Ipsen PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, regulatory scrutiny, and biotech innovation are shaping Ipsen’s strategic path—our concise PESTLE highlights the forces that matter. Ideal for investors and strategists, it translates trends into decision-ready insights. Buy the full PESTLE to get the complete, editable analysis now.

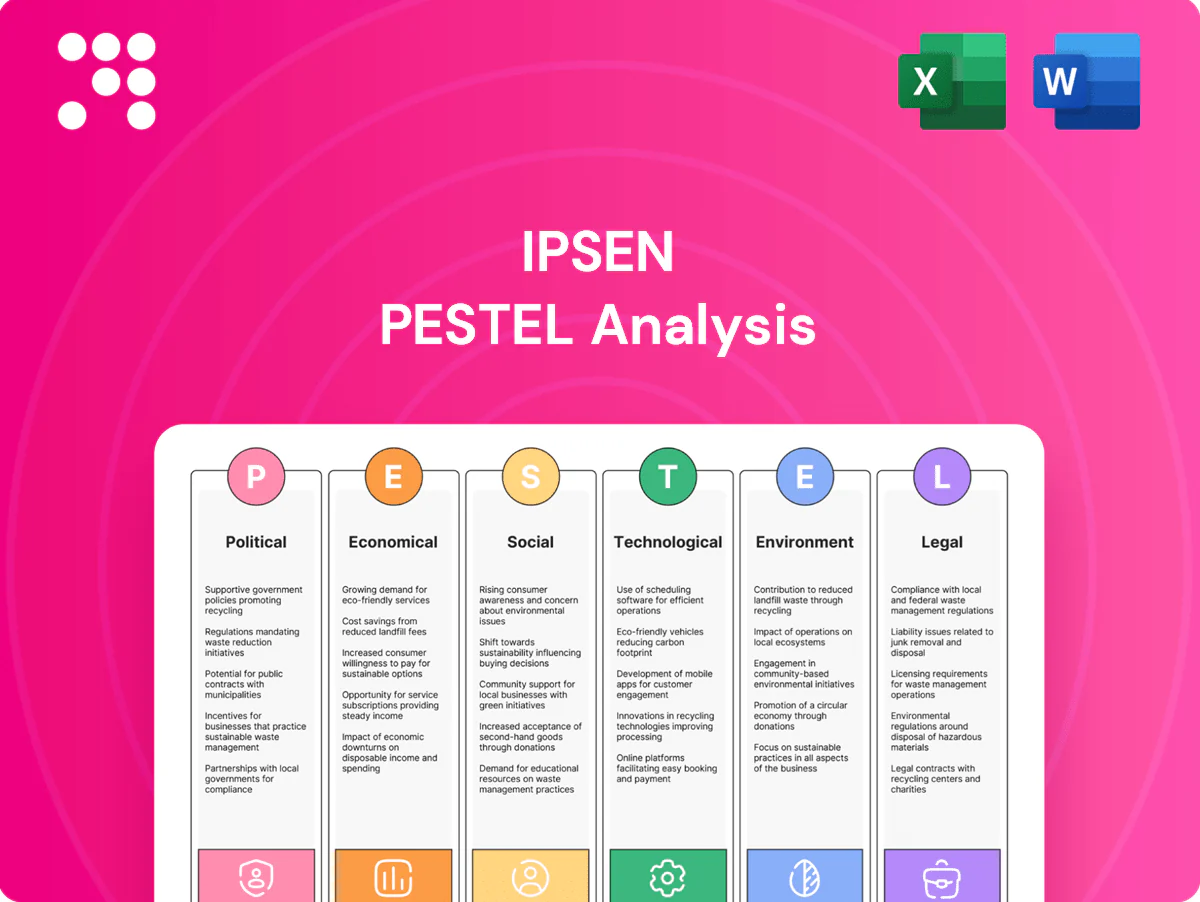

Political factors

Global drug pricing and HTA policies

National health authorities and HTA bodies—notably NICE with a £20,000–30,000/QALY threshold—directly shape pricing, access and reimbursement for specialty medicines, forcing Ipsen to adapt launch sequencing and pricing strategies.

Shifts in reference pricing or cost‑effectiveness thresholds compress margins and can delay launches in high‑price markets.

Proactive evidence generation and value‑based agreements, plus tailored multi‑country dossiers aligned to local priorities, mitigate political pressure on uptake and revenue.

