IVS Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

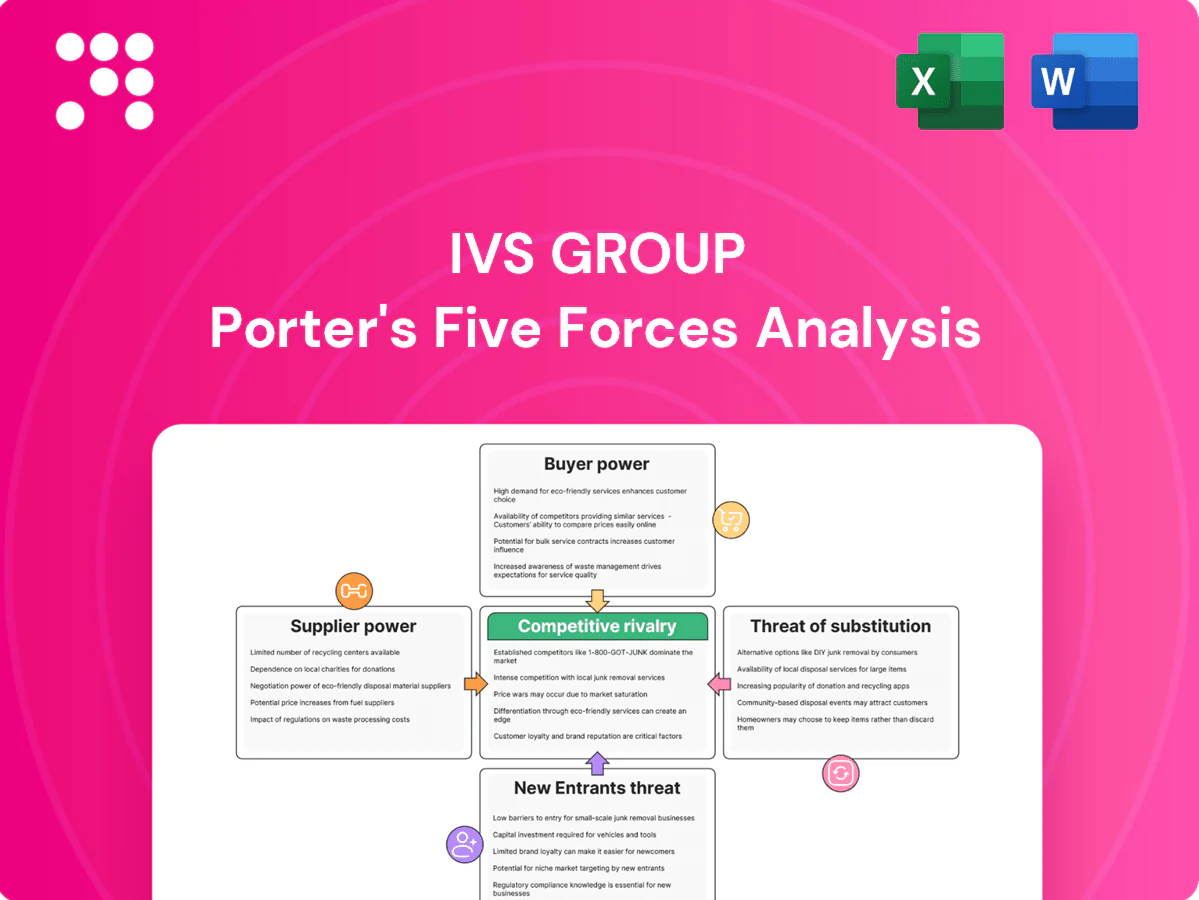

IVS Group’s Porter’s Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, barriers to entry, and substitute threats shaping its market position. This overview uncovers key vulnerabilities and strategic levers but only scratches the surface. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment and strategic decisions.

Suppliers Bargaining Power

Diverse FMCG inputs

IVS sources coffee, drinks, snacks and fresh food from numerous FMCG suppliers across Europe, which limits individual supplier leverage. High product availability and wide brand alternatives temper bargaining power, while private-label and unbranded SKUs—representing roughly 40% share in many European categories in 2024—further reduce dependence on single brands. Seasonal or niche fresh items can tighten local supply and cause short-term price spikes.

