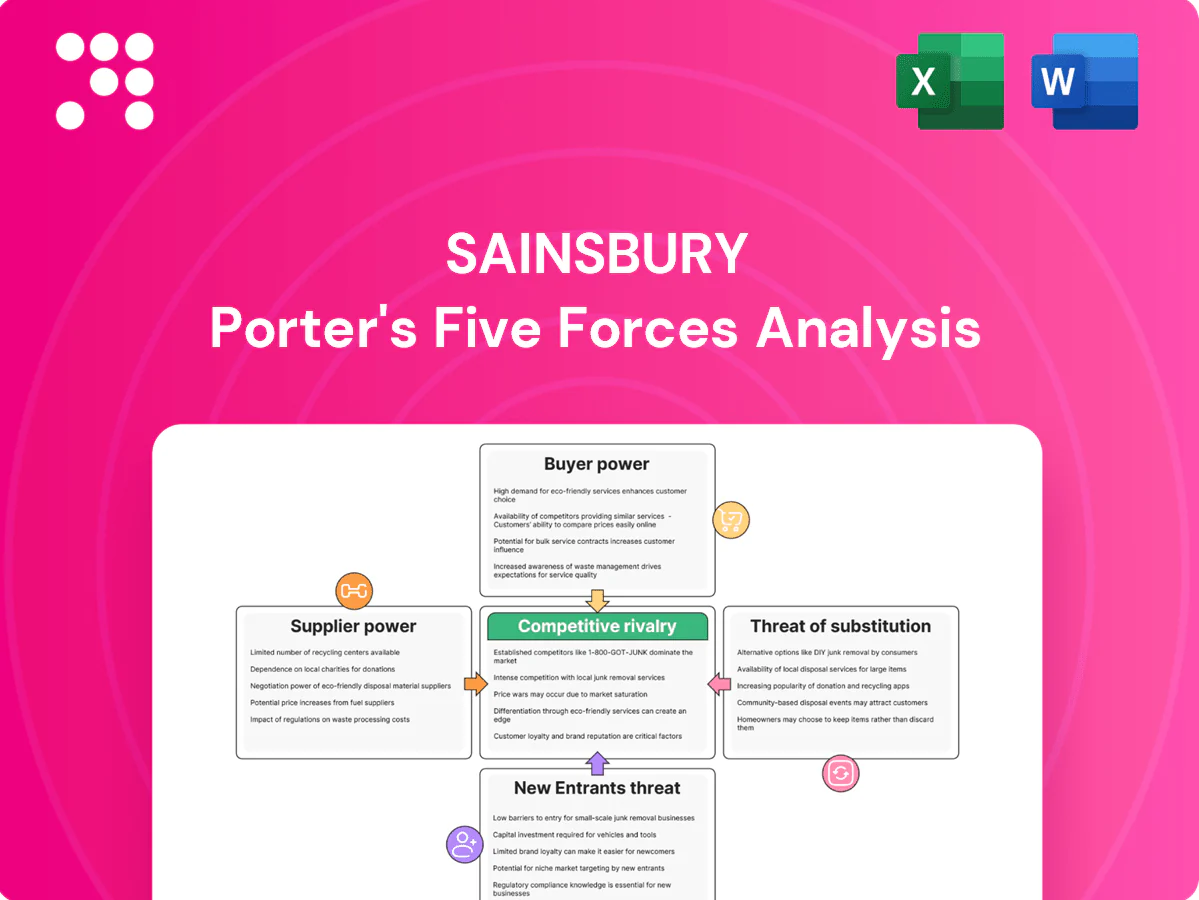

Sainsbury Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Sainsbury’s faces intense competitive pressure from discount grocers, strong buyer bargaining and evolving retail formats, while supplier leverage and digital disruption shape margins and growth prospects. This snapshot highlights key tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sainsbury’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base dilutes leverage

Thousands of food, general merchandise and clothing suppliers—over 7,000 across categories—limit any single vendor’s bargaining power with Sainsbury’s, allowing rapid switching for commoditized goods. Multi-sourcing and global procurement highlighted in Sainsbury’s 2024 reporting reduce dependency risk and support cost resilience. Niche premium or local-provenance lines, however, retain concentrated influence and can command price premiums.

