Itafos Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

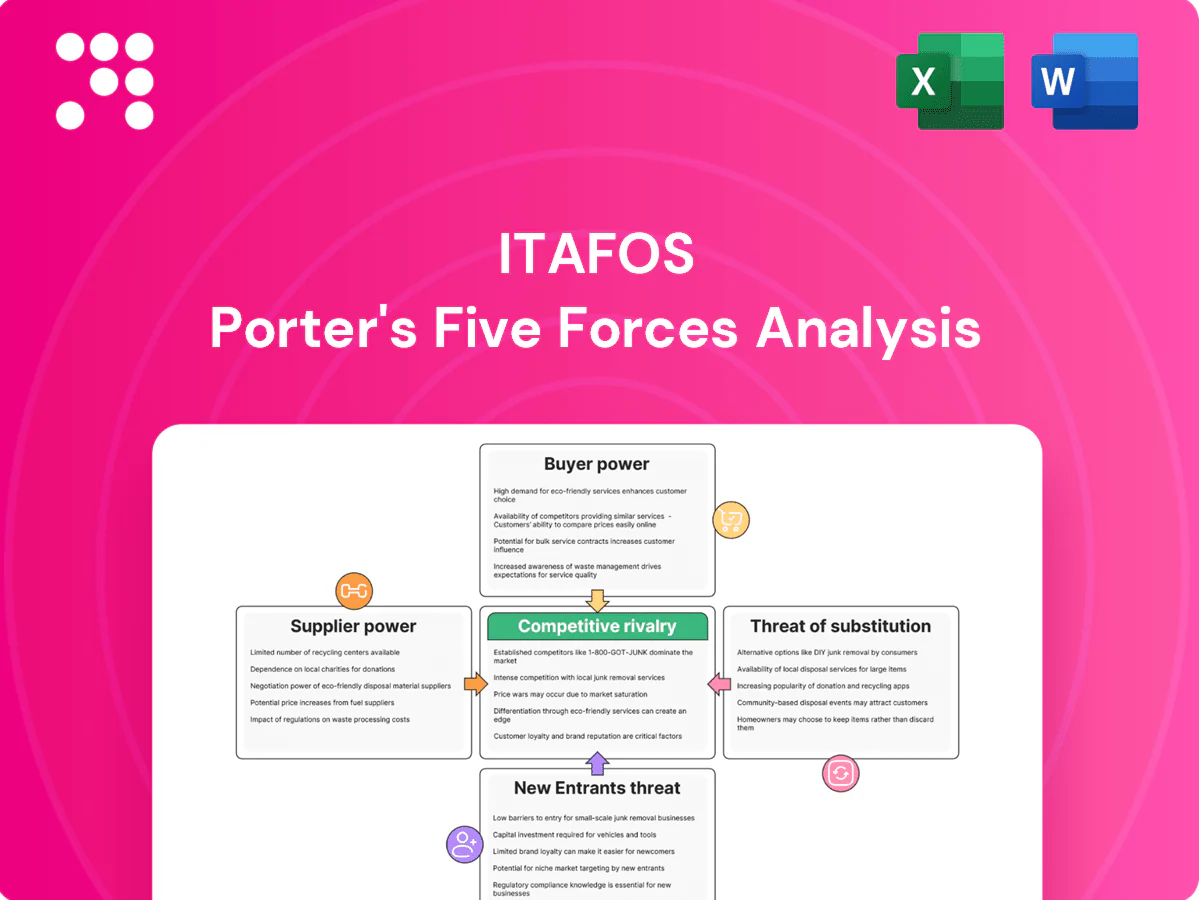

Itafos’s Porter's Five Forces snapshot highlights concentrated supplier power, moderate buyer leverage, limited substitute threats, and barriers that shape its phosphates-focused moat; competitive rivalry and regulatory pressures remain key risks to monitor. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for investment and planning.

Suppliers Bargaining Power

Concentrated phosphate rock sources

Phosphate rock supply is concentrated—Morocco/Western Sahara hold roughly 70% of global reserves (USGS 2024) while world production is about 230 million tonnes, elevating supplier leverage on pricing and terms. Long-term contracts and captive resources can blunt exposure, but spot-market purchases remain highly volatile. Political or logistical disruptions in key basins can quickly push input costs, so Itafos must balance multi-sourcing with inventory buffers to reduce shocks.

Ammonia and sulfur feedstock volatility

Ammonia and sulfur are critical inputs with prices tied to energy markets; energy typically represents roughly 60–80% of ammonia production cost, creating strong cost-pass-through pressure.

