Ipsos PESTLE Analysis

Your Shortcut to Market Insight Starts Here

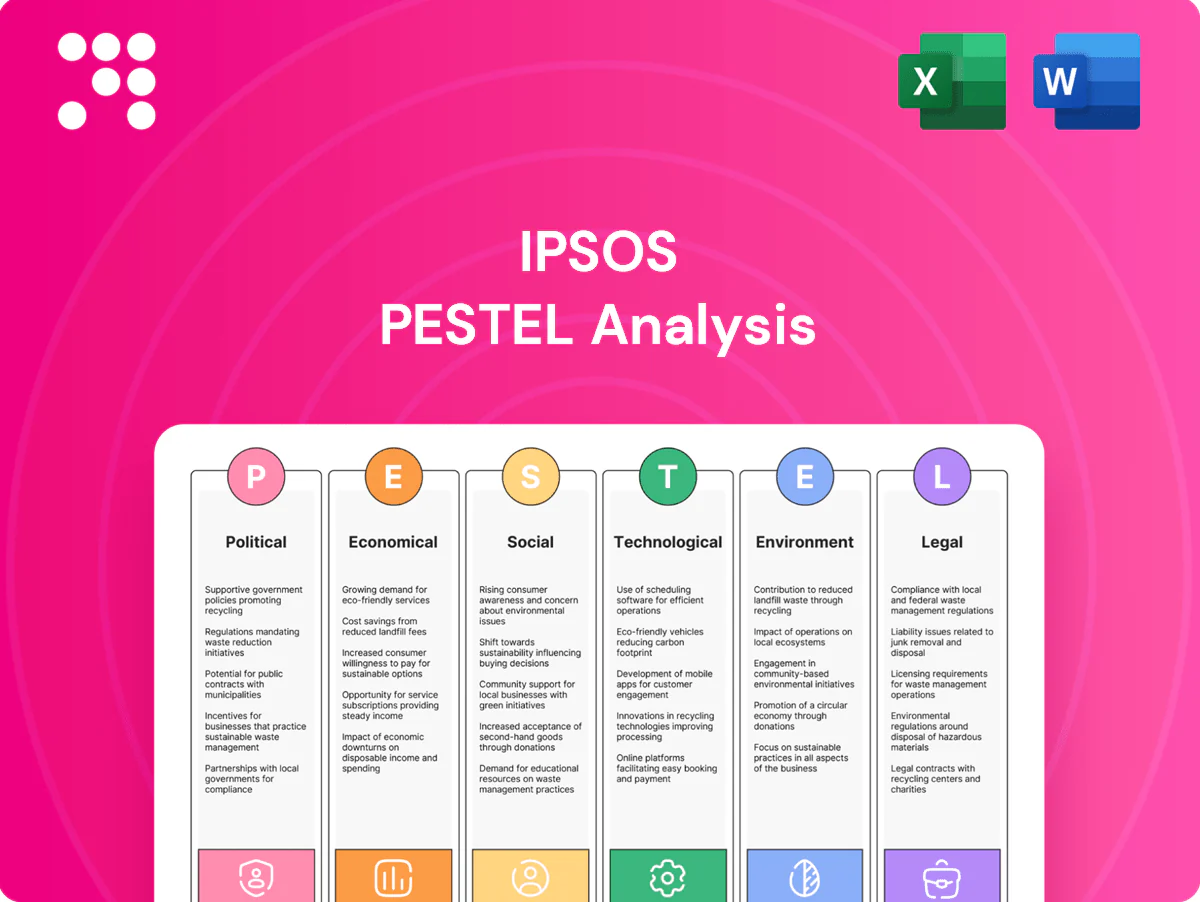

Gain strategic foresight with our Ipsos PESTLE Analysis—concise, expert-reviewed insights into political, economic, social, technological, legal, and environmental factors shaping the company. Ideal for investors and strategists, it’s fully editable and actionable for reports or pitches. Purchase the full report to download immediate, in-depth findings and seize opportunities before competitors.

