/CPUs, leaving InterDigital exposed to hyperscaler suppliers; the top three hyperscalers held about 66% of global IaaS in 2024 (Statista), giving them moderate pricing power. Multi-cloud strategies and reserved/Savings Plans (up to ~72% discounts on AWS) can materially temper costs. GPU hardware cycles and surging demand for data‑center GPUs in 2024 periodically tightened capacity and raised supplier leverage.

- Supplier concentration: top-3 ≈66% IaaS (2024)

- Cost mitigation: reserved/Savings Plans up to ~72% off

- Exposure: heavy GPU reliance for training/simulation/video

- Volatility: GPU cycles/demand in 2024 caused temporary supply tightness

Patent acquisition and collaborators

Occasional portfolio top-ups from universities or peers create episodic supplier power, with sellers of standards-essential patents able to demand premiums, especially when auction dynamics and litigation history signal strong enforcement outcomes.

InterDigital’s sustained internal R&D productivity and active patent prosecution reduce reliance on external IP, tempering supplier leverage during licensing negotiations.

- episodic university/peer deals raise supplier leverage

- standards-essential patents command premiums

- auction outcomes and litigation precedent drive pricing

- robust internal R&D lowers external dependency

PhD scarcity and 3–5 EDA vendors amplify supplier power; hyperscalers ~66%, reserved deals cut costs

InterDigital faces strong supplier power from scarce PhD wireless talent (US H-1B cap 85,000) and concentrated EDA/test vendors (3–5 leaders), raising wages and switching costs. Hyperscalers held ~66% IaaS in 2024, and reserved plans can cut cloud costs up to ~72%, partially offsetting leverage. In-house R&D and open-source lower but do not remove supplier influence.

| Metric | 2024 Value |

|---|---|

| H-1B cap | 85,000 |

| Top-3 IaaS share | ≈66% |

| Reserved/Savings discount | up to ~72% |

| EDA/test vendor concentration | 3–5 leaders |

What is included in the product

Tailored Porter's Five Forces analysis of InterDigital that uncovers competitive drivers, buyer and supplier power, and threats from substitutes and disruptive entrants. Evaluates market entry barriers, IP strength and licensing dynamics to inform strategy, investor materials, and customizable reports.

One-sheet InterDigital Porter's Five Forces summary that instantly visualizes competitive pressure with a clean spider chart—perfect for quick decisions and slide-ready decks. Easily customize force levels, swap in your data, and duplicate scenarios without macros to relieve analysis bottlenecks.

Customers Bargaining Power

Scale of licensees

Handset OEMs, CE makers and infrastructure vendors are highly consolidated: the top five smartphone OEMs held about 70% of global shipments in 2024 (≈1.2 billion units shipped), while Ericsson, Huawei and Nokia dominated RAN equipment, concentrating buying power. Their volume and legal resources enable tough negotiations, protracted disputes and tactics to delay payments, litigate or push for patent pool rates, yielding high buyer power in practice.

FRAND and regulatory context

SEPs licensed under FRAND anchor rate expectations, with ETSI recording over 100,000 declared 5G-related SEPs as of 2024, compressing negotiated royalties. Buyers leverage FRAND commitments and heightened regulatory scrutiny to push for lower, standardized terms and frequent FRAND challenges. Jurisdictional differences enable forum-shopping by large OEMs, while increased transparency and compliance demands materially limit InterDigital’s pricing latitude.

Cross-licensing dynamics

Vertically integrated players such as Samsung and Apple hold substantial counter-portfolios, enabling cross-licensing that reduces net payments and strengthens buyer leverage. Cross-licenses and netting arrangements commonly compress royalty yield, often turning gross rates into much lower net royalties across product lines. InterDigital’s business model is licensing-focused with no significant device sales, limiting its ability to offset payments via product portfolios. Global smartphone shipments were about 1.1 billion in 2024, amplifying buyers’ negotiating scale.

Patent pools and collective bargaining

Pools in video and IoT offer buyers aggregated, lower-rate access and reduce transaction costs; large buyers often prefer pools for price certainty, shifting bargaining leverage away from bilateral licensors and depressing standalone licensing rates. InterDigital, with roughly 33,000 patents and patent applications, can join or compete with pools, materially shaping its realized economics and royalty mix.

