ITC Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

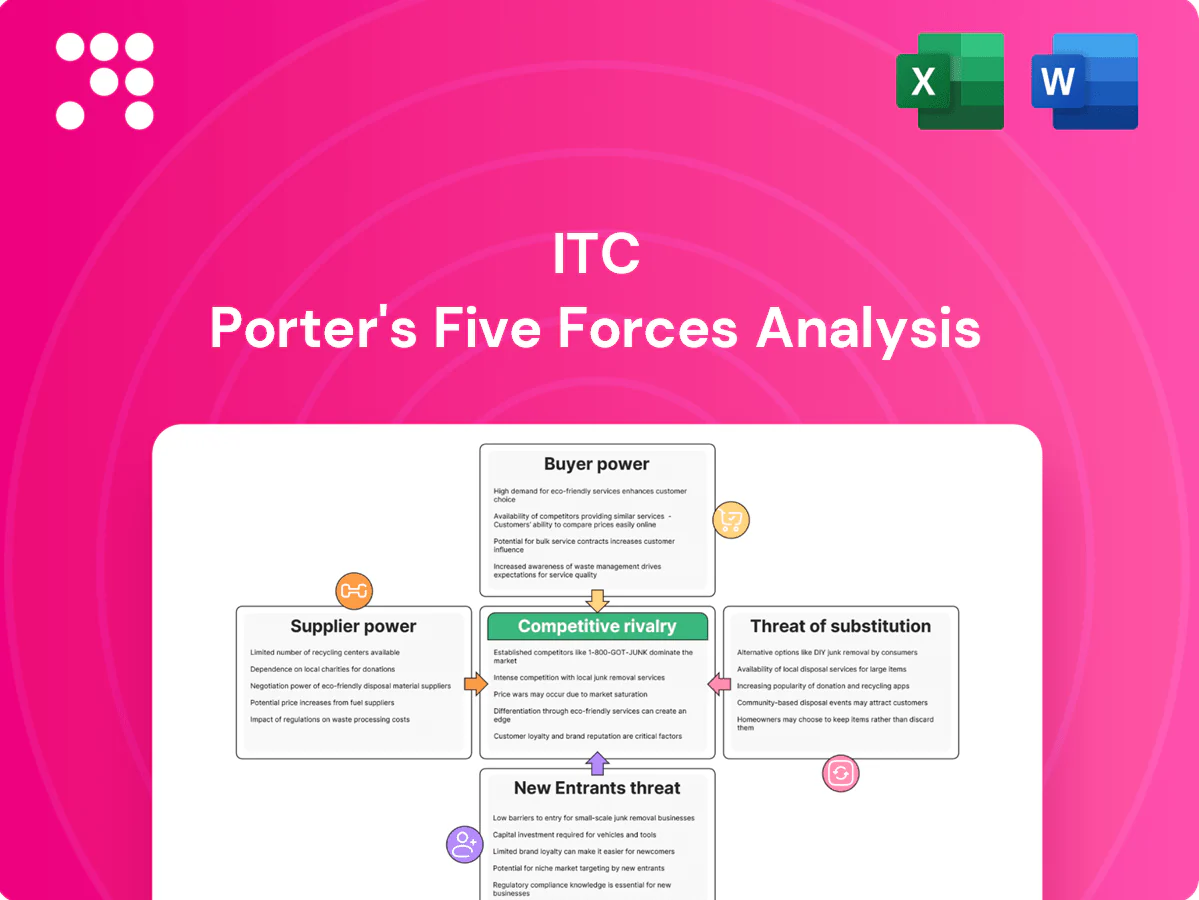

ITC’s Porter's Five Forces snapshot highlights bargaining power of suppliers and buyers, threat of new entrants, competitive rivalry, and substitute pressures that shape its margins and strategic choices. This brief teases key dynamics; unlock the full analysis for force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Diversified input base tempers leverage

ITC sources tobacco, agri-commodities, pulp, energy, fragrances and hospitality supplies across regions, diluting any single supplier’s clout. Multi-sourcing and import optionality cap price escalation and support stable margins. Commodity cycles—especially tobacco and pulp—can still swing input costs. Strategic procurement and hedging reduce volatility but cannot fully eliminate cyclical exposure.

