J. Front Retailing SWOT Analysis

Make Insightful Decisions Backed by Expert Research

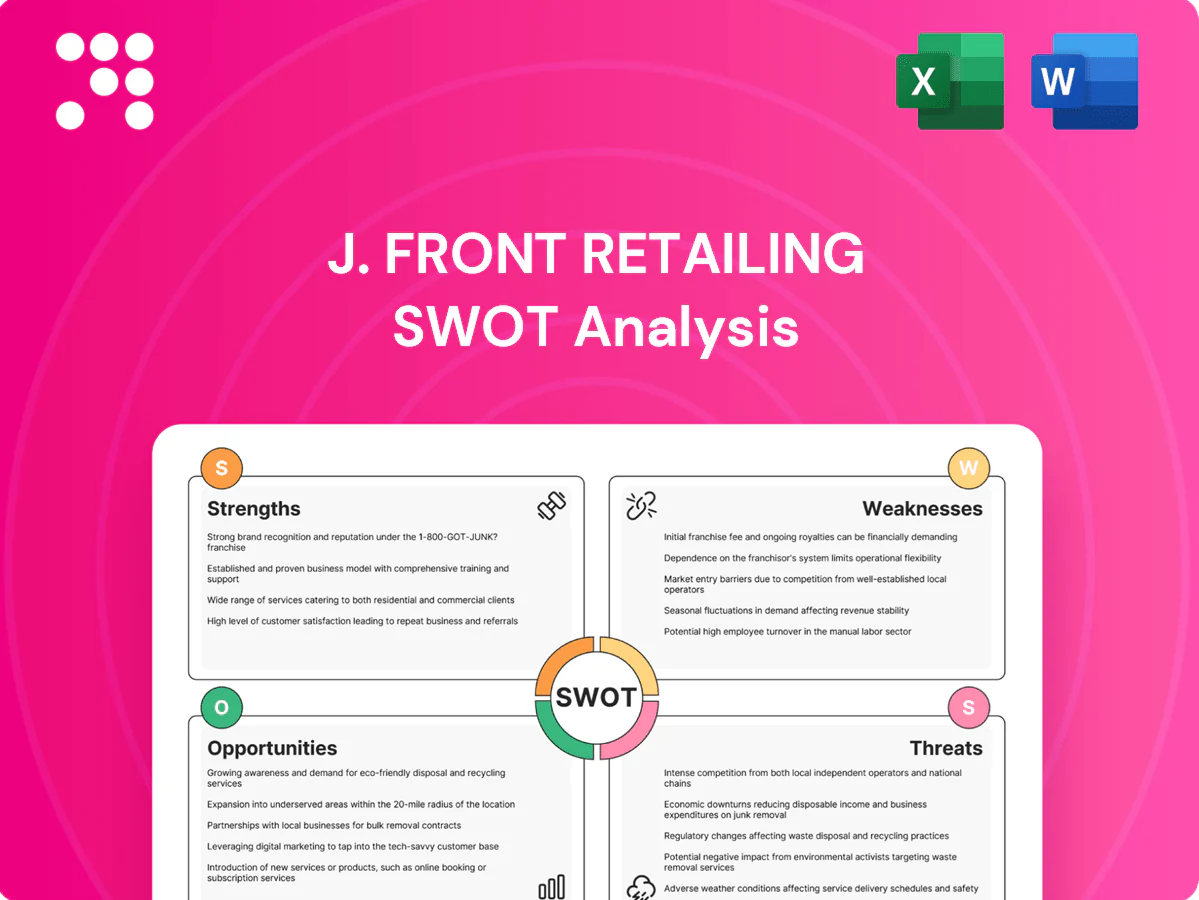

Our J. Front Retailing SWOT analysis uncovers strengths like strong domestic brand portfolio and omnichannel capabilities, alongside weaknesses and risks from intense competition and demographic shifts. Ideal for investors and strategists, it highlights growth levers and threat mitigations. Purchase the full, editable SWOT (Word + Excel) to access detailed, actionable insights for planning and investment.

Strengths

Iconic department store brands

Centuries-old Daimaru (founded 1717) and Matsuzakaya (roots 1611) underpin J. Front Retailing with over 300 and 400 years of brand equity and trust, supporting premium positioning and strong vendor relationships. Their combined flagship network (about 10 department stores) drives domestic footfall and tourist appeal, enabling selective pricing power in luxury and cosmetics categories.