Logistics and transport dependencies

Rail, barge and port capacity constraints during peak seasons empowered logistics providers, with the Baltic Dry Index averaging about 1,350 in 2024, sustaining periodic freight spikes that eroded delivered-cost advantages. Spot surcharges and congestion premiums lifted delivered costs for producers. Contracted capacity and diversified routing reduced exposure, while vertical coordination and local storage near demand centers further diluted supplier bargaining power.

Specialty additives and reagents

Specialty additives and reagents for niche fertilizer grades are often sourced from a limited set of vendors, increasing supplier bargaining power; switching is constrained by qualification cycles and technical validation. Itafos mitigates dependency through dual-qualification and vendor development programs and secures volume commitments to negotiate better pricing and terms.

- Limited vendor pool raises dependency

- Qualification costs increase switching barriers

- Dual-qualification lowers single-supplier risk

- Volume commitments unlock improved terms

Regulatory and mining permits

Permitting and environmental compliance force Itafos to rely on specialized consultants and regulatory authorities, linking operations to external service providers; regulatory tightening or multi-year permit delays can strengthen suppliers and regulators relative to producers.

- Advance permitting strategy

- Community engagement

- Internal regulatory expertise

Supply risk: Morocco ~70% phosphate share; energy, logistics push prices

Supplier power is high: Morocco/Western Sahara hold ~70% of phosphate reserves (USGS 2024) while global production ~230Mt, concentrating pricing risk. Ammonia/sulfur costs are energy-linked (ammonia energy share ~60–80%), enabling pass-through. Logistics volatility (BDI ~1,350 in 2024) and specialty-vendor scarcity increase supplier leverage; Itafos offsets via multi-sourcing, contracts and inventory.

| Metric | Value |

|---|---|

| Phosphate reserves (Morocco/WS) | ~70% (USGS 2024) |

| World phosphate production | ~230 Mt (2024) |

| BDI average | ~1,350 (2024) |

| Ammonia energy cost share | 60–80% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Itafos, uncovering key drivers of competition, supplier and buyer power, substitutes, and entry barriers that shape pricing and profitability. Highlights emerging threats, strategic advantages, and actionable implications for investors and management.

A concise one-sheet Itafos Porter's Five Forces summary—instantly spot competitive pressures and priorities for strategic action; customizable force levels and ready-to-copy layout make it ideal for decks, dashboards, and nontechnical users.

Customers Bargaining Power

Large ag-retailers and co-ops

Large ag-retailers and co-ops in the Americas, led by players such as Nutrien and CHS, command volume and negotiate aggressively on price and credit. Their expanding private-label fertilizer and seed programs in 2024 increased buyer leverage while multi-year offtake contracts and service differentiation stabilize relationships. Performance guarantees and agronomic support shift focus from pure price to total ROI.

Price-sensitive growers

In 2024 farmers remained highly price-sensitive—fertilizer can represent roughly 20–40% of variable production costs, so tight margins and seasonal crop cycles make demand elastic. Growers actively compare alternatives and commonly defer applications when fertilizer prices spike, particularly after increases exceeding mid-teens percent. Tailored blends, on-farm financing and multi-year contracts can soften price pressure, while localized yield trials and ROI data (showing ROI lifts often >10%) help defend premium pricing.

Product standardization in commodities

MAP/DAP/MOP-like products are highly standardized, increasing buyer switching as global fertilizer market value reached about $221 billion in 2024; price and freight parity drive choices. Delivered cost and reliability dominate procurement decisions, with logistics disruptions in 2023–24 showing up to 20–30% swings in landed cost. Logistics excellence and consistent quality offset commoditization by reducing total delivered cost. Specialty SKUs with proven performance create customer stickiness and margin premium.

Seasonality and timing leverage

Planting windows concentrate demand, giving buyers timing leverage over inventory-held suppliers and pressuring margins during peak sowing periods. End-of-season carry forces discounts as distributors clear stock. Dynamic pricing and prepay programs introduced in 2024 help smooth demand and reduce spot volatility, while regional inventory positioning cuts last-mile bargaining power by shortening lead times.