Vending machine OEM dependence

As of 2024 core vending hardware for IVS Group is supplied by a concentrated set of OEMs and spare-part providers, creating an installed-base lock-in that raises format and component switching costs. This dynamic gives OEMs moderate pricing and service leverage over operators and integrators. Long-term framework agreements are commonly used to mitigate cost volatility and lead-time risk.

Payments and telemetry tech

Cashless readers, telemetry units and platform software are specialized inputs with relatively few certified vendors, creating stickiness that can drive merchant service fees commonly in the 0.2–3% range (2024). Interoperability limits and proprietary protocols let vendors levy higher integration and recurring fees, yet rising open APIs and multiple integrators in 2024 have expanded options. IVS can use scale purchasing and multi-vendor deployment to push down unit and integration costs and secure better SLA and pricing terms.

Logistics and consumables exposure

Fuel, packaging and cup/sugar/stirrer consumables are commodity-like but volatile; Brent crude averaged about 86 USD/bbl in 2024, keeping input-price swings elevated. Suppliers commonly pass through inflation, squeezing margins until repricing cycles catch up; multi-country procurement and route optimization mitigate this exposure.

- Commodity volatility: Brent ~86 USD/bbl (2024)

- Pass-through lag: months

- Hedging: multi-country buying

- Cost control: route optimization

Local fresh food partners

Fresh sandwiches and ready meals rely heavily on local commissaries and bakeries, giving suppliers elevated leverage in cities where qualified substitutes are scarce; in 2024 IVS flagged local fresh sourcing as a strategic risk. Quality and food-safety specs limit rapid switching, while dual-sourcing and standardized specs are used to preserve bargaining balance and control COGS volatility.

- 2024: local sourcing = strategic risk

- Constraint: food-safety/specs

- Mitigation: dual-sourcing, standards

FMCG sourcing fragmented; private-label ~40%, cashless 0.2–3%, Brent ~86 USD/bbl

FMCG sourcing is fragmented, private-label/unbranded ~40% (2024) lowering supplier leverage. Vending hardware is concentrated among OEMs, creating installed-base switching costs; cashless/telemetry vendors drive fees ~0.2–3% (2024). Commodity inputs remain volatile (Brent ~86 USD/bbl, 2024) and local fresh suppliers create elevated city-level sourcing risk.

| Metric | 2024 value | Implication |

|---|---|---|

| Private-label share | ~40% | Reduces brand dependence |

| Cashless fees | 0.2–3% | Recurring cost pressure |

| Brent crude | ~86 USD/bbl | Input-price volatility |

| OEM concentration | High | Switching costs, leverage |

| Local fresh risk | Elevated | City-level supply tightness |

What is included in the product

Tailored Porter's Five Forces analysis for IVS Group that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, evaluates pricing and profitability pressures, and delivers actionable strategic insights suitable for investor materials, internal strategy decks or editable reports.

A concise one-sheet Porter's Five Forces for IVS Group that visualizes competitive pressure with an editable spider chart, customizable inputs for scenario analysis, and a clean, no-macros layout ready to drop into decks or integrate into wider reports.

Customers Bargaining Power

Large institutional contracts

Large institutional buyers—corporates, public agencies, hospitals and universities—aggregate volume and drive tender-based procurement (OECD: public procurement ≈12% of GDP in 2024), intensifying price and service concessions; switching costs are moderate because changeovers are scheduled between service windows, while robust SLAs, uptime guarantees and differentiated product ranges mitigate pure price pressure.

Multi-site, multi-country buyers

Pan-European clients favor unified contracts and consolidated reporting; demand consolidation raises buyer leverage on price and innovation. IVS’s multi-country footprint offers one-stop coverage, partially offsetting pressure. Data-driven customization and ESG alignment — amid CSRD expansion to ~50,000 firms in 2024 — increase client stickiness.

Price sensitivity vs convenience

End users prioritize proximity and speed, so convenience dampens extreme price elasticity even as digital ordering exceeds 50% of transactions in 2024; host clients meanwhile pressure commissions (commonly 15–30% in 2024), vend price ceilings and service fees. Promotions, dynamic pricing and assortment mix improve perceived value and margin capture. Premiumization in coffee has lifted ARPU by roughly 10–20% in many markets while preserving satisfaction.