Private label scale strengthens negotiation

Sainsbury's over-40% own-brand penetration in 2024 strengthens cost control and specification power, allowing the retailer to dictate formulations and margins. Consolidated private-label volumes provide bargaining leverage to push for better pricing and quality from suppliers. It can rapidly backfill branded gaps with own-label alternatives, though commitments to quality and ESG standards constrain overly aggressive cost reductions.

Commodity and FX volatility raises input pressure

Fluctuations in energy, grain and packaging costs flow directly into supplier pricing, with UK food inflation averaging about 6.0% in 2024 (ONS), amplifying input pressure on Sainsbury. Currency moves in 2024 raised costs on imported goods and Argos categories, prompting suppliers to seek pass-throughs that test Sainsbury’s margin and pricing stance. Hedging, multi-year supplier contracts and reformulation have partially mitigated cost spikes.

Logistics, tech, and data vendors hold niche power

Logistics, tech and data vendors exert niche supplier power for Sainsbury: reliance on distribution partners, last-mile carriers and IT platforms creates switching frictions; UK online grocery penetration ~13% in 2024 and Sainsbury held ~14.2% market share (Kantar 2024), so outages or carrier capacity constraints can materially hit availability and online service. Payment, data and cybersecurity providers are critical nodes; contracting for redundancy reduces concentration risk.

- Dependence on carriers: switching costs high

- Online reach: 13% UK grocery (2024)

- Market share: Sainsbury ~14.2% (Kantar 2024)

- Mitigation: multi-supplier redundancy

Fresh, seasonal, and branded categories vary power

Perishable produce and tight seasonal windows increase supplier leverage, especially for specialist growers and importers where lead times compress and substitution is limited. Global brands in beverages, confectionery and beauty retain strong shelf and promotional pull, while Sainsbury’s 2024 UK grocery market share stood at about 14.2% (Kantar), informing its range and space decisions. Joint business plans align incentives but increase supplier dependency through shared promotions and forecasts.

- Perishables: tighter windows raise leverage

- Global brands: strong shelf/marketing pull

- Sainsbury market share: ~14.2% (Kantar 2024)

- Range curation/space fees mitigate but create dependency via joint plans

Over 7,000 suppliers and 40% own-brand cap supplier power; niche growers hold leverage

Thousands of suppliers (>7,000), high multi-sourcing and >40% own-brand (2024) limit supplier power, but niche premium growers and global brands retain leverage. Input inflation (~6% UK food 2024) and import costs raise supplier pass-through pressure. Logistics/IT vendor concentration and perishables seasonality create switching frictions despite multi-supplier mitigation.

| Metric | 2024 |

|---|---|

| Supplier count | >7,000 |

| Own-brand penetration | >40% |

| UK grocery share (Sainsbury) | ~14.2% (Kantar) |

| UK food inflation | ~6.0% (ONS) |

What is included in the product

Porter’s Five Forces analysis for Sainsbury uncovers competitive intensity, supplier and buyer leverage, threat of new entrants and substitutes, and industry-specific barriers, with strategic insights to protect market share and profitability.

A concise, one-sheet Sainsbury Porter's Five Forces that instantly highlights competitive pain points with a customizable radar chart and pressure sliders—ready to drop into pitch decks or Excel dashboards and easy for non-finance users to update with current data.

Customers Bargaining Power

High price sensitivity in UK grocery

Cost-of-living pressures keep UK shoppers intensely value-focused, so even small price gaps push switching to discounters or rivals; Aldi and Lidl held roughly 16% combined share (Kantar 2024) while Sainsbury’s retained about 15% (Kantar 2024). Sainsbury’s value tiers and frequent price campaigns must be credible to prevent churn. The margin mix depends on balancing low-margin staples with higher-margin own-label and convenience lines.

Low switching costs across channels

Low switching costs let shoppers move freely between Tesco (27.5%), Sainsbury’s (14.9%), Asda (14.6%), Aldi (10.3%) and Lidl (8.5%) per Kantar 2024, with online grocery penetration ~14% boosting rivals. Delivery slots, substitutions and app UX drive repeat choice; 1 in 4 shoppers cite slot availability as decisive. Argos buyers benchmark against Amazon and specialists. Convenience and speed are critical retention levers.

