International Petroleum PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and tech disruption are reshaping International Petroleum’s outlook in our concise PESTLE snapshot. This practical analysis highlights risks and opportunities for investors and strategists. Purchase the full PESTLE to get the detailed, ready-to-use insights you need now.

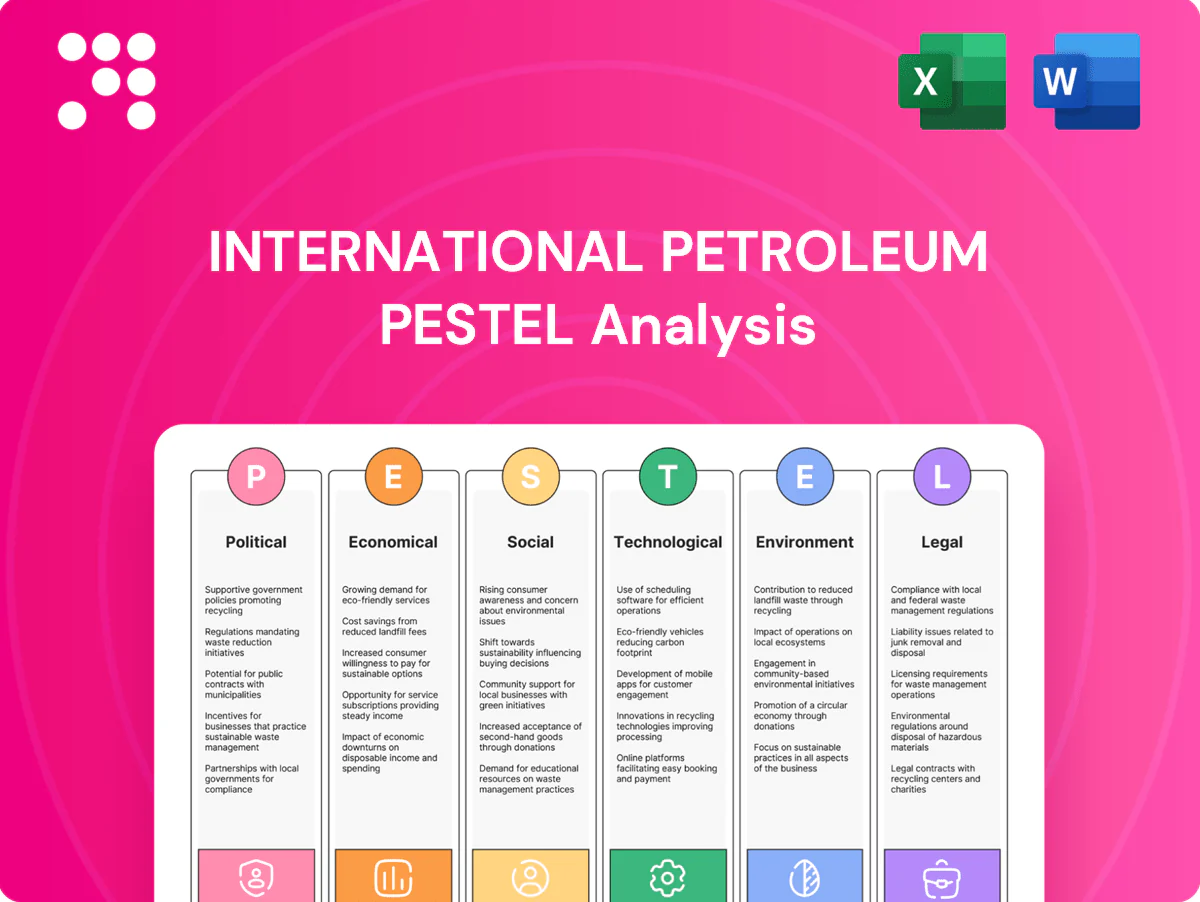

Political factors

Host-government policy stability

IPC operates under Canadian federal/provincial regimes where Canada produced ~4.6 mmb/d in 2023, France pursues aggressive energy transition with domestic hydrocarbon output near zero, and Malaysia (Petronas-led) produced ~0.6 mmb/d in 2023; shifts in hydrocarbons policy, licensing or local-content rules can change project timing and NPV, while stable ties with Ottawa, Paris and Kuala Lumpur and jurisdictional diversification reduce policy shock risk.

