International Petroleum Business Model Canvas

Business Model Canvas: Strategic Blueprint for an Integrated Petroleum Business

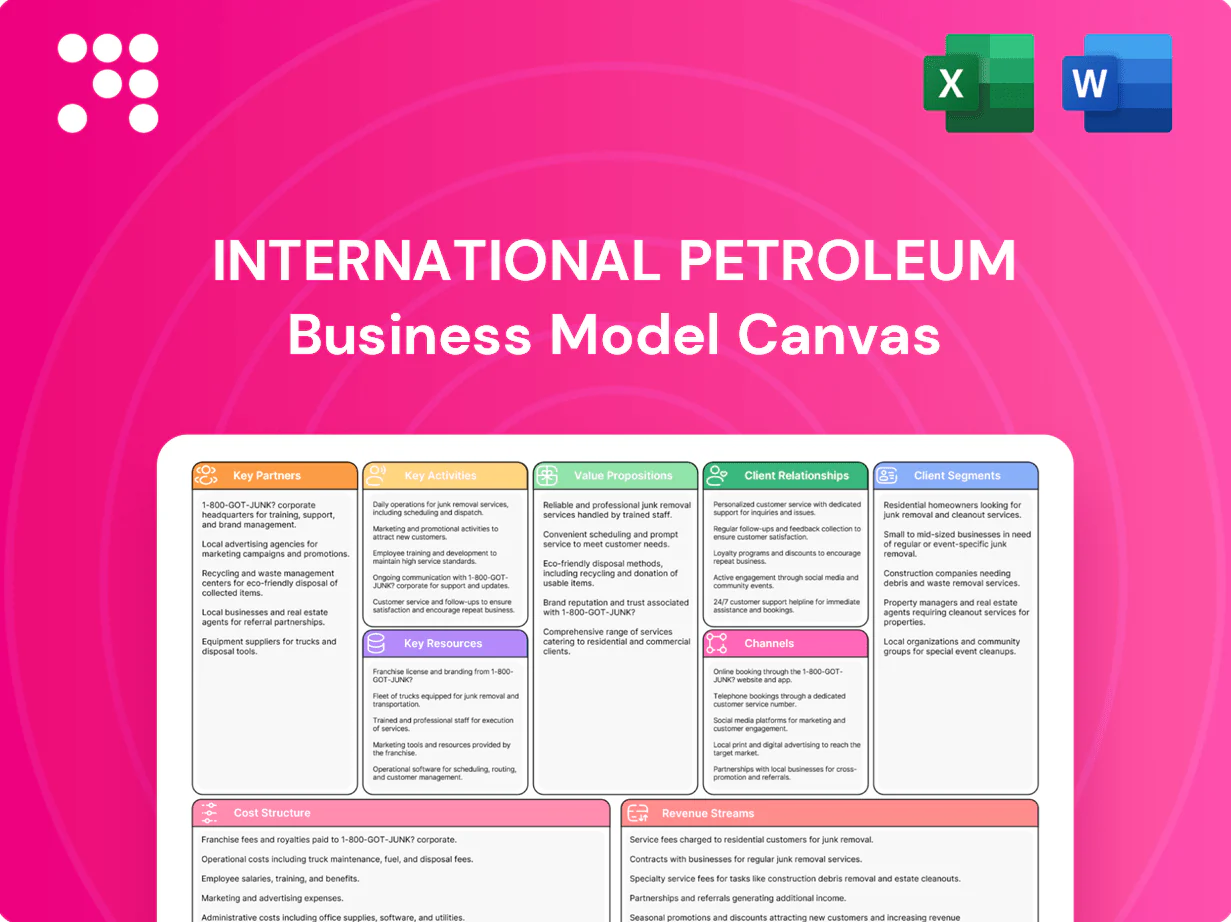

Unlock the strategic blueprint behind International Petroleum with our Business Model Canvas. This concise, sector-specific analysis maps value propositions, key partners, cost structure and revenue streams to show how the company competes and scales. Ideal for investors, advisors and entrepreneurs—download the full Word and Excel Canvas to implement these insights now.

