Itochu Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

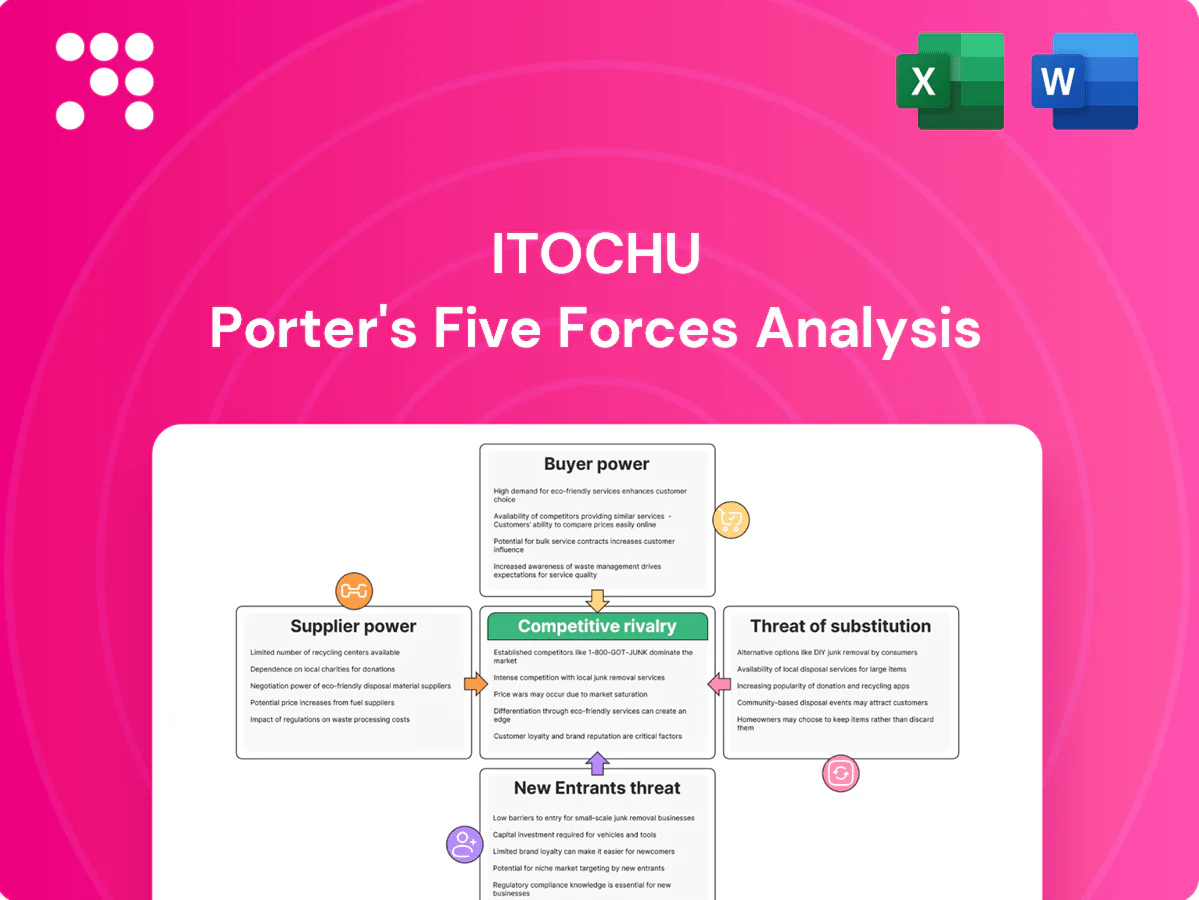

Itochu's Porter's Five Forces snapshot highlights supplier clout across global supply chains, moderate buyer power, high threat from substitutes in commodities, and competitive rivalry among trading houses shaping margins. Regulatory and entry barriers temper new entrants but shift with trade policies. This brief teases strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals and actionable recommendations.