Political factors

Data sovereignty policies

With GDPR in force across 27 EU states and more than 60 countries having data localization rules by 2024, Ipsos—active in 90+ markets—must host and process citizen data locally, raising costs and slowing delivery. Divergent regimes complicate cross‑market benchmarking; proactive compliance design and careful vendor selection reduce risk of project disruption.

Election cycles volatility

Election cycles spike demand for polling and opinion research while raising reputational risk; Ipsos, with roughly EUR 2.5bn revenue and ~19,000 staff in 2024, must scale quickly to capture higher short‑term volumes. Rapid shifts in public funding and messaging constraints can upend project pipelines, so robust forecasting for capacity and QA for fast fieldwork are essential. Strict neutrality policies and scenario planning stabilize revenue amid political churn.

Public sector procurement

Winning government tenders demands certifications, transparent processes and price competitiveness; OECD estimates public procurement equals about 12% of GDP in member countries, making it strategically material. Budget freezes or stimulus programs can swing volumes across policy areas, while contracting cycles often exceed 12 months so early engagement and framework agreements (covering ~30% of spend in some EU markets) matter. Strong local credentials markedly improve award probabilities in regulated markets.

Geopolitical fragmentation

Geopolitical fragmentation—rising sanctions and trade restrictions—undermines multinational samples and panels and can force field operations to be limited or censored in sensitive jurisdictions; Ipsos, active in 90+ markets with ~18,000 employees, must diversify suppliers and shift between CATI, face-to-face and online by country while enforcing clear risk protocols to protect staff and respondents.

- diversify suppliers across 90+ markets

- use CATI/online hybrids by country

- implement clear staff/respondent risk protocols

- monitor sanctions and trade restrictions continuously

Trust in institutions

Political polarization depresses respondent honesty (estimated 15% increase in misreporting) and lowers web survey response rates to about 8% in 2024; Ipsos must stress methodological transparency to sustain credibility. Third-party validation and open-data notes—citing 42% public trust in institutions (Ipsos 2024)—bolster stakeholder confidence and consistent disclosure reduces bias accusations.

- 15% estimated rise in misreporting due to polarization

- 8% average web survey response rate (2024)

- 42% public trust in institutions (Ipsos 2024)

- Third-party validation + open data = higher stakeholder trust

GDPR data localization raises hosting costs; elections spike demand as web response falls to 8%

GDPR (27 EU states) and 60+ countries with data localization (2024) raise hosting costs for Ipsos (90+ markets, EUR 2.5bn rev, ~19,000 staff, 2024). Election cycles spike polling demand but increase reputational and capacity risk; procurement (~12% GDP) drives long sales cycles. Polarization cuts web response to ~8% and boosts misreporting ~15%, while institutional trust ~42% (Ipsos 2024).

| Metric | Value | Year/Source |

|---|---|---|

| Markets | 90+ | Ipsos 2024 |

| Revenue | EUR 2.5bn | Ipsos 2024 |

| Web response | 8% | 2024 |

| Misreporting | +15% | Estimate 2024 |

What is included in the product

Explores how macro-environmental forces uniquely impact Ipsos across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to highlight risks and opportunities for executives and investors.

A concise, visually segmented Ipsos PESTLE summary that’s easily editable and shareable for fast alignment in meetings, presentations, or client reports.

Economic factors

Client budget cycles

Client marketing and insights budgets track GDP cycles; IMF projected global growth of 3.2% in 2024 and 3.0% in 2025, so spend volatility persists. In downturns clients often cut discretionary research or migrate to cheaper automated tools. Ipsos defends ROI with longitudinal panels and mixed methods that justify higher ARPU. Expanding into public and social sectors smooths revenue through countercyclical contracts.

Pricing pressure

Commoditization of basic surveys is compressing margins in a global market research industry of roughly $80 billion (ESOMAR 2023), while automated platforms and DIY tools heighten client price sensitivity. Ipsos must pivot to advanced analytics, sector expertise and outcome-linked offerings to defend pricing. Implementing tiered products and subscription models can stabilize ARPU and reduce churn.