Partnerships

Host governments and regulators (Canada, France, Malaysia)

Partnerships with national and provincial regulators—e.g., Alberta Energy Regulator, France's Ministry for the Ecological Transition, and Petronas—secure licenses, PSCs and compliance approvals, cutting permitting risk and delays. Constructive engagement stabilizes fiscal terms and operational continuity; global oil demand ~101 mb/d in 2024 underscores value of reliable access. Alignment on HSE and environmental standards sustains social license and project timelines.

Oilfield services and equipment providers

Drilling, completions, seismic and maintenance partners enable safe, efficient field operations; the global oilfield services market was about $430 billion in 2024 (Rystad Energy), underpinning scale. Strategic sourcing and long-term contracts commonly cut OPEX ~10% and boost service quality and uptime. Joint tech deployment can raise recovery factors by 5–10% and reduce downtime; local content rules (often 30%+ local supply) improve resilience and response.

Midstream, refiners, and trading offtakers

Pipeline, terminal and storage partners ensure takeaway and market access; Cushing held about 76 million barrels of capacity in 2024 and Permian-to-Gulf pipeline additions totaled roughly 3.5 million b/d by 2024. Refiners and traders supply liquidity, pricing options and destination flexibility; trading houses handled around a third of seaborne crude flows in 2024. Coordinated scheduling cuts bottlenecks and demurrage, while term contracts and lifting programs covering ~60–80% of volumes stabilize cash flow.

Technology, data, and ESG solution providers

Technology partners delivering digital subsurface tools, production-optimization software and emissions-monitoring systems raise uptime, recovery and cost-efficiency while satellite and aerial methane surveys show super-emitters account for roughly half of oil-and-gas methane losses, driving targeted mitigation.

- Digital tools: improve forecasting and integrity management (~20% accuracy gain)

- Methane detection: targets ~50% of emissions from few sites

- Electrification/water partners: cut operational footprint

- Co-development: accelerates innovation with measurable ROI

Banks, insurers, and capital market advisors

Banks, insurers and capital-market advisors enable hedging, bonding and risk transfer for international petroleum firms, with 2024 RCFs commonly sized $200–$2,000m and structured-finance making up roughly 20–30% of upstream project funding in 2024.

- Hedging/bonding: supports collateral and off-take guarantees

- Liquidity: RCFs and structured deals ($200–$2,000m typical)

- Insurance: mitigates operational and political risk (market capacity expanded in 2024)

- Advisors: optimize funding mix and investor communications

Oil market 2024: 101 mb/d demand, $430B services, storage & finance underpin growth

Regulators secure licenses and fiscal stability; world oil demand ~101 mb/d in 2024. Oilfield services market ~430 billion USD in 2024 enables scalable operations. Logistics/storage (Cushing ~76M bbl capacity) and trading support market access. Banks/insurers provide RCFs $200–2,000m and structured finance ~20–30% of upstream funding in 2024.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Licenses/fiscal | 101 mb/d demand |

| OFS | Operations | $430B market |

| Logistics | Storage/flow | Cushing 76M bbl |

| Finance | Liquidity/hedge | RCF $200–2,000M |

| Tech | Optimization/emissions | super-emitters ~50% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for international petroleum companies covering customer segments, channels, value propositions, key activities, partners, cost and revenue structures, risks and competitive advantages, with SWOT-linked insights for investor presentations and strategic decisions.

High-level view of the international petroleum business model with editable cells, letting teams quickly map upstream-to-downstream value chains, risks and partners; saves hours of structuring and accelerates stakeholder alignment for strategic decisions.

Activities

Exploration and appraisal of prospects

Identify and assess resource potential across existing and adjacent acreage using basin-scale screening and data-driven prospect ranking; industry 2024 average exploration success rates ranged 20–35% onshore, 10–15% offshore. Execute seismic (3D surveys typically US$5–20M) and appraisal drilling (appraisal well US$30–120M) to mature inventories. De-risk prospects to feed the development pipeline and optimize scheduling against 2024 Brent ~US$86/bbl and capital allocation constraints.

Field development and drilling programs

Design and execute wells, facilities and tie-ins to unlock reserves, with onshore horizontal wells averaging about 6–8 million USD and deepwater wells commonly exceeding 100 million USD in 2024. Apply fit-for-purpose completions and artificial lift to optimize recovery and lower unit operating costs. Rigorously manage schedules and capex to meet breakeven thresholds (often targeted near 30–50 USD/boe). Integrate HSE by design to reduce incidents and emissions during all phases.