Suppliers Bargaining Power

Diversified global supplier base

Itochu sources from a diversified global supplier base across commodities, food, textiles and chemicals (per its FY2024 Integrated Report), diluting individual supplier leverage; portfolio breadth enables switching and cross-sourcing to mitigate disruptions; long-term ties lower coordination costs but limit supplier hold-up, tempering supplier power across cycles.

Concentration in key commodities

In metals, energy and specialty chemicals a handful of producers or resource nations can set price and volume: OPEC+ supplies roughly 50% of global oil, while China controls about 60% of rare earth output, concentrating upstream leverage. Contract indexation and OPEC-like dynamics transmit volatility downstream; Itochu mitigates via offtake diversification and financial hedges, though exposure rises sharply during tight supply or geopolitical stress.

Value-added partnerships vs. spot

Itochu reduces supplier bargaining by using strategic JVs and equity stakes—backing relationships across over 900 subsidiaries and affiliates as of March 31, 2024—aligning incentives and lowering pricing friction. Where procurement is on spot markets, suppliers retain greater pricing latitude, increasing volatility. A blended procurement mix balances cost and reliability. Partnership depth varies by segment, creating asymmetric supplier power across Itochu’s portfolio.

Logistics and compliance constraints

Specialized logistics, certification, and ESG traceability raise switching costs for Itochu, concentrating supplier leverage as certified providers are scarcer; in 2024 Itochu scaled ESG audits across roughly 1,200 high‑risk suppliers, narrowing alternatives and raising supplier bargaining power. Itochu’s compliance capability widens the qualified pool, but tighter regulation can rapidly re‑concentrate power.

- Higher switching costs

- ~1,200 audited high‑risk suppliers (2024)

- Compliance widens qualified pool

- Regulatory tightening increases supplier leverage

Technology and data transparency

Market intelligence, e-sourcing and real-time pricing reduce information asymmetry for Itochu, with McKinsey estimates showing digital procurement can lower sourcing costs by 10–20% and accelerate decision cycles; transparent benchmarks curb opportunistic pricing, though differentiated inputs retain scarcity premiums that data cannot fully eliminate. Supplier power falls most where commoditization and data depth are highest.

- Market intelligence: lowers asymmetry

- e-sourcing: improves sourcing speed

- Real-time pricing: limits opportunism

- Differentiated inputs: preserve scarcity premiums

Moderate supplier power: diversified sourcing offsets oil and rare-earth concentration risks

Itochu faces moderate supplier power: diversified sourcing and 900+ subsidiaries (Mar 31, 2024) dilute leverage, but concentrated inputs in oil and rare earths elevate upstream pricing risk. Strategic JVs, offtakes and 1,200 audited high‑risk suppliers (2024) reduce hold‑up, while spot buying and certified providers raise switching costs and volatility.

| Metric | Value (2024) |

|---|---|

| Subsidiaries/Affiliates | 900+ |

| Audited high‑risk suppliers | 1,200 |

| OPEC+ oil share | ~50% |

| China rare earths | ~60% |

| Digital procurement savings | 10–20% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Itochu, evaluating supplier and buyer power, competitive rivalry, threats from new entrants and substitutes, and disruptive trends; highlights market entry barriers, pricing and profitability levers, and strategic actions to protect and grow Itochu’s competitive position.

A concise, one‑sheet Porter's Five Forces for Itochu—quick decision-ready summary with customizable pressure levels, spider chart visualization, scenario tabs, copy‑ready layout for decks, no complex code, and seamless Excel/Word integration so you can swap in current data and relieve strategic analysis bottlenecks.

Customers Bargaining Power

Large buyers with scale

Large global F&B, retail and manufacturing buyers purchase at scale and in 2024 pushed for sharper terms, frequent re-tendering and multi-sourcing to reduce risk. Itochu responds with bundled product-logistics-financing packages to deepen ties and offer credit solutions. Despite this, top accounts still exert significant price and service pressure on margins.

