ITAB SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

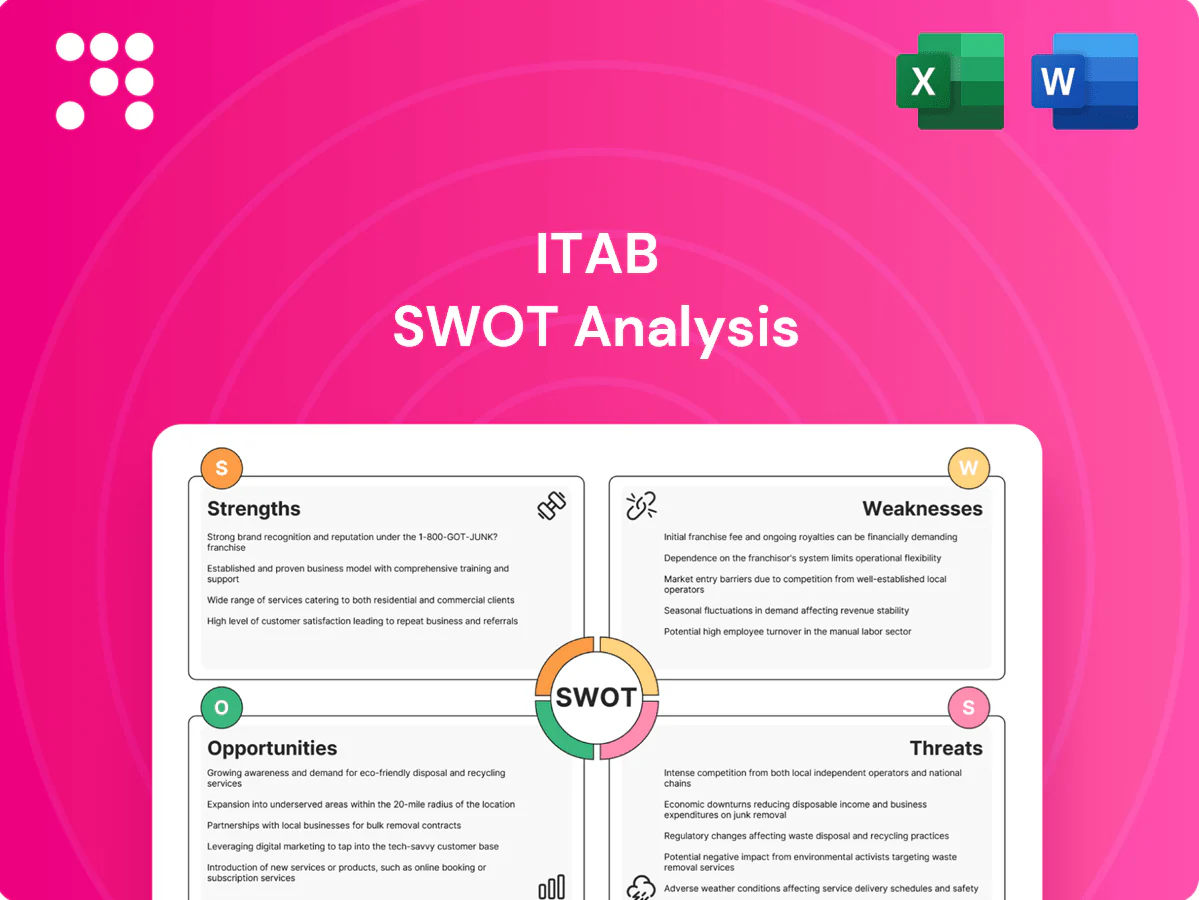

ITAB’s SWOT snapshot highlights strong retail tech integration, global footprint, and innovation-led product suite, alongside margin pressures and supply-chain risks; emerging omnichannel trends offer clear growth levers. Want the full strategic picture and editable tools? Purchase the complete SWOT analysis for a detailed, investor-ready report and Excel deliverables.

Strengths

End-to-end shopfitting solutions

ITAB offers integrated design, manufacture, installation and service, simplifying vendor management for retailers and cutting coordination overhead. A single accountable partner reduces project risk and accelerates rollouts, enabling faster time-to-shelf and consistent store standards. Bundling increases wallet share per store, strengthens customer lock-in and enables cross-selling across fixtures, checkouts, entrances and lighting.

