Ishizuka Glass PESTLE Analysis

Skip the Research. Get the Strategy.

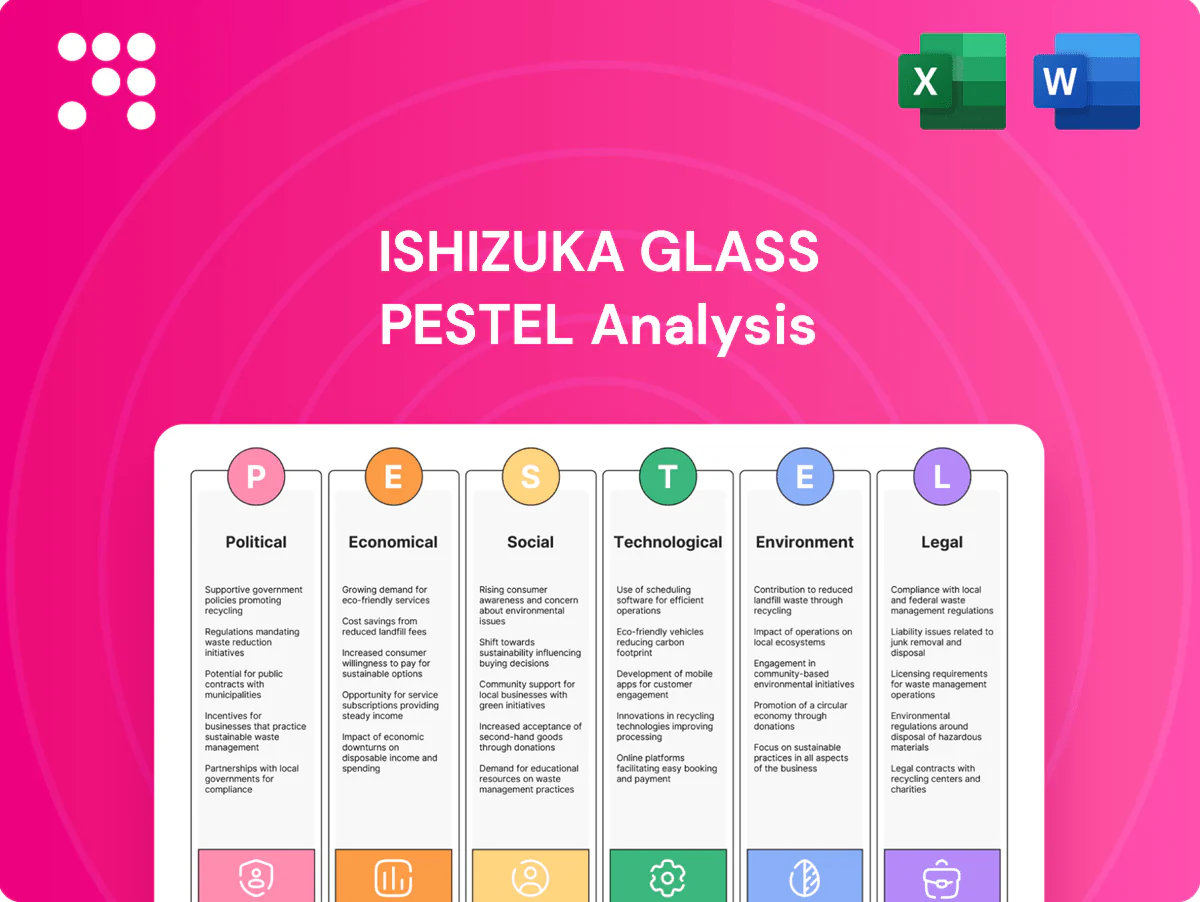

Unlock strategic clarity with our PESTLE Analysis of Ishizuka Glass—concise evaluation of political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it turns external trends into actionable insight. Buy the full report for the complete, downloadable analysis.

Political factors

Trade policy volatility

Shifts in tariffs on glass, plastics, soda ash and silica sand can swing input costs by up to 15% and force export repricing; Japan had about 20 FTAs/EPAs by 2024 easing market entry. U.S. and EU antidumping measures have periodically imposed duties that constrain shipments. Geopolitical tensions in 2024 raised freight lead times roughly 15–20% and energy costs, so proactive hedging of markets and suppliers mitigates shocks.