Switching ease in commoditized lines

In grains, base metals and generic textiles specifications are standard and switching costs are low, so customers pivot among traders on price and delivery. In 2024 commodity trading margins remained compressed, typically below 3%, keeping price the primary lever. Itochu offsets this by emphasizing reliability, advanced risk management and superior logistics performance to retain volume. Thin margins persist where product is undifferentiated.

Embedded solutions and financing

Where Itochu bundles integrated supply, inventory management and trade finance, buyer dependence rises as customers rely on one-stop logistics and liquidity support. These services increase stickiness and reduce direct price haggling by shifting negotiations toward service levels and reliability. Customized solutions reframe discussions around total cost of ownership and lifecycle value. That softens buyer power despite visible price sensitivity.

Regulatory and ESG requirements

End-customers are raising traceability, emissions and ethical sourcing demands; in 2024 the EU CSRD began applying to large firms, increasing disclosure expectations. Fewer suppliers can comply at scale, narrowing alternatives and enabling Itochu to command premiums via compliance capabilities, which reduces buyer leverage. Buyers may still push ESG requirements without paying higher prices.

- CSRD 2024: higher disclosure

- Fewer compliant suppliers = fewer alternatives

- Itochu compliance = premium potential

- Buyers may demand ESG without price uplift

Digital channel transparency

Real-time benchmarks and trading platforms in 2024 gave buyers greater pricing visibility, driving information parity that strengthens negotiation positions; Itochu uses advanced data analytics to tailor offers and hedge exposures, compressing spreads while accelerating contract cycles. Net effect: tighter spreads, faster and more resilient contracting across commodity and logistics deals.

Buyers push margins under 3%; > 60% use digital discovery

Large global buyers in 2024 pressed for sharper terms; top accounts still drive price and service pressure, compressing margins.

Commodity margins remained below 3% in 2024 while >60% of corporate buyers used digital price discovery, increasing information parity.

Bundled supply-finance-logistics and CSRD-driven compliance lift stickiness and permit premiums despite buyer ESG price pushback.

| Metric | 2024 |

|---|---|

| Corp buyers using digital discovery | >60% |

| Typical commodity trading margin | <3% |

| CSRD applicability | In force for large firms 2024 |

What You See Is What You Get

Itochu Porter's Five Forces Analysis

This preview is the exact Itochu Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. It contains a comprehensive assessment of competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, plus actionable insights for strategy and investment decisions.

A Must-Have Tool for Decision-Makers

Itochu's Porter's Five Forces snapshot highlights supplier clout across global supply chains, moderate buyer power, high threat from substitutes in commodities, and competitive rivalry among trading houses shaping margins. Regulatory and entry barriers temper new entrants but shift with trade policies. This brief teases strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals and actionable recommendations.

Suppliers Bargaining Power

Diversified global supplier base

Itochu sources from a diversified global supplier base across commodities, food, textiles and chemicals (per its FY2024 Integrated Report), diluting individual supplier leverage; portfolio breadth enables switching and cross-sourcing to mitigate disruptions; long-term ties lower coordination costs but limit supplier hold-up, tempering supplier power across cycles.

Concentration in key commodities

In metals, energy and specialty chemicals a handful of producers or resource nations can set price and volume: OPEC+ supplies roughly 50% of global oil, while China controls about 60% of rare earth output, concentrating upstream leverage. Contract indexation and OPEC-like dynamics transmit volatility downstream; Itochu mitigates via offtake diversification and financial hedges, though exposure rises sharply during tight supply or geopolitical stress.

Value-added partnerships vs. spot

Itochu reduces supplier bargaining by using strategic JVs and equity stakes—backing relationships across over 900 subsidiaries and affiliates as of March 31, 2024—aligning incentives and lowering pricing friction. Where procurement is on spot markets, suppliers retain greater pricing latitude, increasing volatility. A blended procurement mix balances cost and reliability. Partnership depth varies by segment, creating asymmetric supplier power across Itochu’s portfolio.