Diversified multi-segment portfolio

J. Front Retailing operates Daimaru and Matsuzakaya department stores alongside specialty retail, credit finance and real estate businesses, creating multiple revenue streams that smooth retail cyclicality and boost cross-selling; finance and property operations provide higher margin resilience than pure retail, and the portfolio breadth supports risk management and capital recycling across cycles.

Prime urban locations

Flagship stores sit in high-traffic city centers such as Tokyo (Nihonbashi/Mitsukoshimae) and Osaka (Umeda), providing superior access that boosts luxury, cosmetics and gifting sales. Control of core real estate enables redevelopment upside and mixed-use conversion to capture higher footfall and rents. Locations amplify inbound tourism capture as visitors recover from 31.9 million in 2019 to 20.8 million in 2023, supporting retail rebound as travel normalizes.

Loyal customer base and CRM

Established membership and card programs deepen retention, with the group emphasizing member-driven sales growth in 2024. Rich transaction data enables targeted promotions and curated assortments that lift basket value. Concentration of high-value customers sustains key categories and reduces reliance on mass discounting.

- Membership-driven retention

- Data-enabled targeting

- High-value customer concentration

- Lower dependence on broad discounts

Growing omni-channel capability

Integrated online-to-offline services boost convenience for J. Front Retailing, with click-and-collect, virtual selling and appointment services lifting conversion rates and average basket size. Unified inventory across channels improves product availability and supports higher margins by reducing markdowns. Expanded digital touchpoints strengthen brand engagement and customer lifetime value.

- omni-channel convenience

- click-and-collect & virtual selling

- unified inventory = better availability & margin

- digital touchpoints → stronger engagement

Heritage retailers grow premium sales via membership as tourism hits 20.8M

Heritage brands Daimaru (1717) and Matsuzakaya (1611) provide deep trust and premium positioning across ~10 flagship department stores. Diversified mix—retail, credit finance, real estate—smooths cyclicality and sustains margins; group emphasised member-driven sales growth in 2024. Prime city locations and tourism rebound (31.9M visitors in 2019 → 20.8M in 2023) boost luxury and cosmetics demand.

| Metric | Value |

|---|---|

| Founding years | Daimaru 1717; Matsuzakaya 1611 |

| Flagship stores | ~10 |

| Inbound tourists | 31.9M (2019) → 20.8M (2023) |

| 2024 focus | Membership-driven sales growth |

What is included in the product

Delivers a strategic overview of J. Front Retailing’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, key growth drivers, operational gaps and market risks shaping future performance.

Provides a concise SWOT matrix tailored to J. Front Retailing for fast strategic alignment across retail operations, ideal for executives needing a clear snapshot of strengths, weaknesses, opportunities, and threats for quick decision-making.

Weaknesses

Structural decline in department stores

Legacy department store formats at J. Front face traffic loss to e-commerce (Japan online retail penetration rose to about 15.6% in 2024) and specialty chains, compressing same-store traffic and sales. Floor productivity struggles to keep pace with rising rent and labor, while category mix remains skewed to mature segments like apparel and household goods. Turnaround will require sustained reinvestment and careful curation of brands and space.

High fixed-cost base

Large footprints and premium locations — around 40 department stores under the J. Front group — drive elevated rent and maintenance fixed expenses. High operating leverage means a modest sales decline quickly depresses operating profit. Staffing levels and strict service standards limit the speed and extent of cost cuts. Profitability remains highly sensitive to short-term sales volatility.

Domestic market dependence

Revenue remains concentrated in Japan, exposing J. Front to a mature market where Japan’s population is about 125 million and aging rapidly, constraining long-term volume growth; limited overseas exposure reduces geographic diversification, while swings in the yen (around 155 JPY/USD in 2024) and volatile inbound tourism (28.7 million visitors in 2023) add profit and cash‑flow volatility.

Digital scale gap vs pure-plays

J. Front Retailing's digital scale lags pure-play rivals, with online sales penetration around 8% of group revenue in 2024 versus 20–30% for leading e-commerce players, limiting assortment depth and fulfillment reach.

Customers demand faster delivery and lower prices, compressing margins as logistics costs rise; tech investment must compete with store capex and maintenance.

Complex data integration across department store, specialty and online units slows personalization and omnichannel optimization.