Production operations and optimization

Run assets to >95% availability via vigilant maintenance and integrity programs; leading operators reported uptime targets at or above 95% in 2024. Use data-driven surveillance and predictive analytics to cut unplanned downtime roughly 20–35% and boost recovery. Optimize lift, waterfloods (typical incremental recovery 5–15%) and chemicals (10–20% potential uplift) to lower unit costs. Continuously debottleneck surface facilities to sustain throughput and reduce opex.

Portfolio management and disciplined M&A

Portfolio management and disciplined M&A focus on acquiring, divesting, and farming assets to raise returns and resilience, targeting >15% project IRR and redeploying cash from non-core to higher-margin barrels.

Maintain a mix of short-cycle cash generators and long-life inventory (reserve life index ~8–15 years) and embed NPV10, probabilistic valuation, and strict risk screens.

- Target IRR: >15%

- RLI: 8–15 years

- Use NPV10 & probabilistic risk

HSE, ESG compliance, and stakeholder engagement

Implement robust HSE systems and environmental management across upstream and downstream operations; in 2024, 85% of major oil producers publish TCFD- or ISSB-aligned disclosures to standardize reporting.

Continuously monitor CO2, methane, water use and biodiversity impacts; methane detection deployments rose about 40% in 2023–24, improving leak mitigation.

Engage communities and regulators to maintain trust and align operations with corporate net-zero targets and industry standards.

- HSE systems: mandatory audits, incident rates

- EMISSIONS: CO2, CH4, water, biodiversity metrics

- STAKEHOLDERS: community programs, regulator liaison

Execute 3D & appraisal wells; breakeven US$30–50/bbl, IRR > 15%

Identify and mature prospects (2024 exploration success: onshore 20–35%, offshore 10–15%), execute seismic (3D US$5–20M) and wells (appraisal US$30–120M; deepwater >US$100M) to feed development; run assets to >95% availability and target breakeven US$30–50/bbl; target IRR >15%, RLI 8–15y, embed NPV10 and probabilistic risk.

| Metric | 2024 |

|---|---|

| Expl. success | Onshore 20–35%, Offshore 10–15% |

| 3D cost | US$5–20M |

| Appraisal well | US$30–120M |

| Availability | >95% |

| Target IRR | >15% |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual International Petroleum Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact file—complete, professionally formatted, and ready to edit in Word and Excel. No hidden pages or altered content: what you see is what you’ll download and use for strategy, valuation, or presentations.

Business Model Canvas: Strategic Blueprint for an Integrated Petroleum Business

Unlock the strategic blueprint behind International Petroleum with our Business Model Canvas. This concise, sector-specific analysis maps value propositions, key partners, cost structure and revenue streams to show how the company competes and scales. Ideal for investors, advisors and entrepreneurs—download the full Word and Excel Canvas to implement these insights now.

Partnerships

Host governments and regulators (Canada, France, Malaysia)

Partnerships with national and provincial regulators—e.g., Alberta Energy Regulator, France's Ministry for the Ecological Transition, and Petronas—secure licenses, PSCs and compliance approvals, cutting permitting risk and delays. Constructive engagement stabilizes fiscal terms and operational continuity; global oil demand ~101 mb/d in 2024 underscores value of reliable access. Alignment on HSE and environmental standards sustains social license and project timelines.

Oilfield services and equipment providers

Drilling, completions, seismic and maintenance partners enable safe, efficient field operations; the global oilfield services market was about $430 billion in 2024 (Rystad Energy), underpinning scale. Strategic sourcing and long-term contracts commonly cut OPEX ~10% and boost service quality and uptime. Joint tech deployment can raise recovery factors by 5–10% and reduce downtime; local content rules (often 30%+ local supply) improve resilience and response.

Midstream, refiners, and trading offtakers

Pipeline, terminal and storage partners ensure takeaway and market access; Cushing held about 76 million barrels of capacity in 2024 and Permian-to-Gulf pipeline additions totaled roughly 3.5 million b/d by 2024. Refiners and traders supply liquidity, pricing options and destination flexibility; trading houses handled around a third of seaborne crude flows in 2024. Coordinated scheduling cuts bottlenecks and demurrage, while term contracts and lifting programs covering ~60–80% of volumes stabilize cash flow.

