Itron Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

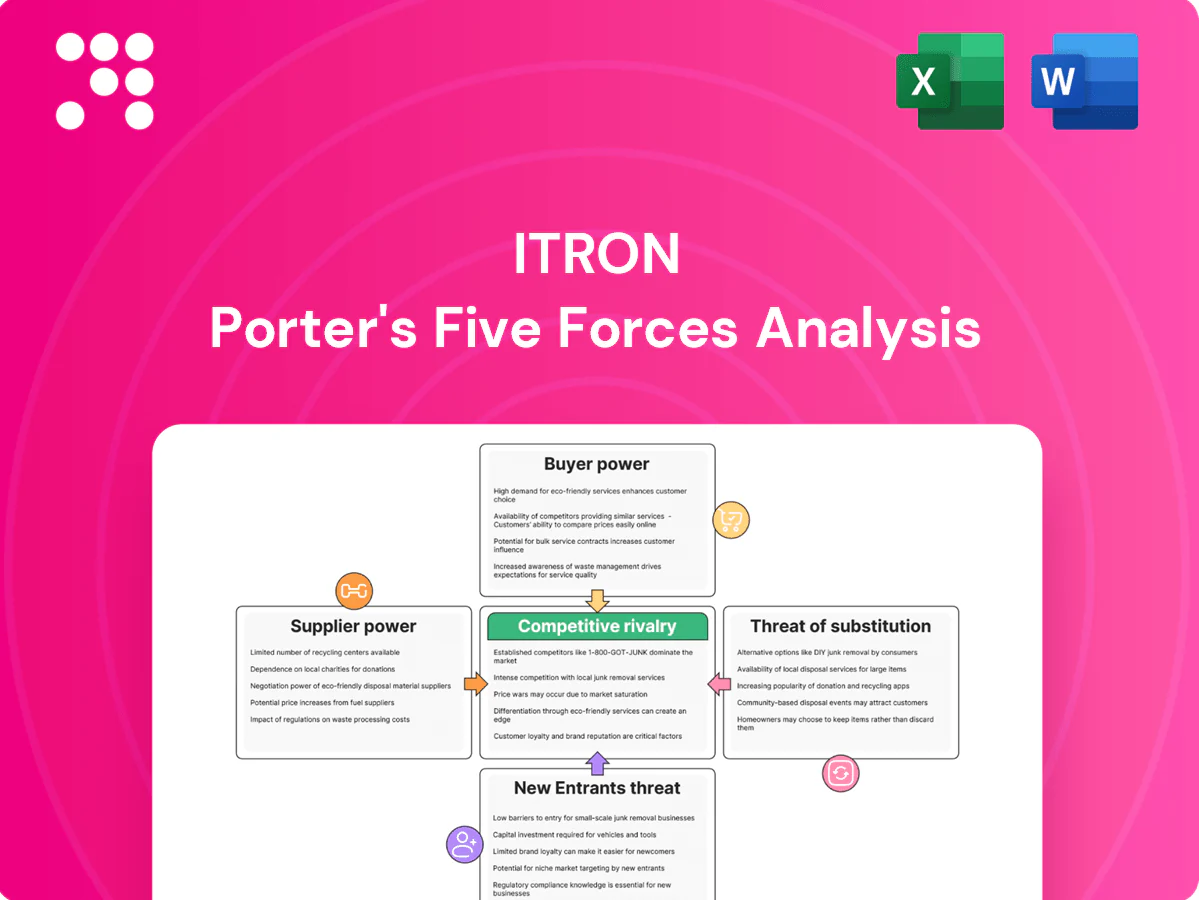

Itron’s Porter’s Five Forces analysis highlights rivalry in smart metering, supplier leverage from specialized component vendors, moderate buyer power from utilities, threats from IoT entrants, and substitute risks from energy-management platforms. This snapshot frames key strategic pressure points. The full report reveals the real forces shaping Itron’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore Itron’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor sources

Itron depends on a limited set of advanced chipmakers for MCUs, RF SoCs and secure elements, creating concentrated supplier power. Global foundry concentration (TSMC ~55% share in 2023) and node transitions can push pricing to suppliers, while qualification cycles of 6–18 months make rapid second-sourcing difficult. Strategic long-term supply agreements and redesigns have partially mitigated but not eliminated this risk.