Energy and industrial policy

Japanese incentives for decarbonization, electrification and hydrogen—driven by the 2050 net‑zero goal and a 46–50% 2030 GHG target—can reduce furnace emissions long‑term. METI's GX initiatives and related financing (including a roughly ¥2 trillion GX fund) and green loans/subsidy schemes lower upfront capex for low‑carbon melting and waste‑heat recovery. Lack of a nationwide carbon price as of 2025 creates ROI timing uncertainty. Aligning Ishizuka Glass roadmaps with METI programs improves chances of securing grants and concessional finance.

Municipal recycling agendas

Local and national targets—the EU’s ~75% glass recycling goal for 2025 and Japan’s national recycling targets—directly affect cullet quality and volumes available to Ishizuka Glass. Strong municipal collection and DRS schemes can cut furnace energy ~2–3% per 10ppt increase in cullet share and lower CO2 accordingly, reducing raw material and energy costs. Divergent systems abroad (DRS vs curbside) force tailored packaging specs and supply-chain shifts, while municipality partnerships can secure steady cullet streams covering >30% of feedstock needs.

Public health and food security priorities

Governments increasingly mandate safe, tamper-evident food and beverage packaging, reinforcing Ishizuka Glass’s focus on compliant closures and barrier glass; the global food packaging market was about USD 387 billion in 2023 (Grand View Research). During crises many states kept packaging plants operational but imposed workforce mobility limits, shifting demand toward shelf-stable formats and accelerating orders for tamper-evident solutions.

- Essential designation: continuity of operations

- USD 387B market (2023)

- Higher demand for shelf-stable, tamper-evident packaging

- Compliance readiness = operational resilience

Localization and reshoring

Political pressure to localize beverage and pharma packaging is driving plant siting decisions; incentives for domestic production (eg US CHIPS Act funding ~280 billion USD) create opportunities but raise expectations of local-content rules (EU Critical Raw Materials Act, 2023). Regionalization lowers geopolitical transport risk and a multi-hub strategy improves resilience.

- Plant siting driven by localization

- Incentives raise domestic-opportunity but imply local-content

- Regionalization cuts transport/geopolitical risk

- Multi-hub strategy boosts supply resilience

Trade shifts, freight delays and ¥2T GX spur low-carbon capex amid localization mandates

Tariffs/antidumping and ~20 Japan FTAs (2024) shift input/export pricing (~±15%); 2024 geopolitical tensions raised freight lead times 15–20%. METI GX support (~¥2T) and 2030 GHG target (46–50%) push low‑carbon capex despite no national carbon price. Localization/recycling mandates affect siting and cullet supply.

| Metric | Value |

|---|---|

| Japan FTAs | ~20 |

| GX fund | ¥2T |

| Freight delays (2024) | 15–20% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Ishizuka Glass, with data-backed insights, region- and industry-specific examples, forward-looking scenario implications, and clean formatting to support executives, investors and strategists.

A concise, visually segmented PESTLE summary for Ishizuka Glass that’s easily droppable into presentations and shareable across teams, enabling quick alignment on external risks and market positioning while allowing editable notes for region- or product-specific context.

Economic factors

Energy price volatility

Glass melting depends heavily on electricity and gas, making margins sensitive to energy spikes — LNG spot (JKM) surged above $60/MMBtu in 2022 before averaging about $14/MMBtu in 2024, pressuring input costs. Long-term PPAs and furnace efficiency upgrades have been used to stabilize cashflow and cap volatility. Fuel switching to oxy-fuel or hybrid-electric furnaces cuts gas exposure, while robust pass-through clauses with FMCG clients remain critical to protect margins.

FX and yen dynamics

Yen weakness since 2023, with USD/JPY trading around 155–160 in mid‑2025, boosts Ishizuka Glass export competitiveness but raises costs for imported raw materials and resins priced in dollars. Strategic FX hedging smooths cash‑flow and operating earnings but cannot remove translation losses on consolidated results. Taking orders priced in local currencies reduces customer friction, while a balanced geographic revenue mix helps limit net FX swings.

