Ishizuka Glass Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

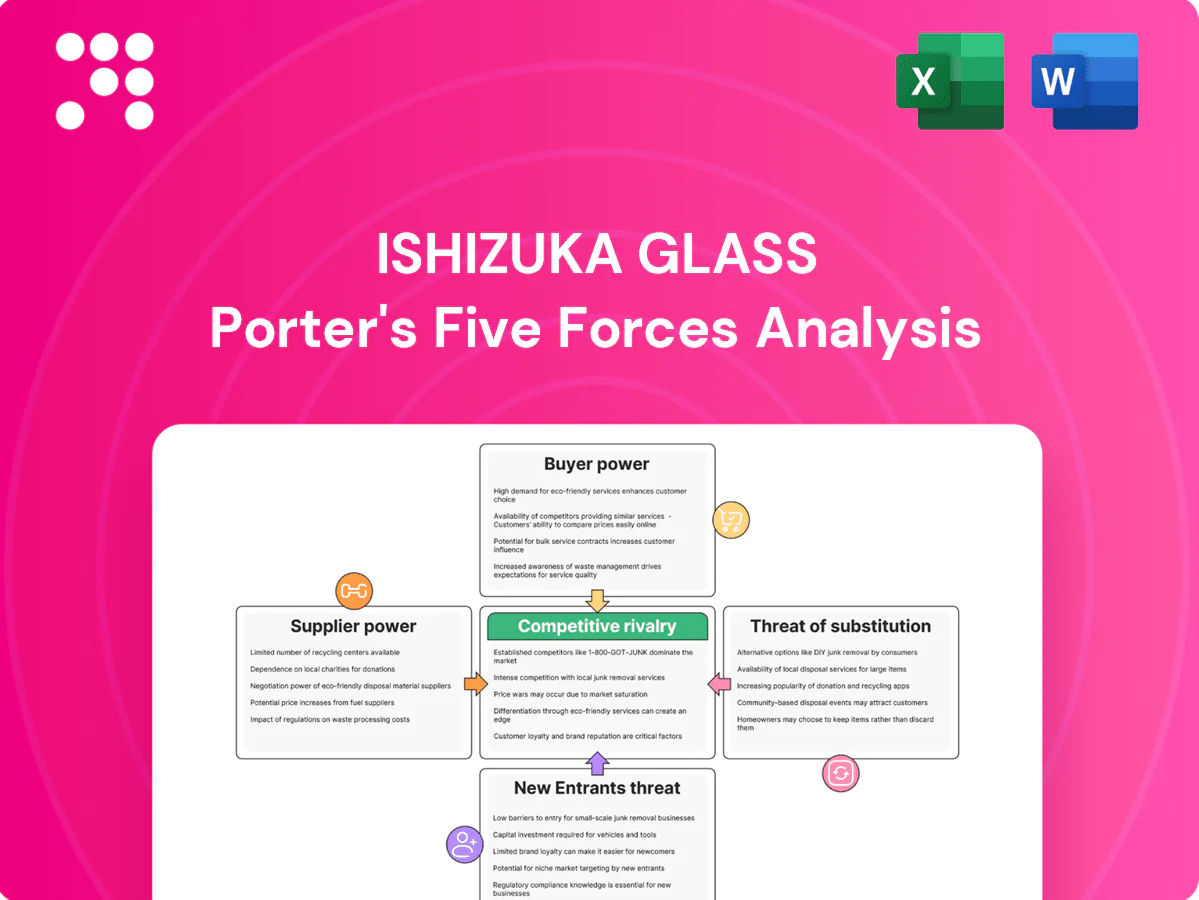

This snapshot highlights Ishizuka Glass’s competitive landscape—supplier leverage, buyer power, incumbent rivalry, and substitution risk—at a glance. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Ishizuka Glass. Get the consultant-grade report to inform investment decisions, strategy, or presentations.

Suppliers Bargaining Power

Concentrated raw materials

Glass production depends on high-purity silica sand, soda ash, limestone and cullet sourced from a limited pool of qualified suppliers, and purity/consistency needs narrow suppliers further. In 2024, regional shortages and logistics shocks tightened access to high-grade silica, lifting supplier leverage on price and contract terms. This concentration increases cost volatility and reduces Ishizuka Glasss bargaining power with vendors.