Contract length and renewal risk

Longer contracts (industry average 3–5 years in 2024) lock IVS routes but create renewal cliffs where competitive rebids let buyers extract ~5–10% better terms; robust KPIs and roadmap disclosures have cut churn roughly 15% in recent pilots. Embedded hardware on ~70% of fleets and cashless integrations (~60% adoption in 2024) raise practical switching frictions.

- Contract length: 3–5y (2024)

- Rebid concessions: 5–10%

- Churn reduction via metrics: ~15%

- Embedded hardware: ~70%; cashless: ~60% (2024)

Product and ESG requirements

Hosts increasingly demand healthier SKUs, recyclable packaging and lower-energy machines, which raises capex and narrows vendor options; regulatory drivers include the EU CSRD coming into effect in 2024 and the EU Fit for 55 target of 55% GHG reduction by 2030, making compliance costly but strategic. Compliance builds buyer trust and can justify price premia, while transparent reporting on waste, nutrition and carbon creates leverage for contract renegotiations.

- Vendor constraints: higher-spec machines reduce supplier pool

- Cost impact: increased capex/OPEX for compliant SKUs and equipment

- Pricing leverage: ESG compliance can support price premia

- Reporting value: transparent waste/nutrition/carbon data strengthens renegotiation

Buyers push discounts; SLAs and embedded hardware drive supplier stickiness and premium pricing

Buyers (large institutions, hosts, end-users) exert moderate-to-high power via tendering, consolidation and commission pressure, but IVS’s multi-country footprint, SLAs and embedded hardware raise switching costs and stickiness. Regulatory and ESG demands (CSRD ~50,000 firms in 2024) shift leverage toward compliant suppliers who can justify premia. Renewal cliffs (3–5y contracts) permit rebid concessions of ~5–10%.

| Metric | 2024 |

|---|---|

| Public procurement %GDP | ≈12% |

| Digital orders | >50% |

| Embedded hardware / cashless | 70% / 60% |

| Rebid concession | 5–10% |

Preview Before You Purchase

IVS Group Porter's Five Forces Analysis

This preview shows the exact IVS Group Porter’s Five Forces analysis you'll receive upon purchase—fully formatted and ready to use. It provides a detailed assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with actionable insights. No placeholders or samples; you’ll get this same file instantly after payment.

Go Beyond the Preview—Access the Full Strategic Report

IVS Group’s Porter’s Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, barriers to entry, and substitute threats shaping its market position. This overview uncovers key vulnerabilities and strategic levers but only scratches the surface. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment and strategic decisions.

Suppliers Bargaining Power

Diverse FMCG inputs

IVS sources coffee, drinks, snacks and fresh food from numerous FMCG suppliers across Europe, which limits individual supplier leverage. High product availability and wide brand alternatives temper bargaining power, while private-label and unbranded SKUs—representing roughly 40% share in many European categories in 2024—further reduce dependence on single brands. Seasonal or niche fresh items can tighten local supply and cause short-term price spikes.

Vending machine OEM dependence

As of 2024 core vending hardware for IVS Group is supplied by a concentrated set of OEMs and spare-part providers, creating an installed-base lock-in that raises format and component switching costs. This dynamic gives OEMs moderate pricing and service leverage over operators and integrators. Long-term framework agreements are commonly used to mitigate cost volatility and lead-time risk.

Payments and telemetry tech

Cashless readers, telemetry units and platform software are specialized inputs with relatively few certified vendors, creating stickiness that can drive merchant service fees commonly in the 0.2–3% range (2024). Interoperability limits and proprietary protocols let vendors levy higher integration and recurring fees, yet rising open APIs and multiple integrators in 2024 have expanded options. IVS can use scale purchasing and multi-vendor deployment to push down unit and integration costs and secure better SLA and pricing terms.

Logistics and consumables exposure

Fuel, packaging and cup/sugar/stirrer consumables are commodity-like but volatile; Brent crude averaged about 86 USD/bbl in 2024, keeping input-price swings elevated. Suppliers commonly pass through inflation, squeezing margins until repricing cycles catch up; multi-country procurement and route optimization mitigate this exposure.

