ITV Porter's Five Forces Analysis

From Overview to Strategy Blueprint

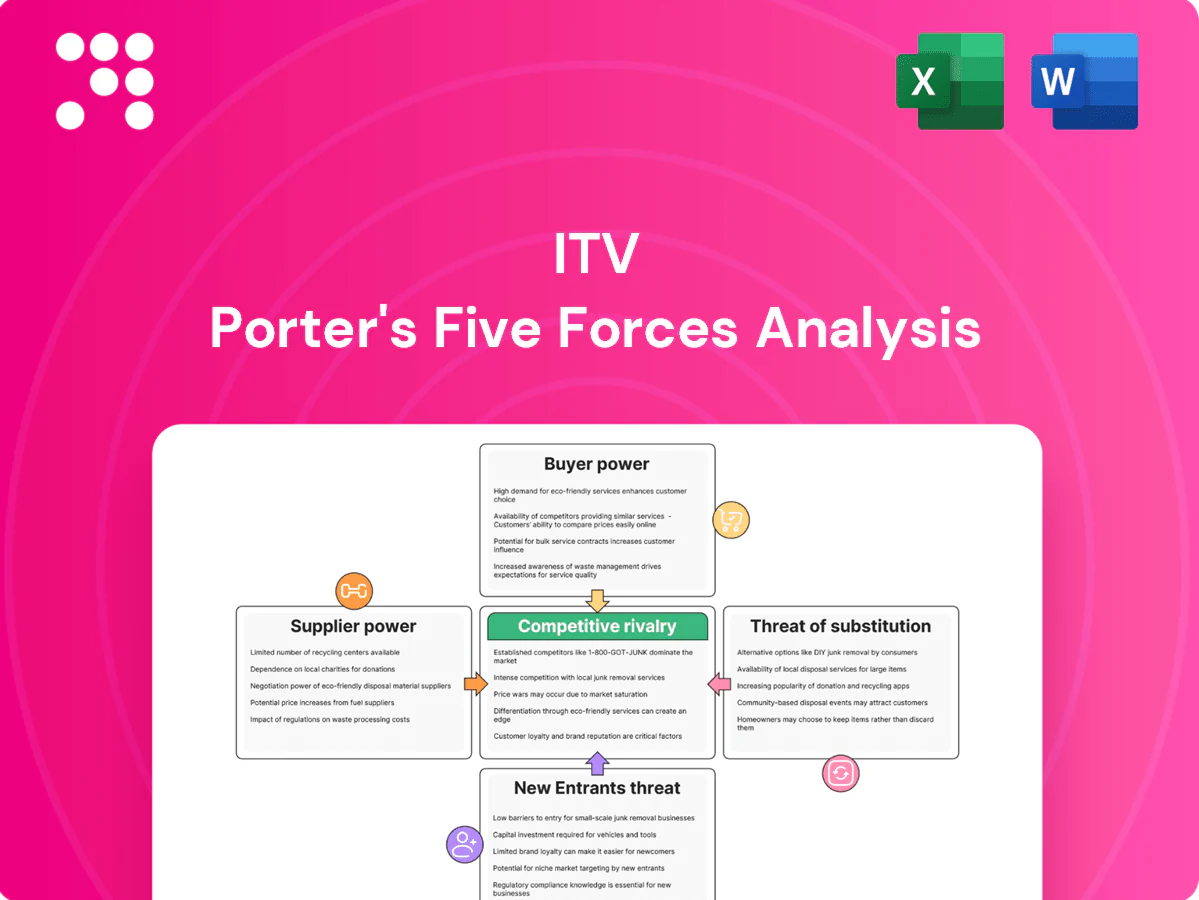

ITV faces moderate rivalry with streaming entrants and strong buyer expectations for digital content, while supplier bargaining and substitute threats shape margins and programming strategies. This snapshot highlights core competitive pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ITV’s market dynamics, force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Scarce premium content rights

Premium sports, reality formats and marquee dramas are concentrated with a few rights owners, forcing ITV into high-stakes bid wars: UK Premier League domestic rights alone were worth £5.1bn for 2022–25, inflating acquisition costs and shifting terms toward suppliers. Losing a single tentpole can dent ratings and ad yield materially. Multi‑year, multi‑territory deals lock ITV into sustained high commitments and reduced negotiating leverage.