Specialized RF and communications modules

Specialized licensed/unlicensed RF, LTE-M/NB-IoT and mesh modules come from niche suppliers, limiting Itron's swap options as performance and FCC/CE certifications commonly exceed $50,000 and add months to qualification. Vendors extract leverage via proprietary protocol stacks and royalty models, with supplier gross margins often higher than commodity silicon peers. Itron's multi-modem roadmaps and adoption of open standards (LoRaWAN, 3GPP IoT) reduce single-vendor dependency.

Battery and sensor component dependencies

Smart meters and endpoints require long-life batteries (typically 10–15 years) and metrology sensors meeting utility accuracy standards (around ±0.5% or better), which narrows qualified suppliers and raises switching costs. Quality and safety certifications limit the supplier base, concentrating bargaining power among certified vendors. Lithium and rare material price volatility—notably large swings between 2022–2024—squeezes margins, so Itron relies on dual-sourcing and inventory buffers to stabilize supply and costs.

Cloud and software infrastructure providers

AMI head-end, analytics and SaaS mostly run on hyperscale clouds (AWS ~32%, Azure ~23%, GCP ~11% in 2024), giving suppliers leverage. Switching clouds is feasible but data egress fees and re-architecture create material friction amid $597B public cloud spend in 2024. Providers influence costs via usage pricing and service bundling; multi-cloud and containerization improve optionality.

- Vendor concentration: hyperscalers dominant

- Cost levers: egress, consumption tiers, bundles

- Mitigants: multi-cloud, containers, abstraction layers

Firmware, security IP, and standards compliance

Security libraries, PKI and protocol stacks are often licensed from specialists, giving suppliers leverage because compliance to DLMS/COSEM, IEEE and OCPP ties firmware updates to vendor roadmaps and can delay certifications. Suppliers gain further power when third-party IP is a certification prerequisite. Building in-house stacks reduces this exposure and shortens dependency-driven timelines.

- Supplier IP can gate certifications

- Standards lock updates to vendor roadmaps

- In-house stacks cut dependency risk

Concentrated silicon and cloud supplier power raising costs; mitigated by dual-sourcing

Itron faces concentrated supplier power across advanced silicon (TSMC ~55% share in 2023), niche RF/modem vendors, long-life battery/metrology suppliers and hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024), raising switching costs, certification friction and input-price volatility observed 2022–2024. Mitigants: dual-sourcing, long-term contracts, multi-cloud and in-house stacks.

| Category | Key metric | Impact |

|---|---|---|

| Foundries | TSMC ~55% (2023) | High concentration |

| Cloud | AWS 32%/Azure 23%/GCP 11% (2024) | Vendor leverage |

| Cloud spend | $597B (2024) | egress/pricing risk |

What is included in the product

Tailored Porter's Five Forces analysis for Itron, uncovering competitive intensity, buyer and supplier bargaining power, threats from substitutes and new entrants, and highlighting disruptive technologies and regulatory shifts that affect its pricing, margins, and market positioning.

Clear one-sheet Porter's Five Forces for Itron—pinpoints competitive pain points and priorities for quick strategic decisions, with customizable pressure levels and a radar view ready for decks or dashboards.

Customers Bargaining Power

Large, concentrated utility customers

Investor-owned utilities and large municipalities buy at scale via competitive RFPs, with many meter and grid contracts in 2024 exceeding $10M per award, concentrating buying power and squeezing supplier margins. Concentration gives buyers leverage to demand lower prices and tougher contract terms; visible wins and referenceability further amplify price pressure across peers. Suppliers often accept multi-year deals (commonly 3-5 years) trading margin for volume certainty.

High switching costs but formal procurement

Integration with CIS/MDM, head-end systems and field ops creates high switching costs for Itron customers by tying billing, analytics and operations together; nonetheless periodic public tenders enforce competitive bidding and price transparency, as buyers routinely demand interoperability tests and pilot programs to de-risk migration, so incumbency provides advantage but is not decisive.

Performance, reliability, and SLAs driven

Utilities demand accuracy, uptime, cybersecurity, and strict SLAs; common uptime targets cited across industry contracts are 99.99% (≈52.6 minutes downtime/year), with formal acceptance testing and security certifications required. Penalties and acceptance testing legally shift operational and financial risk to vendors, increasing customer leverage in negotiations. Consistently strong performance allows vendors to command premium pricing, while high-profile failures rapidly erase bargaining power and invite contract penalties or termination.

