Intesa Sanpaolo Assicura Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Intesa Sanpaolo Assicura faces moderate buyer power, high regulatory scrutiny, and fierce rivalry tempered by strong bancassurance distribution and brand advantages; supplier leverage and digital insurtech substitutes present emerging risks. This snapshot highlights strategic pressures and opportunity areas. Unlock the full Porter's Five Forces Analysis to explore Intesa Sanpaolo Assicura’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on bank distribution

Intesa Sanpaolo’s reliance on its c.3,300-branch network concentrates distribution power inside the group, making branch priorities a de facto supplier with material influence on premium growth. Any shift in bank incentives or cross-sell focus can move significant volumes—bank channels account for roughly 80% of Assicura’s premiums—so opportunity cost within branches can reduce shelf space. Strong intra-group governance lowers conflict but does not eliminate medium supplier leverage.

Reinsurers and capital providers

Reinsurers supply risk capacity and shape terms, ceding commissions and underwriting appetite; in 2023–24 peak-cat and volatile lines saw reinsurance pricing increases of roughly 30–60%, boosting reinsurers’ bargaining power and compressing primary margins. Strong credit quality and diversified books enable Intesa Sanpaolo Assicura to secure firmer treaty terms and lower cession rates. Nonetheless, dependence on external reinsurance capacity remains a structural supplier power.

Data, IT platforms, and analytics vendors

Pricing, fraud detection and claims automation for Intesa Sanpaolo Assicura depend on specialized data and analytics vendors, giving them leverage as switching costs and integration complexity are high. Top 3 cloud vendors held roughly 64% of the global cloud market in 2023–24, concentrating supplier power for core infrastructure. Modular cloud stacks and APIs can reduce lock-in over time, but critical systems in the near term sustain supplier negotiating power.

Repair, medical, and service networks

Repair, medical and service networks are essential for non-life and health claims, and local concentration in some Italian regions raises suppliers’ leverage on tariffs and service terms, forcing insurers to negotiate access and pricing. Volume steering and preferred-provider networks help Intesa Sanpaolo Assicura rebalance unit economics, though service-cost inflation can still transmit into loss ratios.

- Regional concentration elevates tariff leverage

- Preferred networks enable cost steering

- Service inflation feeds loss ratios

Actuarial and technical talent

- Specialist scarcity: elevates bargaining power

- Mitigation: internal training, group mobility

- Cost impact: higher retention spend

- Operational risk: delayed launches/innovation

Supplier power: banks ~80%, reinsurers +30-60%

Supplier power is moderate-high: bank channels (c.80% of premiums) and c.3,300 branches give the group internal distribution leverage but create internal supplier risk. Reinsurer pricing rose ~30–60% in 2023–24, increasing external bargaining power and margin pressure. Cloud and analytics vendors (top3 ~64% market share) and scarce actuarial talent (group ~95,000 employees in 2024) sustain switching costs and retention expense.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Bank channels | % premiums | ~80% |

| Branches | count | ~3,300 |

| Reinsurance | pricing change | +30–60% |

| Cloud vendors | top3 market share | ~64% |

| Employees | group headcount | ~95,000 (2024) |

What is included in the product

Tailored Porter’s Five Forces analysis for Intesa Sanpaolo Assicura that uncovers competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and regulatory risks shaping pricing, market share, and profitability.

A clear, one-sheet summary of all five forces for Intesa Sanpaolo Assicura—perfect for quick decision-making and pinpointing competitive pain points. Swap in your own data and duplicate tabs for regulatory or market scenarios to relieve analysis bottlenecks.

Customers Bargaining Power

Retail customers via bancassurance

Branch-originated retail customers of Intesa Sanpaolo Assicura benefit from convenience and product bundling via a bancassurance network of over 3,000 branches, which reduces price sensitivity and shopping behavior. Cross-selling with banking products drives stickiness and keeps churn in the low single digits, further lowering buyer leverage. IDD-driven transparency and IVASS oversight in 2024 raise value expectations, tempering but not overturning bargaining power, which remains moderate-to-low.