Star talent and unions

Top on‑screen talent, writers and showrunners exert strong leverage over ITV, amplified by agents and unions: the WGA strike ran 149 days in 2023 and SAG‑AFTRA 118 days, causing widespread schedule disruption. Pay floors, increased streaming residuals and work‑rule provisions raise fixed content costs. Talent often multi‑homes across platforms, increasing switching risk and making delays from labor actions directly hit monetization.

Independent producers’ clout

UK indies with proven IP can secure favorable commissioning terms and back-end participation as competing buyers raise their bids; Netflix committed £1bn to UK production over 2022–25, strengthening buyers’ BATNA. Retaining format ownership is harder without co‑pro terms, and although ITV Studios vertically integrates supply, it cannot fill all commissioning slots across the market.

Distribution gatekeepers

Distribution gatekeepers — Sky, Virgin, Freeview and smart TV OS vendors — control carriage, UI placement and data flows that materially shape ITV’s ad impressions and AVOD/SVOD take-up; Ofcom 2024 reports Freeview reaches ~90% of UK TV homes and smart TVs are in ~80% of households, concentrating leverage with platform operators (Sky UK ~5.6m pay-TV subs in 2024).

- UI placement & data: direct impact on ad impressions and discovery

- Costs: carriage fees + technical standards raise distribution costs and complexity

- Regulation: PSB prominence aids ITV but prominence rules are evolving (Ofcom 2024)

Tech and data vendors

Tech and data vendors are concentrated and sticky: top 3 ad-tech providers accounted for roughly 60% of programmatic inventory in 2024, while identity and CTV ad-insertion require specialized stacks, raising switching and integration costs and giving vendors pricing power. CDN outages or latency directly reduce delivery and, by some estimates in 2024, cost publishers millions per hour in lost revenue.

- Concentration: top-3 ≈60% (2024)

- Specialization: identity/CTV stacks required

- Pricing power: high switching/integration costs

- Operational risk: outages cost publishers millions/hour (2024 est.)

Rights £5.1bn, platforms ~90% reach, ad-tech 60%

Supplier power is high: sports/IP owners drive bidding (Premier League rights £5.1bn 2022–25), talent strikes in 2023 disrupted schedules and raised pay floors, and distribution/platform gatekeepers concentrate reach (Freeview ~90% homes; Sky ~5.6m subs 2024). Ad-tech/top‑3 vendors hold ~60% programmatic inventory, raising switching costs and pricing power.

| Supplier | Metric | Impact |

|---|---|---|

| Rights owners | Premier League £5.1bn (2022–25) | High acquisition cost |

| Platforms | Freeview ~90% homes; Sky 5.6m | Control distribution/UI |

| Ad-tech | Top‑3 ~60% inventory (2024) | Pricing power |

What is included in the product

Tailored Porter's Five Forces analysis for ITV that uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes and disruptive threats, evaluating how these forces shape ITV’s pricing power, profitability and strategic positioning within the UK and global media landscape.

A one-sheet ITV Porter's Five Forces summary that visualizes strategic pressure with a spider chart and lets you customize force levels and scenarios without macros—ideal for quick decisions, slides, or integration into dashboards.

Customers Bargaining Power

Advertisers’ budget fluidity

Agencies can reallocate budgets across TV, CTV, social and search within days, and in 2024 digital channels accounted for over half of global ad spend, increasing customers’ leverage over ITV. Performance benchmarks and ROI models tighten pricing pressure as advertisers demand measurable CPM-to-conversion outcomes. Scatter markets amplify cyclical CPM swings seasonally, while upfronts give visibility but lock in concessions that weaken short-term pricing power.

Agency consolidation

Agency consolidation gives large holding groups—WPP remained the world’s largest agency group in 2024—outsized leverage to pool client demand and press ITV on price and first‑party data access. Preferred partner lists and trading agreements increasingly exclude or commoditise standalone inventory, pushing ITV to treat sponsorships and integrations as baseline offers. Heightened transparency and measurement demands in 2024 have raised reporting and verification costs for broadcasters.