Loyalty ecosystems temper power

Nectar loyalty (over 18 million members) plus personalized offers and SmartShop perks create strong stickiness for Sainsbury’s by embedding rewards and convenience into shopping behavior. Data-driven pricing and targeted promotions further narrow perceived price differentials. However, rival loyalty schemes reduce uniqueness, so benefits must stay tangible and frequent to prevent churn.

Transparency and reviews amplify choice

Transparency from price-matching, comparison sites and social reviews raises buyer knowledge, shifting leverage to customers who can easily find lower prices and alternatives.

Poor service or stock-outs are quickly penalized via instant online feedback; Argos product ratings now directly affect conversion rates and return frequencies, making reputation management a core defense for Sainsbury.

- price-matching increases visible competition

- comparison sites amplify switching ease

- social reviews drive conversion and returns

- reputation management is strategic

Substitution across baskets and formats

Shoppers can downtrade to Sainsbury’s own-label, buy smaller pack sizes, or switch cuisines, and commonly split baskets across retailers to maximise value. Convenience missions increasingly shift to c-stores and quick-commerce, forcing channel mix and assortment changes. To retain spend Sainsbury’s must serve value, convenience and full-shop missions seamlessly across formats.

- Sainsbury’s UK grocery market share ~15.3% (Kantar 2024)

UK grocery shoppers flip on small price gaps; delivery slots, loyalty and reviews sway choices

Cost-sensitive UK shoppers switch on small price gaps; Sainsbury’s 15.3% share vs Aldi+Lidl ~16% (Kantar 2024), online grocery ~14% penetration and 1-in-4 shoppers citing delivery slots as decisive. Nectar >18m members and SmartShop drive retention but rival schemes and price-matching raise buyer leverage. Stock-outs, reviews and Argos ratings quickly affect conversion and returns.

| Metric | Value |

|---|---|

| Market share (Sainsbury) | 15.3% |

| Aldi+Lidl | ~16% |

| Online grocery | ~14% |

| Nectar members | >18m |

Preview Before You Purchase

Sainsbury Porter's Five Forces Analysis

This preview shows the exact Sainsbury Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document provides a concise evaluation of competitive rivalry, buyer and supplier power, substitution risk, and barriers to entry tailored to Sainsbury. It's professionally formatted and ready for instant download and use upon payment.

A Must-Have Tool for Decision-Makers

Sainsbury’s faces intense competitive pressure from discount grocers, strong buyer bargaining and evolving retail formats, while supplier leverage and digital disruption shape margins and growth prospects. This snapshot highlights key tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sainsbury’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base dilutes leverage

Thousands of food, general merchandise and clothing suppliers—over 7,000 across categories—limit any single vendor’s bargaining power with Sainsbury’s, allowing rapid switching for commoditized goods. Multi-sourcing and global procurement highlighted in Sainsbury’s 2024 reporting reduce dependency risk and support cost resilience. Niche premium or local-provenance lines, however, retain concentrated influence and can command price premiums.

Private label scale strengthens negotiation

Sainsbury's over-40% own-brand penetration in 2024 strengthens cost control and specification power, allowing the retailer to dictate formulations and margins. Consolidated private-label volumes provide bargaining leverage to push for better pricing and quality from suppliers. It can rapidly backfill branded gaps with own-label alternatives, though commitments to quality and ESG standards constrain overly aggressive cost reductions.

Commodity and FX volatility raises input pressure

Fluctuations in energy, grain and packaging costs flow directly into supplier pricing, with UK food inflation averaging about 6.0% in 2024 (ONS), amplifying input pressure on Sainsbury. Currency moves in 2024 raised costs on imported goods and Argos categories, prompting suppliers to seek pass-throughs that test Sainsbury’s margin and pricing stance. Hedging, multi-year supplier contracts and reformulation have partially mitigated cost spikes.

Logistics, tech, and data vendors hold niche power

Logistics, tech and data vendors exert niche supplier power for Sainsbury: reliance on distribution partners, last-mile carriers and IT platforms creates switching frictions; UK online grocery penetration ~13% in 2024 and Sainsbury held ~14.2% market share (Kantar 2024), so outages or carrier capacity constraints can materially hit availability and online service. Payment, data and cybersecurity providers are critical nodes; contracting for redundancy reduces concentration risk.

