Ionis Boston Consulting Group Matrix

Unlock Strategic Clarity

Want a straight answer on where Ionis’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot points you in the right direction, but buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel files. Get instant access and a practical playbook to reallocate capital, prioritize R&D, and make smarter product decisions—fast.

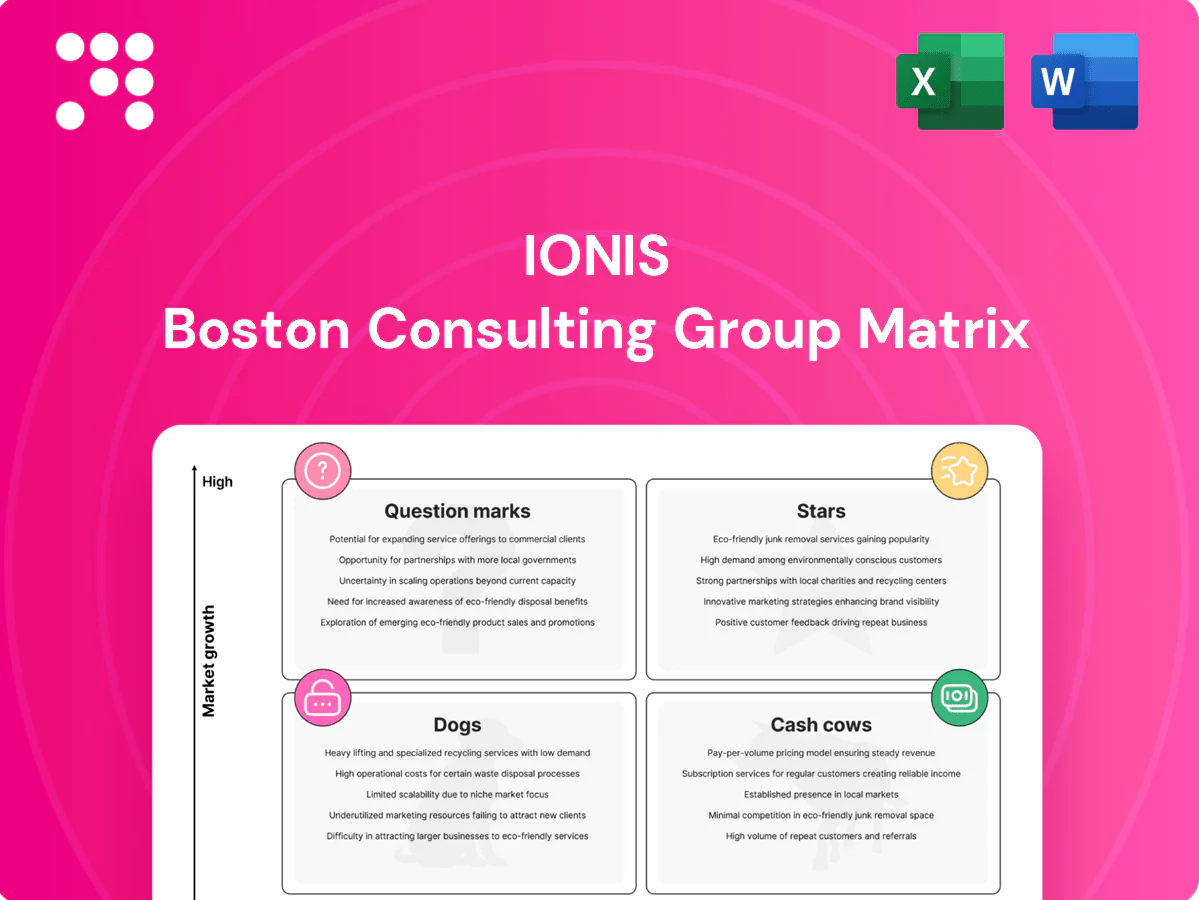

Stars

Antisense platform leadership

Ionis, founded in 1989, effectively owns the antisense lane with 30+ years of IP and chemistry know‑how that has attracted partners including Biogen, AstraZeneca and Roche. That high share in a still‑expanding modality fuels dozens of partnered programs and premium talent pipelines others struggle to replicate. Prioritize more clinical data, faster IND/POC timelines and tighter CMC to convert platform leadership into a compounding revenue engine.