Total cost of ownership focus

Buyers increasingly evaluate TCO across device, communications, installation and maintenance, favoring solutions where analytics and outage-reduction capabilities offset higher unit prices; industry reports in 2024 note double-digit TCO savings for analytics-enabled deployments. Unbundling of services pressures hardware margins, while vertically bundled solutions (hardware+software+services) allow suppliers to reclaim value capture and sustain pricing.

- TCO-focused procurement

- Analytics-driven savings

- Unbundling depresses hardware margins

- Bundled solutions reclaim value

Regulatory and standards requirements

Compliance mandates shape specs and vendor eligibility, with utilities and municipalities enforcing IEEE, IEC and ANSI-aligned requirements that prioritize interoperability and data security. Buyers leverage these standards to avoid lock-in; certification gates, which commonly take 3–12 months and cost roughly 10,000–100,000 USD, reduce the vendor pool and heighten competition among qualified suppliers. Custom local requirements and legacy integrations can still limit buyer options.

- Standards enforced: IEEE, IEC, ANSI

- Certification impact: 3–12 months, 10k–100k USD

- Buyer leverage: interoperability to prevent lock-in

- Constraint: local/legacy requirements reduce choices

Utilities use $10M+ RFPs to secure 3-5yr deals, driving double-digit TCO savings

Large utilities and municipalities concentrate buying power via $10M+ RFPs in 2024, forcing price concessions and multi-year (3–5yr) deals for volume certainty. High switching costs from CIS/MDM integration limit churn but public tenders and certifications (3–12m, $10k–$100k) sustain competition. TCO and analytics drive procurement, producing reported double-digit TCO savings.

| Metric | 2024 value |

|---|---|

| Typical award size | $10M+ |

| Contract length | 3–5 yrs |

| Cert cost/time | $10k–$100k / 3–12m |

| TCO savings | Double-digit % |

Full Version Awaits

Itron Porter's Five Forces Analysis

This Itron Porter's Five Forces Analysis provides a concise, professionally formatted evaluation of industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to Itron. This preview is the exact file you’ll receive after purchase—no placeholders, no mockups. Once bought, you get immediate access to the same ready-to-use document.

A Must-Have Tool for Decision-Makers

Itron’s Porter’s Five Forces analysis highlights rivalry in smart metering, supplier leverage from specialized component vendors, moderate buyer power from utilities, threats from IoT entrants, and substitute risks from energy-management platforms. This snapshot frames key strategic pressure points. The full report reveals the real forces shaping Itron’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore Itron’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor sources

Itron depends on a limited set of advanced chipmakers for MCUs, RF SoCs and secure elements, creating concentrated supplier power. Global foundry concentration (TSMC ~55% share in 2023) and node transitions can push pricing to suppliers, while qualification cycles of 6–18 months make rapid second-sourcing difficult. Strategic long-term supply agreements and redesigns have partially mitigated but not eliminated this risk.

Specialized RF and communications modules

Specialized licensed/unlicensed RF, LTE-M/NB-IoT and mesh modules come from niche suppliers, limiting Itron's swap options as performance and FCC/CE certifications commonly exceed $50,000 and add months to qualification. Vendors extract leverage via proprietary protocol stacks and royalty models, with supplier gross margins often higher than commodity silicon peers. Itron's multi-modem roadmaps and adoption of open standards (LoRaWAN, 3GPP IoT) reduce single-vendor dependency.

Battery and sensor component dependencies

Smart meters and endpoints require long-life batteries (typically 10–15 years) and metrology sensors meeting utility accuracy standards (around ±0.5% or better), which narrows qualified suppliers and raises switching costs. Quality and safety certifications limit the supplier base, concentrating bargaining power among certified vendors. Lithium and rare material price volatility—notably large swings between 2022–2024—squeezes margins, so Itron relies on dual-sourcing and inventory buffers to stabilize supply and costs.