Energy dependency

Melting furnaces are highly energy-intensive, making Ishizuka Glass sensitive to fuel and electricity price swings; in 2024 energy cost volatility increased supplier leverage. Utilities and LNG suppliers can pass through higher costs in volatile markets, while long-term supply contracts improve price certainty but reduce operational flexibility. Carbon pricing and 2024 energy policy shifts further amplify supplier influence on margins.

Specialty plastics resins

Specialty plastics resins for Ishizuka Glass are concentrated among petrochemical majors, which control over 50% of global high-spec grade capacity, limiting supplier alternatives. Certification and tight performance specs make switching costly and slow. Feedstock-driven cycles drove resin price swings of about ±20% between 2022–24, amplifying pass-through. This concentration and volatility elevate bargaining power for high-spec resin providers.

Molds, refractories, and machinery

Precision molds, forming machines and refractory bricks are supplied by specialized OEMs with typical lead times of 6–12 months, creating strong switching frictions; maintenance parts and custom tooling further lock in vendors, enabling suppliers to extract value through service, spares and upgrade pricing.

- Specialized OEM supply

- 6–12 month lead times

- Customization = switching cost

- Spare parts lock-in

- Revenue from service/upgrades

Recycled cullet and sustainability inputs

High cullet ratios lower melting energy and CO2: roughly every 10% cullet can cut furnace energy by about 2–3% and CO2 emissions materially, but reliable volumes hinge on municipal collection quality and sorting yields. Competing demand for premium, food‑grade cullet tightens supply and lifts prices, while specialized additives and coatings for lightweighting remain niche, concentrated inputs that boost supplier bargaining power in green materials.

- Cullet energy/CO2 benefits: ~2–3% energy saved per 10% cullet

- Municipal collection quality = primary volume constraint

- Premium cullet demand tightens supply, raises prices

- Lightweighting additives/coatings are niche, increasing supplier clout

Concentrated suppliers, ±20% resin swings and long OEM lead times tighten 2024 margins

Supplier base is concentrated for high‑purity silica, specialty resins and OEM equipment, limiting alternatives and raising switching costs. 2024 saw tighter access to high‑grade silica and higher energy price volatility, reducing Ishizuka Glasss negotiating leverage; resins swung ~±20% 2022–24. OEM lead times 6–12 months and cullet limits (10% cullet ≈2–3% energy cut) further strengthen supplier power.

| Input | Market feature | 2024 impact |

|---|---|---|

| Silica | Concentrated, purity‑sensitive | Tighter access in 2024 |

| Energy | High volatility | Higher supplier leverage 2024 |

| Resins | Concentrated capacity | Price swings ~±20% (2022–24) |

What is included in the product

Tailored Porter's Five Forces for Ishizuka Glass uncovering competitive intensity, buyer/supplier power, substitute threats, and entry barriers, with strategic commentary on disruptive forces and market positioning.

Ishizuka Glass Porter's Five Forces one-sheet distills competitive pressures into a clear radar chart and editable scorecard—ideal for swift strategic decisions, slide-ready summaries, and easy scenario swaps without macros.

Customers Bargaining Power

Consolidated beverage and food clients

Consolidated FMCG and beverage bottlers such as PepsiCo (2024 net revenue ~86 billion USD) and Coca‑Cola (~44 billion USD in 2024) extract strong concessions on price and service from glass suppliers. Their scale enables multi‑sourcing and reverse auctions, and the ability to reallocate volumes across regions amplifies buyer power. For Ishizuka Glass this concentration compresses margins and forces capex alignment with major clients.

Low differentiation in commodity SKUs

Standard bottles and jars are highly price-sensitive and largely comparable across vendors, with the global glass packaging market ~USD 58 billion (2023), intensifying commodity competition. Switching costs are moderate once molds and regulatory approvals are aligned, letting buyers extract concessions. To blunt price pressure buyers demand value-adds—custom coatings, quick lead times, or sustainability certifications—to protect margins.

Specification lock-in and quality assurance

For pharma, baby food and premium beverages Ishizuka faces stringent qualification regimes—technical, regulatory and mold-specific requirements that materially raise switching costs; long validation cycles, typically 6–18 months, blunt immediate buyer leverage. These barriers concentrate power with qualified suppliers, allowing Ishizuka in 2024 to better defend premium pricing and sustain margins.