SMEs and corporate clients

Larger SME and corporate buyers—in a market where SMEs account for over 99% of EU firms and about 67% of employment in 2024—increasingly solicit multiple quotes and push hard on terms. Their demand for risk engineering and bespoke coverage raises bargaining leverage, while Intesa Sanpaolo Assicura’s bancassurance ties aid retention but cannot prevent price-sensitive defections. Resulting frequent discounts and endorsement requests compress margins and shift underwriting risk.

Price comparison and digital channels

Aggregators and online reviews have tightened information symmetry, with 2024 industry reports showing comparison sites influence over 60% of online insurance purchase decisions in Italy. Commoditized lines such as motor see elevated buyer power as price becomes easily comparable across providers. Intuitive digital onboarding and UX can raise conversion rates and foster loyalty, partially offsetting price pressure. Still, headline premium remains the primary decision driver for most online shoppers.

Switching costs and product complexity

Life and multi-year policies for Intesa Sanpaolo Assicura create customer inertia and perceived switching costs, reinforced by bancassurance channels that account for about 50% of Italian life premiums in 2023-24; bank staff advice further anchors choices and reduces churn. Claims experience and service quality remain decisive at renewal, with poor service able to reverse low switching despite product complexity.

- Inertia: long-term policies

- Advisor anchoring: bancassurance ~50% (2023-24)

- Service-driven churn: claims quality critical

- Complexity lowers buyer power but is fragile

Sensitivity to macro and rates

Customers of Intesa Sanpaolo Assicura are sensitive to inflation, income pressure and interest-rate moves; Italian inflation eased to about 2.6% in 2024 while the ECB deposit rate averaged near 4.0%, making attractive deposit yields a stronger competitor to life savings. In tight times buyers press for lower premiums or stronger guarantees, and episodic macro shocks raise buyer leverage, reducing pricing power.

- Inflation: 2.6% (2024)

- ECB deposit rate: ~4.0% (2024)

- Effect: higher deposit pull vs life products

Branch 3,000+, aggregators > 60% shape online sales

Branch retail via 3,000+ branches and cross-selling reduces price sensitivity and keeps churn in low single digits. SME/corporate buyers push on price for bespoke cover, raising bargaining leverage. Aggregators influence >60% of online purchases, boosting price comparability. Life bancassurance ~50% (2023-24); inflation 2.6% and ECB rate ~4.0% increase deposit competition.