Currency fluctuations

Global operations in 90+ markets expose Ipsos to FX risk on revenues and costs; Ipsos reported roughly €2.0bn revenue in 2023, so currency swings materially affect top-line translation. Mismatches between fieldwork expenses (often local currencies) and client billing currencies compress margins in volatile FX periods. Hedging programs and shifting to local cost bases reduce volatility, while transparent FX clauses in contracts protect project profitability.

Emerging market growth

Emerging market growth fuels demand for brand and retail insights as rising middle classes boost spend; Ipsos' footprint in 90+ countries captures this trend. Infrastructure and panel quality remain uneven across markets, but local partnerships and mobile-first methodologies enable rapid scale. Country risk-adjusted pricing (typical risk premia 3–8%) helps protect returns.

- Reach: 90+ markets

- Mobile-first scaling

- Panel variance: high

- Risk premia: 3–8%

Industry mix shifts

Industry mix shifts favor tech, healthcare and public-sector projects that show more resilient research spend versus cyclical CPG work; aligning vertical practices to those high-growth sectors raises utilization and billability. Thought leadership and proprietary benchmarks attract premium clients and pricing power. A balanced portfolio reduces client concentration risk and revenue volatility.

- sector_resilience

- utilization_gain

- premium_pricing

- concentration_reduction

GDPR data localization raises hosting costs; elections spike demand as web response falls to 8%

Client spend tracks GDP (IMF 2024 3.2%, 2025 3.0%), so research budgets remain volatile; Ipsos defends ARPU via panels and mixed methods and expands public/social work to smooth revenues. Commoditization and DIY tools compress margins in a $80bn market (ESOMAR 2023); move to advanced analytics and subscription tiers. FX exposure (90+ markets) and local cost mismatches require hedging and local pricing (risk premia 3–8%).

| Metric | Value |

|---|---|

| IMF global growth | 3.2% (2024), 3.0% (2025) |

| Market size | $80bn (ESOMAR 2023) |

| Ipsos revenue | €2.0bn (2023) |

| Markets | 90+ |

| Risk premia | 3–8% |

What You See Is What You Get

Ipsos PESTLE Analysis

The preview shown is the exact Ipsos PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content, layout, and structure are identical to the downloadable file. After payment you’ll instantly obtain this same finished document.

Your Shortcut to Market Insight Starts Here

Gain strategic foresight with our Ipsos PESTLE Analysis—concise, expert-reviewed insights into political, economic, social, technological, legal, and environmental factors shaping the company. Ideal for investors and strategists, it’s fully editable and actionable for reports or pitches. Purchase the full report to download immediate, in-depth findings and seize opportunities before competitors.

Political factors

Data sovereignty policies

With GDPR in force across 27 EU states and more than 60 countries having data localization rules by 2024, Ipsos—active in 90+ markets—must host and process citizen data locally, raising costs and slowing delivery. Divergent regimes complicate cross‑market benchmarking; proactive compliance design and careful vendor selection reduce risk of project disruption.

Election cycles volatility

Election cycles spike demand for polling and opinion research while raising reputational risk; Ipsos, with roughly EUR 2.5bn revenue and ~19,000 staff in 2024, must scale quickly to capture higher short‑term volumes. Rapid shifts in public funding and messaging constraints can upend project pipelines, so robust forecasting for capacity and QA for fast fieldwork are essential. Strict neutrality policies and scenario planning stabilize revenue amid political churn.

Public sector procurement

Winning government tenders demands certifications, transparent processes and price competitiveness; OECD estimates public procurement equals about 12% of GDP in member countries, making it strategically material. Budget freezes or stimulus programs can swing volumes across policy areas, while contracting cycles often exceed 12 months so early engagement and framework agreements (covering ~30% of spend in some EU markets) matter. Strong local credentials markedly improve award probabilities in regulated markets.