Technology, data, and ESG solution providers

Technology partners delivering digital subsurface tools, production-optimization software and emissions-monitoring systems raise uptime, recovery and cost-efficiency while satellite and aerial methane surveys show super-emitters account for roughly half of oil-and-gas methane losses, driving targeted mitigation.

- Digital tools: improve forecasting and integrity management (~20% accuracy gain)

- Methane detection: targets ~50% of emissions from few sites

- Electrification/water partners: cut operational footprint

- Co-development: accelerates innovation with measurable ROI

Banks, insurers, and capital market advisors

Banks, insurers and capital-market advisors enable hedging, bonding and risk transfer for international petroleum firms, with 2024 RCFs commonly sized $200–$2,000m and structured-finance making up roughly 20–30% of upstream project funding in 2024.

- Hedging/bonding: supports collateral and off-take guarantees

- Liquidity: RCFs and structured deals ($200–$2,000m typical)

- Insurance: mitigates operational and political risk (market capacity expanded in 2024)

- Advisors: optimize funding mix and investor communications

Oil market 2024: 101 mb/d demand, $430B services, storage & finance underpin growth

Regulators secure licenses and fiscal stability; world oil demand ~101 mb/d in 2024. Oilfield services market ~430 billion USD in 2024 enables scalable operations. Logistics/storage (Cushing ~76M bbl capacity) and trading support market access. Banks/insurers provide RCFs $200–2,000m and structured finance ~20–30% of upstream funding in 2024.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Licenses/fiscal | 101 mb/d demand |

| OFS | Operations | $430B market |

| Logistics | Storage/flow | Cushing 76M bbl |

| Finance | Liquidity/hedge | RCF $200–2,000M |

| Tech | Optimization/emissions | super-emitters ~50% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for international petroleum companies covering customer segments, channels, value propositions, key activities, partners, cost and revenue structures, risks and competitive advantages, with SWOT-linked insights for investor presentations and strategic decisions.

High-level view of the international petroleum business model with editable cells, letting teams quickly map upstream-to-downstream value chains, risks and partners; saves hours of structuring and accelerates stakeholder alignment for strategic decisions.

Activities

Exploration and appraisal of prospects

Identify and assess resource potential across existing and adjacent acreage using basin-scale screening and data-driven prospect ranking; industry 2024 average exploration success rates ranged 20–35% onshore, 10–15% offshore. Execute seismic (3D surveys typically US$5–20M) and appraisal drilling (appraisal well US$30–120M) to mature inventories. De-risk prospects to feed the development pipeline and optimize scheduling against 2024 Brent ~US$86/bbl and capital allocation constraints.

Field development and drilling programs

Design and execute wells, facilities and tie-ins to unlock reserves, with onshore horizontal wells averaging about 6–8 million USD and deepwater wells commonly exceeding 100 million USD in 2024. Apply fit-for-purpose completions and artificial lift to optimize recovery and lower unit operating costs. Rigorously manage schedules and capex to meet breakeven thresholds (often targeted near 30–50 USD/boe). Integrate HSE by design to reduce incidents and emissions during all phases.

Production operations and optimization

Run assets to >95% availability via vigilant maintenance and integrity programs; leading operators reported uptime targets at or above 95% in 2024. Use data-driven surveillance and predictive analytics to cut unplanned downtime roughly 20–35% and boost recovery. Optimize lift, waterfloods (typical incremental recovery 5–15%) and chemicals (10–20% potential uplift) to lower unit costs. Continuously debottleneck surface facilities to sustain throughput and reduce opex.

Portfolio management and disciplined M&A

Portfolio management and disciplined M&A focus on acquiring, divesting, and farming assets to raise returns and resilience, targeting >15% project IRR and redeploying cash from non-core to higher-margin barrels.

Maintain a mix of short-cycle cash generators and long-life inventory (reserve life index ~8–15 years) and embed NPV10, probabilistic valuation, and strict risk screens.

- Target IRR: >15%

- RLI: 8–15 years

- Use NPV10 & probabilistic risk

HSE, ESG compliance, and stakeholder engagement

Implement robust HSE systems and environmental management across upstream and downstream operations; in 2024, 85% of major oil producers publish TCFD- or ISSB-aligned disclosures to standardize reporting.