Geopolitical stability and supply continuity

Conflicts, sanctions, and trade restrictions can disrupt active ingredient sourcing and distribution, so Ipsen must diversify suppliers and maintain buffer inventories for critical oncology and rare-disease products; political instability also raises logistics costs and lead times, increasing the need for regional business continuity planning and multi-country supply routes to protect patient supply.

Government incentives for biopharma R&D

Government incentives—R&D tax credits, grants and public–private partnerships—shape Ipsen site selection and pipeline investment; France's CIR (Crédit d'Impôt Recherche) alone offers up to 30% support on qualifying R&D costs, while Horizon Europe (budget ~€95.5bn for 2021–27) and UK/US tax credits and grants further lower net R&D expense. Policy shifts can expand or curtail these benefits, so active engagement secures supportive innovation ecosystems.

Public health priorities and pandemic readiness

Governments prioritize spending on life‑threatening, high‑burden conditions: WHO reports 10 million cancer deaths in 2020 and rare diseases affect ~300 million people globally, aligning with Ipsen’s oncology and rare disease focus. Post‑pandemic policies favor supply resilience and local manufacturing, shifting capital toward supply chains. Emergency use pathways can speed access but invite political scrutiny; Ipsen’s adherence to preparedness initiatives enhances stakeholder trust.

- WHO: 10M cancer deaths (2020)

- Rare diseases ~300M people

- Post‑COVID: increased focus on local manufacturing and supply resilience

- Emergency authorizations accelerate access but increase political oversight

Trade, IP, and cross-border data flows

Trade agreements and data localization laws shape Ipsen clinical-trial setups and pharmacovigilance flows; navigating EU-US data transfer rules and China localization increases operational costs and delays. Strong IP in key markets underpins ROI on specialty drugs; Ipsen reported €3.8bn revenue in 2024 supporting R&D investments. Political debates over biologics IP waivers could erode exclusivity value, so Ipsen must enforce protections while safeguarding cross-border data integrity.

- Regulatory burden: cross-border data rules raise compliance costs

- IP strength: key to recouping specialty drug R&D

- Policy risk: WTO/TRIPS debates on biologics affect exclusivity

- Operational need: robust data governance across jurisdictions

NICE £20–30k/QALY limits pricing; incentives shape R&D; cancer 10M, rare 300M

National HTA/pricing (NICE £20–30k/QALY) and reimbursement rules dictate launch sequencing and pricing, compressing margins if thresholds tighten. Trade rules, sanctions and data localization raise supply and compliance costs; strong IP and diversified suppliers protect revenues (Ipsen €3.8bn 2024). R&D incentives (France CIR up to 30%, Horizon Europe €95.5bn 2021–27) guide site and pipeline investment; political instability elevates logistics risk. WHO: cancer 10M deaths (2020); rare diseases ~300M.

| Metric | Value |

|---|---|

| NICE threshold | £20–30k/QALY |

| Ipsen revenue (2024) | €3.8bn |

| France CIR | up to 30% |

| Horizon Europe | €95.5bn (2021–27) |

| WHO cancer deaths (2020) | 10M |

| Rare disease population | ~300M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ipsen across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and detailed sub-points; designed for executives, investors and consultants to identify risks, opportunities and inform proactive strategy and funding decisions.

A concise, visually segmented Ipsen PESTLE summary highlighting regulatory, R&D, pricing and geopolitical risks for quick team alignment and slide-ready use; editable notes let users tailor insights by region, therapeutic area or business line for faster decision-making.

Economic factors

Macroeconomic cycles and healthcare budgets

Economic slowdowns pressure payer budgets and lengthen reimbursement timelines for high-cost therapies, forcing longer HTA reviews and deferred launches; Ipsen reported FY 2024 sales of about €3.4bn, underscoring exposure to timing shifts. Oncology indications often remain protected, while rare-disease funding faces greater scrutiny and tighter cost-effectiveness thresholds. Ipsen therefore needs robust health-economic evidence and a diversified portfolio to smooth revenue volatility.

Currency fluctuations and global revenue mix

As a multinational, Ipsen reported 2024 revenue of €4.03bn and faces FX risk across sales and COGS, with roughly 60% of sales outside the eurozone exposing margins to USD and emerging-market currencies. A stronger dollar versus euro can inflate reported results but compress euro-denominated margins; natural hedging through local manufacturing and financial hedges (forward contracts) reduced FX volatility in 2024. Pricing corridors in emerging markets should factor currency sensitivity and pass-through limits to protect real revenues.