Geopolitical fragmentation

Geopolitical fragmentation—rising sanctions and trade restrictions—undermines multinational samples and panels and can force field operations to be limited or censored in sensitive jurisdictions; Ipsos, active in 90+ markets with ~18,000 employees, must diversify suppliers and shift between CATI, face-to-face and online by country while enforcing clear risk protocols to protect staff and respondents.

- diversify suppliers across 90+ markets

- use CATI/online hybrids by country

- implement clear staff/respondent risk protocols

- monitor sanctions and trade restrictions continuously

Trust in institutions

Political polarization depresses respondent honesty (estimated 15% increase in misreporting) and lowers web survey response rates to about 8% in 2024; Ipsos must stress methodological transparency to sustain credibility. Third-party validation and open-data notes—citing 42% public trust in institutions (Ipsos 2024)—bolster stakeholder confidence and consistent disclosure reduces bias accusations.

- 15% estimated rise in misreporting due to polarization

- 8% average web survey response rate (2024)

- 42% public trust in institutions (Ipsos 2024)

- Third-party validation + open data = higher stakeholder trust

GDPR data localization raises hosting costs; elections spike demand as web response falls to 8%

GDPR (27 EU states) and 60+ countries with data localization (2024) raise hosting costs for Ipsos (90+ markets, EUR 2.5bn rev, ~19,000 staff, 2024). Election cycles spike polling demand but increase reputational and capacity risk; procurement (~12% GDP) drives long sales cycles. Polarization cuts web response to ~8% and boosts misreporting ~15%, while institutional trust ~42% (Ipsos 2024).

| Metric | Value | Year/Source |

|---|---|---|

| Markets | 90+ | Ipsos 2024 |

| Revenue | EUR 2.5bn | Ipsos 2024 |

| Web response | 8% | 2024 |

| Misreporting | +15% | Estimate 2024 |

What is included in the product

Explores how macro-environmental forces uniquely impact Ipsos across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to highlight risks and opportunities for executives and investors.

A concise, visually segmented Ipsos PESTLE summary that’s easily editable and shareable for fast alignment in meetings, presentations, or client reports.

Economic factors

Client budget cycles

Client marketing and insights budgets track GDP cycles; IMF projected global growth of 3.2% in 2024 and 3.0% in 2025, so spend volatility persists. In downturns clients often cut discretionary research or migrate to cheaper automated tools. Ipsos defends ROI with longitudinal panels and mixed methods that justify higher ARPU. Expanding into public and social sectors smooths revenue through countercyclical contracts.

Pricing pressure

Commoditization of basic surveys is compressing margins in a global market research industry of roughly $80 billion (ESOMAR 2023), while automated platforms and DIY tools heighten client price sensitivity. Ipsos must pivot to advanced analytics, sector expertise and outcome-linked offerings to defend pricing. Implementing tiered products and subscription models can stabilize ARPU and reduce churn.

Currency fluctuations

Global operations in 90+ markets expose Ipsos to FX risk on revenues and costs; Ipsos reported roughly €2.0bn revenue in 2023, so currency swings materially affect top-line translation. Mismatches between fieldwork expenses (often local currencies) and client billing currencies compress margins in volatile FX periods. Hedging programs and shifting to local cost bases reduce volatility, while transparent FX clauses in contracts protect project profitability.

Emerging market growth

Emerging market growth fuels demand for brand and retail insights as rising middle classes boost spend; Ipsos' footprint in 90+ countries captures this trend. Infrastructure and panel quality remain uneven across markets, but local partnerships and mobile-first methodologies enable rapid scale. Country risk-adjusted pricing (typical risk premia 3–8%) helps protect returns.

- Reach: 90+ markets

- Mobile-first scaling

- Panel variance: high

- Risk premia: 3–8%

Industry mix shifts

Industry mix shifts favor tech, healthcare and public-sector projects that show more resilient research spend versus cyclical CPG work; aligning vertical practices to those high-growth sectors raises utilization and billability. Thought leadership and proprietary benchmarks attract premium clients and pricing power. A balanced portfolio reduces client concentration risk and revenue volatility.