Logistics and compliance constraints

Specialized logistics, certification, and ESG traceability raise switching costs for Itochu, concentrating supplier leverage as certified providers are scarcer; in 2024 Itochu scaled ESG audits across roughly 1,200 high‑risk suppliers, narrowing alternatives and raising supplier bargaining power. Itochu’s compliance capability widens the qualified pool, but tighter regulation can rapidly re‑concentrate power.

- Higher switching costs

- ~1,200 audited high‑risk suppliers (2024)

- Compliance widens qualified pool

- Regulatory tightening increases supplier leverage

Technology and data transparency

Market intelligence, e-sourcing and real-time pricing reduce information asymmetry for Itochu, with McKinsey estimates showing digital procurement can lower sourcing costs by 10–20% and accelerate decision cycles; transparent benchmarks curb opportunistic pricing, though differentiated inputs retain scarcity premiums that data cannot fully eliminate. Supplier power falls most where commoditization and data depth are highest.

- Market intelligence: lowers asymmetry

- e-sourcing: improves sourcing speed

- Real-time pricing: limits opportunism

- Differentiated inputs: preserve scarcity premiums

Moderate supplier power: diversified sourcing offsets oil and rare-earth concentration risks

Itochu faces moderate supplier power: diversified sourcing and 900+ subsidiaries (Mar 31, 2024) dilute leverage, but concentrated inputs in oil and rare earths elevate upstream pricing risk. Strategic JVs, offtakes and 1,200 audited high‑risk suppliers (2024) reduce hold‑up, while spot buying and certified providers raise switching costs and volatility.

| Metric | Value (2024) |

|---|---|

| Subsidiaries/Affiliates | 900+ |

| Audited high‑risk suppliers | 1,200 |

| OPEC+ oil share | ~50% |

| China rare earths | ~60% |

| Digital procurement savings | 10–20% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Itochu, evaluating supplier and buyer power, competitive rivalry, threats from new entrants and substitutes, and disruptive trends; highlights market entry barriers, pricing and profitability levers, and strategic actions to protect and grow Itochu’s competitive position.

A concise, one‑sheet Porter's Five Forces for Itochu—quick decision-ready summary with customizable pressure levels, spider chart visualization, scenario tabs, copy‑ready layout for decks, no complex code, and seamless Excel/Word integration so you can swap in current data and relieve strategic analysis bottlenecks.

Customers Bargaining Power

Large buyers with scale

Large global F&B, retail and manufacturing buyers purchase at scale and in 2024 pushed for sharper terms, frequent re-tendering and multi-sourcing to reduce risk. Itochu responds with bundled product-logistics-financing packages to deepen ties and offer credit solutions. Despite this, top accounts still exert significant price and service pressure on margins.

Switching ease in commoditized lines

In grains, base metals and generic textiles specifications are standard and switching costs are low, so customers pivot among traders on price and delivery. In 2024 commodity trading margins remained compressed, typically below 3%, keeping price the primary lever. Itochu offsets this by emphasizing reliability, advanced risk management and superior logistics performance to retain volume. Thin margins persist where product is undifferentiated.

Embedded solutions and financing

Where Itochu bundles integrated supply, inventory management and trade finance, buyer dependence rises as customers rely on one-stop logistics and liquidity support. These services increase stickiness and reduce direct price haggling by shifting negotiations toward service levels and reliability. Customized solutions reframe discussions around total cost of ownership and lifecycle value. That softens buyer power despite visible price sensitivity.

Regulatory and ESG requirements

End-customers are raising traceability, emissions and ethical sourcing demands; in 2024 the EU CSRD began applying to large firms, increasing disclosure expectations. Fewer suppliers can comply at scale, narrowing alternatives and enabling Itochu to command premiums via compliance capabilities, which reduces buyer leverage. Buyers may still push ESG requirements without paying higher prices.