Continuously monitor CO2, methane, water use and biodiversity impacts; methane detection deployments rose about 40% in 2023–24, improving leak mitigation.

Engage communities and regulators to maintain trust and align operations with corporate net-zero targets and industry standards.

- HSE systems: mandatory audits, incident rates

- EMISSIONS: CO2, CH4, water, biodiversity metrics

- STAKEHOLDERS: community programs, regulator liaison

Execute 3D & appraisal wells; breakeven US$30–50/bbl, IRR > 15%

Identify and mature prospects (2024 exploration success: onshore 20–35%, offshore 10–15%), execute seismic (3D US$5–20M) and wells (appraisal US$30–120M; deepwater >US$100M) to feed development; run assets to >95% availability and target breakeven US$30–50/bbl; target IRR >15%, RLI 8–15y, embed NPV10 and probabilistic risk.

| Metric | 2024 |

|---|---|

| Expl. success | Onshore 20–35%, Offshore 10–15% |

| 3D cost | US$5–20M |

| Appraisal well | US$30–120M |

| Availability | >95% |

| Target IRR | >15% |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual International Petroleum Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact file—complete, professionally formatted, and ready to edit in Word and Excel. No hidden pages or altered content: what you see is what you’ll download and use for strategy, valuation, or presentations.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: Strategic Blueprint for an Integrated Petroleum Business

Unlock the strategic blueprint behind International Petroleum with our Business Model Canvas. This concise, sector-specific analysis maps value propositions, key partners, cost structure and revenue streams to show how the company competes and scales. Ideal for investors, advisors and entrepreneurs—download the full Word and Excel Canvas to implement these insights now.

Partnerships

Host governments and regulators (Canada, France, Malaysia)

Partnerships with national and provincial regulators—e.g., Alberta Energy Regulator, France's Ministry for the Ecological Transition, and Petronas—secure licenses, PSCs and compliance approvals, cutting permitting risk and delays. Constructive engagement stabilizes fiscal terms and operational continuity; global oil demand ~101 mb/d in 2024 underscores value of reliable access. Alignment on HSE and environmental standards sustains social license and project timelines.

Oilfield services and equipment providers

Drilling, completions, seismic and maintenance partners enable safe, efficient field operations; the global oilfield services market was about $430 billion in 2024 (Rystad Energy), underpinning scale. Strategic sourcing and long-term contracts commonly cut OPEX ~10% and boost service quality and uptime. Joint tech deployment can raise recovery factors by 5–10% and reduce downtime; local content rules (often 30%+ local supply) improve resilience and response.

Midstream, refiners, and trading offtakers

Pipeline, terminal and storage partners ensure takeaway and market access; Cushing held about 76 million barrels of capacity in 2024 and Permian-to-Gulf pipeline additions totaled roughly 3.5 million b/d by 2024. Refiners and traders supply liquidity, pricing options and destination flexibility; trading houses handled around a third of seaborne crude flows in 2024. Coordinated scheduling cuts bottlenecks and demurrage, while term contracts and lifting programs covering ~60–80% of volumes stabilize cash flow.

Technology, data, and ESG solution providers

Technology partners delivering digital subsurface tools, production-optimization software and emissions-monitoring systems raise uptime, recovery and cost-efficiency while satellite and aerial methane surveys show super-emitters account for roughly half of oil-and-gas methane losses, driving targeted mitigation.

- Digital tools: improve forecasting and integrity management (~20% accuracy gain)

- Methane detection: targets ~50% of emissions from few sites

- Electrification/water partners: cut operational footprint

- Co-development: accelerates innovation with measurable ROI

Banks, insurers, and capital market advisors

Banks, insurers and capital-market advisors enable hedging, bonding and risk transfer for international petroleum firms, with 2024 RCFs commonly sized $200–$2,000m and structured-finance making up roughly 20–30% of upstream project funding in 2024.

- Hedging/bonding: supports collateral and off-take guarantees

- Liquidity: RCFs and structured deals ($200–$2,000m typical)

- Insurance: mitigates operational and political risk (market capacity expanded in 2024)

- Advisors: optimize funding mix and investor communications

Oil market 2024: 101 mb/d demand, $430B services, storage & finance underpin growth

Regulators secure licenses and fiscal stability; world oil demand ~101 mb/d in 2024. Oilfield services market ~430 billion USD in 2024 enables scalable operations. Logistics/storage (Cushing ~76M bbl capacity) and trading support market access. Banks/insurers provide RCFs $200–2,000m and structured finance ~20–30% of upstream funding in 2024.