Carbon policy and emissions caps

Canada’s federal carbon price rose to CAD 70/t in 2024 with CAD 80/t planned for 2025, and proposed oil and gas emissions caps add direct compliance and operating cost pressures for producers. France’s strong decarbonization agenda and net‑zero 2050 commitment increase regulatory risk for mature assets and could accelerate decommissioning. Malaysia, having pledged net‑zero by 2050, is rolling out a carbon framework and exploring offsets markets that will reshape project economics. Proactive emissions planning preserves portfolio optionality and reduces stranded‑asset risk.

Geopolitical and trade dynamics

Global tensions drive oil price volatility—Brent averaged about $86/bbl in 2024—while supply-chain disruptions raise lead times for drilling and EPC equipment. Sanctions and trade barriers have repeatedly disrupted procurement and services, increasing project risk and contingency costs. Malacca and nearby sea lanes, handling roughly 25% of global traded goods, are critical for Malaysian offshore logistics and maritime security. IPC’s exposure to OECD markets and stable ASEAN growth (≈4.9% in 2024) reduces extreme geopolitical risk but not market shocks.

Indigenous and local stakeholder relations

Canadian petroleum projects must align with Indigenous rights and negotiated benefit agreements, with Indigenous peoples comprising about 5% of Canada’s population (Statistics Canada, 2021) and legal duties to consult established by Canadian courts and federal policy.

Strong, early engagement lowers permitting delays and social risk; local political support depends on jobs and environmental stewardship, while consistent community investment builds the social licence to operate.

- Regulatory: duty to consult and benefit agreements

- Risk: engagement reduces permitting delays

- Local buy-in: jobs + environmental stewardship

- Continuity: sustained community investment

Fiscal regime competitiveness

Fiscal regime competitiveness drives netbacks: Alberta and Saskatchewan royalty/tax adjustments in 2023–24 shifted producer netbacks by several percentage points, France’s levies and special taxes raise operating costs for onshore/offshore fields, and Malaysia’s PSC terms and bonus structures materially affect government take and investor returns. Stable, predictable terms support long-cycle planning and M&A, so IPC must press via industry bodies to keep regimes investment‑friendly.

- Alberta/Saskatchewan: royalty/tax tweaks → netback impact (mid-single-digit % range)

- France: elevated levies increase OPEX and reduce post‑tax cashflow

- Malaysia: PSC terms determine government take and project IRR

- Action: IPC advocacy via industry bodies to preserve competitiveness

Canada CAD 70→80/t; FR levies; Malaysia ~0.6 mmb/d

Canada: federal carbon price CAD 70/t in 2024, CAD 80/t planned 2025; Indigenous duty to consult raises permit timelines. France: net‑zero 2050, near‑zero domestic hydrocarbon output and high levies increase decommissioning and tax risk. Malaysia: Petronas‑led production ~0.6 mmb/d (2023) with net‑zero 2050 pledge and evolving carbon framework affecting PSC economics.

| Country | 2023 prod (mmb/d) | Key policy | Carbon price / levy |

|---|---|---|---|

| Canada | ≈4.6 | Duty to consult; emissions caps | CAD 70/t (2024), CAD 80/t (2025) |

| France | ≈0.0 | Net‑zero 2050; high levies | Elevated sector taxes |

| Malaysia | ≈0.6 | PSC reforms; carbon framework | Under development |

What is included in the product

Explores how macro-environmental forces uniquely impact International Petroleum across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities. Designed for executives and investors, it delivers actionable, forward-looking insights and ready-to-use content for strategy, funding, and scenario planning.

Condenses international petroleum PESTLE insights into a compact, visually segmented brief for quick reference in meetings, enabling teams to align on geopolitical, regulatory and market risks and add context-specific notes.