Cloud and software infrastructure providers

AMI head-end, analytics and SaaS mostly run on hyperscale clouds (AWS ~32%, Azure ~23%, GCP ~11% in 2024), giving suppliers leverage. Switching clouds is feasible but data egress fees and re-architecture create material friction amid $597B public cloud spend in 2024. Providers influence costs via usage pricing and service bundling; multi-cloud and containerization improve optionality.

- Vendor concentration: hyperscalers dominant

- Cost levers: egress, consumption tiers, bundles

- Mitigants: multi-cloud, containers, abstraction layers

Firmware, security IP, and standards compliance

Security libraries, PKI and protocol stacks are often licensed from specialists, giving suppliers leverage because compliance to DLMS/COSEM, IEEE and OCPP ties firmware updates to vendor roadmaps and can delay certifications. Suppliers gain further power when third-party IP is a certification prerequisite. Building in-house stacks reduces this exposure and shortens dependency-driven timelines.

- Supplier IP can gate certifications

- Standards lock updates to vendor roadmaps

- In-house stacks cut dependency risk

Concentrated silicon and cloud supplier power raising costs; mitigated by dual-sourcing

Itron faces concentrated supplier power across advanced silicon (TSMC ~55% share in 2023), niche RF/modem vendors, long-life battery/metrology suppliers and hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024), raising switching costs, certification friction and input-price volatility observed 2022–2024. Mitigants: dual-sourcing, long-term contracts, multi-cloud and in-house stacks.

| Category | Key metric | Impact |

|---|---|---|

| Foundries | TSMC ~55% (2023) | High concentration |

| Cloud | AWS 32%/Azure 23%/GCP 11% (2024) | Vendor leverage |

| Cloud spend | $597B (2024) | egress/pricing risk |

What is included in the product

Tailored Porter's Five Forces analysis for Itron, uncovering competitive intensity, buyer and supplier bargaining power, threats from substitutes and new entrants, and highlighting disruptive technologies and regulatory shifts that affect its pricing, margins, and market positioning.

Clear one-sheet Porter's Five Forces for Itron—pinpoints competitive pain points and priorities for quick strategic decisions, with customizable pressure levels and a radar view ready for decks or dashboards.

Customers Bargaining Power

Large, concentrated utility customers

Investor-owned utilities and large municipalities buy at scale via competitive RFPs, with many meter and grid contracts in 2024 exceeding $10M per award, concentrating buying power and squeezing supplier margins. Concentration gives buyers leverage to demand lower prices and tougher contract terms; visible wins and referenceability further amplify price pressure across peers. Suppliers often accept multi-year deals (commonly 3-5 years) trading margin for volume certainty.

High switching costs but formal procurement

Integration with CIS/MDM, head-end systems and field ops creates high switching costs for Itron customers by tying billing, analytics and operations together; nonetheless periodic public tenders enforce competitive bidding and price transparency, as buyers routinely demand interoperability tests and pilot programs to de-risk migration, so incumbency provides advantage but is not decisive.

Performance, reliability, and SLAs driven

Utilities demand accuracy, uptime, cybersecurity, and strict SLAs; common uptime targets cited across industry contracts are 99.99% (≈52.6 minutes downtime/year), with formal acceptance testing and security certifications required. Penalties and acceptance testing legally shift operational and financial risk to vendors, increasing customer leverage in negotiations. Consistently strong performance allows vendors to command premium pricing, while high-profile failures rapidly erase bargaining power and invite contract penalties or termination.

Total cost of ownership focus

Buyers increasingly evaluate TCO across device, communications, installation and maintenance, favoring solutions where analytics and outage-reduction capabilities offset higher unit prices; industry reports in 2024 note double-digit TCO savings for analytics-enabled deployments. Unbundling of services pressures hardware margins, while vertically bundled solutions (hardware+software+services) allow suppliers to reclaim value capture and sustain pricing.

- TCO-focused procurement

- Analytics-driven savings

- Unbundling depresses hardware margins

- Bundled solutions reclaim value

Regulatory and standards requirements

Compliance mandates shape specs and vendor eligibility, with utilities and municipalities enforcing IEEE, IEC and ANSI-aligned requirements that prioritize interoperability and data security. Buyers leverage these standards to avoid lock-in; certification gates, which commonly take 3–12 months and cost roughly 10,000–100,000 USD, reduce the vendor pool and heighten competition among qualified suppliers. Custom local requirements and legacy integrations can still limit buyer options.