Viewer switching ease

Audiences can move to streamers or social with minimal friction: global paid streaming subscriptions topped about 1.1 billion in 2024, raising alternative supply. If schedules disappoint, ratings fall and ad slot values drop, pressuring ITV CPMs. Retention on ITVX depends on fresh IP and UX improvements. Higher churn risk forces increased content and marketing spend to defend share.

Content buyers globally

Content buyers worldwide—broadcasters, SVOD and FAST platforms—have multiple supplier options, squeezing ITV Studios on price and rights terms; co-production demands and complex windowing further compress margins and extend payback periods. Pre-sales and minimum guarantees de-risk production but cap upside for hit payoffs, while format buyers prioritize localizable, repeatable formats, reducing leverage for niche IP and one-off innovations.

- Multiple suppliers — lowers seller bargaining power

- Co-pros & windowing — margin pressure

- Pre-sales — risk mitigation, upside limit

- Format buyers — favor repeatability, limit niche leverage

Subscription sensitivity

ITVX Premium faces strong customer bargaining power as it competes with low‑cost, high‑value bundles; UK streaming subscriptions exceeded 40 million in 2024, amplifying choice and price sensitivity. Price elasticity is elevated amid household budget pressure and slower real income growth in 2024, forcing ad‑free tiers to justify higher ARPU versus ad‑funded options. Introductory offers train deal‑seeking behavior, increasing churn risk.

- High choice: >40m UK subscriptions (2024)

- Elastic demand: pressure on ARPU vs ad revenue

- Intro offers = higher churn and deal-seeking

Ad budgets tighten as digital spend hits 50% and streaming churn rises

Advertisers and agencies hold strong leverage over ITV: digital channels exceeded 50% of global ad spend in 2024 and WPP remained the largest agency, enabling rapid budget shifts and tougher ROI demands. Global paid streaming subscriptions reached ~1.1bn in 2024 and UK streaming users topped 40m, raising churn and price sensitivity for ITVX. Content buyers and co‑pro terms compress studio margins and cap upside.

| Metric | 2024 |

|---|---|

| Digital ad share | >50% |

| Global paid stream subs | ~1.1bn |

| UK streaming subs | >40m |

| Largest agency | WPP |

Full Version Awaits

ITV Porter's Five Forces Analysis

This preview displays the exact ITV Porter's Five Forces analysis you'll receive upon purchase—no placeholders or samples. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. The file is fully formatted and ready for immediate download and use.

From Overview to Strategy Blueprint

ITV faces moderate rivalry with streaming entrants and strong buyer expectations for digital content, while supplier bargaining and substitute threats shape margins and programming strategies. This snapshot highlights core competitive pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ITV’s market dynamics, force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Scarce premium content rights

Premium sports, reality formats and marquee dramas are concentrated with a few rights owners, forcing ITV into high-stakes bid wars: UK Premier League domestic rights alone were worth £5.1bn for 2022–25, inflating acquisition costs and shifting terms toward suppliers. Losing a single tentpole can dent ratings and ad yield materially. Multi‑year, multi‑territory deals lock ITV into sustained high commitments and reduced negotiating leverage.

Star talent and unions

Top on‑screen talent, writers and showrunners exert strong leverage over ITV, amplified by agents and unions: the WGA strike ran 149 days in 2023 and SAG‑AFTRA 118 days, causing widespread schedule disruption. Pay floors, increased streaming residuals and work‑rule provisions raise fixed content costs. Talent often multi‑homes across platforms, increasing switching risk and making delays from labor actions directly hit monetization.

Independent producers’ clout

UK indies with proven IP can secure favorable commissioning terms and back-end participation as competing buyers raise their bids; Netflix committed £1bn to UK production over 2022–25, strengthening buyers’ BATNA. Retaining format ownership is harder without co‑pro terms, and although ITV Studios vertically integrates supply, it cannot fill all commissioning slots across the market.

Distribution gatekeepers

Distribution gatekeepers — Sky, Virgin, Freeview and smart TV OS vendors — control carriage, UI placement and data flows that materially shape ITV’s ad impressions and AVOD/SVOD take-up; Ofcom 2024 reports Freeview reaches ~90% of UK TV homes and smart TVs are in ~80% of households, concentrating leverage with platform operators (Sky UK ~5.6m pay-TV subs in 2024).