- CSRD 2024: higher disclosure

- Fewer compliant suppliers = fewer alternatives

- Itochu compliance = premium potential

- Buyers may demand ESG without price uplift

Digital channel transparency

Real-time benchmarks and trading platforms in 2024 gave buyers greater pricing visibility, driving information parity that strengthens negotiation positions; Itochu uses advanced data analytics to tailor offers and hedge exposures, compressing spreads while accelerating contract cycles. Net effect: tighter spreads, faster and more resilient contracting across commodity and logistics deals.

Buyers push margins under 3%; > 60% use digital discovery

Large global buyers in 2024 pressed for sharper terms; top accounts still drive price and service pressure, compressing margins.

Commodity margins remained below 3% in 2024 while >60% of corporate buyers used digital price discovery, increasing information parity.

Bundled supply-finance-logistics and CSRD-driven compliance lift stickiness and permit premiums despite buyer ESG price pushback.

| Metric | 2024 |

|---|---|

| Corp buyers using digital discovery | >60% |

| Typical commodity trading margin | <3% |

| CSRD applicability | In force for large firms 2024 |

What You See Is What You Get

Itochu Porter's Five Forces Analysis

This preview is the exact Itochu Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. It contains a comprehensive assessment of competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, plus actionable insights for strategy and investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Itochu's Porter's Five Forces snapshot highlights supplier clout across global supply chains, moderate buyer power, high threat from substitutes in commodities, and competitive rivalry among trading houses shaping margins. Regulatory and entry barriers temper new entrants but shift with trade policies. This brief teases strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals and actionable recommendations.

Suppliers Bargaining Power

Diversified global supplier base

Itochu sources from a diversified global supplier base across commodities, food, textiles and chemicals (per its FY2024 Integrated Report), diluting individual supplier leverage; portfolio breadth enables switching and cross-sourcing to mitigate disruptions; long-term ties lower coordination costs but limit supplier hold-up, tempering supplier power across cycles.

Concentration in key commodities

In metals, energy and specialty chemicals a handful of producers or resource nations can set price and volume: OPEC+ supplies roughly 50% of global oil, while China controls about 60% of rare earth output, concentrating upstream leverage. Contract indexation and OPEC-like dynamics transmit volatility downstream; Itochu mitigates via offtake diversification and financial hedges, though exposure rises sharply during tight supply or geopolitical stress.

Value-added partnerships vs. spot

Itochu reduces supplier bargaining by using strategic JVs and equity stakes—backing relationships across over 900 subsidiaries and affiliates as of March 31, 2024—aligning incentives and lowering pricing friction. Where procurement is on spot markets, suppliers retain greater pricing latitude, increasing volatility. A blended procurement mix balances cost and reliability. Partnership depth varies by segment, creating asymmetric supplier power across Itochu’s portfolio.

Logistics and compliance constraints

Specialized logistics, certification, and ESG traceability raise switching costs for Itochu, concentrating supplier leverage as certified providers are scarcer; in 2024 Itochu scaled ESG audits across roughly 1,200 high‑risk suppliers, narrowing alternatives and raising supplier bargaining power. Itochu’s compliance capability widens the qualified pool, but tighter regulation can rapidly re‑concentrate power.

- Higher switching costs

- ~1,200 audited high‑risk suppliers (2024)

- Compliance widens qualified pool

- Regulatory tightening increases supplier leverage

Technology and data transparency

Market intelligence, e-sourcing and real-time pricing reduce information asymmetry for Itochu, with McKinsey estimates showing digital procurement can lower sourcing costs by 10–20% and accelerate decision cycles; transparent benchmarks curb opportunistic pricing, though differentiated inputs retain scarcity premiums that data cannot fully eliminate. Supplier power falls most where commoditization and data depth are highest.