Backward integration lowers dependence

ITC’s agri-sourcing platforms reach over 4.5 million farmers (2024) and its captive paperboards/pulp capacity of ~1.2 mtpa gives the company clear bargaining leverage with suppliers.

Direct farm linkages improve quality, traceability and pricing power, enabling ITC to pay competitive rates while controlling input costs and standards.

Disintermediation squeezes middlemen margins, shortens lead times and enhances supply assurance for FMCG and paper businesses.

Specialty inputs retain some power

Certain leaf tobacco grades, specialty chemicals, premium packaging and hotel perishables face supply constraints, with niche suppliers often commanding premiums (commonly around 15–25% in 2024) due to tight quality specs and compliance demands. Switching costs arise from costly reformulation, regulatory re-approvals and supplier audits, sometimes delaying product changes by months. Long-term contracts and forward buys (covering a substantial share of volumes) partly mitigate supply risk and price volatility.

Regulatory and ESG constraints affect costs

Regulatory and ESG compliance in tobacco, forestry and sustainability narrows ITC’s supplier pool as stricter licensing and product restrictions limit eligible vendors.

Certified inputs (FSC for packaging, food-safety certifications) command premiums; FSC reported 226 million hectares certified in 2023, reflecting higher certified-material demand and cost pressure.

Enhanced traceability systems and third-party ESG audits raise transaction and compliance costs, and the risk of supplier non-compliance forces stricter selection and monitoring.

- Compliance-driven supplier narrowing

- Certified-material premium (FSC 226M ha, 2023)

- Higher transaction costs from traceability & audits

- Stricter supplier selection due to non-compliance risk

Logistics and energy market dynamics matter

Freight, fuel and power tariffs materially affect delivered costs; freight volatility in 2024 kept landed costs elevated versus pre‑pandemic levels. Port congestion and monsoon disruptions can tighten near‑term supply and raise spot logistics premiums. ITC’s 60+ distributed manufacturing units reduce some transport intensity, though systemic shocks can temporarily boost supplier bargaining power.

- Freight volatility 2024: elevated vs pre‑2020

- Supply tighteners: port congestion, monsoon

- Mitigation: 60+ manufacturing units

Multi-sourcing, 4.5M farmer reach stabilizes margins amid freight spikes

ITC’s multi‑sourcing, 4.5M farmer reach (2024) and ~1.2 mtpa captive pulp limit supplier clout, stabilising margins. Niche inputs (leaf grades, specialty chemicals, premium packaging) carried 15–25% premiums in 2024, sustaining pockets of supplier power. Freight/power volatility in 2024 elevated landed costs despite 60+ plants, increasing short‑term supplier leverage.

| Metric | 2024 |

|---|---|

| Farmer reach | 4.5M |

| Pulp capacity | ~1.2 mtpa |

| Supplier premium (niche) | 15–25% |

| Manufacturing units | 60+ |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, threat of new entrants and substitutes, and industry rivalry as they specifically affect ITC’s diversified FMCG, hospitality and agribusiness portfolio, highlighting strategic vulnerabilities and defensive advantages.

One-sheet Porter's Five Forces for ITC—instantly spot competitive pressures, tweak force levels with real data, and export a clean spider chart for decks or boardrooms.

Customers Bargaining Power

Fragmented consumers yet price sensitive

Retail FMCG buyers are highly fragmented across c.12 million kirana and small outlets in India (2024), limiting individual bargaining power versus FMCG majors like ITC. Yet staples and personal-care categories are intensely price sensitive, creating strong collective pressure on pricing and margin. Rising private-label assortments increase direct price comparisons, forcing sharper promotions. Pack-price architecture and targeted promotions remain essential levers to defend share and margins.

Strong brands curb switching in cigarettes

Brand loyalty and habitual use sharply curb buyer power in cigarettes; ITC held over 80% of India’s legal branded cigarette market in 2024, making switching costly. Restrictive advertising boosts entrenched brand equity, but past tax hikes have driven down-trading to lower-price segments. Illicit trade, estimated around 5–10% in recent studies, complicates pricing and margin choices.