Consumer demand cycles

Beverage, food and hospitality cycles strongly drive bottle and tableware volumes; the global glass packaging market was about USD 65 billion in 2023 with ~4% CAGR projected to 2028, reflecting steady demand for bottles. Premiumization has lifted glass mix and value-per-unit, with premium glass segments growing faster than commodity packs in 2023–24. Downturns shift volumes to lighter, cheaper packs, while on-premise recovery—restaurant sales near 90–95% of pre‑pandemic levels by 2024—aided tableware rebound. SKU agility helps protect plant utilization and margins amid these swings.

Raw materials and logistics

- Soda ash global output ~53 mt (2022)

- EU glass cullet recycling ~76%

- Freight volatility: ~70% drop from 2021 to 2024 peaks

- Nearshoring cuts logistics costs/emissions ~10–30%

Labor and productivity

Japan’s aging workforce tightens skilled labor supply in hot-end operations, with 65+ at about 29% of the population in 2024; shortages raise reliance on experienced operators. Automation and AI inspection raise throughput and cut defects (industry reports cite defect reductions of 20–30%), while ~3% nominal wage growth in 2024 pressures unit costs absent efficiency gains; targeted training and ergonomics boost retention.

- Aging workforce: 65+ ≈29% (2024)

- Defect reduction: AI/automation 20–30%

- Wage pressure: ≈3% nominal pay rise (2024)

- Retention: training + ergonomics lowers turnover

Trade shifts, freight delays and ¥2T GX spur low-carbon capex amid localization mandates

High energy intensity leaves margins exposed—JKM peaked >$60/MMBtu in 2022, averaged ~$14/MMBtu in 2024; PPAs, efficiency and fuel-switching reduce volatility. Yen ~155–160 (mid‑2025) aids exports but raises dollar‑priced input costs; FX hedges smooth cash flow. Global glass market ≈$65bn (2023) with ~4% CAGR to 2028; cullet, soda ash (≈53mt 2022) and freight swings drive unit costs.

| Metric | Value |

|---|---|

| JKM 2024 avg | $14/MMBtu |

| USD/JPY mid‑2025 | 155–160 |

| Glass market 2023 | $65bn |

| Soda ash 2022 | 53 mt |

Full Version Awaits

Ishizuka Glass PESTLE Analysis

The preview shown here is the exact Ishizuka Glass PESTLE document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental analysis with charts and citations as displayed. No placeholders or surprises; download this exact file immediately after payment.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Ishizuka Glass—concise evaluation of political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it turns external trends into actionable insight. Buy the full report for the complete, downloadable analysis.

Political factors

Trade policy volatility

Shifts in tariffs on glass, plastics, soda ash and silica sand can swing input costs by up to 15% and force export repricing; Japan had about 20 FTAs/EPAs by 2024 easing market entry. U.S. and EU antidumping measures have periodically imposed duties that constrain shipments. Geopolitical tensions in 2024 raised freight lead times roughly 15–20% and energy costs, so proactive hedging of markets and suppliers mitigates shocks.

Energy and industrial policy

Japanese incentives for decarbonization, electrification and hydrogen—driven by the 2050 net‑zero goal and a 46–50% 2030 GHG target—can reduce furnace emissions long‑term. METI's GX initiatives and related financing (including a roughly ¥2 trillion GX fund) and green loans/subsidy schemes lower upfront capex for low‑carbon melting and waste‑heat recovery. Lack of a nationwide carbon price as of 2025 creates ROI timing uncertainty. Aligning Ishizuka Glass roadmaps with METI programs improves chances of securing grants and concessional finance.

Municipal recycling agendas

Local and national targets—the EU’s ~75% glass recycling goal for 2025 and Japan’s national recycling targets—directly affect cullet quality and volumes available to Ishizuka Glass. Strong municipal collection and DRS schemes can cut furnace energy ~2–3% per 10ppt increase in cullet share and lower CO2 accordingly, reducing raw material and energy costs. Divergent systems abroad (DRS vs curbside) force tailored packaging specs and supply-chain shifts, while municipality partnerships can secure steady cullet streams covering >30% of feedstock needs.

