Jack Henry PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

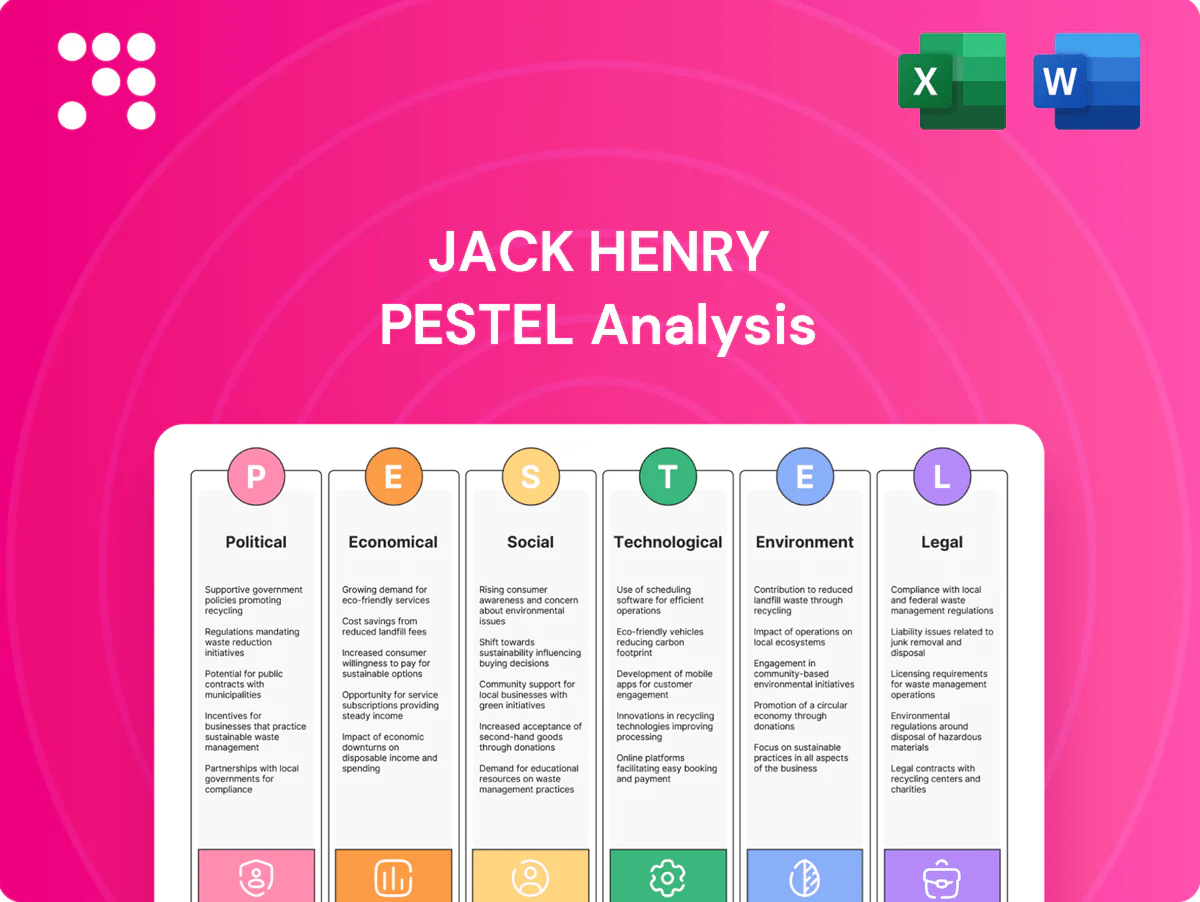

Gain a competitive edge with our PESTLE analysis of Jack Henry. Explore political, economic, social, technological, legal, and environmental trends shaping its strategy and risk profile. Purchase the full, downloadable report for actionable insights and ready-to-use slides and spreadsheets.