Economic factors

Oil and gas price cycles

Brent (~85 USD/bbl in June 2025) and WTI (~81 USD/bbl) plus regional gas benchmarks (Henry Hub ~3.0 USD/MMBtu; TTF ~25 EUR/MWh) drive cash flow and capital allocation, with downturns compressing margins and forcing conservative reserve bookings. Upcycles boost M&A and growth opportunities, while hedging stabilizes returns at the cost of capped upside. Portfolio flexibility lets firms reallocate spend to highest-return assets across geographies.

FX and inflation impacts

CAD, EUR and MYR swings of roughly 3–8% versus USD in 2024–H1 2025 materially affected reported USD results and local-currency cost bases, amplifying P&L volatility. Services and steel input costs rose about 8–12% in 2024, lifting capex/opex and squeezing breakevens. Local revenues in CAD/EUR/MYR with USD-linked inputs create cash‑flow mismatches. Strong cost discipline and strategic procurement hedge much of this volatility.

Differentials and market access

Canadian heavy/light differentials (WCS vs WTI) have historically widened to as much as US$40/bbl during takeaway constraints, while typical averages have trended lower when pipeline capacity is available. Canada's export pipeline network, including Trans Mountain expansion adding about 590 kb/d to roughly 4.8–4.9 mb/d total capacity, directly influences realized pricing. French and Malaysian seaborne sales benefit from Brent-linked benchmarks, improving netbacks versus inland indices. Diversified marketing, blending and strategic storage capacity compresses discounts and optimizes netbacks.

Capital availability and cost

- Financing cost: US fed funds 5.25–5.50% (mid‑2025)

- ESG impact: reduced capital access for hydrocarbons

- Cash returns: industry buybacks/dividends >50bn USD (2024)

- M&A: adds value if leverage remains conservative

Demand trajectory and energy mix

Medium-term oil demand remains resilient at about 101.7 mb/d in 2024 (IEA) while long-term outcomes hinge on EV adoption and policy pathways; stronger EV penetration could materially lower transport oil demand by 2030. Gas can provide transitional growth where prices, LNG supply and pipelines permit, and Asia—especially Southeast Asia—drives regional demand growth benefiting Malaysian exposure. Strategy: balance decline management with selective growth.

- IEA 2024 oil demand ~101.7 mb/d

- Asia/Southeast Asia major demand growth, supporting Malaysia

- Gas as transitional fuel where infrastructure and prices align

- Strategy: manage decline, target selective growth

Canada CAD 70→80/t; FR levies; Malaysia ~0.6 mmb/d

Commodity prices (Brent ~85 USD/bbl; WTI ~81 USD/bbl; Henry Hub ~3 USD/MMBtu; TTF ~25 EUR/MWh) drive cash flow and hedging caps upside. FX swings (3–8% 2024–H1 2025) and +8–12% service/steel inflation raised capex/opex. Rates ~5.25–5.50% mid‑2025 and ESG constraints lift financing costs. IEA 2024 demand ~101.7 mb/d supports selective Asia growth.

| Metric | Value |

|---|---|

| Brent (Jun 2025) | ~85 USD/bbl |

| WTI (Jun 2025) | ~81 USD/bbl |

| Henry Hub | ~3 USD/MMBtu |

| TTF | ~25 EUR/MWh |

| Fed funds (mid‑2025) | 5.25–5.50% |

| IEA 2024 demand | ~101.7 mb/d |

| Buybacks/Dividends 2024 | >50 bn USD |

Full Version Awaits

International Petroleum PESTLE Analysis

The preview shown here is the exact International Petroleum PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and insights are final with no placeholders. After checkout you’ll download this same professional file immediately.

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and tech disruption are reshaping International Petroleum’s outlook in our concise PESTLE snapshot. This practical analysis highlights risks and opportunities for investors and strategists. Purchase the full PESTLE to get the detailed, ready-to-use insights you need now.