Deep retail domain expertise

Deep retail domain expertise across grocery, fashion and specialty formats enables fit-for-purpose concepts that align SKU mix and store zoning with sales density. Understanding store flows and shrink drivers helps optimize checkout and entrance designs, critical given global retail shrink averages about 1.8% of sales (NRF recent data). Proven references from large chains de-risk decisions, shortening procurement cycles and supporting premium pricing and positioning.

Integrated hardware + lighting portfolio

Combining fixtures with LED and control systems boosts energy efficiency and shopper experience, as LEDs use up to 75% less energy than incandescent (U.S. DOE) and tunable lighting improves dwell time and perceived product quality. Lighting can represent 20–40% of retail energy use; integrated solutions cut power and labor costs and often yield paybacks under three years, differentiating ITAB from single-category suppliers.

Global footprint and install network

ITABs global footprint and install network enables consistent execution for international retailers, leveraging local production and partnerships to cut lead times and meet regional standards. A dedicated field service network delivers reliable installation and ongoing maintenance, allowing rapid scaling of large rollouts and regular refresh programs across markets.

Modular, scalable concepts

Modular, scalable concepts shorten design cycles and lower total cost of ownership by enabling reuse of standardized modules; McKinsey 2024 estimates format rollouts accelerate by about 20% with modular approaches. Retailers can reconfigure layouts as formats evolve, supporting rapid pilots and A/B testing in stores while easing sourcing and inventory planning.

E2E delivery speeds rollout 20%; LEDs cut energy 75%

Integrated end-to-end delivery shortens time-to-shelf and raises wallet share; modular concepts accelerate rollouts ~20% (McKinsey 2024). LED+controls cut lighting energy up to 75% (U.S. DOE) with typical paybacks <3 years; domain expertise and references reduce procurement risk (NRF retail shrink ~1.8%). Global install/service network enables rapid, consistent multiregional scale.

| Metric | Value |

|---|---|

| Rollout speed | +20% (McKinsey 2024) |

| Lighting energy | -75% (U.S. DOE) |

| Payback | <3 yrs |

| Retail shrink | 1.8% (NRF) |

What is included in the product

Provides a concise SWOT analysis of ITAB, highlighting internal capabilities and operational weaknesses while mapping market opportunities and external threats that shape the company’s strategic direction.

Delivers a clear SWOT matrix tailored to ITAB for rapid alignment of retail display and checkout strategies, enabling executives to spot opportunities and mitigate risks quickly.

Weaknesses

Exposure to retail capex cycles

Project revenues at ITAB hinge on store openings, refurbishments and retailer budgets, so retail capex slowdowns or retailer distress can push projects and receipts into later quarters. Industry experience shows fixture suppliers can face revenue swings up to 20% year‑on‑year during downturns, creating pronounced cyclicality. That volatility complicates forecasting and lowers capacity utilization, raising short‑term margin pressure.

Margin pressure and commoditization

Fixtures and standard checkouts face intense price competition from low-cost manufacturers, pressuring ITABs margins as retail tenders increasingly prioritize unit cost over lifecycle value. Mix shifts toward basic, low-margin products can compress gross margins and lowered EBITA. Sustainable differentiation must lean on superior design, integrated services and measurable retail outcomes to defend pricing power. ITAB is listed on Nasdaq Stockholm, reinforcing capital-market scrutiny.

Concentration risk in key accounts

Nasdaq Stockholm-listed ITAB faces concentration risk as large retail chains can constitute a significant portion of order intake; losing a major contract or facing client insourcing would have an outsized effect on revenue and EBITDA. Powerful buyers among big-box retailers exert strong pricing pressure, making margin resilience challenging. Diversification across customer segments and geographies is therefore essential to reduce vulnerability.

Supply chain and input cost sensitivity

Steel, electronics and freight volatility have raised ITABs COGS, with market-reported component lead times commonly stretching 8–20 weeks in 2024 and freight rate swings adding episodic cost spikes.

Long project lead times limit speed to pass higher input costs to customers, while component shortages in 2024 delayed a notable share of installations, stressing working capital and dampening customer satisfaction.

- COGS exposure: steel, electronics, freight

- Lead times: 8–20 weeks

- Delays: component shortages impact installations

- Cash strain: working capital and satisfaction hit

Limited software/analytics depth

Compared with tech-native rivals, ITABs data platforms show less maturity while retailers increasingly demand IoT analytics, computer vision and AI-driven insights; global AI systems spending was forecast to top $300 billion in 2024 (IDC). Hardware-heavy offerings reduce customer stickiness and margin resilience, so partnerships or rapid software build-out are required to stay competitive.