- sector_resilience

- utilization_gain

- premium_pricing

- concentration_reduction

GDPR data localization raises hosting costs; elections spike demand as web response falls to 8%

Client spend tracks GDP (IMF 2024 3.2%, 2025 3.0%), so research budgets remain volatile; Ipsos defends ARPU via panels and mixed methods and expands public/social work to smooth revenues. Commoditization and DIY tools compress margins in a $80bn market (ESOMAR 2023); move to advanced analytics and subscription tiers. FX exposure (90+ markets) and local cost mismatches require hedging and local pricing (risk premia 3–8%).

| Metric | Value |

|---|---|

| IMF global growth | 3.2% (2024), 3.0% (2025) |

| Market size | $80bn (ESOMAR 2023) |

| Ipsos revenue | €2.0bn (2023) |

| Markets | 90+ |

| Risk premia | 3–8% |

What You See Is What You Get

Ipsos PESTLE Analysis

The preview shown is the exact Ipsos PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content, layout, and structure are identical to the downloadable file. After payment you’ll instantly obtain this same finished document.

Description

Your Shortcut to Market Insight Starts Here

Gain strategic foresight with our Ipsos PESTLE Analysis—concise, expert-reviewed insights into political, economic, social, technological, legal, and environmental factors shaping the company. Ideal for investors and strategists, it’s fully editable and actionable for reports or pitches. Purchase the full report to download immediate, in-depth findings and seize opportunities before competitors.

Political factors

Data sovereignty policies

With GDPR in force across 27 EU states and more than 60 countries having data localization rules by 2024, Ipsos—active in 90+ markets—must host and process citizen data locally, raising costs and slowing delivery. Divergent regimes complicate cross‑market benchmarking; proactive compliance design and careful vendor selection reduce risk of project disruption.

Election cycles volatility

Election cycles spike demand for polling and opinion research while raising reputational risk; Ipsos, with roughly EUR 2.5bn revenue and ~19,000 staff in 2024, must scale quickly to capture higher short‑term volumes. Rapid shifts in public funding and messaging constraints can upend project pipelines, so robust forecasting for capacity and QA for fast fieldwork are essential. Strict neutrality policies and scenario planning stabilize revenue amid political churn.

Public sector procurement

Winning government tenders demands certifications, transparent processes and price competitiveness; OECD estimates public procurement equals about 12% of GDP in member countries, making it strategically material. Budget freezes or stimulus programs can swing volumes across policy areas, while contracting cycles often exceed 12 months so early engagement and framework agreements (covering ~30% of spend in some EU markets) matter. Strong local credentials markedly improve award probabilities in regulated markets.

Geopolitical fragmentation

Geopolitical fragmentation—rising sanctions and trade restrictions—undermines multinational samples and panels and can force field operations to be limited or censored in sensitive jurisdictions; Ipsos, active in 90+ markets with ~18,000 employees, must diversify suppliers and shift between CATI, face-to-face and online by country while enforcing clear risk protocols to protect staff and respondents.

- diversify suppliers across 90+ markets

- use CATI/online hybrids by country

- implement clear staff/respondent risk protocols

- monitor sanctions and trade restrictions continuously

Trust in institutions

Political polarization depresses respondent honesty (estimated 15% increase in misreporting) and lowers web survey response rates to about 8% in 2024; Ipsos must stress methodological transparency to sustain credibility. Third-party validation and open-data notes—citing 42% public trust in institutions (Ipsos 2024)—bolster stakeholder confidence and consistent disclosure reduces bias accusations.