Eplontersen (ATTR polyneuropathy) launch

ATTR market ~3.5B in 2024 with ~12% CAGR; eplontersen launches with a strong partner and a clean safety profile, early momentum plus category expansion should drive rapid uptake, but launch will require ~200M for access, hubs and field buildout; prioritize adherence and real‑world outcomes now to transition to Cash Cow as the market matures.

Neurology franchise (ALS and beyond)

Tofersen established a technical ownership in SOD1‑ALS after FDA approval in April 2023, securing a beachhead in a small but high-value segment where SOD1 mutations account for roughly 1–2% of ALS cases. That real-world credibility lifts Ionis’s broader neurology franchise as regulators and KOLs grow comfortable with RNA therapeutics—there were over 20 approved RNA drugs by 2024. Continued investment in centers of excellence and patient registries will help lock in share and expand lifetime patient capture.

Partnering flywheel (tier‑one pharmas)

Partnering flywheel with tier‑one pharmas de‑risks large indications and opens payer channels; top 10 pharma firms captured roughly 40% of global drug sales in 2024, accelerating reimbursement conversations and market access for collaborators.

In hot markets alliances close faster and compound awareness; 2024 biotech‑pharma deals commonly featured upfronts plus milestones >$100M and royalty bands ~10–25%, enabling co‑dev now and outsized royalties later. Stay selective and insist on co‑promotion rights where commercial leverage matters.

- De‑risk: top10 ≈40% global sales (2024)

- Deal economics: upfronts+milestones often >$100M (2024)

- Royalty range: ~10–25% (2024)

- Strategy: push co‑promotion rights

Cardio-renal visibility (brand halo)

Even before approvals, Ionis is being perceived as the RNA cardiometabolic specialist, which strengthens trial recruitment, site engagement, and patient trust in a crowded cardiometabolic market.

That brand halo drives high expectations and elevated R&D and commercial spend now; maintaining a tight data cadence and frequent positive readouts is essential to convert visibility into durable market share.

Antisense leadership drives partnered launches; ATTR market $3.5B

Ionis’s Stars: antisense leadership (30+ yr IP) fuels partnered launches (ATTR market $3.5B in 2024, ~12% CAGR) and neurology beachhead (SOD1 ≈1–2% ALS). Tier‑1 partners de‑risk commercialization (top10 ≈40% global sales 2024); prioritize faster IND/POC, CMC, and real‑world outcomes to shift Stars to Cash Cows.

| Metric | Value |

|---|---|

| Antisense IP | 30+ yrs |

| ATTR market 2024 | $3.5B |

| CAGR | ~12% |

| SOD1 ALS | 1–2% |

| Top10 pharma share | ~40% |

What is included in the product

BCG Matrix review of Ionis products with quadrant strategies, investment priorities, and key risks.

One-page BCG matrix highlighting pain points per unit, ready to export to PowerPoint and print.

Cash Cows

Spinraza (SMA) royalty stream

Spinraza (nusinersen), approved in 2016, has a large installed global patient base and chronic dosing, marking it as a classic mature market leader. Growth is modest under SMA competition and gene-therapy entrants, but the royalty stream delivers steady cash to Ionis with low incremental cost. Continued analytics and lifecycle management defend the tail and optimize lifetime value.

Legacy and partnered royalty portfolio

Legacy and partnered royalty portfolio provides a diversified basket of royalties and milestones that smooths Ionis’s P&L, with 2024 receipts bolstering cash flow from multiple partners. Individually small, these royalties aggregate into a meaningful revenue stream that reduces volatility. Minimal promotional spend is required from Ionis while maintaining partner support and strict IP hygiene ensures timely royalty checks.