- Data platform maturity gap

- Rising demand for IoT/vision/AI

- Hardware-only lowers stickiness

- Need partnerships or build-out

Revenue swings, client concentration and long lead times squeeze margins amid AI surge

Revenue cyclicality (up to 20% y/y swings) and client concentration expose ITAB to order volatility and outsized EBITDA hits. Rising COGS and 8–20 week lead times strain working capital and delay installations. Lower data-platform maturity vs. tech rivals amid $300B AI spend in 2024 risks reduced stickiness and margin pressure.

| Metric | Value |

|---|---|

| Revenue swing (industry) | up to 20% y/y |

| Lead times (2024) | 8–20 weeks |

| AI market (2024) | $300B (IDC) |

Preview Before You Purchase

ITAB SWOT Analysis

This is the actual ITAB SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version for download.

Dive Deeper Into the Company’s Strategic Blueprint

ITAB’s SWOT snapshot highlights strong retail tech integration, global footprint, and innovation-led product suite, alongside margin pressures and supply-chain risks; emerging omnichannel trends offer clear growth levers. Want the full strategic picture and editable tools? Purchase the complete SWOT analysis for a detailed, investor-ready report and Excel deliverables.

Strengths

End-to-end shopfitting solutions

ITAB offers integrated design, manufacture, installation and service, simplifying vendor management for retailers and cutting coordination overhead. A single accountable partner reduces project risk and accelerates rollouts, enabling faster time-to-shelf and consistent store standards. Bundling increases wallet share per store, strengthens customer lock-in and enables cross-selling across fixtures, checkouts, entrances and lighting.

Deep retail domain expertise

Deep retail domain expertise across grocery, fashion and specialty formats enables fit-for-purpose concepts that align SKU mix and store zoning with sales density. Understanding store flows and shrink drivers helps optimize checkout and entrance designs, critical given global retail shrink averages about 1.8% of sales (NRF recent data). Proven references from large chains de-risk decisions, shortening procurement cycles and supporting premium pricing and positioning.

Integrated hardware + lighting portfolio

Combining fixtures with LED and control systems boosts energy efficiency and shopper experience, as LEDs use up to 75% less energy than incandescent (U.S. DOE) and tunable lighting improves dwell time and perceived product quality. Lighting can represent 20–40% of retail energy use; integrated solutions cut power and labor costs and often yield paybacks under three years, differentiating ITAB from single-category suppliers.

Global footprint and install network

ITABs global footprint and install network enables consistent execution for international retailers, leveraging local production and partnerships to cut lead times and meet regional standards. A dedicated field service network delivers reliable installation and ongoing maintenance, allowing rapid scaling of large rollouts and regular refresh programs across markets.

Modular, scalable concepts

Modular, scalable concepts shorten design cycles and lower total cost of ownership by enabling reuse of standardized modules; McKinsey 2024 estimates format rollouts accelerate by about 20% with modular approaches. Retailers can reconfigure layouts as formats evolve, supporting rapid pilots and A/B testing in stores while easing sourcing and inventory planning.

E2E delivery speeds rollout 20%; LEDs cut energy 75%

Integrated end-to-end delivery shortens time-to-shelf and raises wallet share; modular concepts accelerate rollouts ~20% (McKinsey 2024). LED+controls cut lighting energy up to 75% (U.S. DOE) with typical paybacks <3 years; domain expertise and references reduce procurement risk (NRF retail shrink ~1.8%). Global install/service network enables rapid, consistent multiregional scale.

| Metric | Value |

|---|---|

| Rollout speed | +20% (McKinsey 2024) |

| Lighting energy | -75% (U.S. DOE) |

| Payback | <3 yrs |

| Retail shrink | 1.8% (NRF) |

What is included in the product

Provides a concise SWOT analysis of ITAB, highlighting internal capabilities and operational weaknesses while mapping market opportunities and external threats that shape the company’s strategic direction.

Delivers a clear SWOT matrix tailored to ITAB for rapid alignment of retail display and checkout strategies, enabling executives to spot opportunities and mitigate risks quickly.

Weaknesses

Exposure to retail capex cycles

Project revenues at ITAB hinge on store openings, refurbishments and retailer budgets, so retail capex slowdowns or retailer distress can push projects and receipts into later quarters. Industry experience shows fixture suppliers can face revenue swings up to 20% year‑on‑year during downturns, creating pronounced cyclicality. That volatility complicates forecasting and lowers capacity utilization, raising short‑term margin pressure.