Public health and food security priorities

Governments increasingly mandate safe, tamper-evident food and beverage packaging, reinforcing Ishizuka Glass’s focus on compliant closures and barrier glass; the global food packaging market was about USD 387 billion in 2023 (Grand View Research). During crises many states kept packaging plants operational but imposed workforce mobility limits, shifting demand toward shelf-stable formats and accelerating orders for tamper-evident solutions.

- Essential designation: continuity of operations

- USD 387B market (2023)

- Higher demand for shelf-stable, tamper-evident packaging

- Compliance readiness = operational resilience

Localization and reshoring

Political pressure to localize beverage and pharma packaging is driving plant siting decisions; incentives for domestic production (eg US CHIPS Act funding ~280 billion USD) create opportunities but raise expectations of local-content rules (EU Critical Raw Materials Act, 2023). Regionalization lowers geopolitical transport risk and a multi-hub strategy improves resilience.

- Plant siting driven by localization

- Incentives raise domestic-opportunity but imply local-content

- Regionalization cuts transport/geopolitical risk

- Multi-hub strategy boosts supply resilience

Trade shifts, freight delays and ¥2T GX spur low-carbon capex amid localization mandates

Tariffs/antidumping and ~20 Japan FTAs (2024) shift input/export pricing (~±15%); 2024 geopolitical tensions raised freight lead times 15–20%. METI GX support (~¥2T) and 2030 GHG target (46–50%) push low‑carbon capex despite no national carbon price. Localization/recycling mandates affect siting and cullet supply.

| Metric | Value |

|---|---|

| Japan FTAs | ~20 |

| GX fund | ¥2T |

| Freight delays (2024) | 15–20% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Ishizuka Glass, with data-backed insights, region- and industry-specific examples, forward-looking scenario implications, and clean formatting to support executives, investors and strategists.

A concise, visually segmented PESTLE summary for Ishizuka Glass that’s easily droppable into presentations and shareable across teams, enabling quick alignment on external risks and market positioning while allowing editable notes for region- or product-specific context.

Economic factors

Energy price volatility

Glass melting depends heavily on electricity and gas, making margins sensitive to energy spikes — LNG spot (JKM) surged above $60/MMBtu in 2022 before averaging about $14/MMBtu in 2024, pressuring input costs. Long-term PPAs and furnace efficiency upgrades have been used to stabilize cashflow and cap volatility. Fuel switching to oxy-fuel or hybrid-electric furnaces cuts gas exposure, while robust pass-through clauses with FMCG clients remain critical to protect margins.

FX and yen dynamics

Yen weakness since 2023, with USD/JPY trading around 155–160 in mid‑2025, boosts Ishizuka Glass export competitiveness but raises costs for imported raw materials and resins priced in dollars. Strategic FX hedging smooths cash‑flow and operating earnings but cannot remove translation losses on consolidated results. Taking orders priced in local currencies reduces customer friction, while a balanced geographic revenue mix helps limit net FX swings.

Consumer demand cycles

Beverage, food and hospitality cycles strongly drive bottle and tableware volumes; the global glass packaging market was about USD 65 billion in 2023 with ~4% CAGR projected to 2028, reflecting steady demand for bottles. Premiumization has lifted glass mix and value-per-unit, with premium glass segments growing faster than commodity packs in 2023–24. Downturns shift volumes to lighter, cheaper packs, while on-premise recovery—restaurant sales near 90–95% of pre‑pandemic levels by 2024—aided tableware rebound. SKU agility helps protect plant utilization and margins amid these swings.

Raw materials and logistics

- Soda ash global output ~53 mt (2022)

- EU glass cullet recycling ~76%

- Freight volatility: ~70% drop from 2021 to 2024 peaks

- Nearshoring cuts logistics costs/emissions ~10–30%

Labor and productivity

Japan’s aging workforce tightens skilled labor supply in hot-end operations, with 65+ at about 29% of the population in 2024; shortages raise reliance on experienced operators. Automation and AI inspection raise throughput and cut defects (industry reports cite defect reductions of 20–30%), while ~3% nominal wage growth in 2024 pressures unit costs absent efficiency gains; targeted training and ergonomics boost retention.