Platform access/licensing economics

Platform access and method‑of‑use IP deals generate cash without field operations, with licensing revenue models delivering industry gross margins often above 80% and typically low single‑digit annual growth in 2024. These high‑margin, low‑capex inflows fund Ionis’ R&D pipeline and reduce need for equity dilution. Maintain disciplined terms and avoid underpricing the toolkit to preserve long‑term value and bargaining leverage.

Established rare-disease geographies (select markets)

Niche territories with entrenched prescribers and predictable demand deliver steady trickle‑in revenue for Ionis in established rare‑disease markets. Little promotional lift is needed beyond targeted medical education. Margins improve with supply‑chain tuning; optimize distribution and avoid bloating local footprints. Rare diseases affect about 300 million people worldwide (WHO).

- Steady revenue: low marketing spend

- High margin upside: supply tuning

- Distribution focus: avoid footprint bloat

- Clinical reach: entrenched prescribers

Back-end milestones from late-stage partners

Back-end milestones from late-stage partners convert trial endpoints and regulatory filings into episodic cash inflows; as partnered assets reach submissions or approvals, milestone checks are triggered and deposited without the need for a salesforce or DTC spend. In 2024 Ionis’s mature deal stack smoothed variability across quarters, turning paper-based royalty and milestone clauses into predictable yield when governance prevents slippage. Keep program governance tight to preserve timing and amount of these payouts.

- No salesforce or DTC: lower opex, higher net yield

- Episodic but averaged: portfolio smoothing across quarters

- Governance focus: reduces milestone slippage and payment delays

Cash cows: royalties & assets fund R&D with >80% licensing margins

Cash cows: established royalties and legacy assets deliver predictable, high‑margin cash with minimal opex, funding R&D and reducing dilution. Spinraza’s chronic-use base and partnered milestones in 2024 smoothed quarterly receipts. Licensing/platform fees offer >80% gross margins and low capex, while niche rare‑disease territories sustain stable demand.

| Metric | 2024 Fact |

|---|---|

| Rare disease prevalence | WHO: ~300 million |

| Platform margins | >80% (licensing) |

Full Transparency, Always

Ionis BCG Matrix

The file you're previewing here is the exact Ionis BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted strategic report ready to use. It arrives immediately for editing, printing, or presenting. Designed by analysts for clear decision-making, no surprises—just plug-and-play value.

Unlock Strategic Clarity

Want a straight answer on where Ionis’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot points you in the right direction, but buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel files. Get instant access and a practical playbook to reallocate capital, prioritize R&D, and make smarter product decisions—fast.

Stars

Antisense platform leadership

Ionis, founded in 1989, effectively owns the antisense lane with 30+ years of IP and chemistry know‑how that has attracted partners including Biogen, AstraZeneca and Roche. That high share in a still‑expanding modality fuels dozens of partnered programs and premium talent pipelines others struggle to replicate. Prioritize more clinical data, faster IND/POC timelines and tighter CMC to convert platform leadership into a compounding revenue engine.

Eplontersen (ATTR polyneuropathy) launch

ATTR market ~3.5B in 2024 with ~12% CAGR; eplontersen launches with a strong partner and a clean safety profile, early momentum plus category expansion should drive rapid uptake, but launch will require ~200M for access, hubs and field buildout; prioritize adherence and real‑world outcomes now to transition to Cash Cow as the market matures.

Neurology franchise (ALS and beyond)

Tofersen established a technical ownership in SOD1‑ALS after FDA approval in April 2023, securing a beachhead in a small but high-value segment where SOD1 mutations account for roughly 1–2% of ALS cases. That real-world credibility lifts Ionis’s broader neurology franchise as regulators and KOLs grow comfortable with RNA therapeutics—there were over 20 approved RNA drugs by 2024. Continued investment in centers of excellence and patient registries will help lock in share and expand lifetime patient capture.