Margin pressure and commoditization

Fixtures and standard checkouts face intense price competition from low-cost manufacturers, pressuring ITABs margins as retail tenders increasingly prioritize unit cost over lifecycle value. Mix shifts toward basic, low-margin products can compress gross margins and lowered EBITA. Sustainable differentiation must lean on superior design, integrated services and measurable retail outcomes to defend pricing power. ITAB is listed on Nasdaq Stockholm, reinforcing capital-market scrutiny.

Concentration risk in key accounts

Nasdaq Stockholm-listed ITAB faces concentration risk as large retail chains can constitute a significant portion of order intake; losing a major contract or facing client insourcing would have an outsized effect on revenue and EBITDA. Powerful buyers among big-box retailers exert strong pricing pressure, making margin resilience challenging. Diversification across customer segments and geographies is therefore essential to reduce vulnerability.

Supply chain and input cost sensitivity

Steel, electronics and freight volatility have raised ITABs COGS, with market-reported component lead times commonly stretching 8–20 weeks in 2024 and freight rate swings adding episodic cost spikes.

Long project lead times limit speed to pass higher input costs to customers, while component shortages in 2024 delayed a notable share of installations, stressing working capital and dampening customer satisfaction.

- COGS exposure: steel, electronics, freight

- Lead times: 8–20 weeks

- Delays: component shortages impact installations

- Cash strain: working capital and satisfaction hit

Limited software/analytics depth

Compared with tech-native rivals, ITABs data platforms show less maturity while retailers increasingly demand IoT analytics, computer vision and AI-driven insights; global AI systems spending was forecast to top $300 billion in 2024 (IDC). Hardware-heavy offerings reduce customer stickiness and margin resilience, so partnerships or rapid software build-out are required to stay competitive.

- Data platform maturity gap

- Rising demand for IoT/vision/AI

- Hardware-only lowers stickiness

- Need partnerships or build-out

Revenue swings, client concentration and long lead times squeeze margins amid AI surge

Revenue cyclicality (up to 20% y/y swings) and client concentration expose ITAB to order volatility and outsized EBITDA hits. Rising COGS and 8–20 week lead times strain working capital and delay installations. Lower data-platform maturity vs. tech rivals amid $300B AI spend in 2024 risks reduced stickiness and margin pressure.

| Metric | Value |

|---|---|

| Revenue swing (industry) | up to 20% y/y |

| Lead times (2024) | 8–20 weeks |

| AI market (2024) | $300B (IDC) |

Preview Before You Purchase

ITAB SWOT Analysis

This is the actual ITAB SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version for download.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

ITAB’s SWOT snapshot highlights strong retail tech integration, global footprint, and innovation-led product suite, alongside margin pressures and supply-chain risks; emerging omnichannel trends offer clear growth levers. Want the full strategic picture and editable tools? Purchase the complete SWOT analysis for a detailed, investor-ready report and Excel deliverables.

Strengths

End-to-end shopfitting solutions

ITAB offers integrated design, manufacture, installation and service, simplifying vendor management for retailers and cutting coordination overhead. A single accountable partner reduces project risk and accelerates rollouts, enabling faster time-to-shelf and consistent store standards. Bundling increases wallet share per store, strengthens customer lock-in and enables cross-selling across fixtures, checkouts, entrances and lighting.

Deep retail domain expertise

Deep retail domain expertise across grocery, fashion and specialty formats enables fit-for-purpose concepts that align SKU mix and store zoning with sales density. Understanding store flows and shrink drivers helps optimize checkout and entrance designs, critical given global retail shrink averages about 1.8% of sales (NRF recent data). Proven references from large chains de-risk decisions, shortening procurement cycles and supporting premium pricing and positioning.

Integrated hardware + lighting portfolio

Combining fixtures with LED and control systems boosts energy efficiency and shopper experience, as LEDs use up to 75% less energy than incandescent (U.S. DOE) and tunable lighting improves dwell time and perceived product quality. Lighting can represent 20–40% of retail energy use; integrated solutions cut power and labor costs and often yield paybacks under three years, differentiating ITAB from single-category suppliers.

Global footprint and install network

ITABs global footprint and install network enables consistent execution for international retailers, leveraging local production and partnerships to cut lead times and meet regional standards. A dedicated field service network delivers reliable installation and ongoing maintenance, allowing rapid scaling of large rollouts and regular refresh programs across markets.