- Commodity volatility: Brent ~86 USD/bbl (2024)

- Pass-through lag: months

- Hedging: multi-country buying

- Cost control: route optimization

Local fresh food partners

Fresh sandwiches and ready meals rely heavily on local commissaries and bakeries, giving suppliers elevated leverage in cities where qualified substitutes are scarce; in 2024 IVS flagged local fresh sourcing as a strategic risk. Quality and food-safety specs limit rapid switching, while dual-sourcing and standardized specs are used to preserve bargaining balance and control COGS volatility.

- 2024: local sourcing = strategic risk

- Constraint: food-safety/specs

- Mitigation: dual-sourcing, standards

FMCG sourcing fragmented; private-label ~40%, cashless 0.2–3%, Brent ~86 USD/bbl

FMCG sourcing is fragmented, private-label/unbranded ~40% (2024) lowering supplier leverage. Vending hardware is concentrated among OEMs, creating installed-base switching costs; cashless/telemetry vendors drive fees ~0.2–3% (2024). Commodity inputs remain volatile (Brent ~86 USD/bbl, 2024) and local fresh suppliers create elevated city-level sourcing risk.

| Metric | 2024 value | Implication |

|---|---|---|

| Private-label share | ~40% | Reduces brand dependence |

| Cashless fees | 0.2–3% | Recurring cost pressure |

| Brent crude | ~86 USD/bbl | Input-price volatility |

| OEM concentration | High | Switching costs, leverage |

| Local fresh risk | Elevated | City-level supply tightness |

What is included in the product

Tailored Porter's Five Forces analysis for IVS Group that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, evaluates pricing and profitability pressures, and delivers actionable strategic insights suitable for investor materials, internal strategy decks or editable reports.

A concise one-sheet Porter's Five Forces for IVS Group that visualizes competitive pressure with an editable spider chart, customizable inputs for scenario analysis, and a clean, no-macros layout ready to drop into decks or integrate into wider reports.

Customers Bargaining Power

Large institutional contracts

Large institutional buyers—corporates, public agencies, hospitals and universities—aggregate volume and drive tender-based procurement (OECD: public procurement ≈12% of GDP in 2024), intensifying price and service concessions; switching costs are moderate because changeovers are scheduled between service windows, while robust SLAs, uptime guarantees and differentiated product ranges mitigate pure price pressure.

Multi-site, multi-country buyers

Pan-European clients favor unified contracts and consolidated reporting; demand consolidation raises buyer leverage on price and innovation. IVS’s multi-country footprint offers one-stop coverage, partially offsetting pressure. Data-driven customization and ESG alignment — amid CSRD expansion to ~50,000 firms in 2024 — increase client stickiness.

Price sensitivity vs convenience

End users prioritize proximity and speed, so convenience dampens extreme price elasticity even as digital ordering exceeds 50% of transactions in 2024; host clients meanwhile pressure commissions (commonly 15–30% in 2024), vend price ceilings and service fees. Promotions, dynamic pricing and assortment mix improve perceived value and margin capture. Premiumization in coffee has lifted ARPU by roughly 10–20% in many markets while preserving satisfaction.

Contract length and renewal risk

Longer contracts (industry average 3–5 years in 2024) lock IVS routes but create renewal cliffs where competitive rebids let buyers extract ~5–10% better terms; robust KPIs and roadmap disclosures have cut churn roughly 15% in recent pilots. Embedded hardware on ~70% of fleets and cashless integrations (~60% adoption in 2024) raise practical switching frictions.

- Contract length: 3–5y (2024)

- Rebid concessions: 5–10%

- Churn reduction via metrics: ~15%

- Embedded hardware: ~70%; cashless: ~60% (2024)

Product and ESG requirements

Hosts increasingly demand healthier SKUs, recyclable packaging and lower-energy machines, which raises capex and narrows vendor options; regulatory drivers include the EU CSRD coming into effect in 2024 and the EU Fit for 55 target of 55% GHG reduction by 2030, making compliance costly but strategic. Compliance builds buyer trust and can justify price premia, while transparent reporting on waste, nutrition and carbon creates leverage for contract renegotiations.