- Online penetration ~8% (2024)

- Pure-play peer range 20–30%

- Logistics and tech capex trade-offs

- Fragmented data across units

Portfolio complexity

Department stores (≈40) face traffic loss; online penetration ~8% vs peers

Legacy department stores (≈40 stores) see traffic loss to e-commerce; online penetration ~8% of group sales (2024) vs peers 20–30%, while FY2023 revenue ¥1,074bn. High fixed costs and rent sensitivity compress margins; yen ~155 JPY/USD (2024) and inbound tourism volatility (28.7m in 2023) add cash‑flow risk.

| Metric | Value |

|---|---|

| Online penetration (2024) | ~8% |

| Revenue FY2023 | ¥1,074bn |

| Stores | ~40 |

| Yen (2024) | ~155 JPY/USD |

| Inbound tourists (2023) | 28.7m |

Full Version Awaits

J. Front Retailing SWOT Analysis

This is a real excerpt from the J. Front Retailing SWOT analysis you’re viewing—the same professional document you’ll receive after purchase. The preview below is pulled directly from the full, editable report, so there are no surprises. Buy now to unlock the complete, detailed SWOT file ready for immediate download and use.

Make Insightful Decisions Backed by Expert Research

Our J. Front Retailing SWOT analysis uncovers strengths like strong domestic brand portfolio and omnichannel capabilities, alongside weaknesses and risks from intense competition and demographic shifts. Ideal for investors and strategists, it highlights growth levers and threat mitigations. Purchase the full, editable SWOT (Word + Excel) to access detailed, actionable insights for planning and investment.

Strengths

Iconic department store brands

Centuries-old Daimaru (founded 1717) and Matsuzakaya (roots 1611) underpin J. Front Retailing with over 300 and 400 years of brand equity and trust, supporting premium positioning and strong vendor relationships. Their combined flagship network (about 10 department stores) drives domestic footfall and tourist appeal, enabling selective pricing power in luxury and cosmetics categories.

Diversified multi-segment portfolio

J. Front Retailing operates Daimaru and Matsuzakaya department stores alongside specialty retail, credit finance and real estate businesses, creating multiple revenue streams that smooth retail cyclicality and boost cross-selling; finance and property operations provide higher margin resilience than pure retail, and the portfolio breadth supports risk management and capital recycling across cycles.

Prime urban locations

Flagship stores sit in high-traffic city centers such as Tokyo (Nihonbashi/Mitsukoshimae) and Osaka (Umeda), providing superior access that boosts luxury, cosmetics and gifting sales. Control of core real estate enables redevelopment upside and mixed-use conversion to capture higher footfall and rents. Locations amplify inbound tourism capture as visitors recover from 31.9 million in 2019 to 20.8 million in 2023, supporting retail rebound as travel normalizes.

Loyal customer base and CRM

Established membership and card programs deepen retention, with the group emphasizing member-driven sales growth in 2024. Rich transaction data enables targeted promotions and curated assortments that lift basket value. Concentration of high-value customers sustains key categories and reduces reliance on mass discounting.

- Membership-driven retention

- Data-enabled targeting

- High-value customer concentration

- Lower dependence on broad discounts

Growing omni-channel capability

Integrated online-to-offline services boost convenience for J. Front Retailing, with click-and-collect, virtual selling and appointment services lifting conversion rates and average basket size. Unified inventory across channels improves product availability and supports higher margins by reducing markdowns. Expanded digital touchpoints strengthen brand engagement and customer lifetime value.

- omni-channel convenience

- click-and-collect & virtual selling

- unified inventory = better availability & margin

- digital touchpoints → stronger engagement

Heritage retailers grow premium sales via membership as tourism hits 20.8M

Heritage brands Daimaru (1717) and Matsuzakaya (1611) provide deep trust and premium positioning across ~10 flagship department stores. Diversified mix—retail, credit finance, real estate—smooths cyclicality and sustains margins; group emphasised member-driven sales growth in 2024. Prime city locations and tourism rebound (31.9M visitors in 2019 → 20.8M in 2023) boost luxury and cosmetics demand.

| Metric | Value |

|---|---|

| Founding years | Daimaru 1717; Matsuzakaya 1611 |

| Flagship stores | ~10 |

| Inbound tourists | 31.9M (2019) → 20.8M (2023) |

| 2024 focus | Membership-driven sales growth |

What is included in the product

Delivers a strategic overview of J. Front Retailing’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, key growth drivers, operational gaps and market risks shaping future performance.

Provides a concise SWOT matrix tailored to J. Front Retailing for fast strategic alignment across retail operations, ideal for executives needing a clear snapshot of strengths, weaknesses, opportunities, and threats for quick decision-making.