Modern trade and e-commerce wield clout

Modern trade and e-commerce wield clout as global e-commerce reached about 22% of retail sales in 2024 and dominant platforms (Amazon ~38% of US e‑commerce) extract margins, visibility fees and data access from FMCG partners. Shelf space and algorithmic placement drive velocity, forcing ITC to balance onerous channel terms with growing direct‑to‑consumer investment. Joint business plans and exclusives align incentives and protect margins.

Institutional buyers negotiate in B2B

Institutional buyers in B2B—paperboards, packaging clients and hospitality corporates—leverage volume and specification demands to extract concessions; formal tendering frequently compresses margins. Value-added grades and integrated solutions shift negotiations from price to total cost of ownership, while service levels and sustainability certifications such as FSC and ISO 14001 act as premium differentiators.

- Volume/spec leverage

- Tendering compresses margins

- Value-added reduces price-only talks

- Service & sustainability premium

Substitute availability heightens options

Substitute availability heightens options for ITC: many categories face alternatives at similar price points, so consumers can switch to local/D2C brands or unbranded staples. Convenience and availability drive quick switching, while loyalty programs and product innovation help retain share in a market estimated at about $110 billion in 2024.

- Alternatives at parity: local/D2C/unbranded

- Availability drives quick switching

- Retention via loyalty programs and NPD

- India FMCG ≈ $110 billion (2024)

~12m kiranas, ~22% e-commerce fees, illicit 5–10% squeeze FMCG margins

Retail FMCG buyers hugely fragmented (~12m kiranas, 2024) limiting individual power; price sensitivity and private labels pressure margins. Cigarette buyers constrained by brand loyalty—ITC >80% legal market (2024)—but taxes and illicit trade (5–10%) compress value. Modern trade/e‑commerce (~22% digital share, 2024) extract fees, raising channel leverage.

| Metric | 2024 |

|---|---|

| Kirana outlets | ~12m |

| ITC cigarette share | >80% |

| Illicit trade | 5–10% |

| E‑commerce share | ~22% |

Preview Before You Purchase

ITC Porter's Five Forces Analysis

This preview shows the full Porter's Five Forces analysis for ITC, covering supplier and buyer power, competitive rivalry, and threats of substitution and entry. The document you see is the exact file delivered after purchase—fully formatted and ready for download. No placeholders or summaries; the analysis is complete and actionable for strategy, valuation, or market assessment.

Go Beyond the Preview—Access the Full Strategic Report

ITC’s Porter's Five Forces snapshot highlights bargaining power of suppliers and buyers, threat of new entrants, competitive rivalry, and substitute pressures that shape its margins and strategic choices. This brief teases key dynamics; unlock the full analysis for force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Diversified input base tempers leverage

ITC sources tobacco, agri-commodities, pulp, energy, fragrances and hospitality supplies across regions, diluting any single supplier’s clout. Multi-sourcing and import optionality cap price escalation and support stable margins. Commodity cycles—especially tobacco and pulp—can still swing input costs. Strategic procurement and hedging reduce volatility but cannot fully eliminate cyclical exposure.

Backward integration lowers dependence

ITC’s agri-sourcing platforms reach over 4.5 million farmers (2024) and its captive paperboards/pulp capacity of ~1.2 mtpa gives the company clear bargaining leverage with suppliers.

Direct farm linkages improve quality, traceability and pricing power, enabling ITC to pay competitive rates while controlling input costs and standards.

Disintermediation squeezes middlemen margins, shortens lead times and enhances supply assurance for FMCG and paper businesses.

Specialty inputs retain some power

Certain leaf tobacco grades, specialty chemicals, premium packaging and hotel perishables face supply constraints, with niche suppliers often commanding premiums (commonly around 15–25% in 2024) due to tight quality specs and compliance demands. Switching costs arise from costly reformulation, regulatory re-approvals and supplier audits, sometimes delaying product changes by months. Long-term contracts and forward buys (covering a substantial share of volumes) partly mitigate supply risk and price volatility.

Regulatory and ESG constraints affect costs

Regulatory and ESG compliance in tobacco, forestry and sustainability narrows ITC’s supplier pool as stricter licensing and product restrictions limit eligible vendors.