Cost inflation in biologics manufacturing

Energy, raw material and single-use system costs remained inflationary into 2023–24, with EU industrial electricity ~30% above 2019 levels in 2024 and single-use bioprocessing consumables market growth around 8% in 2023, pushing COGS for Ipsen’s complex injectables and biologics higher. Efficiency programs, yield improvements and long-term supplier contracts can protect gross margins, while strategic capacity planning limits premium spot purchases.

M&A and licensing market dynamics

Competition for assets in oncology, neuroscience and rare diseases has pushed deal multiples higher, compressing bargain opportunities for mid-sized acquirers like Ipsen.

Higher interest rates raise WACC and tighten deal hurdles, forcing stricter return thresholds for BD versus funding internal R&D programs.

Earn-outs and risk-sharing structures are increasingly used to align valuation under clinical and commercial uncertainty while preserving pipeline growth.

- Competition elevates multiples

- Higher rates raise WACC

- Balance BD and R&D

- Use earn-outs/risk-share

Payer mix and private market expansion

Payer mix shifts between public programs and private insurers materially change Ipsen’s net price realization: in the US ~67% of people have private coverage while specialty medicines accounted for about 53% of US drug spend in 2023, amplifying the impact of channel and payer mix on revenue. Growth of specialty pharmacy channels and higher patient support costs compress net revenue unless market access segments by payer willingness-to-pay; copay assistance and outcomes-based contracts help sustain uptake.

- Private coverage ~67% (US, 2023)

- Specialty medicines ~53% of US drug spend (IQVIA, 2023)

NICE £20–30k/QALY limits pricing; incentives shape R&D; cancer 10M, rare 300M

Economic headwinds—slower payer budgets, higher rates and inflation—lengthen HTA timelines and pressure Ipsen’s FY2024 revenue of €4.03bn; ~60% sales outside euro expose margins to FX. COGS rose with energy ~30% above 2019 and bioprocess cost inflation; higher WACC raises deal hurdles, pushing earn-outs and risk-share deals.

| Metric | Value (2023–24) |

|---|---|

| Ipsen revenue | €4.03bn (FY2024) |

| Sales outside euro | ~60% |

| EU industrial electricity vs 2019 | +~30% |

| US private coverage | ~67% (2023) |

| Specialty med US spend | ~53% (2023) |

Preview the Actual Deliverable

Ipsen PESTLE Analysis

The preview shown here of the Ipsen PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers; this is the final, professionally structured report.

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, regulatory scrutiny, and biotech innovation are shaping Ipsen’s strategic path—our concise PESTLE highlights the forces that matter. Ideal for investors and strategists, it translates trends into decision-ready insights. Buy the full PESTLE to get the complete, editable analysis now.

Political factors

Global drug pricing and HTA policies

National health authorities and HTA bodies—notably NICE with a £20,000–30,000/QALY threshold—directly shape pricing, access and reimbursement for specialty medicines, forcing Ipsen to adapt launch sequencing and pricing strategies.

Shifts in reference pricing or cost‑effectiveness thresholds compress margins and can delay launches in high‑price markets.

Proactive evidence generation and value‑based agreements, plus tailored multi‑country dossiers aligned to local priorities, mitigate political pressure on uptake and revenue.

Geopolitical stability and supply continuity

Conflicts, sanctions, and trade restrictions can disrupt active ingredient sourcing and distribution, so Ipsen must diversify suppliers and maintain buffer inventories for critical oncology and rare-disease products; political instability also raises logistics costs and lead times, increasing the need for regional business continuity planning and multi-country supply routes to protect patient supply.

Government incentives for biopharma R&D

Government incentives—R&D tax credits, grants and public–private partnerships—shape Ipsen site selection and pipeline investment; France's CIR (Crédit d'Impôt Recherche) alone offers up to 30% support on qualifying R&D costs, while Horizon Europe (budget ~€95.5bn for 2021–27) and UK/US tax credits and grants further lower net R&D expense. Policy shifts can expand or curtail these benefits, so active engagement secures supportive innovation ecosystems.

Public health priorities and pandemic readiness

Governments prioritize spending on life‑threatening, high‑burden conditions: WHO reports 10 million cancer deaths in 2020 and rare diseases affect ~300 million people globally, aligning with Ipsen’s oncology and rare disease focus. Post‑pandemic policies favor supply resilience and local manufacturing, shifting capital toward supply chains. Emergency use pathways can speed access but invite political scrutiny; Ipsen’s adherence to preparedness initiatives enhances stakeholder trust.