Political factors

Host-government policy stability

IPC operates under Canadian federal/provincial regimes where Canada produced ~4.6 mmb/d in 2023, France pursues aggressive energy transition with domestic hydrocarbon output near zero, and Malaysia (Petronas-led) produced ~0.6 mmb/d in 2023; shifts in hydrocarbons policy, licensing or local-content rules can change project timing and NPV, while stable ties with Ottawa, Paris and Kuala Lumpur and jurisdictional diversification reduce policy shock risk.

Carbon policy and emissions caps

Canada’s federal carbon price rose to CAD 70/t in 2024 with CAD 80/t planned for 2025, and proposed oil and gas emissions caps add direct compliance and operating cost pressures for producers. France’s strong decarbonization agenda and net‑zero 2050 commitment increase regulatory risk for mature assets and could accelerate decommissioning. Malaysia, having pledged net‑zero by 2050, is rolling out a carbon framework and exploring offsets markets that will reshape project economics. Proactive emissions planning preserves portfolio optionality and reduces stranded‑asset risk.

Geopolitical and trade dynamics

Global tensions drive oil price volatility—Brent averaged about $86/bbl in 2024—while supply-chain disruptions raise lead times for drilling and EPC equipment. Sanctions and trade barriers have repeatedly disrupted procurement and services, increasing project risk and contingency costs. Malacca and nearby sea lanes, handling roughly 25% of global traded goods, are critical for Malaysian offshore logistics and maritime security. IPC’s exposure to OECD markets and stable ASEAN growth (≈4.9% in 2024) reduces extreme geopolitical risk but not market shocks.

Indigenous and local stakeholder relations

Canadian petroleum projects must align with Indigenous rights and negotiated benefit agreements, with Indigenous peoples comprising about 5% of Canada’s population (Statistics Canada, 2021) and legal duties to consult established by Canadian courts and federal policy.

Strong, early engagement lowers permitting delays and social risk; local political support depends on jobs and environmental stewardship, while consistent community investment builds the social licence to operate.

- Regulatory: duty to consult and benefit agreements

- Risk: engagement reduces permitting delays

- Local buy-in: jobs + environmental stewardship

- Continuity: sustained community investment

Fiscal regime competitiveness

Fiscal regime competitiveness drives netbacks: Alberta and Saskatchewan royalty/tax adjustments in 2023–24 shifted producer netbacks by several percentage points, France’s levies and special taxes raise operating costs for onshore/offshore fields, and Malaysia’s PSC terms and bonus structures materially affect government take and investor returns. Stable, predictable terms support long-cycle planning and M&A, so IPC must press via industry bodies to keep regimes investment‑friendly.

- Alberta/Saskatchewan: royalty/tax tweaks → netback impact (mid-single-digit % range)

- France: elevated levies increase OPEX and reduce post‑tax cashflow

- Malaysia: PSC terms determine government take and project IRR

- Action: IPC advocacy via industry bodies to preserve competitiveness

Canada CAD 70→80/t; FR levies; Malaysia ~0.6 mmb/d

Canada: federal carbon price CAD 70/t in 2024, CAD 80/t planned 2025; Indigenous duty to consult raises permit timelines. France: net‑zero 2050, near‑zero domestic hydrocarbon output and high levies increase decommissioning and tax risk. Malaysia: Petronas‑led production ~0.6 mmb/d (2023) with net‑zero 2050 pledge and evolving carbon framework affecting PSC economics.

| Country | 2023 prod (mmb/d) | Key policy | Carbon price / levy |

|---|---|---|---|

| Canada | ≈4.6 | Duty to consult; emissions caps | CAD 70/t (2024), CAD 80/t (2025) |

| France | ≈0.0 | Net‑zero 2050; high levies | Elevated sector taxes |

| Malaysia | ≈0.6 | PSC reforms; carbon framework | Under development |

What is included in the product

Explores how macro-environmental forces uniquely impact International Petroleum across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities. Designed for executives and investors, it delivers actionable, forward-looking insights and ready-to-use content for strategy, funding, and scenario planning.