Demand volatility and inventory terms

Demand seasonality and promotion-driven spikes shift inventory risk to Ishizuka Glass suppliers, prompting buyers in 2024 to increasingly demand VMI, shorter lead times and contractual penalties; working-capital terms (payment days, consignment stock) became explicit negotiation levers, strengthening buyer bargaining power and margin pressure.

- VMI demand up (2024): ~60% of key OEM buyers

- Payment-term leverage: longer DPO requests, shorter DSO

- Promotional spikes drive inventory stockouts and penalties

Sustainability and design requirements

Customers increasingly demand lightweighting, recycled content and eco-labels, driven by 2024 EU and OEM sustainability targets and a reported 35% year‑on‑year rise in supplier eco-requests. Compliance investment often shifts costs onto Ishizuka, yet co-development projects embed the company in customer roadmaps and reduce pure price leverage. This duality turns price bargaining into partnership negotiation.

- Customer demand: lightweighting, recycled content, eco-labels

- 2024 trend: +35% supplier eco-requests

- Cost shift: compliance capital borne by supplier

- Counterweight: co-development = roadmap lock‑in

Buyer power squeezes glass margins; VMI and eco demands raise supplier costs

Large FMCG buyers (PepsiCo rev ~86bn USD, Coca‑Cola ~44bn USD in 2024) exert strong price and terms pressure via multi‑sourcing and reverse auctions, compressing Ishizuka Glass margins. Commodity nature of bottles (global glass packaging ~58bn USD in 2023) and moderate switching costs boost buyer leverage, but pharma/premium segments with 6–18 month qualifications protect pricing. Sustainability and VMI trends (2024: ~60% key OEMs demand VMI; +35% eco‑requests) shift compliance costs to suppliers while creating co‑development lock‑ins.

| Metric | Value |

|---|---|

| PepsiCo 2024 rev | ~86bn USD |

| Coca‑Cola 2024 rev | ~44bn USD |

| Glass market (2023) | ~58bn USD |

| VMI demand (2024) | ~60% key OEMs |

| Eco‑requests change (2024) | +35% |

Same Document Delivered

Ishizuka Glass Porter's Five Forces Analysis

This preview shows the Ishizuka Glass Porter’s Five Forces analysis exactly as delivered—no placeholders or excerpts. The document displayed is the full, professionally formatted file you’ll receive immediately after purchase. You’ll get instant access to this same analysis, ready for download and use. No mockups, no samples—what you see is what you get.

A Must-Have Tool for Decision-Makers

This snapshot highlights Ishizuka Glass’s competitive landscape—supplier leverage, buyer power, incumbent rivalry, and substitution risk—at a glance. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Ishizuka Glass. Get the consultant-grade report to inform investment decisions, strategy, or presentations.

Suppliers Bargaining Power

Concentrated raw materials

Glass production depends on high-purity silica sand, soda ash, limestone and cullet sourced from a limited pool of qualified suppliers, and purity/consistency needs narrow suppliers further. In 2024, regional shortages and logistics shocks tightened access to high-grade silica, lifting supplier leverage on price and contract terms. This concentration increases cost volatility and reduces Ishizuka Glasss bargaining power with vendors.

Energy dependency

Melting furnaces are highly energy-intensive, making Ishizuka Glass sensitive to fuel and electricity price swings; in 2024 energy cost volatility increased supplier leverage. Utilities and LNG suppliers can pass through higher costs in volatile markets, while long-term supply contracts improve price certainty but reduce operational flexibility. Carbon pricing and 2024 energy policy shifts further amplify supplier influence on margins.

Specialty plastics resins

Specialty plastics resins for Ishizuka Glass are concentrated among petrochemical majors, which control over 50% of global high-spec grade capacity, limiting supplier alternatives. Certification and tight performance specs make switching costly and slow. Feedstock-driven cycles drove resin price swings of about ±20% between 2022–24, amplifying pass-through. This concentration and volatility elevate bargaining power for high-spec resin providers.

Molds, refractories, and machinery

Precision molds, forming machines and refractory bricks are supplied by specialized OEMs with typical lead times of 6–12 months, creating strong switching frictions; maintenance parts and custom tooling further lock in vendors, enabling suppliers to extract value through service, spares and upgrade pricing.