- Pools = aggregated access, lower per-unit rates

- Large buyers favor pools for price certainty, pressuring standalone rates

- InterDigital's ~33,000 patents give it strategic choice to join or compete with pools

Substitution and delay options

Bidders cannot avoid SEPs for standard compliance, but buyers in 2024 routinely use execution delays, legal timelines and partial design-arounds to lower royalty exposure; OEMs commonly negotiate payment timing of 30–180 days, creating 60–120 day cash float advantages for large buyers.

- Delay leverage: exploit litigation/timing

- Design-arounds: reduce non‑essential SEP exposure

- Payment timing: 30–180 day terms

- Settlement cycles: favor large buyers via 60–120 day cash management

OEM concentration, >100,000 5G SEPs and 30-180 day terms squeeze royalties

Handset OEMs, CE and RAN vendors are concentrated: top five smartphone OEMs held ~70% of shipments (≈1.2bn units in 2024), giving buyers scale and legal leverage. ETSI recorded >100,000 declared 5G SEPs (2024) and FRAND anchors compress royalties; buyers push FRAND challenges and forum shopping. Vertically integrated OEMs cross‑license and use delay, design‑arounds and 30–180 day payment terms (60–120 day cash float), pressuring licensors like InterDigital (~33,000 patents).

| Metric | 2024 |

|---|---|

| Top5 OEM share | ~70% |

| Smartphone shipments | ≈1.2bn |

| Declared 5G SEPs | >100,000 |

| InterDigital patents | ≈33,000 |

| Payment terms | 30–180 days |

What You See Is What You Get

InterDigital Porter's Five Forces Analysis

This preview shows the exact InterDigital Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted, and contains the same detailed assessment of supplier power, buyer power, competitive rivalry, threats of substitution and entry. Once you buy, you get instant access to this identical downloadable document, ready for use.

From Overview to Strategy Blueprint

InterDigital operates in a patent-heavy, licensing-driven ecosystem where supplier power is moderate, buyer negotiations are pivotal, and rivalry hinges on IP strength and cross-licensing; substitutes and new entrants face high barriers yet technological shifts pose risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore InterDigital’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce deep-tech talent

InterDigital depends on a scarce global pool of PhD-level engineers and scientists in wireless and video, giving these suppliers strong bargaining power through wage and retention pressure. Visa constraints—notably the US H-1B cap of 85,000—plus location and hybrid-work dynamics further tighten supply. The company’s long-term incentives and research culture mitigate turnover but do not eliminate talent leverage. Recruitment costs and premium compensation remain material.

Standards participation inputs

Access to standards bodies, testbeds and academic partners (eg 3GPP, ETSI, IEEE) is critical; 3GPP involved over 700 contributors in 2024, concentrating influence among leading labs. Influential contributors can secure funding, co-authorship or IP-sharing terms, giving selective upstream partners negotiation leverage. Multi-partner consortia dilute single-source dependence and lower supplier bargaining power.

Specialized tools and IP

Simulation software, test equipment and complementary IP for wireless systems are supplied mainly by a small set of vendors—Synopsys, Cadence, Siemens EDA for simulation and Keysight, Rohde & Schwarz, Anritsu for test gear—concentration among roughly 3–5 leaders elevates supplier leverage.

Vendor dominance increases switching costs and pricing power, especially given multi-year licensing and interoperability requirements that lock in toolchains.

Long contracts and certified IP bundles (codecs, FEC) further entrench relationships and can raise renewal prices.

Open-source stacks and in-house emulation efforts partially offset supplier power but typically cover only a minority of high-end needs.

Cloud and compute resources

Training, simulation and video workloads depend on major cloud GPUs/CPUs, leaving InterDigital exposed to hyperscaler suppliers; the top three hyperscalers held about 66% of global IaaS in 2024 (Statista), giving them moderate pricing power. Multi-cloud strategies and reserved/Savings Plans (up to ~72% discounts on AWS) can materially temper costs. GPU hardware cycles and surging demand for data‑center GPUs in 2024 periodically tightened capacity and raised supplier leverage.

- Supplier concentration: top-3 ≈66% IaaS (2024)

- Cost mitigation: reserved/Savings Plans up to ~72% off

- Exposure: heavy GPU reliance for training/simulation/video

- Volatility: GPU cycles/demand in 2024 caused temporary supply tightness

Patent acquisition and collaborators

Occasional portfolio top-ups from universities or peers create episodic supplier power, with sellers of standards-essential patents able to demand premiums, especially when auction dynamics and litigation history signal strong enforcement outcomes.