- Market intelligence: lowers asymmetry

- e-sourcing: improves sourcing speed

- Real-time pricing: limits opportunism

- Differentiated inputs: preserve scarcity premiums

Moderate supplier power: diversified sourcing offsets oil and rare-earth concentration risks

Itochu faces moderate supplier power: diversified sourcing and 900+ subsidiaries (Mar 31, 2024) dilute leverage, but concentrated inputs in oil and rare earths elevate upstream pricing risk. Strategic JVs, offtakes and 1,200 audited high‑risk suppliers (2024) reduce hold‑up, while spot buying and certified providers raise switching costs and volatility.

| Metric | Value (2024) |

|---|---|

| Subsidiaries/Affiliates | 900+ |

| Audited high‑risk suppliers | 1,200 |

| OPEC+ oil share | ~50% |

| China rare earths | ~60% |

| Digital procurement savings | 10–20% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Itochu, evaluating supplier and buyer power, competitive rivalry, threats from new entrants and substitutes, and disruptive trends; highlights market entry barriers, pricing and profitability levers, and strategic actions to protect and grow Itochu’s competitive position.

A concise, one‑sheet Porter's Five Forces for Itochu—quick decision-ready summary with customizable pressure levels, spider chart visualization, scenario tabs, copy‑ready layout for decks, no complex code, and seamless Excel/Word integration so you can swap in current data and relieve strategic analysis bottlenecks.

Customers Bargaining Power

Large buyers with scale

Large global F&B, retail and manufacturing buyers purchase at scale and in 2024 pushed for sharper terms, frequent re-tendering and multi-sourcing to reduce risk. Itochu responds with bundled product-logistics-financing packages to deepen ties and offer credit solutions. Despite this, top accounts still exert significant price and service pressure on margins.

Switching ease in commoditized lines

In grains, base metals and generic textiles specifications are standard and switching costs are low, so customers pivot among traders on price and delivery. In 2024 commodity trading margins remained compressed, typically below 3%, keeping price the primary lever. Itochu offsets this by emphasizing reliability, advanced risk management and superior logistics performance to retain volume. Thin margins persist where product is undifferentiated.

Embedded solutions and financing

Where Itochu bundles integrated supply, inventory management and trade finance, buyer dependence rises as customers rely on one-stop logistics and liquidity support. These services increase stickiness and reduce direct price haggling by shifting negotiations toward service levels and reliability. Customized solutions reframe discussions around total cost of ownership and lifecycle value. That softens buyer power despite visible price sensitivity.

Regulatory and ESG requirements

End-customers are raising traceability, emissions and ethical sourcing demands; in 2024 the EU CSRD began applying to large firms, increasing disclosure expectations. Fewer suppliers can comply at scale, narrowing alternatives and enabling Itochu to command premiums via compliance capabilities, which reduces buyer leverage. Buyers may still push ESG requirements without paying higher prices.

- CSRD 2024: higher disclosure

- Fewer compliant suppliers = fewer alternatives

- Itochu compliance = premium potential

- Buyers may demand ESG without price uplift

Digital channel transparency

Real-time benchmarks and trading platforms in 2024 gave buyers greater pricing visibility, driving information parity that strengthens negotiation positions; Itochu uses advanced data analytics to tailor offers and hedge exposures, compressing spreads while accelerating contract cycles. Net effect: tighter spreads, faster and more resilient contracting across commodity and logistics deals.

Buyers push margins under 3%; > 60% use digital discovery

Large global buyers in 2024 pressed for sharper terms; top accounts still drive price and service pressure, compressing margins.

Commodity margins remained below 3% in 2024 while >60% of corporate buyers used digital price discovery, increasing information parity.

Bundled supply-finance-logistics and CSRD-driven compliance lift stickiness and permit premiums despite buyer ESG price pushback.

| Metric | 2024 |

|---|---|

| Corp buyers using digital discovery | >60% |

| Typical commodity trading margin | <3% |

| CSRD applicability | In force for large firms 2024 |

What You See Is What You Get

Itochu Porter's Five Forces Analysis

This preview is the exact Itochu Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. It contains a comprehensive assessment of competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, plus actionable insights for strategy and investment decisions.