Weaknesses

Structural decline in department stores

Legacy department store formats at J. Front face traffic loss to e-commerce (Japan online retail penetration rose to about 15.6% in 2024) and specialty chains, compressing same-store traffic and sales. Floor productivity struggles to keep pace with rising rent and labor, while category mix remains skewed to mature segments like apparel and household goods. Turnaround will require sustained reinvestment and careful curation of brands and space.

High fixed-cost base

Large footprints and premium locations — around 40 department stores under the J. Front group — drive elevated rent and maintenance fixed expenses. High operating leverage means a modest sales decline quickly depresses operating profit. Staffing levels and strict service standards limit the speed and extent of cost cuts. Profitability remains highly sensitive to short-term sales volatility.

Domestic market dependence

Revenue remains concentrated in Japan, exposing J. Front to a mature market where Japan’s population is about 125 million and aging rapidly, constraining long-term volume growth; limited overseas exposure reduces geographic diversification, while swings in the yen (around 155 JPY/USD in 2024) and volatile inbound tourism (28.7 million visitors in 2023) add profit and cash‑flow volatility.

Digital scale gap vs pure-plays

J. Front Retailing's digital scale lags pure-play rivals, with online sales penetration around 8% of group revenue in 2024 versus 20–30% for leading e-commerce players, limiting assortment depth and fulfillment reach.

Customers demand faster delivery and lower prices, compressing margins as logistics costs rise; tech investment must compete with store capex and maintenance.

Complex data integration across department store, specialty and online units slows personalization and omnichannel optimization.

- Online penetration ~8% (2024)

- Pure-play peer range 20–30%

- Logistics and tech capex trade-offs

- Fragmented data across units

Portfolio complexity

Department stores (≈40) face traffic loss; online penetration ~8% vs peers

Legacy department stores (≈40 stores) see traffic loss to e-commerce; online penetration ~8% of group sales (2024) vs peers 20–30%, while FY2023 revenue ¥1,074bn. High fixed costs and rent sensitivity compress margins; yen ~155 JPY/USD (2024) and inbound tourism volatility (28.7m in 2023) add cash‑flow risk.

| Metric | Value |

|---|---|

| Online penetration (2024) | ~8% |

| Revenue FY2023 | ¥1,074bn |

| Stores | ~40 |

| Yen (2024) | ~155 JPY/USD |

| Inbound tourists (2023) | 28.7m |

Full Version Awaits

J. Front Retailing SWOT Analysis

This is a real excerpt from the J. Front Retailing SWOT analysis you’re viewing—the same professional document you’ll receive after purchase. The preview below is pulled directly from the full, editable report, so there are no surprises. Buy now to unlock the complete, detailed SWOT file ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Our J. Front Retailing SWOT analysis uncovers strengths like strong domestic brand portfolio and omnichannel capabilities, alongside weaknesses and risks from intense competition and demographic shifts. Ideal for investors and strategists, it highlights growth levers and threat mitigations. Purchase the full, editable SWOT (Word + Excel) to access detailed, actionable insights for planning and investment.

Strengths

Iconic department store brands

Centuries-old Daimaru (founded 1717) and Matsuzakaya (roots 1611) underpin J. Front Retailing with over 300 and 400 years of brand equity and trust, supporting premium positioning and strong vendor relationships. Their combined flagship network (about 10 department stores) drives domestic footfall and tourist appeal, enabling selective pricing power in luxury and cosmetics categories.

Diversified multi-segment portfolio

J. Front Retailing operates Daimaru and Matsuzakaya department stores alongside specialty retail, credit finance and real estate businesses, creating multiple revenue streams that smooth retail cyclicality and boost cross-selling; finance and property operations provide higher margin resilience than pure retail, and the portfolio breadth supports risk management and capital recycling across cycles.

Prime urban locations

Flagship stores sit in high-traffic city centers such as Tokyo (Nihonbashi/Mitsukoshimae) and Osaka (Umeda), providing superior access that boosts luxury, cosmetics and gifting sales. Control of core real estate enables redevelopment upside and mixed-use conversion to capture higher footfall and rents. Locations amplify inbound tourism capture as visitors recover from 31.9 million in 2019 to 20.8 million in 2023, supporting retail rebound as travel normalizes.

Loyal customer base and CRM

Established membership and card programs deepen retention, with the group emphasizing member-driven sales growth in 2024. Rich transaction data enables targeted promotions and curated assortments that lift basket value. Concentration of high-value customers sustains key categories and reduces reliance on mass discounting.