Certified inputs (FSC for packaging, food-safety certifications) command premiums; FSC reported 226 million hectares certified in 2023, reflecting higher certified-material demand and cost pressure.

Enhanced traceability systems and third-party ESG audits raise transaction and compliance costs, and the risk of supplier non-compliance forces stricter selection and monitoring.

- Compliance-driven supplier narrowing

- Certified-material premium (FSC 226M ha, 2023)

- Higher transaction costs from traceability & audits

- Stricter supplier selection due to non-compliance risk

Logistics and energy market dynamics matter

Freight, fuel and power tariffs materially affect delivered costs; freight volatility in 2024 kept landed costs elevated versus pre‑pandemic levels. Port congestion and monsoon disruptions can tighten near‑term supply and raise spot logistics premiums. ITC’s 60+ distributed manufacturing units reduce some transport intensity, though systemic shocks can temporarily boost supplier bargaining power.

- Freight volatility 2024: elevated vs pre‑2020

- Supply tighteners: port congestion, monsoon

- Mitigation: 60+ manufacturing units

Multi-sourcing, 4.5M farmer reach stabilizes margins amid freight spikes

ITC’s multi‑sourcing, 4.5M farmer reach (2024) and ~1.2 mtpa captive pulp limit supplier clout, stabilising margins. Niche inputs (leaf grades, specialty chemicals, premium packaging) carried 15–25% premiums in 2024, sustaining pockets of supplier power. Freight/power volatility in 2024 elevated landed costs despite 60+ plants, increasing short‑term supplier leverage.

| Metric | 2024 |

|---|---|

| Farmer reach | 4.5M |

| Pulp capacity | ~1.2 mtpa |

| Supplier premium (niche) | 15–25% |

| Manufacturing units | 60+ |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, threat of new entrants and substitutes, and industry rivalry as they specifically affect ITC’s diversified FMCG, hospitality and agribusiness portfolio, highlighting strategic vulnerabilities and defensive advantages.

One-sheet Porter's Five Forces for ITC—instantly spot competitive pressures, tweak force levels with real data, and export a clean spider chart for decks or boardrooms.

Customers Bargaining Power

Fragmented consumers yet price sensitive

Retail FMCG buyers are highly fragmented across c.12 million kirana and small outlets in India (2024), limiting individual bargaining power versus FMCG majors like ITC. Yet staples and personal-care categories are intensely price sensitive, creating strong collective pressure on pricing and margin. Rising private-label assortments increase direct price comparisons, forcing sharper promotions. Pack-price architecture and targeted promotions remain essential levers to defend share and margins.

Strong brands curb switching in cigarettes

Brand loyalty and habitual use sharply curb buyer power in cigarettes; ITC held over 80% of India’s legal branded cigarette market in 2024, making switching costly. Restrictive advertising boosts entrenched brand equity, but past tax hikes have driven down-trading to lower-price segments. Illicit trade, estimated around 5–10% in recent studies, complicates pricing and margin choices.

Modern trade and e-commerce wield clout

Modern trade and e-commerce wield clout as global e-commerce reached about 22% of retail sales in 2024 and dominant platforms (Amazon ~38% of US e‑commerce) extract margins, visibility fees and data access from FMCG partners. Shelf space and algorithmic placement drive velocity, forcing ITC to balance onerous channel terms with growing direct‑to‑consumer investment. Joint business plans and exclusives align incentives and protect margins.

Institutional buyers negotiate in B2B

Institutional buyers in B2B—paperboards, packaging clients and hospitality corporates—leverage volume and specification demands to extract concessions; formal tendering frequently compresses margins. Value-added grades and integrated solutions shift negotiations from price to total cost of ownership, while service levels and sustainability certifications such as FSC and ISO 14001 act as premium differentiators.

- Volume/spec leverage

- Tendering compresses margins

- Value-added reduces price-only talks

- Service & sustainability premium

Substitute availability heightens options

Substitute availability heightens options for ITC: many categories face alternatives at similar price points, so consumers can switch to local/D2C brands or unbranded staples. Convenience and availability drive quick switching, while loyalty programs and product innovation help retain share in a market estimated at about $110 billion in 2024.