- Dependence on carriers: switching costs high

- Online reach: 13% UK grocery (2024)

- Market share: Sainsbury ~14.2% (Kantar 2024)

- Mitigation: multi-supplier redundancy

Fresh, seasonal, and branded categories vary power

Perishable produce and tight seasonal windows increase supplier leverage, especially for specialist growers and importers where lead times compress and substitution is limited. Global brands in beverages, confectionery and beauty retain strong shelf and promotional pull, while Sainsbury’s 2024 UK grocery market share stood at about 14.2% (Kantar), informing its range and space decisions. Joint business plans align incentives but increase supplier dependency through shared promotions and forecasts.

- Perishables: tighter windows raise leverage

- Global brands: strong shelf/marketing pull

- Sainsbury market share: ~14.2% (Kantar 2024)

- Range curation/space fees mitigate but create dependency via joint plans

Over 7,000 suppliers and 40% own-brand cap supplier power; niche growers hold leverage

Thousands of suppliers (>7,000), high multi-sourcing and >40% own-brand (2024) limit supplier power, but niche premium growers and global brands retain leverage. Input inflation (~6% UK food 2024) and import costs raise supplier pass-through pressure. Logistics/IT vendor concentration and perishables seasonality create switching frictions despite multi-supplier mitigation.

| Metric | 2024 |

|---|---|

| Supplier count | >7,000 |

| Own-brand penetration | >40% |

| UK grocery share (Sainsbury) | ~14.2% (Kantar) |

| UK food inflation | ~6.0% (ONS) |

What is included in the product

Porter’s Five Forces analysis for Sainsbury uncovers competitive intensity, supplier and buyer leverage, threat of new entrants and substitutes, and industry-specific barriers, with strategic insights to protect market share and profitability.

A concise, one-sheet Sainsbury Porter's Five Forces that instantly highlights competitive pain points with a customizable radar chart and pressure sliders—ready to drop into pitch decks or Excel dashboards and easy for non-finance users to update with current data.

Customers Bargaining Power

High price sensitivity in UK grocery

Cost-of-living pressures keep UK shoppers intensely value-focused, so even small price gaps push switching to discounters or rivals; Aldi and Lidl held roughly 16% combined share (Kantar 2024) while Sainsbury’s retained about 15% (Kantar 2024). Sainsbury’s value tiers and frequent price campaigns must be credible to prevent churn. The margin mix depends on balancing low-margin staples with higher-margin own-label and convenience lines.

Low switching costs across channels

Low switching costs let shoppers move freely between Tesco (27.5%), Sainsbury’s (14.9%), Asda (14.6%), Aldi (10.3%) and Lidl (8.5%) per Kantar 2024, with online grocery penetration ~14% boosting rivals. Delivery slots, substitutions and app UX drive repeat choice; 1 in 4 shoppers cite slot availability as decisive. Argos buyers benchmark against Amazon and specialists. Convenience and speed are critical retention levers.

Loyalty ecosystems temper power

Nectar loyalty (over 18 million members) plus personalized offers and SmartShop perks create strong stickiness for Sainsbury’s by embedding rewards and convenience into shopping behavior. Data-driven pricing and targeted promotions further narrow perceived price differentials. However, rival loyalty schemes reduce uniqueness, so benefits must stay tangible and frequent to prevent churn.

Transparency and reviews amplify choice

Transparency from price-matching, comparison sites and social reviews raises buyer knowledge, shifting leverage to customers who can easily find lower prices and alternatives.

Poor service or stock-outs are quickly penalized via instant online feedback; Argos product ratings now directly affect conversion rates and return frequencies, making reputation management a core defense for Sainsbury.

- price-matching increases visible competition

- comparison sites amplify switching ease

- social reviews drive conversion and returns

- reputation management is strategic

Substitution across baskets and formats

Shoppers can downtrade to Sainsbury’s own-label, buy smaller pack sizes, or switch cuisines, and commonly split baskets across retailers to maximise value. Convenience missions increasingly shift to c-stores and quick-commerce, forcing channel mix and assortment changes. To retain spend Sainsbury’s must serve value, convenience and full-shop missions seamlessly across formats.