- 15% estimated rise in misreporting due to polarization

- 8% average web survey response rate (2024)

- 42% public trust in institutions (Ipsos 2024)

- Third-party validation + open data = higher stakeholder trust

GDPR data localization raises hosting costs; elections spike demand as web response falls to 8%

GDPR (27 EU states) and 60+ countries with data localization (2024) raise hosting costs for Ipsos (90+ markets, EUR 2.5bn rev, ~19,000 staff, 2024). Election cycles spike polling demand but increase reputational and capacity risk; procurement (~12% GDP) drives long sales cycles. Polarization cuts web response to ~8% and boosts misreporting ~15%, while institutional trust ~42% (Ipsos 2024).

| Metric | Value | Year/Source |

|---|---|---|

| Markets | 90+ | Ipsos 2024 |

| Revenue | EUR 2.5bn | Ipsos 2024 |

| Web response | 8% | 2024 |

| Misreporting | +15% | Estimate 2024 |

What is included in the product

Explores how macro-environmental forces uniquely impact Ipsos across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to highlight risks and opportunities for executives and investors.

A concise, visually segmented Ipsos PESTLE summary that’s easily editable and shareable for fast alignment in meetings, presentations, or client reports.

Economic factors

Client budget cycles

Client marketing and insights budgets track GDP cycles; IMF projected global growth of 3.2% in 2024 and 3.0% in 2025, so spend volatility persists. In downturns clients often cut discretionary research or migrate to cheaper automated tools. Ipsos defends ROI with longitudinal panels and mixed methods that justify higher ARPU. Expanding into public and social sectors smooths revenue through countercyclical contracts.

Pricing pressure

Commoditization of basic surveys is compressing margins in a global market research industry of roughly $80 billion (ESOMAR 2023), while automated platforms and DIY tools heighten client price sensitivity. Ipsos must pivot to advanced analytics, sector expertise and outcome-linked offerings to defend pricing. Implementing tiered products and subscription models can stabilize ARPU and reduce churn.

Currency fluctuations

Global operations in 90+ markets expose Ipsos to FX risk on revenues and costs; Ipsos reported roughly €2.0bn revenue in 2023, so currency swings materially affect top-line translation. Mismatches between fieldwork expenses (often local currencies) and client billing currencies compress margins in volatile FX periods. Hedging programs and shifting to local cost bases reduce volatility, while transparent FX clauses in contracts protect project profitability.

Emerging market growth

Emerging market growth fuels demand for brand and retail insights as rising middle classes boost spend; Ipsos' footprint in 90+ countries captures this trend. Infrastructure and panel quality remain uneven across markets, but local partnerships and mobile-first methodologies enable rapid scale. Country risk-adjusted pricing (typical risk premia 3–8%) helps protect returns.

- Reach: 90+ markets

- Mobile-first scaling

- Panel variance: high

- Risk premia: 3–8%

Industry mix shifts

Industry mix shifts favor tech, healthcare and public-sector projects that show more resilient research spend versus cyclical CPG work; aligning vertical practices to those high-growth sectors raises utilization and billability. Thought leadership and proprietary benchmarks attract premium clients and pricing power. A balanced portfolio reduces client concentration risk and revenue volatility.

- sector_resilience

- utilization_gain

- premium_pricing

- concentration_reduction

GDPR data localization raises hosting costs; elections spike demand as web response falls to 8%

Client spend tracks GDP (IMF 2024 3.2%, 2025 3.0%), so research budgets remain volatile; Ipsos defends ARPU via panels and mixed methods and expands public/social work to smooth revenues. Commoditization and DIY tools compress margins in a $80bn market (ESOMAR 2023); move to advanced analytics and subscription tiers. FX exposure (90+ markets) and local cost mismatches require hedging and local pricing (risk premia 3–8%).

| Metric | Value |

|---|---|

| IMF global growth | 3.2% (2024), 3.0% (2025) |

| Market size | $80bn (ESOMAR 2023) |

| Ipsos revenue | €2.0bn (2023) |

| Markets | 90+ |

| Risk premia | 3–8% |

What You See Is What You Get

Ipsos PESTLE Analysis

The preview shown is the exact Ipsos PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content, layout, and structure are identical to the downloadable file. After payment you’ll instantly obtain this same finished document.