- WHO: 10M cancer deaths (2020)

- Rare diseases ~300M people

- Post‑COVID: increased focus on local manufacturing and supply resilience

- Emergency authorizations accelerate access but increase political oversight

Trade, IP, and cross-border data flows

Trade agreements and data localization laws shape Ipsen clinical-trial setups and pharmacovigilance flows; navigating EU-US data transfer rules and China localization increases operational costs and delays. Strong IP in key markets underpins ROI on specialty drugs; Ipsen reported €3.8bn revenue in 2024 supporting R&D investments. Political debates over biologics IP waivers could erode exclusivity value, so Ipsen must enforce protections while safeguarding cross-border data integrity.

- Regulatory burden: cross-border data rules raise compliance costs

- IP strength: key to recouping specialty drug R&D

- Policy risk: WTO/TRIPS debates on biologics affect exclusivity

- Operational need: robust data governance across jurisdictions

NICE £20–30k/QALY limits pricing; incentives shape R&D; cancer 10M, rare 300M

National HTA/pricing (NICE £20–30k/QALY) and reimbursement rules dictate launch sequencing and pricing, compressing margins if thresholds tighten. Trade rules, sanctions and data localization raise supply and compliance costs; strong IP and diversified suppliers protect revenues (Ipsen €3.8bn 2024). R&D incentives (France CIR up to 30%, Horizon Europe €95.5bn 2021–27) guide site and pipeline investment; political instability elevates logistics risk. WHO: cancer 10M deaths (2020); rare diseases ~300M.

| Metric | Value |

|---|---|

| NICE threshold | £20–30k/QALY |

| Ipsen revenue (2024) | €3.8bn |

| France CIR | up to 30% |

| Horizon Europe | €95.5bn (2021–27) |

| WHO cancer deaths (2020) | 10M |

| Rare disease population | ~300M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ipsen across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and detailed sub-points; designed for executives, investors and consultants to identify risks, opportunities and inform proactive strategy and funding decisions.

A concise, visually segmented Ipsen PESTLE summary highlighting regulatory, R&D, pricing and geopolitical risks for quick team alignment and slide-ready use; editable notes let users tailor insights by region, therapeutic area or business line for faster decision-making.

Economic factors

Macroeconomic cycles and healthcare budgets

Economic slowdowns pressure payer budgets and lengthen reimbursement timelines for high-cost therapies, forcing longer HTA reviews and deferred launches; Ipsen reported FY 2024 sales of about €3.4bn, underscoring exposure to timing shifts. Oncology indications often remain protected, while rare-disease funding faces greater scrutiny and tighter cost-effectiveness thresholds. Ipsen therefore needs robust health-economic evidence and a diversified portfolio to smooth revenue volatility.

Currency fluctuations and global revenue mix

As a multinational, Ipsen reported 2024 revenue of €4.03bn and faces FX risk across sales and COGS, with roughly 60% of sales outside the eurozone exposing margins to USD and emerging-market currencies. A stronger dollar versus euro can inflate reported results but compress euro-denominated margins; natural hedging through local manufacturing and financial hedges (forward contracts) reduced FX volatility in 2024. Pricing corridors in emerging markets should factor currency sensitivity and pass-through limits to protect real revenues.

Cost inflation in biologics manufacturing

Energy, raw material and single-use system costs remained inflationary into 2023–24, with EU industrial electricity ~30% above 2019 levels in 2024 and single-use bioprocessing consumables market growth around 8% in 2023, pushing COGS for Ipsen’s complex injectables and biologics higher. Efficiency programs, yield improvements and long-term supplier contracts can protect gross margins, while strategic capacity planning limits premium spot purchases.

M&A and licensing market dynamics

Competition for assets in oncology, neuroscience and rare diseases has pushed deal multiples higher, compressing bargain opportunities for mid-sized acquirers like Ipsen.

Higher interest rates raise WACC and tighten deal hurdles, forcing stricter return thresholds for BD versus funding internal R&D programs.

Earn-outs and risk-sharing structures are increasingly used to align valuation under clinical and commercial uncertainty while preserving pipeline growth.

- Competition elevates multiples

- Higher rates raise WACC

- Balance BD and R&D

- Use earn-outs/risk-share

Payer mix and private market expansion

Payer mix shifts between public programs and private insurers materially change Ipsen’s net price realization: in the US ~67% of people have private coverage while specialty medicines accounted for about 53% of US drug spend in 2023, amplifying the impact of channel and payer mix on revenue. Growth of specialty pharmacy channels and higher patient support costs compress net revenue unless market access segments by payer willingness-to-pay; copay assistance and outcomes-based contracts help sustain uptake.