- Sainsbury’s UK grocery market share ~15.3% (Kantar 2024)

UK grocery shoppers flip on small price gaps; delivery slots, loyalty and reviews sway choices

Cost-sensitive UK shoppers switch on small price gaps; Sainsbury’s 15.3% share vs Aldi+Lidl ~16% (Kantar 2024), online grocery ~14% penetration and 1-in-4 shoppers citing delivery slots as decisive. Nectar >18m members and SmartShop drive retention but rival schemes and price-matching raise buyer leverage. Stock-outs, reviews and Argos ratings quickly affect conversion and returns.

| Metric | Value |

|---|---|

| Market share (Sainsbury) | 15.3% |

| Aldi+Lidl | ~16% |

| Online grocery | ~14% |

| Nectar members | >18m |

Preview Before You Purchase

Sainsbury Porter's Five Forces Analysis

This preview shows the exact Sainsbury Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document provides a concise evaluation of competitive rivalry, buyer and supplier power, substitution risk, and barriers to entry tailored to Sainsbury. It's professionally formatted and ready for instant download and use upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Sainsbury’s faces intense competitive pressure from discount grocers, strong buyer bargaining and evolving retail formats, while supplier leverage and digital disruption shape margins and growth prospects. This snapshot highlights key tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sainsbury’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base dilutes leverage

Thousands of food, general merchandise and clothing suppliers—over 7,000 across categories—limit any single vendor’s bargaining power with Sainsbury’s, allowing rapid switching for commoditized goods. Multi-sourcing and global procurement highlighted in Sainsbury’s 2024 reporting reduce dependency risk and support cost resilience. Niche premium or local-provenance lines, however, retain concentrated influence and can command price premiums.

Private label scale strengthens negotiation

Sainsbury's over-40% own-brand penetration in 2024 strengthens cost control and specification power, allowing the retailer to dictate formulations and margins. Consolidated private-label volumes provide bargaining leverage to push for better pricing and quality from suppliers. It can rapidly backfill branded gaps with own-label alternatives, though commitments to quality and ESG standards constrain overly aggressive cost reductions.

Commodity and FX volatility raises input pressure

Fluctuations in energy, grain and packaging costs flow directly into supplier pricing, with UK food inflation averaging about 6.0% in 2024 (ONS), amplifying input pressure on Sainsbury. Currency moves in 2024 raised costs on imported goods and Argos categories, prompting suppliers to seek pass-throughs that test Sainsbury’s margin and pricing stance. Hedging, multi-year supplier contracts and reformulation have partially mitigated cost spikes.

Logistics, tech, and data vendors hold niche power

Logistics, tech and data vendors exert niche supplier power for Sainsbury: reliance on distribution partners, last-mile carriers and IT platforms creates switching frictions; UK online grocery penetration ~13% in 2024 and Sainsbury held ~14.2% market share (Kantar 2024), so outages or carrier capacity constraints can materially hit availability and online service. Payment, data and cybersecurity providers are critical nodes; contracting for redundancy reduces concentration risk.

- Dependence on carriers: switching costs high

- Online reach: 13% UK grocery (2024)

- Market share: Sainsbury ~14.2% (Kantar 2024)

- Mitigation: multi-supplier redundancy

Fresh, seasonal, and branded categories vary power

Perishable produce and tight seasonal windows increase supplier leverage, especially for specialist growers and importers where lead times compress and substitution is limited. Global brands in beverages, confectionery and beauty retain strong shelf and promotional pull, while Sainsbury’s 2024 UK grocery market share stood at about 14.2% (Kantar), informing its range and space decisions. Joint business plans align incentives but increase supplier dependency through shared promotions and forecasts.