- UI placement & data: direct impact on ad impressions and discovery

- Costs: carriage fees + technical standards raise distribution costs and complexity

- Regulation: PSB prominence aids ITV but prominence rules are evolving (Ofcom 2024)

Tech and data vendors

Tech and data vendors are concentrated and sticky: top 3 ad-tech providers accounted for roughly 60% of programmatic inventory in 2024, while identity and CTV ad-insertion require specialized stacks, raising switching and integration costs and giving vendors pricing power. CDN outages or latency directly reduce delivery and, by some estimates in 2024, cost publishers millions per hour in lost revenue.

- Concentration: top-3 ≈60% (2024)

- Specialization: identity/CTV stacks required

- Pricing power: high switching/integration costs

- Operational risk: outages cost publishers millions/hour (2024 est.)

Rights £5.1bn, platforms ~90% reach, ad-tech 60%

Supplier power is high: sports/IP owners drive bidding (Premier League rights £5.1bn 2022–25), talent strikes in 2023 disrupted schedules and raised pay floors, and distribution/platform gatekeepers concentrate reach (Freeview ~90% homes; Sky ~5.6m subs 2024). Ad-tech/top‑3 vendors hold ~60% programmatic inventory, raising switching costs and pricing power.

| Supplier | Metric | Impact |

|---|---|---|

| Rights owners | Premier League £5.1bn (2022–25) | High acquisition cost |

| Platforms | Freeview ~90% homes; Sky 5.6m | Control distribution/UI |

| Ad-tech | Top‑3 ~60% inventory (2024) | Pricing power |

What is included in the product

Tailored Porter's Five Forces analysis for ITV that uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes and disruptive threats, evaluating how these forces shape ITV’s pricing power, profitability and strategic positioning within the UK and global media landscape.

A one-sheet ITV Porter's Five Forces summary that visualizes strategic pressure with a spider chart and lets you customize force levels and scenarios without macros—ideal for quick decisions, slides, or integration into dashboards.

Customers Bargaining Power

Advertisers’ budget fluidity

Agencies can reallocate budgets across TV, CTV, social and search within days, and in 2024 digital channels accounted for over half of global ad spend, increasing customers’ leverage over ITV. Performance benchmarks and ROI models tighten pricing pressure as advertisers demand measurable CPM-to-conversion outcomes. Scatter markets amplify cyclical CPM swings seasonally, while upfronts give visibility but lock in concessions that weaken short-term pricing power.

Agency consolidation

Agency consolidation gives large holding groups—WPP remained the world’s largest agency group in 2024—outsized leverage to pool client demand and press ITV on price and first‑party data access. Preferred partner lists and trading agreements increasingly exclude or commoditise standalone inventory, pushing ITV to treat sponsorships and integrations as baseline offers. Heightened transparency and measurement demands in 2024 have raised reporting and verification costs for broadcasters.

Viewer switching ease

Audiences can move to streamers or social with minimal friction: global paid streaming subscriptions topped about 1.1 billion in 2024, raising alternative supply. If schedules disappoint, ratings fall and ad slot values drop, pressuring ITV CPMs. Retention on ITVX depends on fresh IP and UX improvements. Higher churn risk forces increased content and marketing spend to defend share.

Content buyers globally

Content buyers worldwide—broadcasters, SVOD and FAST platforms—have multiple supplier options, squeezing ITV Studios on price and rights terms; co-production demands and complex windowing further compress margins and extend payback periods. Pre-sales and minimum guarantees de-risk production but cap upside for hit payoffs, while format buyers prioritize localizable, repeatable formats, reducing leverage for niche IP and one-off innovations.

- Multiple suppliers — lowers seller bargaining power

- Co-pros & windowing — margin pressure

- Pre-sales — risk mitigation, upside limit

- Format buyers — favor repeatability, limit niche leverage

Subscription sensitivity

ITVX Premium faces strong customer bargaining power as it competes with low‑cost, high‑value bundles; UK streaming subscriptions exceeded 40 million in 2024, amplifying choice and price sensitivity. Price elasticity is elevated amid household budget pressure and slower real income growth in 2024, forcing ad‑free tiers to justify higher ARPU versus ad‑funded options. Introductory offers train deal‑seeking behavior, increasing churn risk.