| Metric | 2024 Value |

|---|---|

| Branches | >3,000 |

| Online comparison influence | >60% |

| Bancassurance life share | ~50% (2023-24) |

| Inflation | 2.6% |

| ECB deposit rate | ~4.0% |

Preview the Actual Deliverable

Intesa Sanpaolo Assicura Porter's Five Forces Analysis

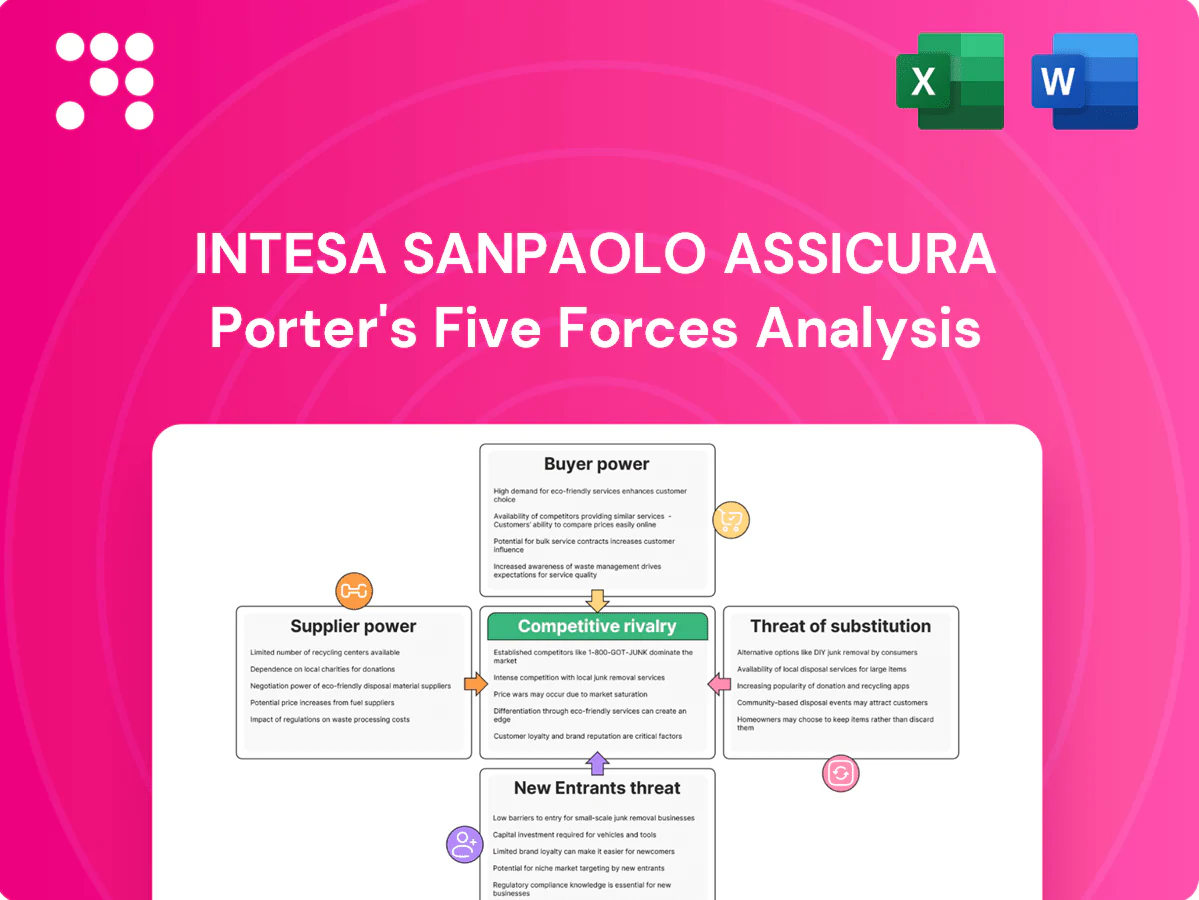

This preview displays the exact Porter’s Five Forces analysis for Intesa Sanpaolo Assicura you’ll receive—fully formatted and ready to use. The assessment covers competitive rivalry, supplier and buyer power, threats of entry and substitution with actionable insights. No placeholders or samples; purchase grants immediate download of this same file. Use it as-is for strategy, valuation, or reporting.

Go Beyond the Preview—Access the Full Strategic Report

Intesa Sanpaolo Assicura faces moderate buyer power, high regulatory scrutiny, and fierce rivalry tempered by strong bancassurance distribution and brand advantages; supplier leverage and digital insurtech substitutes present emerging risks. This snapshot highlights strategic pressures and opportunity areas. Unlock the full Porter's Five Forces Analysis to explore Intesa Sanpaolo Assicura’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on bank distribution

Intesa Sanpaolo’s reliance on its c.3,300-branch network concentrates distribution power inside the group, making branch priorities a de facto supplier with material influence on premium growth. Any shift in bank incentives or cross-sell focus can move significant volumes—bank channels account for roughly 80% of Assicura’s premiums—so opportunity cost within branches can reduce shelf space. Strong intra-group governance lowers conflict but does not eliminate medium supplier leverage.

Reinsurers and capital providers

Reinsurers supply risk capacity and shape terms, ceding commissions and underwriting appetite; in 2023–24 peak-cat and volatile lines saw reinsurance pricing increases of roughly 30–60%, boosting reinsurers’ bargaining power and compressing primary margins. Strong credit quality and diversified books enable Intesa Sanpaolo Assicura to secure firmer treaty terms and lower cession rates. Nonetheless, dependence on external reinsurance capacity remains a structural supplier power.

Data, IT platforms, and analytics vendors

Pricing, fraud detection and claims automation for Intesa Sanpaolo Assicura depend on specialized data and analytics vendors, giving them leverage as switching costs and integration complexity are high. Top 3 cloud vendors held roughly 64% of the global cloud market in 2023–24, concentrating supplier power for core infrastructure. Modular cloud stacks and APIs can reduce lock-in over time, but critical systems in the near term sustain supplier negotiating power.