InterDigital’s sustained internal R&D productivity and active patent prosecution reduce reliance on external IP, tempering supplier leverage during licensing negotiations.

- episodic university/peer deals raise supplier leverage

- standards-essential patents command premiums

- auction outcomes and litigation precedent drive pricing

- robust internal R&D lowers external dependency

PhD scarcity and 3–5 EDA vendors amplify supplier power; hyperscalers ~66%, reserved deals cut costs

InterDigital faces strong supplier power from scarce PhD wireless talent (US H-1B cap 85,000) and concentrated EDA/test vendors (3–5 leaders), raising wages and switching costs. Hyperscalers held ~66% IaaS in 2024, and reserved plans can cut cloud costs up to ~72%, partially offsetting leverage. In-house R&D and open-source lower but do not remove supplier influence.

| Metric | 2024 Value |

|---|---|

| H-1B cap | 85,000 |

| Top-3 IaaS share | ≈66% |

| Reserved/Savings discount | up to ~72% |

| EDA/test vendor concentration | 3–5 leaders |

What is included in the product

Tailored Porter's Five Forces analysis of InterDigital that uncovers competitive drivers, buyer and supplier power, and threats from substitutes and disruptive entrants. Evaluates market entry barriers, IP strength and licensing dynamics to inform strategy, investor materials, and customizable reports.

One-sheet InterDigital Porter's Five Forces summary that instantly visualizes competitive pressure with a clean spider chart—perfect for quick decisions and slide-ready decks. Easily customize force levels, swap in your data, and duplicate scenarios without macros to relieve analysis bottlenecks.

Customers Bargaining Power

Scale of licensees

Handset OEMs, CE makers and infrastructure vendors are highly consolidated: the top five smartphone OEMs held about 70% of global shipments in 2024 (≈1.2 billion units shipped), while Ericsson, Huawei and Nokia dominated RAN equipment, concentrating buying power. Their volume and legal resources enable tough negotiations, protracted disputes and tactics to delay payments, litigate or push for patent pool rates, yielding high buyer power in practice.

FRAND and regulatory context

SEPs licensed under FRAND anchor rate expectations, with ETSI recording over 100,000 declared 5G-related SEPs as of 2024, compressing negotiated royalties. Buyers leverage FRAND commitments and heightened regulatory scrutiny to push for lower, standardized terms and frequent FRAND challenges. Jurisdictional differences enable forum-shopping by large OEMs, while increased transparency and compliance demands materially limit InterDigital’s pricing latitude.

Cross-licensing dynamics

Vertically integrated players such as Samsung and Apple hold substantial counter-portfolios, enabling cross-licensing that reduces net payments and strengthens buyer leverage. Cross-licenses and netting arrangements commonly compress royalty yield, often turning gross rates into much lower net royalties across product lines. InterDigital’s business model is licensing-focused with no significant device sales, limiting its ability to offset payments via product portfolios. Global smartphone shipments were about 1.1 billion in 2024, amplifying buyers’ negotiating scale.

Patent pools and collective bargaining

Pools in video and IoT offer buyers aggregated, lower-rate access and reduce transaction costs; large buyers often prefer pools for price certainty, shifting bargaining leverage away from bilateral licensors and depressing standalone licensing rates. InterDigital, with roughly 33,000 patents and patent applications, can join or compete with pools, materially shaping its realized economics and royalty mix.

- Pools = aggregated access, lower per-unit rates

- Large buyers favor pools for price certainty, pressuring standalone rates

- InterDigital's ~33,000 patents give it strategic choice to join or compete with pools

Substitution and delay options

Bidders cannot avoid SEPs for standard compliance, but buyers in 2024 routinely use execution delays, legal timelines and partial design-arounds to lower royalty exposure; OEMs commonly negotiate payment timing of 30–180 days, creating 60–120 day cash float advantages for large buyers.