- Vendor constraints: higher-spec machines reduce supplier pool

- Cost impact: increased capex/OPEX for compliant SKUs and equipment

- Pricing leverage: ESG compliance can support price premia

- Reporting value: transparent waste/nutrition/carbon data strengthens renegotiation

Buyers push discounts; SLAs and embedded hardware drive supplier stickiness and premium pricing

Buyers (large institutions, hosts, end-users) exert moderate-to-high power via tendering, consolidation and commission pressure, but IVS’s multi-country footprint, SLAs and embedded hardware raise switching costs and stickiness. Regulatory and ESG demands (CSRD ~50,000 firms in 2024) shift leverage toward compliant suppliers who can justify premia. Renewal cliffs (3–5y contracts) permit rebid concessions of ~5–10%.

| Metric | 2024 |

|---|---|

| Public procurement %GDP | ≈12% |

| Digital orders | >50% |

| Embedded hardware / cashless | 70% / 60% |

| Rebid concession | 5–10% |

Preview Before You Purchase

IVS Group Porter's Five Forces Analysis

This preview shows the exact IVS Group Porter’s Five Forces analysis you'll receive upon purchase—fully formatted and ready to use. It provides a detailed assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with actionable insights. No placeholders or samples; you’ll get this same file instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

IVS Group’s Porter’s Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, barriers to entry, and substitute threats shaping its market position. This overview uncovers key vulnerabilities and strategic levers but only scratches the surface. Unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment and strategic decisions.

Suppliers Bargaining Power

Diverse FMCG inputs

IVS sources coffee, drinks, snacks and fresh food from numerous FMCG suppliers across Europe, which limits individual supplier leverage. High product availability and wide brand alternatives temper bargaining power, while private-label and unbranded SKUs—representing roughly 40% share in many European categories in 2024—further reduce dependence on single brands. Seasonal or niche fresh items can tighten local supply and cause short-term price spikes.

Vending machine OEM dependence

As of 2024 core vending hardware for IVS Group is supplied by a concentrated set of OEMs and spare-part providers, creating an installed-base lock-in that raises format and component switching costs. This dynamic gives OEMs moderate pricing and service leverage over operators and integrators. Long-term framework agreements are commonly used to mitigate cost volatility and lead-time risk.

Payments and telemetry tech

Cashless readers, telemetry units and platform software are specialized inputs with relatively few certified vendors, creating stickiness that can drive merchant service fees commonly in the 0.2–3% range (2024). Interoperability limits and proprietary protocols let vendors levy higher integration and recurring fees, yet rising open APIs and multiple integrators in 2024 have expanded options. IVS can use scale purchasing and multi-vendor deployment to push down unit and integration costs and secure better SLA and pricing terms.

Logistics and consumables exposure

Fuel, packaging and cup/sugar/stirrer consumables are commodity-like but volatile; Brent crude averaged about 86 USD/bbl in 2024, keeping input-price swings elevated. Suppliers commonly pass through inflation, squeezing margins until repricing cycles catch up; multi-country procurement and route optimization mitigate this exposure.

- Commodity volatility: Brent ~86 USD/bbl (2024)

- Pass-through lag: months

- Hedging: multi-country buying

- Cost control: route optimization

Local fresh food partners

Fresh sandwiches and ready meals rely heavily on local commissaries and bakeries, giving suppliers elevated leverage in cities where qualified substitutes are scarce; in 2024 IVS flagged local fresh sourcing as a strategic risk. Quality and food-safety specs limit rapid switching, while dual-sourcing and standardized specs are used to preserve bargaining balance and control COGS volatility.

- 2024: local sourcing = strategic risk

- Constraint: food-safety/specs

- Mitigation: dual-sourcing, standards

FMCG sourcing fragmented; private-label ~40%, cashless 0.2–3%, Brent ~86 USD/bbl

FMCG sourcing is fragmented, private-label/unbranded ~40% (2024) lowering supplier leverage. Vending hardware is concentrated among OEMs, creating installed-base switching costs; cashless/telemetry vendors drive fees ~0.2–3% (2024). Commodity inputs remain volatile (Brent ~86 USD/bbl, 2024) and local fresh suppliers create elevated city-level sourcing risk.

| Metric | 2024 value | Implication |

|---|---|---|

| Private-label share | ~40% | Reduces brand dependence |

| Cashless fees | 0.2–3% | Recurring cost pressure |

| Brent crude | ~86 USD/bbl | Input-price volatility |

| OEM concentration | High | Switching costs, leverage |

| Local fresh risk | Elevated | City-level supply tightness |

What is included in the product

Tailored Porter's Five Forces analysis for IVS Group that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, evaluates pricing and profitability pressures, and delivers actionable strategic insights suitable for investor materials, internal strategy decks or editable reports.