Repair, medical, and service networks

Repair, medical and service networks are essential for non-life and health claims, and local concentration in some Italian regions raises suppliers’ leverage on tariffs and service terms, forcing insurers to negotiate access and pricing. Volume steering and preferred-provider networks help Intesa Sanpaolo Assicura rebalance unit economics, though service-cost inflation can still transmit into loss ratios.

- Regional concentration elevates tariff leverage

- Preferred networks enable cost steering

- Service inflation feeds loss ratios

Actuarial and technical talent

- Specialist scarcity: elevates bargaining power

- Mitigation: internal training, group mobility

- Cost impact: higher retention spend

- Operational risk: delayed launches/innovation

Supplier power: banks ~80%, reinsurers +30-60%

Supplier power is moderate-high: bank channels (c.80% of premiums) and c.3,300 branches give the group internal distribution leverage but create internal supplier risk. Reinsurer pricing rose ~30–60% in 2023–24, increasing external bargaining power and margin pressure. Cloud and analytics vendors (top3 ~64% market share) and scarce actuarial talent (group ~95,000 employees in 2024) sustain switching costs and retention expense.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Bank channels | % premiums | ~80% |

| Branches | count | ~3,300 |

| Reinsurance | pricing change | +30–60% |

| Cloud vendors | top3 market share | ~64% |

| Employees | group headcount | ~95,000 (2024) |

What is included in the product

Tailored Porter’s Five Forces analysis for Intesa Sanpaolo Assicura that uncovers competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and regulatory risks shaping pricing, market share, and profitability.

A clear, one-sheet summary of all five forces for Intesa Sanpaolo Assicura—perfect for quick decision-making and pinpointing competitive pain points. Swap in your own data and duplicate tabs for regulatory or market scenarios to relieve analysis bottlenecks.

Customers Bargaining Power

Retail customers via bancassurance

Branch-originated retail customers of Intesa Sanpaolo Assicura benefit from convenience and product bundling via a bancassurance network of over 3,000 branches, which reduces price sensitivity and shopping behavior. Cross-selling with banking products drives stickiness and keeps churn in the low single digits, further lowering buyer leverage. IDD-driven transparency and IVASS oversight in 2024 raise value expectations, tempering but not overturning bargaining power, which remains moderate-to-low.

SMEs and corporate clients

Larger SME and corporate buyers—in a market where SMEs account for over 99% of EU firms and about 67% of employment in 2024—increasingly solicit multiple quotes and push hard on terms. Their demand for risk engineering and bespoke coverage raises bargaining leverage, while Intesa Sanpaolo Assicura’s bancassurance ties aid retention but cannot prevent price-sensitive defections. Resulting frequent discounts and endorsement requests compress margins and shift underwriting risk.

Price comparison and digital channels

Aggregators and online reviews have tightened information symmetry, with 2024 industry reports showing comparison sites influence over 60% of online insurance purchase decisions in Italy. Commoditized lines such as motor see elevated buyer power as price becomes easily comparable across providers. Intuitive digital onboarding and UX can raise conversion rates and foster loyalty, partially offsetting price pressure. Still, headline premium remains the primary decision driver for most online shoppers.

Switching costs and product complexity

Life and multi-year policies for Intesa Sanpaolo Assicura create customer inertia and perceived switching costs, reinforced by bancassurance channels that account for about 50% of Italian life premiums in 2023-24; bank staff advice further anchors choices and reduces churn. Claims experience and service quality remain decisive at renewal, with poor service able to reverse low switching despite product complexity.

- Inertia: long-term policies

- Advisor anchoring: bancassurance ~50% (2023-24)

- Service-driven churn: claims quality critical

- Complexity lowers buyer power but is fragile

Sensitivity to macro and rates

Customers of Intesa Sanpaolo Assicura are sensitive to inflation, income pressure and interest-rate moves; Italian inflation eased to about 2.6% in 2024 while the ECB deposit rate averaged near 4.0%, making attractive deposit yields a stronger competitor to life savings. In tight times buyers press for lower premiums or stronger guarantees, and episodic macro shocks raise buyer leverage, reducing pricing power.