- Delay leverage: exploit litigation/timing

- Design-arounds: reduce non‑essential SEP exposure

- Payment timing: 30–180 day terms

- Settlement cycles: favor large buyers via 60–120 day cash management

OEM concentration, >100,000 5G SEPs and 30-180 day terms squeeze royalties

Handset OEMs, CE and RAN vendors are concentrated: top five smartphone OEMs held ~70% of shipments (≈1.2bn units in 2024), giving buyers scale and legal leverage. ETSI recorded >100,000 declared 5G SEPs (2024) and FRAND anchors compress royalties; buyers push FRAND challenges and forum shopping. Vertically integrated OEMs cross‑license and use delay, design‑arounds and 30–180 day payment terms (60–120 day cash float), pressuring licensors like InterDigital (~33,000 patents).

| Metric | 2024 |

|---|---|

| Top5 OEM share | ~70% |

| Smartphone shipments | ≈1.2bn |

| Declared 5G SEPs | >100,000 |

| InterDigital patents | ≈33,000 |

| Payment terms | 30–180 days |

What You See Is What You Get

InterDigital Porter's Five Forces Analysis

This preview shows the exact InterDigital Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted, and contains the same detailed assessment of supplier power, buyer power, competitive rivalry, threats of substitution and entry. Once you buy, you get instant access to this identical downloadable document, ready for use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

InterDigital operates in a patent-heavy, licensing-driven ecosystem where supplier power is moderate, buyer negotiations are pivotal, and rivalry hinges on IP strength and cross-licensing; substitutes and new entrants face high barriers yet technological shifts pose risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore InterDigital’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce deep-tech talent

InterDigital depends on a scarce global pool of PhD-level engineers and scientists in wireless and video, giving these suppliers strong bargaining power through wage and retention pressure. Visa constraints—notably the US H-1B cap of 85,000—plus location and hybrid-work dynamics further tighten supply. The company’s long-term incentives and research culture mitigate turnover but do not eliminate talent leverage. Recruitment costs and premium compensation remain material.

Standards participation inputs

Access to standards bodies, testbeds and academic partners (eg 3GPP, ETSI, IEEE) is critical; 3GPP involved over 700 contributors in 2024, concentrating influence among leading labs. Influential contributors can secure funding, co-authorship or IP-sharing terms, giving selective upstream partners negotiation leverage. Multi-partner consortia dilute single-source dependence and lower supplier bargaining power.

Specialized tools and IP

Simulation software, test equipment and complementary IP for wireless systems are supplied mainly by a small set of vendors—Synopsys, Cadence, Siemens EDA for simulation and Keysight, Rohde & Schwarz, Anritsu for test gear—concentration among roughly 3–5 leaders elevates supplier leverage.

Vendor dominance increases switching costs and pricing power, especially given multi-year licensing and interoperability requirements that lock in toolchains.

Long contracts and certified IP bundles (codecs, FEC) further entrench relationships and can raise renewal prices.

Open-source stacks and in-house emulation efforts partially offset supplier power but typically cover only a minority of high-end needs.

Cloud and compute resources

Training, simulation and video workloads depend on major cloud GPUs/CPUs, leaving InterDigital exposed to hyperscaler suppliers; the top three hyperscalers held about 66% of global IaaS in 2024 (Statista), giving them moderate pricing power. Multi-cloud strategies and reserved/Savings Plans (up to ~72% discounts on AWS) can materially temper costs. GPU hardware cycles and surging demand for data‑center GPUs in 2024 periodically tightened capacity and raised supplier leverage.

- Supplier concentration: top-3 ≈66% IaaS (2024)

- Cost mitigation: reserved/Savings Plans up to ~72% off

- Exposure: heavy GPU reliance for training/simulation/video

- Volatility: GPU cycles/demand in 2024 caused temporary supply tightness

Patent acquisition and collaborators

Occasional portfolio top-ups from universities or peers create episodic supplier power, with sellers of standards-essential patents able to demand premiums, especially when auction dynamics and litigation history signal strong enforcement outcomes.

InterDigital’s sustained internal R&D productivity and active patent prosecution reduce reliance on external IP, tempering supplier leverage during licensing negotiations.

- episodic university/peer deals raise supplier leverage

- standards-essential patents command premiums

- auction outcomes and litigation precedent drive pricing

- robust internal R&D lowers external dependency

PhD scarcity and 3–5 EDA vendors amplify supplier power; hyperscalers ~66%, reserved deals cut costs

InterDigital faces strong supplier power from scarce PhD wireless talent (US H-1B cap 85,000) and concentrated EDA/test vendors (3–5 leaders), raising wages and switching costs. Hyperscalers held ~66% IaaS in 2024, and reserved plans can cut cloud costs up to ~72%, partially offsetting leverage. In-house R&D and open-source lower but do not remove supplier influence.

| Metric | 2024 Value |

|---|---|

| H-1B cap | 85,000 |

| Top-3 IaaS share | ≈66% |

| Reserved/Savings discount | up to ~72% |

| EDA/test vendor concentration | 3–5 leaders |

What is included in the product

Tailored Porter's Five Forces analysis of InterDigital that uncovers competitive drivers, buyer and supplier power, and threats from substitutes and disruptive entrants. Evaluates market entry barriers, IP strength and licensing dynamics to inform strategy, investor materials, and customizable reports.