- Private coverage ~67% (US, 2023)

- Specialty medicines ~53% of US drug spend (IQVIA, 2023)

NICE £20–30k/QALY limits pricing; incentives shape R&D; cancer 10M, rare 300M

Economic headwinds—slower payer budgets, higher rates and inflation—lengthen HTA timelines and pressure Ipsen’s FY2024 revenue of €4.03bn; ~60% sales outside euro expose margins to FX. COGS rose with energy ~30% above 2019 and bioprocess cost inflation; higher WACC raises deal hurdles, pushing earn-outs and risk-share deals.

| Metric | Value (2023–24) |

|---|---|

| Ipsen revenue | €4.03bn (FY2024) |

| Sales outside euro | ~60% |

| EU industrial electricity vs 2019 | +~30% |

| US private coverage | ~67% (2023) |

| Specialty med US spend | ~53% (2023) |

Preview the Actual Deliverable

Ipsen PESTLE Analysis

The preview shown here of the Ipsen PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers; this is the final, professionally structured report.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, regulatory scrutiny, and biotech innovation are shaping Ipsen’s strategic path—our concise PESTLE highlights the forces that matter. Ideal for investors and strategists, it translates trends into decision-ready insights. Buy the full PESTLE to get the complete, editable analysis now.

Political factors

Global drug pricing and HTA policies

National health authorities and HTA bodies—notably NICE with a £20,000–30,000/QALY threshold—directly shape pricing, access and reimbursement for specialty medicines, forcing Ipsen to adapt launch sequencing and pricing strategies.

Shifts in reference pricing or cost‑effectiveness thresholds compress margins and can delay launches in high‑price markets.

Proactive evidence generation and value‑based agreements, plus tailored multi‑country dossiers aligned to local priorities, mitigate political pressure on uptake and revenue.

Geopolitical stability and supply continuity

Conflicts, sanctions, and trade restrictions can disrupt active ingredient sourcing and distribution, so Ipsen must diversify suppliers and maintain buffer inventories for critical oncology and rare-disease products; political instability also raises logistics costs and lead times, increasing the need for regional business continuity planning and multi-country supply routes to protect patient supply.

Government incentives for biopharma R&D

Government incentives—R&D tax credits, grants and public–private partnerships—shape Ipsen site selection and pipeline investment; France's CIR (Crédit d'Impôt Recherche) alone offers up to 30% support on qualifying R&D costs, while Horizon Europe (budget ~€95.5bn for 2021–27) and UK/US tax credits and grants further lower net R&D expense. Policy shifts can expand or curtail these benefits, so active engagement secures supportive innovation ecosystems.

Public health priorities and pandemic readiness

Governments prioritize spending on life‑threatening, high‑burden conditions: WHO reports 10 million cancer deaths in 2020 and rare diseases affect ~300 million people globally, aligning with Ipsen’s oncology and rare disease focus. Post‑pandemic policies favor supply resilience and local manufacturing, shifting capital toward supply chains. Emergency use pathways can speed access but invite political scrutiny; Ipsen’s adherence to preparedness initiatives enhances stakeholder trust.

- WHO: 10M cancer deaths (2020)

- Rare diseases ~300M people

- Post‑COVID: increased focus on local manufacturing and supply resilience

- Emergency authorizations accelerate access but increase political oversight

Trade, IP, and cross-border data flows

Trade agreements and data localization laws shape Ipsen clinical-trial setups and pharmacovigilance flows; navigating EU-US data transfer rules and China localization increases operational costs and delays. Strong IP in key markets underpins ROI on specialty drugs; Ipsen reported €3.8bn revenue in 2024 supporting R&D investments. Political debates over biologics IP waivers could erode exclusivity value, so Ipsen must enforce protections while safeguarding cross-border data integrity.