- Specialized OEM supply

- 6–12 month lead times

- Customization = switching cost

- Spare parts lock-in

- Revenue from service/upgrades

Recycled cullet and sustainability inputs

High cullet ratios lower melting energy and CO2: roughly every 10% cullet can cut furnace energy by about 2–3% and CO2 emissions materially, but reliable volumes hinge on municipal collection quality and sorting yields. Competing demand for premium, food‑grade cullet tightens supply and lifts prices, while specialized additives and coatings for lightweighting remain niche, concentrated inputs that boost supplier bargaining power in green materials.

- Cullet energy/CO2 benefits: ~2–3% energy saved per 10% cullet

- Municipal collection quality = primary volume constraint

- Premium cullet demand tightens supply, raises prices

- Lightweighting additives/coatings are niche, increasing supplier clout

Concentrated suppliers, ±20% resin swings and long OEM lead times tighten 2024 margins

Supplier base is concentrated for high‑purity silica, specialty resins and OEM equipment, limiting alternatives and raising switching costs. 2024 saw tighter access to high‑grade silica and higher energy price volatility, reducing Ishizuka Glasss negotiating leverage; resins swung ~±20% 2022–24. OEM lead times 6–12 months and cullet limits (10% cullet ≈2–3% energy cut) further strengthen supplier power.

| Input | Market feature | 2024 impact |

|---|---|---|

| Silica | Concentrated, purity‑sensitive | Tighter access in 2024 |

| Energy | High volatility | Higher supplier leverage 2024 |

| Resins | Concentrated capacity | Price swings ~±20% (2022–24) |

What is included in the product

Tailored Porter's Five Forces for Ishizuka Glass uncovering competitive intensity, buyer/supplier power, substitute threats, and entry barriers, with strategic commentary on disruptive forces and market positioning.

Ishizuka Glass Porter's Five Forces one-sheet distills competitive pressures into a clear radar chart and editable scorecard—ideal for swift strategic decisions, slide-ready summaries, and easy scenario swaps without macros.

Customers Bargaining Power

Consolidated beverage and food clients

Consolidated FMCG and beverage bottlers such as PepsiCo (2024 net revenue ~86 billion USD) and Coca‑Cola (~44 billion USD in 2024) extract strong concessions on price and service from glass suppliers. Their scale enables multi‑sourcing and reverse auctions, and the ability to reallocate volumes across regions amplifies buyer power. For Ishizuka Glass this concentration compresses margins and forces capex alignment with major clients.

Low differentiation in commodity SKUs

Standard bottles and jars are highly price-sensitive and largely comparable across vendors, with the global glass packaging market ~USD 58 billion (2023), intensifying commodity competition. Switching costs are moderate once molds and regulatory approvals are aligned, letting buyers extract concessions. To blunt price pressure buyers demand value-adds—custom coatings, quick lead times, or sustainability certifications—to protect margins.

Specification lock-in and quality assurance

For pharma, baby food and premium beverages Ishizuka faces stringent qualification regimes—technical, regulatory and mold-specific requirements that materially raise switching costs; long validation cycles, typically 6–18 months, blunt immediate buyer leverage. These barriers concentrate power with qualified suppliers, allowing Ishizuka in 2024 to better defend premium pricing and sustain margins.

Demand volatility and inventory terms

Demand seasonality and promotion-driven spikes shift inventory risk to Ishizuka Glass suppliers, prompting buyers in 2024 to increasingly demand VMI, shorter lead times and contractual penalties; working-capital terms (payment days, consignment stock) became explicit negotiation levers, strengthening buyer bargaining power and margin pressure.

- VMI demand up (2024): ~60% of key OEM buyers

- Payment-term leverage: longer DPO requests, shorter DSO

- Promotional spikes drive inventory stockouts and penalties

Sustainability and design requirements

Customers increasingly demand lightweighting, recycled content and eco-labels, driven by 2024 EU and OEM sustainability targets and a reported 35% year‑on‑year rise in supplier eco-requests. Compliance investment often shifts costs onto Ishizuka, yet co-development projects embed the company in customer roadmaps and reduce pure price leverage. This duality turns price bargaining into partnership negotiation.