- Standards enforced: IEEE, IEC, ANSI

- Certification impact: 3–12 months, 10k–100k USD

- Buyer leverage: interoperability to prevent lock-in

- Constraint: local/legacy requirements reduce choices

Utilities use $10M+ RFPs to secure 3-5yr deals, driving double-digit TCO savings

Large utilities and municipalities concentrate buying power via $10M+ RFPs in 2024, forcing price concessions and multi-year (3–5yr) deals for volume certainty. High switching costs from CIS/MDM integration limit churn but public tenders and certifications (3–12m, $10k–$100k) sustain competition. TCO and analytics drive procurement, producing reported double-digit TCO savings.

| Metric | 2024 value |

|---|---|

| Typical award size | $10M+ |

| Contract length | 3–5 yrs |

| Cert cost/time | $10k–$100k / 3–12m |

| TCO savings | Double-digit % |

Full Version Awaits

Itron Porter's Five Forces Analysis

This Itron Porter's Five Forces Analysis provides a concise, professionally formatted evaluation of industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to Itron. This preview is the exact file you’ll receive after purchase—no placeholders, no mockups. Once bought, you get immediate access to the same ready-to-use document.

Description

A Must-Have Tool for Decision-Makers

Itron’s Porter’s Five Forces analysis highlights rivalry in smart metering, supplier leverage from specialized component vendors, moderate buyer power from utilities, threats from IoT entrants, and substitute risks from energy-management platforms. This snapshot frames key strategic pressure points. The full report reveals the real forces shaping Itron’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore Itron’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor sources

Itron depends on a limited set of advanced chipmakers for MCUs, RF SoCs and secure elements, creating concentrated supplier power. Global foundry concentration (TSMC ~55% share in 2023) and node transitions can push pricing to suppliers, while qualification cycles of 6–18 months make rapid second-sourcing difficult. Strategic long-term supply agreements and redesigns have partially mitigated but not eliminated this risk.

Specialized RF and communications modules

Specialized licensed/unlicensed RF, LTE-M/NB-IoT and mesh modules come from niche suppliers, limiting Itron's swap options as performance and FCC/CE certifications commonly exceed $50,000 and add months to qualification. Vendors extract leverage via proprietary protocol stacks and royalty models, with supplier gross margins often higher than commodity silicon peers. Itron's multi-modem roadmaps and adoption of open standards (LoRaWAN, 3GPP IoT) reduce single-vendor dependency.

Battery and sensor component dependencies

Smart meters and endpoints require long-life batteries (typically 10–15 years) and metrology sensors meeting utility accuracy standards (around ±0.5% or better), which narrows qualified suppliers and raises switching costs. Quality and safety certifications limit the supplier base, concentrating bargaining power among certified vendors. Lithium and rare material price volatility—notably large swings between 2022–2024—squeezes margins, so Itron relies on dual-sourcing and inventory buffers to stabilize supply and costs.

Cloud and software infrastructure providers

AMI head-end, analytics and SaaS mostly run on hyperscale clouds (AWS ~32%, Azure ~23%, GCP ~11% in 2024), giving suppliers leverage. Switching clouds is feasible but data egress fees and re-architecture create material friction amid $597B public cloud spend in 2024. Providers influence costs via usage pricing and service bundling; multi-cloud and containerization improve optionality.

- Vendor concentration: hyperscalers dominant

- Cost levers: egress, consumption tiers, bundles

- Mitigants: multi-cloud, containers, abstraction layers

Firmware, security IP, and standards compliance

Security libraries, PKI and protocol stacks are often licensed from specialists, giving suppliers leverage because compliance to DLMS/COSEM, IEEE and OCPP ties firmware updates to vendor roadmaps and can delay certifications. Suppliers gain further power when third-party IP is a certification prerequisite. Building in-house stacks reduces this exposure and shortens dependency-driven timelines.