Partnering flywheel (tier‑one pharmas)

Partnering flywheel with tier‑one pharmas de‑risks large indications and opens payer channels; top 10 pharma firms captured roughly 40% of global drug sales in 2024, accelerating reimbursement conversations and market access for collaborators.

In hot markets alliances close faster and compound awareness; 2024 biotech‑pharma deals commonly featured upfronts plus milestones >$100M and royalty bands ~10–25%, enabling co‑dev now and outsized royalties later. Stay selective and insist on co‑promotion rights where commercial leverage matters.

- De‑risk: top10 ≈40% global sales (2024)

- Deal economics: upfronts+milestones often >$100M (2024)

- Royalty range: ~10–25% (2024)

- Strategy: push co‑promotion rights

Cardio-renal visibility (brand halo)

Even before approvals, Ionis is being perceived as the RNA cardiometabolic specialist, which strengthens trial recruitment, site engagement, and patient trust in a crowded cardiometabolic market.

That brand halo drives high expectations and elevated R&D and commercial spend now; maintaining a tight data cadence and frequent positive readouts is essential to convert visibility into durable market share.

Antisense leadership drives partnered launches; ATTR market $3.5B

Ionis’s Stars: antisense leadership (30+ yr IP) fuels partnered launches (ATTR market $3.5B in 2024, ~12% CAGR) and neurology beachhead (SOD1 ≈1–2% ALS). Tier‑1 partners de‑risk commercialization (top10 ≈40% global sales 2024); prioritize faster IND/POC, CMC, and real‑world outcomes to shift Stars to Cash Cows.

| Metric | Value |

|---|---|

| Antisense IP | 30+ yrs |

| ATTR market 2024 | $3.5B |

| CAGR | ~12% |

| SOD1 ALS | 1–2% |

| Top10 pharma share | ~40% |

What is included in the product

BCG Matrix review of Ionis products with quadrant strategies, investment priorities, and key risks.

One-page BCG matrix highlighting pain points per unit, ready to export to PowerPoint and print.

Cash Cows

Spinraza (SMA) royalty stream

Spinraza (nusinersen), approved in 2016, has a large installed global patient base and chronic dosing, marking it as a classic mature market leader. Growth is modest under SMA competition and gene-therapy entrants, but the royalty stream delivers steady cash to Ionis with low incremental cost. Continued analytics and lifecycle management defend the tail and optimize lifetime value.

Legacy and partnered royalty portfolio

Legacy and partnered royalty portfolio provides a diversified basket of royalties and milestones that smooths Ionis’s P&L, with 2024 receipts bolstering cash flow from multiple partners. Individually small, these royalties aggregate into a meaningful revenue stream that reduces volatility. Minimal promotional spend is required from Ionis while maintaining partner support and strict IP hygiene ensures timely royalty checks.

Platform access/licensing economics

Platform access and method‑of‑use IP deals generate cash without field operations, with licensing revenue models delivering industry gross margins often above 80% and typically low single‑digit annual growth in 2024. These high‑margin, low‑capex inflows fund Ionis’ R&D pipeline and reduce need for equity dilution. Maintain disciplined terms and avoid underpricing the toolkit to preserve long‑term value and bargaining leverage.

Established rare-disease geographies (select markets)

Niche territories with entrenched prescribers and predictable demand deliver steady trickle‑in revenue for Ionis in established rare‑disease markets. Little promotional lift is needed beyond targeted medical education. Margins improve with supply‑chain tuning; optimize distribution and avoid bloating local footprints. Rare diseases affect about 300 million people worldwide (WHO).

- Steady revenue: low marketing spend

- High margin upside: supply tuning

- Distribution focus: avoid footprint bloat

- Clinical reach: entrenched prescribers

Back-end milestones from late-stage partners

Back-end milestones from late-stage partners convert trial endpoints and regulatory filings into episodic cash inflows; as partnered assets reach submissions or approvals, milestone checks are triggered and deposited without the need for a salesforce or DTC spend. In 2024 Ionis’s mature deal stack smoothed variability across quarters, turning paper-based royalty and milestone clauses into predictable yield when governance prevents slippage. Keep program governance tight to preserve timing and amount of these payouts.