- Inflation: 2.6% (2024)

- ECB deposit rate: ~4.0% (2024)

- Effect: higher deposit pull vs life products

Branch 3,000+, aggregators > 60% shape online sales

Branch retail via 3,000+ branches and cross-selling reduces price sensitivity and keeps churn in low single digits. SME/corporate buyers push on price for bespoke cover, raising bargaining leverage. Aggregators influence >60% of online purchases, boosting price comparability. Life bancassurance ~50% (2023-24); inflation 2.6% and ECB rate ~4.0% increase deposit competition.

| Metric | 2024 Value |

|---|---|

| Branches | >3,000 |

| Online comparison influence | >60% |

| Bancassurance life share | ~50% (2023-24) |

| Inflation | 2.6% |

| ECB deposit rate | ~4.0% |

Preview the Actual Deliverable

Intesa Sanpaolo Assicura Porter's Five Forces Analysis

This preview displays the exact Porter’s Five Forces analysis for Intesa Sanpaolo Assicura you’ll receive—fully formatted and ready to use. The assessment covers competitive rivalry, supplier and buyer power, threats of entry and substitution with actionable insights. No placeholders or samples; purchase grants immediate download of this same file. Use it as-is for strategy, valuation, or reporting.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Intesa Sanpaolo Assicura faces moderate buyer power, high regulatory scrutiny, and fierce rivalry tempered by strong bancassurance distribution and brand advantages; supplier leverage and digital insurtech substitutes present emerging risks. This snapshot highlights strategic pressures and opportunity areas. Unlock the full Porter's Five Forces Analysis to explore Intesa Sanpaolo Assicura’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on bank distribution

Intesa Sanpaolo’s reliance on its c.3,300-branch network concentrates distribution power inside the group, making branch priorities a de facto supplier with material influence on premium growth. Any shift in bank incentives or cross-sell focus can move significant volumes—bank channels account for roughly 80% of Assicura’s premiums—so opportunity cost within branches can reduce shelf space. Strong intra-group governance lowers conflict but does not eliminate medium supplier leverage.

Reinsurers and capital providers

Reinsurers supply risk capacity and shape terms, ceding commissions and underwriting appetite; in 2023–24 peak-cat and volatile lines saw reinsurance pricing increases of roughly 30–60%, boosting reinsurers’ bargaining power and compressing primary margins. Strong credit quality and diversified books enable Intesa Sanpaolo Assicura to secure firmer treaty terms and lower cession rates. Nonetheless, dependence on external reinsurance capacity remains a structural supplier power.

Data, IT platforms, and analytics vendors

Pricing, fraud detection and claims automation for Intesa Sanpaolo Assicura depend on specialized data and analytics vendors, giving them leverage as switching costs and integration complexity are high. Top 3 cloud vendors held roughly 64% of the global cloud market in 2023–24, concentrating supplier power for core infrastructure. Modular cloud stacks and APIs can reduce lock-in over time, but critical systems in the near term sustain supplier negotiating power.

Repair, medical, and service networks

Repair, medical and service networks are essential for non-life and health claims, and local concentration in some Italian regions raises suppliers’ leverage on tariffs and service terms, forcing insurers to negotiate access and pricing. Volume steering and preferred-provider networks help Intesa Sanpaolo Assicura rebalance unit economics, though service-cost inflation can still transmit into loss ratios.

- Regional concentration elevates tariff leverage

- Preferred networks enable cost steering

- Service inflation feeds loss ratios

Actuarial and technical talent

- Specialist scarcity: elevates bargaining power

- Mitigation: internal training, group mobility

- Cost impact: higher retention spend

- Operational risk: delayed launches/innovation

Supplier power: banks ~80%, reinsurers +30-60%

Supplier power is moderate-high: bank channels (c.80% of premiums) and c.3,300 branches give the group internal distribution leverage but create internal supplier risk. Reinsurer pricing rose ~30–60% in 2023–24, increasing external bargaining power and margin pressure. Cloud and analytics vendors (top3 ~64% market share) and scarce actuarial talent (group ~95,000 employees in 2024) sustain switching costs and retention expense.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Bank channels | % premiums | ~80% |

| Branches | count | ~3,300 |

| Reinsurance | pricing change | +30–60% |

| Cloud vendors | top3 market share | ~64% |

| Employees | group headcount | ~95,000 (2024) |

What is included in the product

Tailored Porter’s Five Forces analysis for Intesa Sanpaolo Assicura that uncovers competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and regulatory risks shaping pricing, market share, and profitability.