- Timing leverage: concentrated planting demand

- End-of-season: discount pressure

- Mitigation: dynamic pricing/prepay programs (2024 uptake)

- Defense: regional inventory reduces last-mile leverage

Information transparency

- Market indices: higher transparency in 2024

- Buyer benchmarking: pressure on margins

- Service bundles: reclaim margin via agronomy

- Data-sharing: curbs haggling, raises efficiency

Timing, freight & services dent retailer power; fertilizer 20–40%

Large ag‑retailers and co‑ops (eg Nutrien, CHS) leveraged volume in 2024, pressuring price and credit while multi‑year contracts and service bundles limited pure price competition. Farmers stayed price‑sensitive—fertilizer ~20–40% of variable costs—so timing and freight give buyers leverage. Differentiation ( agronomy, ROI >10%) and regional inventory trimmed bargaining power.

| Metric | 2024 |

|---|---|

| Global market | $221B |

| Fertilizer share of var. costs | 20–40% |

| Logistics landed cost swings | 20–30% |

| ROI lift from services | >10% |

Same Document Delivered

Itafos Porter's Five Forces Analysis

This preview shows the exact Itafos Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You’re looking at the final deliverable, identical to the file you’ll get upon payment.

A Must-Have Tool for Decision-Makers

Itafos’s Porter's Five Forces snapshot highlights concentrated supplier power, moderate buyer leverage, limited substitute threats, and barriers that shape its phosphates-focused moat; competitive rivalry and regulatory pressures remain key risks to monitor. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for investment and planning.

Suppliers Bargaining Power

Concentrated phosphate rock sources

Phosphate rock supply is concentrated—Morocco/Western Sahara hold roughly 70% of global reserves (USGS 2024) while world production is about 230 million tonnes, elevating supplier leverage on pricing and terms. Long-term contracts and captive resources can blunt exposure, but spot-market purchases remain highly volatile. Political or logistical disruptions in key basins can quickly push input costs, so Itafos must balance multi-sourcing with inventory buffers to reduce shocks.

Ammonia and sulfur feedstock volatility

Ammonia and sulfur are critical inputs with prices tied to energy markets; energy typically represents roughly 60–80% of ammonia production cost, creating strong cost-pass-through pressure.

Logistics and transport dependencies

Rail, barge and port capacity constraints during peak seasons empowered logistics providers, with the Baltic Dry Index averaging about 1,350 in 2024, sustaining periodic freight spikes that eroded delivered-cost advantages. Spot surcharges and congestion premiums lifted delivered costs for producers. Contracted capacity and diversified routing reduced exposure, while vertical coordination and local storage near demand centers further diluted supplier bargaining power.

Specialty additives and reagents

Specialty additives and reagents for niche fertilizer grades are often sourced from a limited set of vendors, increasing supplier bargaining power; switching is constrained by qualification cycles and technical validation. Itafos mitigates dependency through dual-qualification and vendor development programs and secures volume commitments to negotiate better pricing and terms.

- Limited vendor pool raises dependency

- Qualification costs increase switching barriers

- Dual-qualification lowers single-supplier risk

- Volume commitments unlock improved terms

Regulatory and mining permits

Permitting and environmental compliance force Itafos to rely on specialized consultants and regulatory authorities, linking operations to external service providers; regulatory tightening or multi-year permit delays can strengthen suppliers and regulators relative to producers.

- Advance permitting strategy

- Community engagement

- Internal regulatory expertise

Supply risk: Morocco ~70% phosphate share; energy, logistics push prices

Supplier power is high: Morocco/Western Sahara hold ~70% of phosphate reserves (USGS 2024) while global production ~230Mt, concentrating pricing risk. Ammonia/sulfur costs are energy-linked (ammonia energy share ~60–80%), enabling pass-through. Logistics volatility (BDI ~1,350 in 2024) and specialty-vendor scarcity increase supplier leverage; Itafos offsets via multi-sourcing, contracts and inventory.

| Metric | Value |

|---|---|

| Phosphate reserves (Morocco/WS) | ~70% (USGS 2024) |

| World phosphate production | ~230 Mt (2024) |

| BDI average | ~1,350 (2024) |

| Ammonia energy cost share | 60–80% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Itafos, uncovering key drivers of competition, supplier and buyer power, substitutes, and entry barriers that shape pricing and profitability. Highlights emerging threats, strategic advantages, and actionable implications for investors and management.

A concise one-sheet Itafos Porter's Five Forces summary—instantly spot competitive pressures and priorities for strategic action; customizable force levels and ready-to-copy layout make it ideal for decks, dashboards, and nontechnical users.

Customers Bargaining Power

Large ag-retailers and co-ops

Large ag-retailers and co-ops in the Americas, led by players such as Nutrien and CHS, command volume and negotiate aggressively on price and credit. Their expanding private-label fertilizer and seed programs in 2024 increased buyer leverage while multi-year offtake contracts and service differentiation stabilize relationships. Performance guarantees and agronomic support shift focus from pure price to total ROI.