- No salesforce or DTC: lower opex, higher net yield

- Episodic but averaged: portfolio smoothing across quarters

- Governance focus: reduces milestone slippage and payment delays

Cash cows: royalties & assets fund R&D with >80% licensing margins

Cash cows: established royalties and legacy assets deliver predictable, high‑margin cash with minimal opex, funding R&D and reducing dilution. Spinraza’s chronic-use base and partnered milestones in 2024 smoothed quarterly receipts. Licensing/platform fees offer >80% gross margins and low capex, while niche rare‑disease territories sustain stable demand.

| Metric | 2024 Fact |

|---|---|

| Rare disease prevalence | WHO: ~300 million |

| Platform margins | >80% (licensing) |

Full Transparency, Always

Ionis BCG Matrix

The file you're previewing here is the exact Ionis BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted strategic report ready to use. It arrives immediately for editing, printing, or presenting. Designed by analysts for clear decision-making, no surprises—just plug-and-play value.

Description

Unlock Strategic Clarity

Want a straight answer on where Ionis’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot points you in the right direction, but buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel files. Get instant access and a practical playbook to reallocate capital, prioritize R&D, and make smarter product decisions—fast.

Stars

Antisense platform leadership

Ionis, founded in 1989, effectively owns the antisense lane with 30+ years of IP and chemistry know‑how that has attracted partners including Biogen, AstraZeneca and Roche. That high share in a still‑expanding modality fuels dozens of partnered programs and premium talent pipelines others struggle to replicate. Prioritize more clinical data, faster IND/POC timelines and tighter CMC to convert platform leadership into a compounding revenue engine.

Eplontersen (ATTR polyneuropathy) launch

ATTR market ~3.5B in 2024 with ~12% CAGR; eplontersen launches with a strong partner and a clean safety profile, early momentum plus category expansion should drive rapid uptake, but launch will require ~200M for access, hubs and field buildout; prioritize adherence and real‑world outcomes now to transition to Cash Cow as the market matures.

Neurology franchise (ALS and beyond)

Tofersen established a technical ownership in SOD1‑ALS after FDA approval in April 2023, securing a beachhead in a small but high-value segment where SOD1 mutations account for roughly 1–2% of ALS cases. That real-world credibility lifts Ionis’s broader neurology franchise as regulators and KOLs grow comfortable with RNA therapeutics—there were over 20 approved RNA drugs by 2024. Continued investment in centers of excellence and patient registries will help lock in share and expand lifetime patient capture.

Partnering flywheel (tier‑one pharmas)

Partnering flywheel with tier‑one pharmas de‑risks large indications and opens payer channels; top 10 pharma firms captured roughly 40% of global drug sales in 2024, accelerating reimbursement conversations and market access for collaborators.

In hot markets alliances close faster and compound awareness; 2024 biotech‑pharma deals commonly featured upfronts plus milestones >$100M and royalty bands ~10–25%, enabling co‑dev now and outsized royalties later. Stay selective and insist on co‑promotion rights where commercial leverage matters.

- De‑risk: top10 ≈40% global sales (2024)

- Deal economics: upfronts+milestones often >$100M (2024)

- Royalty range: ~10–25% (2024)

- Strategy: push co‑promotion rights

Cardio-renal visibility (brand halo)

Even before approvals, Ionis is being perceived as the RNA cardiometabolic specialist, which strengthens trial recruitment, site engagement, and patient trust in a crowded cardiometabolic market.

That brand halo drives high expectations and elevated R&D and commercial spend now; maintaining a tight data cadence and frequent positive readouts is essential to convert visibility into durable market share.