Political factors

Regulatory oversight of banking tech

Supervision by banking regulators shapes Jack Henry product standards, certifications, and audit readiness, and in 2024 regulators emphasized third-party risk and payments resilience. Jack Henry must align roadmaps for core, digital, and payments to those supervisory priorities to protect its more than 9,000 client institutions. Policy shifts can accelerate or delay client upgrades, impacting deployment timelines and revenue recognition. Proactive engagement with regulators de-risks rollouts and shortens remediation cycles.

Government cybersecurity initiatives

National cyber directives and funding—backed by SEC incident rules in 2024 and growing CISA resources—push stronger controls across financial infrastructure, raising baseline expectations for vendors and clients. IBM 2024 reports average breach costs around $4.45M (financials ~$5–6M), so compliance raises costs but bolsters trust and sales. Participation in FS-ISAC and public–private intel sharing (7,000+ members) improves resilience.

Public sector payments and RTP policy

Government support for instant payments, including the Federal Reserve's FedNow launched July 2023, accelerates institutional adoption timelines. Community institutions increasingly rely on vendors for compliance and connectivity, seeking turnkey RTP integrations. Jack Henry, which serves over 9,000 financial institutions, can convert RTP enablement into competitive wins. Clear policy reduces integration uncertainty and shortens time-to-market.

Rural and community banking policy support

Geopolitical supply chain and talent

Global tensions strain hardware sourcing, cloud capacity and security talent — the ISC2 2023 global cybersecurity workforce gap was about 3.4 million, limiting hires. US/EC export controls since 2022 constrain some partnerships and advanced tools. Jack Henry and peers mitigate via diversified vendors and nearshoring; continuity planning preserves institutional service levels.

- 3.4M cybersecurity workforce gap (ISC2 2023)

- Export controls (post-2022) limit some tech partnerships

- Diversified vendors + nearshoring reduce supply risk

- Continuity plans protect service SLAs

Regulatory push forces core banking vendor to shore up 9,000 clients, $1.6B

Regulatory focus on third-party risk, payments resilience and cyber rules (SEC/CISA 2024) forces Jack Henry to align roadmaps to protect 9,000 clients and $1.6B FY2024 revenue. FedNow and instant-pay policy accelerate RTP demand among ~3,300 community banks. Export controls and a 3.4M cyber talent gap raise sourcing and ops risk; proactive regulator engagement shortens remediations.

| Metric | Value |

|---|---|

| Clients | ~9,000 |

| Community banks | ~3,300 (2024) |

| FY2024 revenue | $1.6B |

| Cyber workforce gap | 3.4M (ISC2 2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Jack Henry across Political, Economic, Social, Technological, Environmental and Legal dimensions. Each section offers data-backed trends, forward-looking insights and actionable subpoints to help executives, investors and consultants identify risks, opportunities and strategic responses.

A clean, summarized and visually segmented Jack Henry PESTLE that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and action priorities.

Economic factors

Interest rate cycles and bank profitability

Rising policy rates (fed funds 5.25–5.50% in 2023–24) lifted bank net interest margins to roughly 3.4–3.6% (FDIC/2023), which boosted IT budgets and drove core upgrades plus digital add‑ons; when margins compress, deals stall and buyers favor lower‑cost modules; flexible pricing and clear ROI metrics have preserved bookings and shortened sales cycles.

Credit cycle and bank health

Credit stress raises operational-risk priorities at Jack Henry, driving demand for risk, fraud, and collections tools while healthy credit cycles enable broader platform migrations; Jack Henry serves over 9,000 financial institutions, and recurring maintenance/subscription revenues—a majority of its business—help stabilize cash flows amid cyclical credit pressures.

Consolidation among FIs

M&A among financial institutions reduces the number of buying centers but creates large platform-replacement opportunities as combined banks rationalize core systems.

Retention after deals hinges on conversion support and migration ease, with vendors that minimize downtime and data friction retaining more clients.