- Alternatives at parity: local/D2C/unbranded

- Availability drives quick switching

- Retention via loyalty programs and NPD

- India FMCG ≈ $110 billion (2024)

~12m kiranas, ~22% e-commerce fees, illicit 5–10% squeeze FMCG margins

Retail FMCG buyers hugely fragmented (~12m kiranas, 2024) limiting individual power; price sensitivity and private labels pressure margins. Cigarette buyers constrained by brand loyalty—ITC >80% legal market (2024)—but taxes and illicit trade (5–10%) compress value. Modern trade/e‑commerce (~22% digital share, 2024) extract fees, raising channel leverage.

| Metric | 2024 |

|---|---|

| Kirana outlets | ~12m |

| ITC cigarette share | >80% |

| Illicit trade | 5–10% |

| E‑commerce share | ~22% |

Preview Before You Purchase

ITC Porter's Five Forces Analysis

This preview shows the full Porter's Five Forces analysis for ITC, covering supplier and buyer power, competitive rivalry, and threats of substitution and entry. The document you see is the exact file delivered after purchase—fully formatted and ready for download. No placeholders or summaries; the analysis is complete and actionable for strategy, valuation, or market assessment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

ITC’s Porter's Five Forces snapshot highlights bargaining power of suppliers and buyers, threat of new entrants, competitive rivalry, and substitute pressures that shape its margins and strategic choices. This brief teases key dynamics; unlock the full analysis for force-by-force ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Diversified input base tempers leverage

ITC sources tobacco, agri-commodities, pulp, energy, fragrances and hospitality supplies across regions, diluting any single supplier’s clout. Multi-sourcing and import optionality cap price escalation and support stable margins. Commodity cycles—especially tobacco and pulp—can still swing input costs. Strategic procurement and hedging reduce volatility but cannot fully eliminate cyclical exposure.

Backward integration lowers dependence

ITC’s agri-sourcing platforms reach over 4.5 million farmers (2024) and its captive paperboards/pulp capacity of ~1.2 mtpa gives the company clear bargaining leverage with suppliers.

Direct farm linkages improve quality, traceability and pricing power, enabling ITC to pay competitive rates while controlling input costs and standards.

Disintermediation squeezes middlemen margins, shortens lead times and enhances supply assurance for FMCG and paper businesses.

Specialty inputs retain some power

Certain leaf tobacco grades, specialty chemicals, premium packaging and hotel perishables face supply constraints, with niche suppliers often commanding premiums (commonly around 15–25% in 2024) due to tight quality specs and compliance demands. Switching costs arise from costly reformulation, regulatory re-approvals and supplier audits, sometimes delaying product changes by months. Long-term contracts and forward buys (covering a substantial share of volumes) partly mitigate supply risk and price volatility.

Regulatory and ESG constraints affect costs

Regulatory and ESG compliance in tobacco, forestry and sustainability narrows ITC’s supplier pool as stricter licensing and product restrictions limit eligible vendors.

Certified inputs (FSC for packaging, food-safety certifications) command premiums; FSC reported 226 million hectares certified in 2023, reflecting higher certified-material demand and cost pressure.

Enhanced traceability systems and third-party ESG audits raise transaction and compliance costs, and the risk of supplier non-compliance forces stricter selection and monitoring.

- Compliance-driven supplier narrowing

- Certified-material premium (FSC 226M ha, 2023)

- Higher transaction costs from traceability & audits

- Stricter supplier selection due to non-compliance risk

Logistics and energy market dynamics matter

Freight, fuel and power tariffs materially affect delivered costs; freight volatility in 2024 kept landed costs elevated versus pre‑pandemic levels. Port congestion and monsoon disruptions can tighten near‑term supply and raise spot logistics premiums. ITC’s 60+ distributed manufacturing units reduce some transport intensity, though systemic shocks can temporarily boost supplier bargaining power.