- Customer demand: lightweighting, recycled content, eco-labels

- 2024 trend: +35% supplier eco-requests

- Cost shift: compliance capital borne by supplier

- Counterweight: co-development = roadmap lock‑in

Buyer power squeezes glass margins; VMI and eco demands raise supplier costs

Large FMCG buyers (PepsiCo rev ~86bn USD, Coca‑Cola ~44bn USD in 2024) exert strong price and terms pressure via multi‑sourcing and reverse auctions, compressing Ishizuka Glass margins. Commodity nature of bottles (global glass packaging ~58bn USD in 2023) and moderate switching costs boost buyer leverage, but pharma/premium segments with 6–18 month qualifications protect pricing. Sustainability and VMI trends (2024: ~60% key OEMs demand VMI; +35% eco‑requests) shift compliance costs to suppliers while creating co‑development lock‑ins.

| Metric | Value |

|---|---|

| PepsiCo 2024 rev | ~86bn USD |

| Coca‑Cola 2024 rev | ~44bn USD |

| Glass market (2023) | ~58bn USD |

| VMI demand (2024) | ~60% key OEMs |

| Eco‑requests change (2024) | +35% |

Same Document Delivered

Ishizuka Glass Porter's Five Forces Analysis

This preview shows the Ishizuka Glass Porter’s Five Forces analysis exactly as delivered—no placeholders or excerpts. The document displayed is the full, professionally formatted file you’ll receive immediately after purchase. You’ll get instant access to this same analysis, ready for download and use. No mockups, no samples—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

This snapshot highlights Ishizuka Glass’s competitive landscape—supplier leverage, buyer power, incumbent rivalry, and substitution risk—at a glance. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Ishizuka Glass. Get the consultant-grade report to inform investment decisions, strategy, or presentations.

Suppliers Bargaining Power

Concentrated raw materials

Glass production depends on high-purity silica sand, soda ash, limestone and cullet sourced from a limited pool of qualified suppliers, and purity/consistency needs narrow suppliers further. In 2024, regional shortages and logistics shocks tightened access to high-grade silica, lifting supplier leverage on price and contract terms. This concentration increases cost volatility and reduces Ishizuka Glasss bargaining power with vendors.

Energy dependency

Melting furnaces are highly energy-intensive, making Ishizuka Glass sensitive to fuel and electricity price swings; in 2024 energy cost volatility increased supplier leverage. Utilities and LNG suppliers can pass through higher costs in volatile markets, while long-term supply contracts improve price certainty but reduce operational flexibility. Carbon pricing and 2024 energy policy shifts further amplify supplier influence on margins.

Specialty plastics resins

Specialty plastics resins for Ishizuka Glass are concentrated among petrochemical majors, which control over 50% of global high-spec grade capacity, limiting supplier alternatives. Certification and tight performance specs make switching costly and slow. Feedstock-driven cycles drove resin price swings of about ±20% between 2022–24, amplifying pass-through. This concentration and volatility elevate bargaining power for high-spec resin providers.

Molds, refractories, and machinery

Precision molds, forming machines and refractory bricks are supplied by specialized OEMs with typical lead times of 6–12 months, creating strong switching frictions; maintenance parts and custom tooling further lock in vendors, enabling suppliers to extract value through service, spares and upgrade pricing.

- Specialized OEM supply

- 6–12 month lead times

- Customization = switching cost

- Spare parts lock-in

- Revenue from service/upgrades

Recycled cullet and sustainability inputs

High cullet ratios lower melting energy and CO2: roughly every 10% cullet can cut furnace energy by about 2–3% and CO2 emissions materially, but reliable volumes hinge on municipal collection quality and sorting yields. Competing demand for premium, food‑grade cullet tightens supply and lifts prices, while specialized additives and coatings for lightweighting remain niche, concentrated inputs that boost supplier bargaining power in green materials.

- Cullet energy/CO2 benefits: ~2–3% energy saved per 10% cullet

- Municipal collection quality = primary volume constraint

- Premium cullet demand tightens supply, raises prices

- Lightweighting additives/coatings are niche, increasing supplier clout

Concentrated suppliers, ±20% resin swings and long OEM lead times tighten 2024 margins

Supplier base is concentrated for high‑purity silica, specialty resins and OEM equipment, limiting alternatives and raising switching costs. 2024 saw tighter access to high‑grade silica and higher energy price volatility, reducing Ishizuka Glasss negotiating leverage; resins swung ~±20% 2022–24. OEM lead times 6–12 months and cullet limits (10% cullet ≈2–3% energy cut) further strengthen supplier power.

| Input | Market feature | 2024 impact |

|---|---|---|

| Silica | Concentrated, purity‑sensitive | Tighter access in 2024 |

| Energy | High volatility | Higher supplier leverage 2024 |

| Resins | Concentrated capacity | Price swings ~±20% (2022–24) |

What is included in the product

Tailored Porter's Five Forces for Ishizuka Glass uncovering competitive intensity, buyer/supplier power, substitute threats, and entry barriers, with strategic commentary on disruptive forces and market positioning.