- High choice: >40m UK subscriptions (2024)

- Elastic demand: pressure on ARPU vs ad revenue

- Intro offers = higher churn and deal-seeking

Ad budgets tighten as digital spend hits 50% and streaming churn rises

Advertisers and agencies hold strong leverage over ITV: digital channels exceeded 50% of global ad spend in 2024 and WPP remained the largest agency, enabling rapid budget shifts and tougher ROI demands. Global paid streaming subscriptions reached ~1.1bn in 2024 and UK streaming users topped 40m, raising churn and price sensitivity for ITVX. Content buyers and co‑pro terms compress studio margins and cap upside.

| Metric | 2024 |

|---|---|

| Digital ad share | >50% |

| Global paid stream subs | ~1.1bn |

| UK streaming subs | >40m |

| Largest agency | WPP |

Full Version Awaits

ITV Porter's Five Forces Analysis

This preview displays the exact ITV Porter's Five Forces analysis you'll receive upon purchase—no placeholders or samples. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. The file is fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

ITV faces moderate rivalry with streaming entrants and strong buyer expectations for digital content, while supplier bargaining and substitute threats shape margins and programming strategies. This snapshot highlights core competitive pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ITV’s market dynamics, force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Scarce premium content rights

Premium sports, reality formats and marquee dramas are concentrated with a few rights owners, forcing ITV into high-stakes bid wars: UK Premier League domestic rights alone were worth £5.1bn for 2022–25, inflating acquisition costs and shifting terms toward suppliers. Losing a single tentpole can dent ratings and ad yield materially. Multi‑year, multi‑territory deals lock ITV into sustained high commitments and reduced negotiating leverage.

Star talent and unions

Top on‑screen talent, writers and showrunners exert strong leverage over ITV, amplified by agents and unions: the WGA strike ran 149 days in 2023 and SAG‑AFTRA 118 days, causing widespread schedule disruption. Pay floors, increased streaming residuals and work‑rule provisions raise fixed content costs. Talent often multi‑homes across platforms, increasing switching risk and making delays from labor actions directly hit monetization.

Independent producers’ clout

UK indies with proven IP can secure favorable commissioning terms and back-end participation as competing buyers raise their bids; Netflix committed £1bn to UK production over 2022–25, strengthening buyers’ BATNA. Retaining format ownership is harder without co‑pro terms, and although ITV Studios vertically integrates supply, it cannot fill all commissioning slots across the market.

Distribution gatekeepers

Distribution gatekeepers — Sky, Virgin, Freeview and smart TV OS vendors — control carriage, UI placement and data flows that materially shape ITV’s ad impressions and AVOD/SVOD take-up; Ofcom 2024 reports Freeview reaches ~90% of UK TV homes and smart TVs are in ~80% of households, concentrating leverage with platform operators (Sky UK ~5.6m pay-TV subs in 2024).

- UI placement & data: direct impact on ad impressions and discovery

- Costs: carriage fees + technical standards raise distribution costs and complexity

- Regulation: PSB prominence aids ITV but prominence rules are evolving (Ofcom 2024)

Tech and data vendors

Tech and data vendors are concentrated and sticky: top 3 ad-tech providers accounted for roughly 60% of programmatic inventory in 2024, while identity and CTV ad-insertion require specialized stacks, raising switching and integration costs and giving vendors pricing power. CDN outages or latency directly reduce delivery and, by some estimates in 2024, cost publishers millions per hour in lost revenue.

- Concentration: top-3 ≈60% (2024)

- Specialization: identity/CTV stacks required

- Pricing power: high switching/integration costs

- Operational risk: outages cost publishers millions/hour (2024 est.)