Antisense leadership drives partnered launches; ATTR market $3.5B

Ionis’s Stars: antisense leadership (30+ yr IP) fuels partnered launches (ATTR market $3.5B in 2024, ~12% CAGR) and neurology beachhead (SOD1 ≈1–2% ALS). Tier‑1 partners de‑risk commercialization (top10 ≈40% global sales 2024); prioritize faster IND/POC, CMC, and real‑world outcomes to shift Stars to Cash Cows.

| Metric | Value |

|---|---|

| Antisense IP | 30+ yrs |

| ATTR market 2024 | $3.5B |

| CAGR | ~12% |

| SOD1 ALS | 1–2% |

| Top10 pharma share | ~40% |

What is included in the product

BCG Matrix review of Ionis products with quadrant strategies, investment priorities, and key risks.

One-page BCG matrix highlighting pain points per unit, ready to export to PowerPoint and print.

Cash Cows

Spinraza (SMA) royalty stream

Spinraza (nusinersen), approved in 2016, has a large installed global patient base and chronic dosing, marking it as a classic mature market leader. Growth is modest under SMA competition and gene-therapy entrants, but the royalty stream delivers steady cash to Ionis with low incremental cost. Continued analytics and lifecycle management defend the tail and optimize lifetime value.

Legacy and partnered royalty portfolio

Legacy and partnered royalty portfolio provides a diversified basket of royalties and milestones that smooths Ionis’s P&L, with 2024 receipts bolstering cash flow from multiple partners. Individually small, these royalties aggregate into a meaningful revenue stream that reduces volatility. Minimal promotional spend is required from Ionis while maintaining partner support and strict IP hygiene ensures timely royalty checks.

Platform access/licensing economics

Platform access and method‑of‑use IP deals generate cash without field operations, with licensing revenue models delivering industry gross margins often above 80% and typically low single‑digit annual growth in 2024. These high‑margin, low‑capex inflows fund Ionis’ R&D pipeline and reduce need for equity dilution. Maintain disciplined terms and avoid underpricing the toolkit to preserve long‑term value and bargaining leverage.

Established rare-disease geographies (select markets)

Niche territories with entrenched prescribers and predictable demand deliver steady trickle‑in revenue for Ionis in established rare‑disease markets. Little promotional lift is needed beyond targeted medical education. Margins improve with supply‑chain tuning; optimize distribution and avoid bloating local footprints. Rare diseases affect about 300 million people worldwide (WHO).

- Steady revenue: low marketing spend

- High margin upside: supply tuning

- Distribution focus: avoid footprint bloat

- Clinical reach: entrenched prescribers

Back-end milestones from late-stage partners

Back-end milestones from late-stage partners convert trial endpoints and regulatory filings into episodic cash inflows; as partnered assets reach submissions or approvals, milestone checks are triggered and deposited without the need for a salesforce or DTC spend. In 2024 Ionis’s mature deal stack smoothed variability across quarters, turning paper-based royalty and milestone clauses into predictable yield when governance prevents slippage. Keep program governance tight to preserve timing and amount of these payouts.

- No salesforce or DTC: lower opex, higher net yield

- Episodic but averaged: portfolio smoothing across quarters

- Governance focus: reduces milestone slippage and payment delays

Cash cows: royalties & assets fund R&D with >80% licensing margins

Cash cows: established royalties and legacy assets deliver predictable, high‑margin cash with minimal opex, funding R&D and reducing dilution. Spinraza’s chronic-use base and partnered milestones in 2024 smoothed quarterly receipts. Licensing/platform fees offer >80% gross margins and low capex, while niche rare‑disease territories sustain stable demand.

| Metric | 2024 Fact |

|---|---|

| Rare disease prevalence | WHO: ~300 million |

| Platform margins | >80% (licensing) |

Full Transparency, Always

Ionis BCG Matrix

The file you're previewing here is the exact Ionis BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted strategic report ready to use. It arrives immediately for editing, printing, or presenting. Designed by analysts for clear decision-making, no surprises—just plug-and-play value.