- Supplier IP can gate certifications

- Standards lock updates to vendor roadmaps

- In-house stacks cut dependency risk

Concentrated silicon and cloud supplier power raising costs; mitigated by dual-sourcing

Itron faces concentrated supplier power across advanced silicon (TSMC ~55% share in 2023), niche RF/modem vendors, long-life battery/metrology suppliers and hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024), raising switching costs, certification friction and input-price volatility observed 2022–2024. Mitigants: dual-sourcing, long-term contracts, multi-cloud and in-house stacks.

| Category | Key metric | Impact |

|---|---|---|

| Foundries | TSMC ~55% (2023) | High concentration |

| Cloud | AWS 32%/Azure 23%/GCP 11% (2024) | Vendor leverage |

| Cloud spend | $597B (2024) | egress/pricing risk |

What is included in the product

Tailored Porter's Five Forces analysis for Itron, uncovering competitive intensity, buyer and supplier bargaining power, threats from substitutes and new entrants, and highlighting disruptive technologies and regulatory shifts that affect its pricing, margins, and market positioning.

Clear one-sheet Porter's Five Forces for Itron—pinpoints competitive pain points and priorities for quick strategic decisions, with customizable pressure levels and a radar view ready for decks or dashboards.

Customers Bargaining Power

Large, concentrated utility customers

Investor-owned utilities and large municipalities buy at scale via competitive RFPs, with many meter and grid contracts in 2024 exceeding $10M per award, concentrating buying power and squeezing supplier margins. Concentration gives buyers leverage to demand lower prices and tougher contract terms; visible wins and referenceability further amplify price pressure across peers. Suppliers often accept multi-year deals (commonly 3-5 years) trading margin for volume certainty.

High switching costs but formal procurement

Integration with CIS/MDM, head-end systems and field ops creates high switching costs for Itron customers by tying billing, analytics and operations together; nonetheless periodic public tenders enforce competitive bidding and price transparency, as buyers routinely demand interoperability tests and pilot programs to de-risk migration, so incumbency provides advantage but is not decisive.

Performance, reliability, and SLAs driven

Utilities demand accuracy, uptime, cybersecurity, and strict SLAs; common uptime targets cited across industry contracts are 99.99% (≈52.6 minutes downtime/year), with formal acceptance testing and security certifications required. Penalties and acceptance testing legally shift operational and financial risk to vendors, increasing customer leverage in negotiations. Consistently strong performance allows vendors to command premium pricing, while high-profile failures rapidly erase bargaining power and invite contract penalties or termination.

Total cost of ownership focus

Buyers increasingly evaluate TCO across device, communications, installation and maintenance, favoring solutions where analytics and outage-reduction capabilities offset higher unit prices; industry reports in 2024 note double-digit TCO savings for analytics-enabled deployments. Unbundling of services pressures hardware margins, while vertically bundled solutions (hardware+software+services) allow suppliers to reclaim value capture and sustain pricing.

- TCO-focused procurement

- Analytics-driven savings

- Unbundling depresses hardware margins

- Bundled solutions reclaim value

Regulatory and standards requirements

Compliance mandates shape specs and vendor eligibility, with utilities and municipalities enforcing IEEE, IEC and ANSI-aligned requirements that prioritize interoperability and data security. Buyers leverage these standards to avoid lock-in; certification gates, which commonly take 3–12 months and cost roughly 10,000–100,000 USD, reduce the vendor pool and heighten competition among qualified suppliers. Custom local requirements and legacy integrations can still limit buyer options.

- Standards enforced: IEEE, IEC, ANSI

- Certification impact: 3–12 months, 10k–100k USD

- Buyer leverage: interoperability to prevent lock-in

- Constraint: local/legacy requirements reduce choices

Utilities use $10M+ RFPs to secure 3-5yr deals, driving double-digit TCO savings

Large utilities and municipalities concentrate buying power via $10M+ RFPs in 2024, forcing price concessions and multi-year (3–5yr) deals for volume certainty. High switching costs from CIS/MDM integration limit churn but public tenders and certifications (3–12m, $10k–$100k) sustain competition. TCO and analytics drive procurement, producing reported double-digit TCO savings.

| Metric | 2024 value |

|---|---|

| Typical award size | $10M+ |

| Contract length | 3–5 yrs |

| Cert cost/time | $10k–$100k / 3–12m |

| TCO savings | Double-digit % |

Full Version Awaits

Itron Porter's Five Forces Analysis

This Itron Porter's Five Forces Analysis provides a concise, professionally formatted evaluation of industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to Itron. This preview is the exact file you’ll receive after purchase—no placeholders, no mockups. Once bought, you get immediate access to the same ready-to-use document.