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Licenses/fiscal | 101 mb/d demand |

| OFS | Operations | $430B market |

| Logistics | Storage/flow | Cushing 76M bbl |

| Finance | Liquidity/hedge | RCF $200–2,000M |

| Tech | Optimization/emissions | super-emitters ~50% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for international petroleum companies covering customer segments, channels, value propositions, key activities, partners, cost and revenue structures, risks and competitive advantages, with SWOT-linked insights for investor presentations and strategic decisions.

High-level view of the international petroleum business model with editable cells, letting teams quickly map upstream-to-downstream value chains, risks and partners; saves hours of structuring and accelerates stakeholder alignment for strategic decisions.

Activities

Exploration and appraisal of prospects

Identify and assess resource potential across existing and adjacent acreage using basin-scale screening and data-driven prospect ranking; industry 2024 average exploration success rates ranged 20–35% onshore, 10–15% offshore. Execute seismic (3D surveys typically US$5–20M) and appraisal drilling (appraisal well US$30–120M) to mature inventories. De-risk prospects to feed the development pipeline and optimize scheduling against 2024 Brent ~US$86/bbl and capital allocation constraints.

Field development and drilling programs

Design and execute wells, facilities and tie-ins to unlock reserves, with onshore horizontal wells averaging about 6–8 million USD and deepwater wells commonly exceeding 100 million USD in 2024. Apply fit-for-purpose completions and artificial lift to optimize recovery and lower unit operating costs. Rigorously manage schedules and capex to meet breakeven thresholds (often targeted near 30–50 USD/boe). Integrate HSE by design to reduce incidents and emissions during all phases.

Production operations and optimization

Run assets to >95% availability via vigilant maintenance and integrity programs; leading operators reported uptime targets at or above 95% in 2024. Use data-driven surveillance and predictive analytics to cut unplanned downtime roughly 20–35% and boost recovery. Optimize lift, waterfloods (typical incremental recovery 5–15%) and chemicals (10–20% potential uplift) to lower unit costs. Continuously debottleneck surface facilities to sustain throughput and reduce opex.

Portfolio management and disciplined M&A

Portfolio management and disciplined M&A focus on acquiring, divesting, and farming assets to raise returns and resilience, targeting >15% project IRR and redeploying cash from non-core to higher-margin barrels.

Maintain a mix of short-cycle cash generators and long-life inventory (reserve life index ~8–15 years) and embed NPV10, probabilistic valuation, and strict risk screens.

- Target IRR: >15%

- RLI: 8–15 years

- Use NPV10 & probabilistic risk

HSE, ESG compliance, and stakeholder engagement

Implement robust HSE systems and environmental management across upstream and downstream operations; in 2024, 85% of major oil producers publish TCFD- or ISSB-aligned disclosures to standardize reporting.

Continuously monitor CO2, methane, water use and biodiversity impacts; methane detection deployments rose about 40% in 2023–24, improving leak mitigation.

Engage communities and regulators to maintain trust and align operations with corporate net-zero targets and industry standards.

- HSE systems: mandatory audits, incident rates

- EMISSIONS: CO2, CH4, water, biodiversity metrics

- STAKEHOLDERS: community programs, regulator liaison

Execute 3D & appraisal wells; breakeven US$30–50/bbl, IRR > 15%

Identify and mature prospects (2024 exploration success: onshore 20–35%, offshore 10–15%), execute seismic (3D US$5–20M) and wells (appraisal US$30–120M; deepwater >US$100M) to feed development; run assets to >95% availability and target breakeven US$30–50/bbl; target IRR >15%, RLI 8–15y, embed NPV10 and probabilistic risk.

| Metric | 2024 |

|---|---|

| Expl. success | Onshore 20–35%, Offshore 10–15% |

| 3D cost | US$5–20M |

| Appraisal well | US$30–120M |

| Availability | >95% |

| Target IRR | >15% |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual International Petroleum Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact file—complete, professionally formatted, and ready to edit in Word and Excel. No hidden pages or altered content: what you see is what you’ll download and use for strategy, valuation, or presentations.