- Membership-driven retention

- Data-enabled targeting

- High-value customer concentration

- Lower dependence on broad discounts

Growing omni-channel capability

Integrated online-to-offline services boost convenience for J. Front Retailing, with click-and-collect, virtual selling and appointment services lifting conversion rates and average basket size. Unified inventory across channels improves product availability and supports higher margins by reducing markdowns. Expanded digital touchpoints strengthen brand engagement and customer lifetime value.

- omni-channel convenience

- click-and-collect & virtual selling

- unified inventory = better availability & margin

- digital touchpoints → stronger engagement

Heritage retailers grow premium sales via membership as tourism hits 20.8M

Heritage brands Daimaru (1717) and Matsuzakaya (1611) provide deep trust and premium positioning across ~10 flagship department stores. Diversified mix—retail, credit finance, real estate—smooths cyclicality and sustains margins; group emphasised member-driven sales growth in 2024. Prime city locations and tourism rebound (31.9M visitors in 2019 → 20.8M in 2023) boost luxury and cosmetics demand.

| Metric | Value |

|---|---|

| Founding years | Daimaru 1717; Matsuzakaya 1611 |

| Flagship stores | ~10 |

| Inbound tourists | 31.9M (2019) → 20.8M (2023) |

| 2024 focus | Membership-driven sales growth |

What is included in the product

Delivers a strategic overview of J. Front Retailing’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, key growth drivers, operational gaps and market risks shaping future performance.

Provides a concise SWOT matrix tailored to J. Front Retailing for fast strategic alignment across retail operations, ideal for executives needing a clear snapshot of strengths, weaknesses, opportunities, and threats for quick decision-making.

Weaknesses

Structural decline in department stores

Legacy department store formats at J. Front face traffic loss to e-commerce (Japan online retail penetration rose to about 15.6% in 2024) and specialty chains, compressing same-store traffic and sales. Floor productivity struggles to keep pace with rising rent and labor, while category mix remains skewed to mature segments like apparel and household goods. Turnaround will require sustained reinvestment and careful curation of brands and space.

High fixed-cost base

Large footprints and premium locations — around 40 department stores under the J. Front group — drive elevated rent and maintenance fixed expenses. High operating leverage means a modest sales decline quickly depresses operating profit. Staffing levels and strict service standards limit the speed and extent of cost cuts. Profitability remains highly sensitive to short-term sales volatility.

Domestic market dependence

Revenue remains concentrated in Japan, exposing J. Front to a mature market where Japan’s population is about 125 million and aging rapidly, constraining long-term volume growth; limited overseas exposure reduces geographic diversification, while swings in the yen (around 155 JPY/USD in 2024) and volatile inbound tourism (28.7 million visitors in 2023) add profit and cash‑flow volatility.

Digital scale gap vs pure-plays

J. Front Retailing's digital scale lags pure-play rivals, with online sales penetration around 8% of group revenue in 2024 versus 20–30% for leading e-commerce players, limiting assortment depth and fulfillment reach.

Customers demand faster delivery and lower prices, compressing margins as logistics costs rise; tech investment must compete with store capex and maintenance.

Complex data integration across department store, specialty and online units slows personalization and omnichannel optimization.

- Online penetration ~8% (2024)

- Pure-play peer range 20–30%

- Logistics and tech capex trade-offs

- Fragmented data across units

Portfolio complexity

Department stores (≈40) face traffic loss; online penetration ~8% vs peers

Legacy department stores (≈40 stores) see traffic loss to e-commerce; online penetration ~8% of group sales (2024) vs peers 20–30%, while FY2023 revenue ¥1,074bn. High fixed costs and rent sensitivity compress margins; yen ~155 JPY/USD (2024) and inbound tourism volatility (28.7m in 2023) add cash‑flow risk.

| Metric | Value |

|---|---|

| Online penetration (2024) | ~8% |

| Revenue FY2023 | ¥1,074bn |

| Stores | ~40 |

| Yen (2024) | ~155 JPY/USD |

| Inbound tourists (2023) | 28.7m |

Full Version Awaits

J. Front Retailing SWOT Analysis

This is a real excerpt from the J. Front Retailing SWOT analysis you’re viewing—the same professional document you’ll receive after purchase. The preview below is pulled directly from the full, editable report, so there are no surprises. Buy now to unlock the complete, detailed SWOT file ready for immediate download and use.