- Regulatory burden: cross-border data rules raise compliance costs

- IP strength: key to recouping specialty drug R&D

- Policy risk: WTO/TRIPS debates on biologics affect exclusivity

- Operational need: robust data governance across jurisdictions

NICE £20–30k/QALY limits pricing; incentives shape R&D; cancer 10M, rare 300M

National HTA/pricing (NICE £20–30k/QALY) and reimbursement rules dictate launch sequencing and pricing, compressing margins if thresholds tighten. Trade rules, sanctions and data localization raise supply and compliance costs; strong IP and diversified suppliers protect revenues (Ipsen €3.8bn 2024). R&D incentives (France CIR up to 30%, Horizon Europe €95.5bn 2021–27) guide site and pipeline investment; political instability elevates logistics risk. WHO: cancer 10M deaths (2020); rare diseases ~300M.

| Metric | Value |

|---|---|

| NICE threshold | £20–30k/QALY |

| Ipsen revenue (2024) | €3.8bn |

| France CIR | up to 30% |

| Horizon Europe | €95.5bn (2021–27) |

| WHO cancer deaths (2020) | 10M |

| Rare disease population | ~300M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ipsen across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and detailed sub-points; designed for executives, investors and consultants to identify risks, opportunities and inform proactive strategy and funding decisions.

A concise, visually segmented Ipsen PESTLE summary highlighting regulatory, R&D, pricing and geopolitical risks for quick team alignment and slide-ready use; editable notes let users tailor insights by region, therapeutic area or business line for faster decision-making.

Economic factors

Macroeconomic cycles and healthcare budgets

Economic slowdowns pressure payer budgets and lengthen reimbursement timelines for high-cost therapies, forcing longer HTA reviews and deferred launches; Ipsen reported FY 2024 sales of about €3.4bn, underscoring exposure to timing shifts. Oncology indications often remain protected, while rare-disease funding faces greater scrutiny and tighter cost-effectiveness thresholds. Ipsen therefore needs robust health-economic evidence and a diversified portfolio to smooth revenue volatility.

Currency fluctuations and global revenue mix

As a multinational, Ipsen reported 2024 revenue of €4.03bn and faces FX risk across sales and COGS, with roughly 60% of sales outside the eurozone exposing margins to USD and emerging-market currencies. A stronger dollar versus euro can inflate reported results but compress euro-denominated margins; natural hedging through local manufacturing and financial hedges (forward contracts) reduced FX volatility in 2024. Pricing corridors in emerging markets should factor currency sensitivity and pass-through limits to protect real revenues.

Cost inflation in biologics manufacturing

Energy, raw material and single-use system costs remained inflationary into 2023–24, with EU industrial electricity ~30% above 2019 levels in 2024 and single-use bioprocessing consumables market growth around 8% in 2023, pushing COGS for Ipsen’s complex injectables and biologics higher. Efficiency programs, yield improvements and long-term supplier contracts can protect gross margins, while strategic capacity planning limits premium spot purchases.

M&A and licensing market dynamics

Competition for assets in oncology, neuroscience and rare diseases has pushed deal multiples higher, compressing bargain opportunities for mid-sized acquirers like Ipsen.

Higher interest rates raise WACC and tighten deal hurdles, forcing stricter return thresholds for BD versus funding internal R&D programs.

Earn-outs and risk-sharing structures are increasingly used to align valuation under clinical and commercial uncertainty while preserving pipeline growth.

- Competition elevates multiples

- Higher rates raise WACC

- Balance BD and R&D

- Use earn-outs/risk-share

Payer mix and private market expansion

Payer mix shifts between public programs and private insurers materially change Ipsen’s net price realization: in the US ~67% of people have private coverage while specialty medicines accounted for about 53% of US drug spend in 2023, amplifying the impact of channel and payer mix on revenue. Growth of specialty pharmacy channels and higher patient support costs compress net revenue unless market access segments by payer willingness-to-pay; copay assistance and outcomes-based contracts help sustain uptake.

- Private coverage ~67% (US, 2023)

- Specialty medicines ~53% of US drug spend (IQVIA, 2023)

NICE £20–30k/QALY limits pricing; incentives shape R&D; cancer 10M, rare 300M

Economic headwinds—slower payer budgets, higher rates and inflation—lengthen HTA timelines and pressure Ipsen’s FY2024 revenue of €4.03bn; ~60% sales outside euro expose margins to FX. COGS rose with energy ~30% above 2019 and bioprocess cost inflation; higher WACC raises deal hurdles, pushing earn-outs and risk-share deals.

| Metric | Value (2023–24) |

|---|---|

| Ipsen revenue | €4.03bn (FY2024) |

| Sales outside euro | ~60% |

| EU industrial electricity vs 2019 | +~30% |

| US private coverage | ~67% (2023) |

| Specialty med US spend | ~53% (2023) |

Preview the Actual Deliverable

Ipsen PESTLE Analysis

The preview shown here of the Ipsen PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers; this is the final, professionally structured report.