Price-sensitive growers

In 2024 farmers remained highly price-sensitive—fertilizer can represent roughly 20–40% of variable production costs, so tight margins and seasonal crop cycles make demand elastic. Growers actively compare alternatives and commonly defer applications when fertilizer prices spike, particularly after increases exceeding mid-teens percent. Tailored blends, on-farm financing and multi-year contracts can soften price pressure, while localized yield trials and ROI data (showing ROI lifts often >10%) help defend premium pricing.

Product standardization in commodities

MAP/DAP/MOP-like products are highly standardized, increasing buyer switching as global fertilizer market value reached about $221 billion in 2024; price and freight parity drive choices. Delivered cost and reliability dominate procurement decisions, with logistics disruptions in 2023–24 showing up to 20–30% swings in landed cost. Logistics excellence and consistent quality offset commoditization by reducing total delivered cost. Specialty SKUs with proven performance create customer stickiness and margin premium.

Seasonality and timing leverage

Planting windows concentrate demand, giving buyers timing leverage over inventory-held suppliers and pressuring margins during peak sowing periods. End-of-season carry forces discounts as distributors clear stock. Dynamic pricing and prepay programs introduced in 2024 help smooth demand and reduce spot volatility, while regional inventory positioning cuts last-mile bargaining power by shortening lead times.

- Timing leverage: concentrated planting demand

- End-of-season: discount pressure

- Mitigation: dynamic pricing/prepay programs (2024 uptake)

- Defense: regional inventory reduces last-mile leverage

Information transparency

- Market indices: higher transparency in 2024

- Buyer benchmarking: pressure on margins

- Service bundles: reclaim margin via agronomy

- Data-sharing: curbs haggling, raises efficiency

Timing, freight & services dent retailer power; fertilizer 20–40%

Large ag‑retailers and co‑ops (eg Nutrien, CHS) leveraged volume in 2024, pressuring price and credit while multi‑year contracts and service bundles limited pure price competition. Farmers stayed price‑sensitive—fertilizer ~20–40% of variable costs—so timing and freight give buyers leverage. Differentiation ( agronomy, ROI >10%) and regional inventory trimmed bargaining power.

| Metric | 2024 |

|---|---|

| Global market | $221B |

| Fertilizer share of var. costs | 20–40% |

| Logistics landed cost swings | 20–30% |

| ROI lift from services | >10% |

Same Document Delivered

Itafos Porter's Five Forces Analysis

This preview shows the exact Itafos Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You’re looking at the final deliverable, identical to the file you’ll get upon payment.

Description

A Must-Have Tool for Decision-Makers

Itafos’s Porter's Five Forces snapshot highlights concentrated supplier power, moderate buyer leverage, limited substitute threats, and barriers that shape its phosphates-focused moat; competitive rivalry and regulatory pressures remain key risks to monitor. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for investment and planning.

Suppliers Bargaining Power

Concentrated phosphate rock sources

Phosphate rock supply is concentrated—Morocco/Western Sahara hold roughly 70% of global reserves (USGS 2024) while world production is about 230 million tonnes, elevating supplier leverage on pricing and terms. Long-term contracts and captive resources can blunt exposure, but spot-market purchases remain highly volatile. Political or logistical disruptions in key basins can quickly push input costs, so Itafos must balance multi-sourcing with inventory buffers to reduce shocks.

Ammonia and sulfur feedstock volatility

Ammonia and sulfur are critical inputs with prices tied to energy markets; energy typically represents roughly 60–80% of ammonia production cost, creating strong cost-pass-through pressure.

Logistics and transport dependencies

Rail, barge and port capacity constraints during peak seasons empowered logistics providers, with the Baltic Dry Index averaging about 1,350 in 2024, sustaining periodic freight spikes that eroded delivered-cost advantages. Spot surcharges and congestion premiums lifted delivered costs for producers. Contracted capacity and diversified routing reduced exposure, while vertical coordination and local storage near demand centers further diluted supplier bargaining power.

Specialty additives and reagents

Specialty additives and reagents for niche fertilizer grades are often sourced from a limited set of vendors, increasing supplier bargaining power; switching is constrained by qualification cycles and technical validation. Itafos mitigates dependency through dual-qualification and vendor development programs and secures volume commitments to negotiate better pricing and terms.