- Aging workforce: 65+ ≈29% (2024)

- Defect reduction: AI/automation 20–30%

- Wage pressure: ≈3% nominal pay rise (2024)

- Retention: training + ergonomics lowers turnover

Trade shifts, freight delays and ¥2T GX spur low-carbon capex amid localization mandates

High energy intensity leaves margins exposed—JKM peaked >$60/MMBtu in 2022, averaged ~$14/MMBtu in 2024; PPAs, efficiency and fuel-switching reduce volatility. Yen ~155–160 (mid‑2025) aids exports but raises dollar‑priced input costs; FX hedges smooth cash flow. Global glass market ≈$65bn (2023) with ~4% CAGR to 2028; cullet, soda ash (≈53mt 2022) and freight swings drive unit costs.

| Metric | Value |

|---|---|

| JKM 2024 avg | $14/MMBtu |

| USD/JPY mid‑2025 | 155–160 |

| Glass market 2023 | $65bn |

| Soda ash 2022 | 53 mt |

Full Version Awaits

Ishizuka Glass PESTLE Analysis

The preview shown here is the exact Ishizuka Glass PESTLE document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental analysis with charts and citations as displayed. No placeholders or surprises; download this exact file immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Ishizuka Glass—concise evaluation of political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it turns external trends into actionable insight. Buy the full report for the complete, downloadable analysis.

Political factors

Trade policy volatility

Shifts in tariffs on glass, plastics, soda ash and silica sand can swing input costs by up to 15% and force export repricing; Japan had about 20 FTAs/EPAs by 2024 easing market entry. U.S. and EU antidumping measures have periodically imposed duties that constrain shipments. Geopolitical tensions in 2024 raised freight lead times roughly 15–20% and energy costs, so proactive hedging of markets and suppliers mitigates shocks.

Energy and industrial policy

Japanese incentives for decarbonization, electrification and hydrogen—driven by the 2050 net‑zero goal and a 46–50% 2030 GHG target—can reduce furnace emissions long‑term. METI's GX initiatives and related financing (including a roughly ¥2 trillion GX fund) and green loans/subsidy schemes lower upfront capex for low‑carbon melting and waste‑heat recovery. Lack of a nationwide carbon price as of 2025 creates ROI timing uncertainty. Aligning Ishizuka Glass roadmaps with METI programs improves chances of securing grants and concessional finance.

Municipal recycling agendas

Local and national targets—the EU’s ~75% glass recycling goal for 2025 and Japan’s national recycling targets—directly affect cullet quality and volumes available to Ishizuka Glass. Strong municipal collection and DRS schemes can cut furnace energy ~2–3% per 10ppt increase in cullet share and lower CO2 accordingly, reducing raw material and energy costs. Divergent systems abroad (DRS vs curbside) force tailored packaging specs and supply-chain shifts, while municipality partnerships can secure steady cullet streams covering >30% of feedstock needs.

Public health and food security priorities

Governments increasingly mandate safe, tamper-evident food and beverage packaging, reinforcing Ishizuka Glass’s focus on compliant closures and barrier glass; the global food packaging market was about USD 387 billion in 2023 (Grand View Research). During crises many states kept packaging plants operational but imposed workforce mobility limits, shifting demand toward shelf-stable formats and accelerating orders for tamper-evident solutions.

- Essential designation: continuity of operations

- USD 387B market (2023)

- Higher demand for shelf-stable, tamper-evident packaging

- Compliance readiness = operational resilience

Localization and reshoring

Political pressure to localize beverage and pharma packaging is driving plant siting decisions; incentives for domestic production (eg US CHIPS Act funding ~280 billion USD) create opportunities but raise expectations of local-content rules (EU Critical Raw Materials Act, 2023). Regionalization lowers geopolitical transport risk and a multi-hub strategy improves resilience.