Modular, scalable concepts

Modular, scalable concepts shorten design cycles and lower total cost of ownership by enabling reuse of standardized modules; McKinsey 2024 estimates format rollouts accelerate by about 20% with modular approaches. Retailers can reconfigure layouts as formats evolve, supporting rapid pilots and A/B testing in stores while easing sourcing and inventory planning.

E2E delivery speeds rollout 20%; LEDs cut energy 75%

Integrated end-to-end delivery shortens time-to-shelf and raises wallet share; modular concepts accelerate rollouts ~20% (McKinsey 2024). LED+controls cut lighting energy up to 75% (U.S. DOE) with typical paybacks <3 years; domain expertise and references reduce procurement risk (NRF retail shrink ~1.8%). Global install/service network enables rapid, consistent multiregional scale.

| Metric | Value |

|---|---|

| Rollout speed | +20% (McKinsey 2024) |

| Lighting energy | -75% (U.S. DOE) |

| Payback | <3 yrs |

| Retail shrink | 1.8% (NRF) |

What is included in the product

Provides a concise SWOT analysis of ITAB, highlighting internal capabilities and operational weaknesses while mapping market opportunities and external threats that shape the company’s strategic direction.

Delivers a clear SWOT matrix tailored to ITAB for rapid alignment of retail display and checkout strategies, enabling executives to spot opportunities and mitigate risks quickly.

Weaknesses

Exposure to retail capex cycles

Project revenues at ITAB hinge on store openings, refurbishments and retailer budgets, so retail capex slowdowns or retailer distress can push projects and receipts into later quarters. Industry experience shows fixture suppliers can face revenue swings up to 20% year‑on‑year during downturns, creating pronounced cyclicality. That volatility complicates forecasting and lowers capacity utilization, raising short‑term margin pressure.

Margin pressure and commoditization

Fixtures and standard checkouts face intense price competition from low-cost manufacturers, pressuring ITABs margins as retail tenders increasingly prioritize unit cost over lifecycle value. Mix shifts toward basic, low-margin products can compress gross margins and lowered EBITA. Sustainable differentiation must lean on superior design, integrated services and measurable retail outcomes to defend pricing power. ITAB is listed on Nasdaq Stockholm, reinforcing capital-market scrutiny.

Concentration risk in key accounts

Nasdaq Stockholm-listed ITAB faces concentration risk as large retail chains can constitute a significant portion of order intake; losing a major contract or facing client insourcing would have an outsized effect on revenue and EBITDA. Powerful buyers among big-box retailers exert strong pricing pressure, making margin resilience challenging. Diversification across customer segments and geographies is therefore essential to reduce vulnerability.

Supply chain and input cost sensitivity

Steel, electronics and freight volatility have raised ITABs COGS, with market-reported component lead times commonly stretching 8–20 weeks in 2024 and freight rate swings adding episodic cost spikes.

Long project lead times limit speed to pass higher input costs to customers, while component shortages in 2024 delayed a notable share of installations, stressing working capital and dampening customer satisfaction.

- COGS exposure: steel, electronics, freight

- Lead times: 8–20 weeks

- Delays: component shortages impact installations

- Cash strain: working capital and satisfaction hit

Limited software/analytics depth

Compared with tech-native rivals, ITABs data platforms show less maturity while retailers increasingly demand IoT analytics, computer vision and AI-driven insights; global AI systems spending was forecast to top $300 billion in 2024 (IDC). Hardware-heavy offerings reduce customer stickiness and margin resilience, so partnerships or rapid software build-out are required to stay competitive.

- Data platform maturity gap

- Rising demand for IoT/vision/AI

- Hardware-only lowers stickiness

- Need partnerships or build-out

Revenue swings, client concentration and long lead times squeeze margins amid AI surge

Revenue cyclicality (up to 20% y/y swings) and client concentration expose ITAB to order volatility and outsized EBITDA hits. Rising COGS and 8–20 week lead times strain working capital and delay installations. Lower data-platform maturity vs. tech rivals amid $300B AI spend in 2024 risks reduced stickiness and margin pressure.

| Metric | Value |

|---|---|

| Revenue swing (industry) | up to 20% y/y |

| Lead times (2024) | 8–20 weeks |

| AI market (2024) | $300B (IDC) |

Preview Before You Purchase

ITAB SWOT Analysis

This is the actual ITAB SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version for download.