- Limited vendor pool raises dependency

- Qualification costs increase switching barriers

- Dual-qualification lowers single-supplier risk

- Volume commitments unlock improved terms

Regulatory and mining permits

Permitting and environmental compliance force Itafos to rely on specialized consultants and regulatory authorities, linking operations to external service providers; regulatory tightening or multi-year permit delays can strengthen suppliers and regulators relative to producers.

- Advance permitting strategy

- Community engagement

- Internal regulatory expertise

Supply risk: Morocco ~70% phosphate share; energy, logistics push prices

Supplier power is high: Morocco/Western Sahara hold ~70% of phosphate reserves (USGS 2024) while global production ~230Mt, concentrating pricing risk. Ammonia/sulfur costs are energy-linked (ammonia energy share ~60–80%), enabling pass-through. Logistics volatility (BDI ~1,350 in 2024) and specialty-vendor scarcity increase supplier leverage; Itafos offsets via multi-sourcing, contracts and inventory.

| Metric | Value |

|---|---|

| Phosphate reserves (Morocco/WS) | ~70% (USGS 2024) |

| World phosphate production | ~230 Mt (2024) |

| BDI average | ~1,350 (2024) |

| Ammonia energy cost share | 60–80% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Itafos, uncovering key drivers of competition, supplier and buyer power, substitutes, and entry barriers that shape pricing and profitability. Highlights emerging threats, strategic advantages, and actionable implications for investors and management.

A concise one-sheet Itafos Porter's Five Forces summary—instantly spot competitive pressures and priorities for strategic action; customizable force levels and ready-to-copy layout make it ideal for decks, dashboards, and nontechnical users.

Customers Bargaining Power

Large ag-retailers and co-ops

Large ag-retailers and co-ops in the Americas, led by players such as Nutrien and CHS, command volume and negotiate aggressively on price and credit. Their expanding private-label fertilizer and seed programs in 2024 increased buyer leverage while multi-year offtake contracts and service differentiation stabilize relationships. Performance guarantees and agronomic support shift focus from pure price to total ROI.

Price-sensitive growers

In 2024 farmers remained highly price-sensitive—fertilizer can represent roughly 20–40% of variable production costs, so tight margins and seasonal crop cycles make demand elastic. Growers actively compare alternatives and commonly defer applications when fertilizer prices spike, particularly after increases exceeding mid-teens percent. Tailored blends, on-farm financing and multi-year contracts can soften price pressure, while localized yield trials and ROI data (showing ROI lifts often >10%) help defend premium pricing.

Product standardization in commodities

MAP/DAP/MOP-like products are highly standardized, increasing buyer switching as global fertilizer market value reached about $221 billion in 2024; price and freight parity drive choices. Delivered cost and reliability dominate procurement decisions, with logistics disruptions in 2023–24 showing up to 20–30% swings in landed cost. Logistics excellence and consistent quality offset commoditization by reducing total delivered cost. Specialty SKUs with proven performance create customer stickiness and margin premium.

Seasonality and timing leverage

Planting windows concentrate demand, giving buyers timing leverage over inventory-held suppliers and pressuring margins during peak sowing periods. End-of-season carry forces discounts as distributors clear stock. Dynamic pricing and prepay programs introduced in 2024 help smooth demand and reduce spot volatility, while regional inventory positioning cuts last-mile bargaining power by shortening lead times.

- Timing leverage: concentrated planting demand

- End-of-season: discount pressure

- Mitigation: dynamic pricing/prepay programs (2024 uptake)

- Defense: regional inventory reduces last-mile leverage

Information transparency

- Market indices: higher transparency in 2024

- Buyer benchmarking: pressure on margins

- Service bundles: reclaim margin via agronomy

- Data-sharing: curbs haggling, raises efficiency

Timing, freight & services dent retailer power; fertilizer 20–40%

Large ag‑retailers and co‑ops (eg Nutrien, CHS) leveraged volume in 2024, pressuring price and credit while multi‑year contracts and service bundles limited pure price competition. Farmers stayed price‑sensitive—fertilizer ~20–40% of variable costs—so timing and freight give buyers leverage. Differentiation ( agronomy, ROI >10%) and regional inventory trimmed bargaining power.

| Metric | 2024 |

|---|---|

| Global market | $221B |

| Fertilizer share of var. costs | 20–40% |

| Logistics landed cost swings | 20–30% |

| ROI lift from services | >10% |

Same Document Delivered

Itafos Porter's Five Forces Analysis

This preview shows the exact Itafos Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You’re looking at the final deliverable, identical to the file you’ll get upon payment.