Ishizuka Glass Porter's Five Forces one-sheet distills competitive pressures into a clear radar chart and editable scorecard—ideal for swift strategic decisions, slide-ready summaries, and easy scenario swaps without macros.

Customers Bargaining Power

Consolidated beverage and food clients

Consolidated FMCG and beverage bottlers such as PepsiCo (2024 net revenue ~86 billion USD) and Coca‑Cola (~44 billion USD in 2024) extract strong concessions on price and service from glass suppliers. Their scale enables multi‑sourcing and reverse auctions, and the ability to reallocate volumes across regions amplifies buyer power. For Ishizuka Glass this concentration compresses margins and forces capex alignment with major clients.

Low differentiation in commodity SKUs

Standard bottles and jars are highly price-sensitive and largely comparable across vendors, with the global glass packaging market ~USD 58 billion (2023), intensifying commodity competition. Switching costs are moderate once molds and regulatory approvals are aligned, letting buyers extract concessions. To blunt price pressure buyers demand value-adds—custom coatings, quick lead times, or sustainability certifications—to protect margins.

Specification lock-in and quality assurance

For pharma, baby food and premium beverages Ishizuka faces stringent qualification regimes—technical, regulatory and mold-specific requirements that materially raise switching costs; long validation cycles, typically 6–18 months, blunt immediate buyer leverage. These barriers concentrate power with qualified suppliers, allowing Ishizuka in 2024 to better defend premium pricing and sustain margins.

Demand volatility and inventory terms

Demand seasonality and promotion-driven spikes shift inventory risk to Ishizuka Glass suppliers, prompting buyers in 2024 to increasingly demand VMI, shorter lead times and contractual penalties; working-capital terms (payment days, consignment stock) became explicit negotiation levers, strengthening buyer bargaining power and margin pressure.

- VMI demand up (2024): ~60% of key OEM buyers

- Payment-term leverage: longer DPO requests, shorter DSO

- Promotional spikes drive inventory stockouts and penalties

Sustainability and design requirements

Customers increasingly demand lightweighting, recycled content and eco-labels, driven by 2024 EU and OEM sustainability targets and a reported 35% year‑on‑year rise in supplier eco-requests. Compliance investment often shifts costs onto Ishizuka, yet co-development projects embed the company in customer roadmaps and reduce pure price leverage. This duality turns price bargaining into partnership negotiation.

- Customer demand: lightweighting, recycled content, eco-labels

- 2024 trend: +35% supplier eco-requests

- Cost shift: compliance capital borne by supplier

- Counterweight: co-development = roadmap lock‑in

Buyer power squeezes glass margins; VMI and eco demands raise supplier costs

Large FMCG buyers (PepsiCo rev ~86bn USD, Coca‑Cola ~44bn USD in 2024) exert strong price and terms pressure via multi‑sourcing and reverse auctions, compressing Ishizuka Glass margins. Commodity nature of bottles (global glass packaging ~58bn USD in 2023) and moderate switching costs boost buyer leverage, but pharma/premium segments with 6–18 month qualifications protect pricing. Sustainability and VMI trends (2024: ~60% key OEMs demand VMI; +35% eco‑requests) shift compliance costs to suppliers while creating co‑development lock‑ins.

| Metric | Value |

|---|---|

| PepsiCo 2024 rev | ~86bn USD |

| Coca‑Cola 2024 rev | ~44bn USD |

| Glass market (2023) | ~58bn USD |

| VMI demand (2024) | ~60% key OEMs |

| Eco‑requests change (2024) | +35% |

Same Document Delivered

Ishizuka Glass Porter's Five Forces Analysis

This preview shows the Ishizuka Glass Porter’s Five Forces analysis exactly as delivered—no placeholders or excerpts. The document displayed is the full, professionally formatted file you’ll receive immediately after purchase. You’ll get instant access to this same analysis, ready for download and use. No mockups, no samples—what you see is what you get.