A concise one-sheet Porter's Five Forces for IVS Group that visualizes competitive pressure with an editable spider chart, customizable inputs for scenario analysis, and a clean, no-macros layout ready to drop into decks or integrate into wider reports.

Customers Bargaining Power

Large institutional contracts

Large institutional buyers—corporates, public agencies, hospitals and universities—aggregate volume and drive tender-based procurement (OECD: public procurement ≈12% of GDP in 2024), intensifying price and service concessions; switching costs are moderate because changeovers are scheduled between service windows, while robust SLAs, uptime guarantees and differentiated product ranges mitigate pure price pressure.

Multi-site, multi-country buyers

Pan-European clients favor unified contracts and consolidated reporting; demand consolidation raises buyer leverage on price and innovation. IVS’s multi-country footprint offers one-stop coverage, partially offsetting pressure. Data-driven customization and ESG alignment — amid CSRD expansion to ~50,000 firms in 2024 — increase client stickiness.

Price sensitivity vs convenience

End users prioritize proximity and speed, so convenience dampens extreme price elasticity even as digital ordering exceeds 50% of transactions in 2024; host clients meanwhile pressure commissions (commonly 15–30% in 2024), vend price ceilings and service fees. Promotions, dynamic pricing and assortment mix improve perceived value and margin capture. Premiumization in coffee has lifted ARPU by roughly 10–20% in many markets while preserving satisfaction.

Contract length and renewal risk

Longer contracts (industry average 3–5 years in 2024) lock IVS routes but create renewal cliffs where competitive rebids let buyers extract ~5–10% better terms; robust KPIs and roadmap disclosures have cut churn roughly 15% in recent pilots. Embedded hardware on ~70% of fleets and cashless integrations (~60% adoption in 2024) raise practical switching frictions.

- Contract length: 3–5y (2024)

- Rebid concessions: 5–10%

- Churn reduction via metrics: ~15%

- Embedded hardware: ~70%; cashless: ~60% (2024)

Product and ESG requirements

Hosts increasingly demand healthier SKUs, recyclable packaging and lower-energy machines, which raises capex and narrows vendor options; regulatory drivers include the EU CSRD coming into effect in 2024 and the EU Fit for 55 target of 55% GHG reduction by 2030, making compliance costly but strategic. Compliance builds buyer trust and can justify price premia, while transparent reporting on waste, nutrition and carbon creates leverage for contract renegotiations.

- Vendor constraints: higher-spec machines reduce supplier pool

- Cost impact: increased capex/OPEX for compliant SKUs and equipment

- Pricing leverage: ESG compliance can support price premia

- Reporting value: transparent waste/nutrition/carbon data strengthens renegotiation

Buyers push discounts; SLAs and embedded hardware drive supplier stickiness and premium pricing

Buyers (large institutions, hosts, end-users) exert moderate-to-high power via tendering, consolidation and commission pressure, but IVS’s multi-country footprint, SLAs and embedded hardware raise switching costs and stickiness. Regulatory and ESG demands (CSRD ~50,000 firms in 2024) shift leverage toward compliant suppliers who can justify premia. Renewal cliffs (3–5y contracts) permit rebid concessions of ~5–10%.

| Metric | 2024 |

|---|---|

| Public procurement %GDP | ≈12% |

| Digital orders | >50% |

| Embedded hardware / cashless | 70% / 60% |

| Rebid concession | 5–10% |

Preview Before You Purchase

IVS Group Porter's Five Forces Analysis

This preview shows the exact IVS Group Porter’s Five Forces analysis you'll receive upon purchase—fully formatted and ready to use. It provides a detailed assessment of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with actionable insights. No placeholders or samples; you’ll get this same file instantly after payment.