- Plant siting driven by localization

- Incentives raise domestic-opportunity but imply local-content

- Regionalization cuts transport/geopolitical risk

- Multi-hub strategy boosts supply resilience

Trade shifts, freight delays and ¥2T GX spur low-carbon capex amid localization mandates

Tariffs/antidumping and ~20 Japan FTAs (2024) shift input/export pricing (~±15%); 2024 geopolitical tensions raised freight lead times 15–20%. METI GX support (~¥2T) and 2030 GHG target (46–50%) push low‑carbon capex despite no national carbon price. Localization/recycling mandates affect siting and cullet supply.

| Metric | Value |

|---|---|

| Japan FTAs | ~20 |

| GX fund | ¥2T |

| Freight delays (2024) | 15–20% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Ishizuka Glass, with data-backed insights, region- and industry-specific examples, forward-looking scenario implications, and clean formatting to support executives, investors and strategists.

A concise, visually segmented PESTLE summary for Ishizuka Glass that’s easily droppable into presentations and shareable across teams, enabling quick alignment on external risks and market positioning while allowing editable notes for region- or product-specific context.

Economic factors

Energy price volatility

Glass melting depends heavily on electricity and gas, making margins sensitive to energy spikes — LNG spot (JKM) surged above $60/MMBtu in 2022 before averaging about $14/MMBtu in 2024, pressuring input costs. Long-term PPAs and furnace efficiency upgrades have been used to stabilize cashflow and cap volatility. Fuel switching to oxy-fuel or hybrid-electric furnaces cuts gas exposure, while robust pass-through clauses with FMCG clients remain critical to protect margins.

FX and yen dynamics

Yen weakness since 2023, with USD/JPY trading around 155–160 in mid‑2025, boosts Ishizuka Glass export competitiveness but raises costs for imported raw materials and resins priced in dollars. Strategic FX hedging smooths cash‑flow and operating earnings but cannot remove translation losses on consolidated results. Taking orders priced in local currencies reduces customer friction, while a balanced geographic revenue mix helps limit net FX swings.

Consumer demand cycles

Beverage, food and hospitality cycles strongly drive bottle and tableware volumes; the global glass packaging market was about USD 65 billion in 2023 with ~4% CAGR projected to 2028, reflecting steady demand for bottles. Premiumization has lifted glass mix and value-per-unit, with premium glass segments growing faster than commodity packs in 2023–24. Downturns shift volumes to lighter, cheaper packs, while on-premise recovery—restaurant sales near 90–95% of pre‑pandemic levels by 2024—aided tableware rebound. SKU agility helps protect plant utilization and margins amid these swings.

Raw materials and logistics

- Soda ash global output ~53 mt (2022)

- EU glass cullet recycling ~76%

- Freight volatility: ~70% drop from 2021 to 2024 peaks

- Nearshoring cuts logistics costs/emissions ~10–30%

Labor and productivity

Japan’s aging workforce tightens skilled labor supply in hot-end operations, with 65+ at about 29% of the population in 2024; shortages raise reliance on experienced operators. Automation and AI inspection raise throughput and cut defects (industry reports cite defect reductions of 20–30%), while ~3% nominal wage growth in 2024 pressures unit costs absent efficiency gains; targeted training and ergonomics boost retention.

- Aging workforce: 65+ ≈29% (2024)

- Defect reduction: AI/automation 20–30%

- Wage pressure: ≈3% nominal pay rise (2024)

- Retention: training + ergonomics lowers turnover

Trade shifts, freight delays and ¥2T GX spur low-carbon capex amid localization mandates

High energy intensity leaves margins exposed—JKM peaked >$60/MMBtu in 2022, averaged ~$14/MMBtu in 2024; PPAs, efficiency and fuel-switching reduce volatility. Yen ~155–160 (mid‑2025) aids exports but raises dollar‑priced input costs; FX hedges smooth cash flow. Global glass market ≈$65bn (2023) with ~4% CAGR to 2028; cullet, soda ash (≈53mt 2022) and freight swings drive unit costs.

| Metric | Value |

|---|---|

| JKM 2024 avg | $14/MMBtu |

| USD/JPY mid‑2025 | 155–160 |

| Glass market 2023 | $65bn |

| Soda ash 2022 | 53 mt |

Full Version Awaits

Ishizuka Glass PESTLE Analysis

The preview shown here is the exact Ishizuka Glass PESTLE document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental analysis with charts and citations as displayed. No placeholders or surprises; download this exact file immediately after payment.