Condenses international petroleum PESTLE insights into a compact, visually segmented brief for quick reference in meetings, enabling teams to align on geopolitical, regulatory and market risks and add context-specific notes.

Economic factors

Oil and gas price cycles

Brent (~85 USD/bbl in June 2025) and WTI (~81 USD/bbl) plus regional gas benchmarks (Henry Hub ~3.0 USD/MMBtu; TTF ~25 EUR/MWh) drive cash flow and capital allocation, with downturns compressing margins and forcing conservative reserve bookings. Upcycles boost M&A and growth opportunities, while hedging stabilizes returns at the cost of capped upside. Portfolio flexibility lets firms reallocate spend to highest-return assets across geographies.

FX and inflation impacts

CAD, EUR and MYR swings of roughly 3–8% versus USD in 2024–H1 2025 materially affected reported USD results and local-currency cost bases, amplifying P&L volatility. Services and steel input costs rose about 8–12% in 2024, lifting capex/opex and squeezing breakevens. Local revenues in CAD/EUR/MYR with USD-linked inputs create cash‑flow mismatches. Strong cost discipline and strategic procurement hedge much of this volatility.

Differentials and market access

Canadian heavy/light differentials (WCS vs WTI) have historically widened to as much as US$40/bbl during takeaway constraints, while typical averages have trended lower when pipeline capacity is available. Canada's export pipeline network, including Trans Mountain expansion adding about 590 kb/d to roughly 4.8–4.9 mb/d total capacity, directly influences realized pricing. French and Malaysian seaborne sales benefit from Brent-linked benchmarks, improving netbacks versus inland indices. Diversified marketing, blending and strategic storage capacity compresses discounts and optimizes netbacks.

Capital availability and cost

- Financing cost: US fed funds 5.25–5.50% (mid‑2025)

- ESG impact: reduced capital access for hydrocarbons

- Cash returns: industry buybacks/dividends >50bn USD (2024)

- M&A: adds value if leverage remains conservative

Demand trajectory and energy mix

Medium-term oil demand remains resilient at about 101.7 mb/d in 2024 (IEA) while long-term outcomes hinge on EV adoption and policy pathways; stronger EV penetration could materially lower transport oil demand by 2030. Gas can provide transitional growth where prices, LNG supply and pipelines permit, and Asia—especially Southeast Asia—drives regional demand growth benefiting Malaysian exposure. Strategy: balance decline management with selective growth.

- IEA 2024 oil demand ~101.7 mb/d

- Asia/Southeast Asia major demand growth, supporting Malaysia

- Gas as transitional fuel where infrastructure and prices align

- Strategy: manage decline, target selective growth

Canada CAD 70→80/t; FR levies; Malaysia ~0.6 mmb/d

Commodity prices (Brent ~85 USD/bbl; WTI ~81 USD/bbl; Henry Hub ~3 USD/MMBtu; TTF ~25 EUR/MWh) drive cash flow and hedging caps upside. FX swings (3–8% 2024–H1 2025) and +8–12% service/steel inflation raised capex/opex. Rates ~5.25–5.50% mid‑2025 and ESG constraints lift financing costs. IEA 2024 demand ~101.7 mb/d supports selective Asia growth.

| Metric | Value |

|---|---|

| Brent (Jun 2025) | ~85 USD/bbl |

| WTI (Jun 2025) | ~81 USD/bbl |

| Henry Hub | ~3 USD/MMBtu |

| TTF | ~25 EUR/MWh |

| Fed funds (mid‑2025) | 5.25–5.50% |

| IEA 2024 demand | ~101.7 mb/d |

| Buybacks/Dividends 2024 | >50 bn USD |

Full Version Awaits

International Petroleum PESTLE Analysis

The preview shown here is the exact International Petroleum PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and insights are final with no placeholders. After checkout you’ll download this same professional file immediately.

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and tech disruption are reshaping International Petroleum’s outlook in our concise PESTLE snapshot. This practical analysis highlights risks and opportunities for investors and strategists. Purchase the full PESTLE to get the detailed, ready-to-use insights you need now.