One-sheet InterDigital Porter's Five Forces summary that instantly visualizes competitive pressure with a clean spider chart—perfect for quick decisions and slide-ready decks. Easily customize force levels, swap in your data, and duplicate scenarios without macros to relieve analysis bottlenecks.

Customers Bargaining Power

Scale of licensees

Handset OEMs, CE makers and infrastructure vendors are highly consolidated: the top five smartphone OEMs held about 70% of global shipments in 2024 (≈1.2 billion units shipped), while Ericsson, Huawei and Nokia dominated RAN equipment, concentrating buying power. Their volume and legal resources enable tough negotiations, protracted disputes and tactics to delay payments, litigate or push for patent pool rates, yielding high buyer power in practice.

FRAND and regulatory context

SEPs licensed under FRAND anchor rate expectations, with ETSI recording over 100,000 declared 5G-related SEPs as of 2024, compressing negotiated royalties. Buyers leverage FRAND commitments and heightened regulatory scrutiny to push for lower, standardized terms and frequent FRAND challenges. Jurisdictional differences enable forum-shopping by large OEMs, while increased transparency and compliance demands materially limit InterDigital’s pricing latitude.

Cross-licensing dynamics

Vertically integrated players such as Samsung and Apple hold substantial counter-portfolios, enabling cross-licensing that reduces net payments and strengthens buyer leverage. Cross-licenses and netting arrangements commonly compress royalty yield, often turning gross rates into much lower net royalties across product lines. InterDigital’s business model is licensing-focused with no significant device sales, limiting its ability to offset payments via product portfolios. Global smartphone shipments were about 1.1 billion in 2024, amplifying buyers’ negotiating scale.

Patent pools and collective bargaining

Pools in video and IoT offer buyers aggregated, lower-rate access and reduce transaction costs; large buyers often prefer pools for price certainty, shifting bargaining leverage away from bilateral licensors and depressing standalone licensing rates. InterDigital, with roughly 33,000 patents and patent applications, can join or compete with pools, materially shaping its realized economics and royalty mix.

- Pools = aggregated access, lower per-unit rates

- Large buyers favor pools for price certainty, pressuring standalone rates

- InterDigital's ~33,000 patents give it strategic choice to join or compete with pools

Substitution and delay options

Bidders cannot avoid SEPs for standard compliance, but buyers in 2024 routinely use execution delays, legal timelines and partial design-arounds to lower royalty exposure; OEMs commonly negotiate payment timing of 30–180 days, creating 60–120 day cash float advantages for large buyers.

- Delay leverage: exploit litigation/timing

- Design-arounds: reduce non‑essential SEP exposure

- Payment timing: 30–180 day terms

- Settlement cycles: favor large buyers via 60–120 day cash management

OEM concentration, >100,000 5G SEPs and 30-180 day terms squeeze royalties

Handset OEMs, CE and RAN vendors are concentrated: top five smartphone OEMs held ~70% of shipments (≈1.2bn units in 2024), giving buyers scale and legal leverage. ETSI recorded >100,000 declared 5G SEPs (2024) and FRAND anchors compress royalties; buyers push FRAND challenges and forum shopping. Vertically integrated OEMs cross‑license and use delay, design‑arounds and 30–180 day payment terms (60–120 day cash float), pressuring licensors like InterDigital (~33,000 patents).

| Metric | 2024 |

|---|---|

| Top5 OEM share | ~70% |

| Smartphone shipments | ≈1.2bn |

| Declared 5G SEPs | >100,000 |

| InterDigital patents | ≈33,000 |

| Payment terms | 30–180 days |

What You See Is What You Get

InterDigital Porter's Five Forces Analysis

This preview shows the exact InterDigital Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted, and contains the same detailed assessment of supplier power, buyer power, competitive rivalry, threats of substitution and entry. Once you buy, you get instant access to this identical downloadable document, ready for use.