- Perishables: tighter windows raise leverage

- Global brands: strong shelf/marketing pull

- Sainsbury market share: ~14.2% (Kantar 2024)

- Range curation/space fees mitigate but create dependency via joint plans

Over 7,000 suppliers and 40% own-brand cap supplier power; niche growers hold leverage

Thousands of suppliers (>7,000), high multi-sourcing and >40% own-brand (2024) limit supplier power, but niche premium growers and global brands retain leverage. Input inflation (~6% UK food 2024) and import costs raise supplier pass-through pressure. Logistics/IT vendor concentration and perishables seasonality create switching frictions despite multi-supplier mitigation.

| Metric | 2024 |

|---|---|

| Supplier count | >7,000 |

| Own-brand penetration | >40% |

| UK grocery share (Sainsbury) | ~14.2% (Kantar) |

| UK food inflation | ~6.0% (ONS) |

What is included in the product

Porter’s Five Forces analysis for Sainsbury uncovers competitive intensity, supplier and buyer leverage, threat of new entrants and substitutes, and industry-specific barriers, with strategic insights to protect market share and profitability.

A concise, one-sheet Sainsbury Porter's Five Forces that instantly highlights competitive pain points with a customizable radar chart and pressure sliders—ready to drop into pitch decks or Excel dashboards and easy for non-finance users to update with current data.

Customers Bargaining Power

High price sensitivity in UK grocery

Cost-of-living pressures keep UK shoppers intensely value-focused, so even small price gaps push switching to discounters or rivals; Aldi and Lidl held roughly 16% combined share (Kantar 2024) while Sainsbury’s retained about 15% (Kantar 2024). Sainsbury’s value tiers and frequent price campaigns must be credible to prevent churn. The margin mix depends on balancing low-margin staples with higher-margin own-label and convenience lines.

Low switching costs across channels

Low switching costs let shoppers move freely between Tesco (27.5%), Sainsbury’s (14.9%), Asda (14.6%), Aldi (10.3%) and Lidl (8.5%) per Kantar 2024, with online grocery penetration ~14% boosting rivals. Delivery slots, substitutions and app UX drive repeat choice; 1 in 4 shoppers cite slot availability as decisive. Argos buyers benchmark against Amazon and specialists. Convenience and speed are critical retention levers.

Loyalty ecosystems temper power

Nectar loyalty (over 18 million members) plus personalized offers and SmartShop perks create strong stickiness for Sainsbury’s by embedding rewards and convenience into shopping behavior. Data-driven pricing and targeted promotions further narrow perceived price differentials. However, rival loyalty schemes reduce uniqueness, so benefits must stay tangible and frequent to prevent churn.

Transparency and reviews amplify choice

Transparency from price-matching, comparison sites and social reviews raises buyer knowledge, shifting leverage to customers who can easily find lower prices and alternatives.

Poor service or stock-outs are quickly penalized via instant online feedback; Argos product ratings now directly affect conversion rates and return frequencies, making reputation management a core defense for Sainsbury.

- price-matching increases visible competition

- comparison sites amplify switching ease

- social reviews drive conversion and returns

- reputation management is strategic

Substitution across baskets and formats

Shoppers can downtrade to Sainsbury’s own-label, buy smaller pack sizes, or switch cuisines, and commonly split baskets across retailers to maximise value. Convenience missions increasingly shift to c-stores and quick-commerce, forcing channel mix and assortment changes. To retain spend Sainsbury’s must serve value, convenience and full-shop missions seamlessly across formats.

- Sainsbury’s UK grocery market share ~15.3% (Kantar 2024)

UK grocery shoppers flip on small price gaps; delivery slots, loyalty and reviews sway choices

Cost-sensitive UK shoppers switch on small price gaps; Sainsbury’s 15.3% share vs Aldi+Lidl ~16% (Kantar 2024), online grocery ~14% penetration and 1-in-4 shoppers citing delivery slots as decisive. Nectar >18m members and SmartShop drive retention but rival schemes and price-matching raise buyer leverage. Stock-outs, reviews and Argos ratings quickly affect conversion and returns.

| Metric | Value |

|---|---|

| Market share (Sainsbury) | 15.3% |

| Aldi+Lidl | ~16% |

| Online grocery | ~14% |

| Nectar members | >18m |

Preview Before You Purchase

Sainsbury Porter's Five Forces Analysis

This preview shows the exact Sainsbury Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document provides a concise evaluation of competitive rivalry, buyer and supplier power, substitution risk, and barriers to entry tailored to Sainsbury. It's professionally formatted and ready for instant download and use upon payment.