Political factors

Host-government policy stability

IPC operates under Canadian federal/provincial regimes where Canada produced ~4.6 mmb/d in 2023, France pursues aggressive energy transition with domestic hydrocarbon output near zero, and Malaysia (Petronas-led) produced ~0.6 mmb/d in 2023; shifts in hydrocarbons policy, licensing or local-content rules can change project timing and NPV, while stable ties with Ottawa, Paris and Kuala Lumpur and jurisdictional diversification reduce policy shock risk.

Carbon policy and emissions caps

Canada’s federal carbon price rose to CAD 70/t in 2024 with CAD 80/t planned for 2025, and proposed oil and gas emissions caps add direct compliance and operating cost pressures for producers. France’s strong decarbonization agenda and net‑zero 2050 commitment increase regulatory risk for mature assets and could accelerate decommissioning. Malaysia, having pledged net‑zero by 2050, is rolling out a carbon framework and exploring offsets markets that will reshape project economics. Proactive emissions planning preserves portfolio optionality and reduces stranded‑asset risk.

Geopolitical and trade dynamics

Global tensions drive oil price volatility—Brent averaged about $86/bbl in 2024—while supply-chain disruptions raise lead times for drilling and EPC equipment. Sanctions and trade barriers have repeatedly disrupted procurement and services, increasing project risk and contingency costs. Malacca and nearby sea lanes, handling roughly 25% of global traded goods, are critical for Malaysian offshore logistics and maritime security. IPC’s exposure to OECD markets and stable ASEAN growth (≈4.9% in 2024) reduces extreme geopolitical risk but not market shocks.

Indigenous and local stakeholder relations

Canadian petroleum projects must align with Indigenous rights and negotiated benefit agreements, with Indigenous peoples comprising about 5% of Canada’s population (Statistics Canada, 2021) and legal duties to consult established by Canadian courts and federal policy.

Strong, early engagement lowers permitting delays and social risk; local political support depends on jobs and environmental stewardship, while consistent community investment builds the social licence to operate.

- Regulatory: duty to consult and benefit agreements

- Risk: engagement reduces permitting delays

- Local buy-in: jobs + environmental stewardship

- Continuity: sustained community investment

Fiscal regime competitiveness

Fiscal regime competitiveness drives netbacks: Alberta and Saskatchewan royalty/tax adjustments in 2023–24 shifted producer netbacks by several percentage points, France’s levies and special taxes raise operating costs for onshore/offshore fields, and Malaysia’s PSC terms and bonus structures materially affect government take and investor returns. Stable, predictable terms support long-cycle planning and M&A, so IPC must press via industry bodies to keep regimes investment‑friendly.

- Alberta/Saskatchewan: royalty/tax tweaks → netback impact (mid-single-digit % range)

- France: elevated levies increase OPEX and reduce post‑tax cashflow

- Malaysia: PSC terms determine government take and project IRR

- Action: IPC advocacy via industry bodies to preserve competitiveness

Canada CAD 70→80/t; FR levies; Malaysia ~0.6 mmb/d

Canada: federal carbon price CAD 70/t in 2024, CAD 80/t planned 2025; Indigenous duty to consult raises permit timelines. France: net‑zero 2050, near‑zero domestic hydrocarbon output and high levies increase decommissioning and tax risk. Malaysia: Petronas‑led production ~0.6 mmb/d (2023) with net‑zero 2050 pledge and evolving carbon framework affecting PSC economics.

| Country | 2023 prod (mmb/d) | Key policy | Carbon price / levy |

|---|---|---|---|

| Canada | ≈4.6 | Duty to consult; emissions caps | CAD 70/t (2024), CAD 80/t (2025) |

| France | ≈0.0 | Net‑zero 2050; high levies | Elevated sector taxes |

| Malaysia | ≈0.6 | PSC reforms; carbon framework | Under development |

What is included in the product

Explores how macro-environmental forces uniquely impact International Petroleum across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify risks and opportunities. Designed for executives and investors, it delivers actionable, forward-looking insights and ready-to-use content for strategy, funding, and scenario planning.