Rights £5.1bn, platforms ~90% reach, ad-tech 60%

Supplier power is high: sports/IP owners drive bidding (Premier League rights £5.1bn 2022–25), talent strikes in 2023 disrupted schedules and raised pay floors, and distribution/platform gatekeepers concentrate reach (Freeview ~90% homes; Sky ~5.6m subs 2024). Ad-tech/top‑3 vendors hold ~60% programmatic inventory, raising switching costs and pricing power.

| Supplier | Metric | Impact |

|---|---|---|

| Rights owners | Premier League £5.1bn (2022–25) | High acquisition cost |

| Platforms | Freeview ~90% homes; Sky 5.6m | Control distribution/UI |

| Ad-tech | Top‑3 ~60% inventory (2024) | Pricing power |

What is included in the product

Tailored Porter's Five Forces analysis for ITV that uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes and disruptive threats, evaluating how these forces shape ITV’s pricing power, profitability and strategic positioning within the UK and global media landscape.

A one-sheet ITV Porter's Five Forces summary that visualizes strategic pressure with a spider chart and lets you customize force levels and scenarios without macros—ideal for quick decisions, slides, or integration into dashboards.

Customers Bargaining Power

Advertisers’ budget fluidity

Agencies can reallocate budgets across TV, CTV, social and search within days, and in 2024 digital channels accounted for over half of global ad spend, increasing customers’ leverage over ITV. Performance benchmarks and ROI models tighten pricing pressure as advertisers demand measurable CPM-to-conversion outcomes. Scatter markets amplify cyclical CPM swings seasonally, while upfronts give visibility but lock in concessions that weaken short-term pricing power.

Agency consolidation

Agency consolidation gives large holding groups—WPP remained the world’s largest agency group in 2024—outsized leverage to pool client demand and press ITV on price and first‑party data access. Preferred partner lists and trading agreements increasingly exclude or commoditise standalone inventory, pushing ITV to treat sponsorships and integrations as baseline offers. Heightened transparency and measurement demands in 2024 have raised reporting and verification costs for broadcasters.

Viewer switching ease

Audiences can move to streamers or social with minimal friction: global paid streaming subscriptions topped about 1.1 billion in 2024, raising alternative supply. If schedules disappoint, ratings fall and ad slot values drop, pressuring ITV CPMs. Retention on ITVX depends on fresh IP and UX improvements. Higher churn risk forces increased content and marketing spend to defend share.

Content buyers globally

Content buyers worldwide—broadcasters, SVOD and FAST platforms—have multiple supplier options, squeezing ITV Studios on price and rights terms; co-production demands and complex windowing further compress margins and extend payback periods. Pre-sales and minimum guarantees de-risk production but cap upside for hit payoffs, while format buyers prioritize localizable, repeatable formats, reducing leverage for niche IP and one-off innovations.

- Multiple suppliers — lowers seller bargaining power

- Co-pros & windowing — margin pressure

- Pre-sales — risk mitigation, upside limit

- Format buyers — favor repeatability, limit niche leverage

Subscription sensitivity

ITVX Premium faces strong customer bargaining power as it competes with low‑cost, high‑value bundles; UK streaming subscriptions exceeded 40 million in 2024, amplifying choice and price sensitivity. Price elasticity is elevated amid household budget pressure and slower real income growth in 2024, forcing ad‑free tiers to justify higher ARPU versus ad‑funded options. Introductory offers train deal‑seeking behavior, increasing churn risk.

- High choice: >40m UK subscriptions (2024)

- Elastic demand: pressure on ARPU vs ad revenue

- Intro offers = higher churn and deal-seeking

Ad budgets tighten as digital spend hits 50% and streaming churn rises

Advertisers and agencies hold strong leverage over ITV: digital channels exceeded 50% of global ad spend in 2024 and WPP remained the largest agency, enabling rapid budget shifts and tougher ROI demands. Global paid streaming subscriptions reached ~1.1bn in 2024 and UK streaming users topped 40m, raising churn and price sensitivity for ITVX. Content buyers and co‑pro terms compress studio margins and cap upside.

| Metric | 2024 |

|---|---|

| Digital ad share | >50% |

| Global paid stream subs | ~1.1bn |

| UK streaming subs | >40m |

| Largest agency | WPP |

Full Version Awaits

ITV Porter's Five Forces Analysis

This preview displays the exact ITV Porter's Five Forces analysis you'll receive upon purchase—no placeholders or samples. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. The file is fully formatted and ready for immediate download and use.