- Freight volatility 2024: elevated vs pre‑2020

- Supply tighteners: port congestion, monsoon

- Mitigation: 60+ manufacturing units

Multi-sourcing, 4.5M farmer reach stabilizes margins amid freight spikes

ITC’s multi‑sourcing, 4.5M farmer reach (2024) and ~1.2 mtpa captive pulp limit supplier clout, stabilising margins. Niche inputs (leaf grades, specialty chemicals, premium packaging) carried 15–25% premiums in 2024, sustaining pockets of supplier power. Freight/power volatility in 2024 elevated landed costs despite 60+ plants, increasing short‑term supplier leverage.

| Metric | 2024 |

|---|---|

| Farmer reach | 4.5M |

| Pulp capacity | ~1.2 mtpa |

| Supplier premium (niche) | 15–25% |

| Manufacturing units | 60+ |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, threat of new entrants and substitutes, and industry rivalry as they specifically affect ITC’s diversified FMCG, hospitality and agribusiness portfolio, highlighting strategic vulnerabilities and defensive advantages.

One-sheet Porter's Five Forces for ITC—instantly spot competitive pressures, tweak force levels with real data, and export a clean spider chart for decks or boardrooms.

Customers Bargaining Power

Fragmented consumers yet price sensitive

Retail FMCG buyers are highly fragmented across c.12 million kirana and small outlets in India (2024), limiting individual bargaining power versus FMCG majors like ITC. Yet staples and personal-care categories are intensely price sensitive, creating strong collective pressure on pricing and margin. Rising private-label assortments increase direct price comparisons, forcing sharper promotions. Pack-price architecture and targeted promotions remain essential levers to defend share and margins.

Strong brands curb switching in cigarettes

Brand loyalty and habitual use sharply curb buyer power in cigarettes; ITC held over 80% of India’s legal branded cigarette market in 2024, making switching costly. Restrictive advertising boosts entrenched brand equity, but past tax hikes have driven down-trading to lower-price segments. Illicit trade, estimated around 5–10% in recent studies, complicates pricing and margin choices.

Modern trade and e-commerce wield clout

Modern trade and e-commerce wield clout as global e-commerce reached about 22% of retail sales in 2024 and dominant platforms (Amazon ~38% of US e‑commerce) extract margins, visibility fees and data access from FMCG partners. Shelf space and algorithmic placement drive velocity, forcing ITC to balance onerous channel terms with growing direct‑to‑consumer investment. Joint business plans and exclusives align incentives and protect margins.

Institutional buyers negotiate in B2B

Institutional buyers in B2B—paperboards, packaging clients and hospitality corporates—leverage volume and specification demands to extract concessions; formal tendering frequently compresses margins. Value-added grades and integrated solutions shift negotiations from price to total cost of ownership, while service levels and sustainability certifications such as FSC and ISO 14001 act as premium differentiators.

- Volume/spec leverage

- Tendering compresses margins

- Value-added reduces price-only talks

- Service & sustainability premium

Substitute availability heightens options

Substitute availability heightens options for ITC: many categories face alternatives at similar price points, so consumers can switch to local/D2C brands or unbranded staples. Convenience and availability drive quick switching, while loyalty programs and product innovation help retain share in a market estimated at about $110 billion in 2024.

- Alternatives at parity: local/D2C/unbranded

- Availability drives quick switching

- Retention via loyalty programs and NPD

- India FMCG ≈ $110 billion (2024)

~12m kiranas, ~22% e-commerce fees, illicit 5–10% squeeze FMCG margins

Retail FMCG buyers hugely fragmented (~12m kiranas, 2024) limiting individual power; price sensitivity and private labels pressure margins. Cigarette buyers constrained by brand loyalty—ITC >80% legal market (2024)—but taxes and illicit trade (5–10%) compress value. Modern trade/e‑commerce (~22% digital share, 2024) extract fees, raising channel leverage.

| Metric | 2024 |

|---|---|

| Kirana outlets | ~12m |

| ITC cigarette share | >80% |

| Illicit trade | 5–10% |

| E‑commerce share | ~22% |

Preview Before You Purchase

ITC Porter's Five Forces Analysis

This preview shows the full Porter's Five Forces analysis for ITC, covering supplier and buyer power, competitive rivalry, and threats of substitution and entry. The document you see is the exact file delivered after purchase—fully formatted and ready for download. No placeholders or summaries; the analysis is complete and actionable for strategy, valuation, or market assessment.