Condenses international petroleum PESTLE insights into a compact, visually segmented brief for quick reference in meetings, enabling teams to align on geopolitical, regulatory and market risks and add context-specific notes.

Economic factors

Oil and gas price cycles

Brent (~85 USD/bbl in June 2025) and WTI (~81 USD/bbl) plus regional gas benchmarks (Henry Hub ~3.0 USD/MMBtu; TTF ~25 EUR/MWh) drive cash flow and capital allocation, with downturns compressing margins and forcing conservative reserve bookings. Upcycles boost M&A and growth opportunities, while hedging stabilizes returns at the cost of capped upside. Portfolio flexibility lets firms reallocate spend to highest-return assets across geographies.

FX and inflation impacts

CAD, EUR and MYR swings of roughly 3–8% versus USD in 2024–H1 2025 materially affected reported USD results and local-currency cost bases, amplifying P&L volatility. Services and steel input costs rose about 8–12% in 2024, lifting capex/opex and squeezing breakevens. Local revenues in CAD/EUR/MYR with USD-linked inputs create cash‑flow mismatches. Strong cost discipline and strategic procurement hedge much of this volatility.

Differentials and market access

Canadian heavy/light differentials (WCS vs WTI) have historically widened to as much as US$40/bbl during takeaway constraints, while typical averages have trended lower when pipeline capacity is available. Canada's export pipeline network, including Trans Mountain expansion adding about 590 kb/d to roughly 4.8–4.9 mb/d total capacity, directly influences realized pricing. French and Malaysian seaborne sales benefit from Brent-linked benchmarks, improving netbacks versus inland indices. Diversified marketing, blending and strategic storage capacity compresses discounts and optimizes netbacks.

Capital availability and cost

- Financing cost: US fed funds 5.25–5.50% (mid‑2025)

- ESG impact: reduced capital access for hydrocarbons

- Cash returns: industry buybacks/dividends >50bn USD (2024)

- M&A: adds value if leverage remains conservative

Demand trajectory and energy mix

Medium-term oil demand remains resilient at about 101.7 mb/d in 2024 (IEA) while long-term outcomes hinge on EV adoption and policy pathways; stronger EV penetration could materially lower transport oil demand by 2030. Gas can provide transitional growth where prices, LNG supply and pipelines permit, and Asia—especially Southeast Asia—drives regional demand growth benefiting Malaysian exposure. Strategy: balance decline management with selective growth.

- IEA 2024 oil demand ~101.7 mb/d

- Asia/Southeast Asia major demand growth, supporting Malaysia

- Gas as transitional fuel where infrastructure and prices align

- Strategy: manage decline, target selective growth

Canada CAD 70→80/t; FR levies; Malaysia ~0.6 mmb/d

Commodity prices (Brent ~85 USD/bbl; WTI ~81 USD/bbl; Henry Hub ~3 USD/MMBtu; TTF ~25 EUR/MWh) drive cash flow and hedging caps upside. FX swings (3–8% 2024–H1 2025) and +8–12% service/steel inflation raised capex/opex. Rates ~5.25–5.50% mid‑2025 and ESG constraints lift financing costs. IEA 2024 demand ~101.7 mb/d supports selective Asia growth.

| Metric | Value |

|---|---|

| Brent (Jun 2025) | ~85 USD/bbl |

| WTI (Jun 2025) | ~81 USD/bbl |

| Henry Hub | ~3 USD/MMBtu |

| TTF | ~25 EUR/MWh |

| Fed funds (mid‑2025) | 5.25–5.50% |

| IEA 2024 demand | ~101.7 mb/d |

| Buybacks/Dividends 2024 | >50 bn USD |

Full Version Awaits

International Petroleum PESTLE Analysis

The preview shown here is the exact International Petroleum PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and insights are final with no placeholders. After checkout you’ll download this same professional file immediately.