A clear, one-sheet summary of all five forces for Intesa Sanpaolo Assicura—perfect for quick decision-making and pinpointing competitive pain points. Swap in your own data and duplicate tabs for regulatory or market scenarios to relieve analysis bottlenecks.

Customers Bargaining Power

Retail customers via bancassurance

Branch-originated retail customers of Intesa Sanpaolo Assicura benefit from convenience and product bundling via a bancassurance network of over 3,000 branches, which reduces price sensitivity and shopping behavior. Cross-selling with banking products drives stickiness and keeps churn in the low single digits, further lowering buyer leverage. IDD-driven transparency and IVASS oversight in 2024 raise value expectations, tempering but not overturning bargaining power, which remains moderate-to-low.

SMEs and corporate clients

Larger SME and corporate buyers—in a market where SMEs account for over 99% of EU firms and about 67% of employment in 2024—increasingly solicit multiple quotes and push hard on terms. Their demand for risk engineering and bespoke coverage raises bargaining leverage, while Intesa Sanpaolo Assicura’s bancassurance ties aid retention but cannot prevent price-sensitive defections. Resulting frequent discounts and endorsement requests compress margins and shift underwriting risk.

Price comparison and digital channels

Aggregators and online reviews have tightened information symmetry, with 2024 industry reports showing comparison sites influence over 60% of online insurance purchase decisions in Italy. Commoditized lines such as motor see elevated buyer power as price becomes easily comparable across providers. Intuitive digital onboarding and UX can raise conversion rates and foster loyalty, partially offsetting price pressure. Still, headline premium remains the primary decision driver for most online shoppers.

Switching costs and product complexity

Life and multi-year policies for Intesa Sanpaolo Assicura create customer inertia and perceived switching costs, reinforced by bancassurance channels that account for about 50% of Italian life premiums in 2023-24; bank staff advice further anchors choices and reduces churn. Claims experience and service quality remain decisive at renewal, with poor service able to reverse low switching despite product complexity.

- Inertia: long-term policies

- Advisor anchoring: bancassurance ~50% (2023-24)

- Service-driven churn: claims quality critical

- Complexity lowers buyer power but is fragile

Sensitivity to macro and rates

Customers of Intesa Sanpaolo Assicura are sensitive to inflation, income pressure and interest-rate moves; Italian inflation eased to about 2.6% in 2024 while the ECB deposit rate averaged near 4.0%, making attractive deposit yields a stronger competitor to life savings. In tight times buyers press for lower premiums or stronger guarantees, and episodic macro shocks raise buyer leverage, reducing pricing power.

- Inflation: 2.6% (2024)

- ECB deposit rate: ~4.0% (2024)

- Effect: higher deposit pull vs life products

Branch 3,000+, aggregators > 60% shape online sales

Branch retail via 3,000+ branches and cross-selling reduces price sensitivity and keeps churn in low single digits. SME/corporate buyers push on price for bespoke cover, raising bargaining leverage. Aggregators influence >60% of online purchases, boosting price comparability. Life bancassurance ~50% (2023-24); inflation 2.6% and ECB rate ~4.0% increase deposit competition.

| Metric | 2024 Value |

|---|---|

| Branches | >3,000 |

| Online comparison influence | >60% |

| Bancassurance life share | ~50% (2023-24) |

| Inflation | 2.6% |

| ECB deposit rate | ~4.0% |

Preview the Actual Deliverable

Intesa Sanpaolo Assicura Porter's Five Forces Analysis

This preview displays the exact Porter’s Five Forces analysis for Intesa Sanpaolo Assicura you’ll receive—fully formatted and ready to use. The assessment covers competitive rivalry, supplier and buyer power, threats of entry and substitution with actionable insights. No placeholders or samples; purchase grants immediate download of this same file. Use it as-is for strategy, valuation, or reporting.