Winning the combined entity expands ARR and cross-sell services, and strong implementation capacity—proven during 2023–2024 wave of bank consolidation—is a clear differentiator.

SMB and consumer spending trends

Payments volume for Jack Henry tracks merchant and consumer activity: U.S. consumer spending rose 2.6% in 2024 (BEA), lifting transaction volumes, while SMB card volume softened ~1.2% in H1 2025 (payment network data), which dampens fee revenue; rebounds reverse this effect. Diversifying rails and value-added services reduces volatility, and data-driven insights enable targeted upsells into faster-growing sectors.

- Payments sensitivity: consumer +2.6% (2024, BEA)

- SMB pressure: -1.2% H1 2025 (payment networks)

- Mitigation: multiple rails + VAS

- Opportunity: data-led upsell into growth segments

Inflation and cost structure

Rising labor, cloud and third-party software costs have pressured Jack Henry margins, with fintech cloud spend across banks up roughly 15% year-over-year into 2024, pushing service delivery costs higher.

Index-linked client contracts and targeted efficiency gains (automation, standardized implementations) helped offset inflationary pressure in 2024, preserving recurring revenue predictability.

Automation and standardized implementations reduce delivery expense and time-to-value, while transparent, value-based pricing supports client retention and upsell.

- Labor pressure: wage inflation in tech sectors up mid-single digits (2024)

- Cloud spend: ~15% YoY rise (industry, 2023–24)

- Offset tools: index-linked contracts, automation, standardization

- Retention: transparent pricing improves renewal rates

Regulatory push forces core banking vendor to shore up 9,000 clients, $1.6B

Higher policy rates (fed funds 5.25–5.50% 2023–24) raised bank NIMs to ~3.4–3.6% (FDIC), boosting IT spend and core upgrades, while NIM compression slows deals; Jack Henry serves >9,000 FIs, with recurring revenues stabilizing cash flow. Credit stress increases demand for risk/fraud tools; M&A reduces buyers but creates platform-replacement opportunities. Payments/activity: consumer spend +2.6% (2024), SMB card -1.2% H1 2025; cloud spend +15% YoY raising delivery costs.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | IT budgets ↑/↓ deals |

| NIM | 3.4–3.6% | Vendor demand |

| FIs served | >9,000 | Stable ARR |

| Consumer spend | +2.6% (2024) | Txn vol ↑ |

| SMB card | -1.2% H1 2025 | Fee pressure |

| Cloud spend | +15% YoY | Margins ↓ |

What You See Is What You Get

Jack Henry PESTLE Analysis

The preview shown here is the exact Jack Henry PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors with actionable insights and clear structure for strategic planning. No placeholders or teasers—this is the final file available for instant download.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE analysis of Jack Henry. Explore political, economic, social, technological, legal, and environmental trends shaping its strategy and risk profile. Purchase the full, downloadable report for actionable insights and ready-to-use slides and spreadsheets.

Political factors

Regulatory oversight of banking tech

Supervision by banking regulators shapes Jack Henry product standards, certifications, and audit readiness, and in 2024 regulators emphasized third-party risk and payments resilience. Jack Henry must align roadmaps for core, digital, and payments to those supervisory priorities to protect its more than 9,000 client institutions. Policy shifts can accelerate or delay client upgrades, impacting deployment timelines and revenue recognition. Proactive engagement with regulators de-risks rollouts and shortens remediation cycles.

Government cybersecurity initiatives

National cyber directives and funding—backed by SEC incident rules in 2024 and growing CISA resources—push stronger controls across financial infrastructure, raising baseline expectations for vendors and clients. IBM 2024 reports average breach costs around $4.45M (financials ~$5–6M), so compliance raises costs but bolsters trust and sales. Participation in FS-ISAC and public–private intel sharing (7,000+ members) improves resilience.

Public sector payments and RTP policy

Government support for instant payments, including the Federal Reserve's FedNow launched July 2023, accelerates institutional adoption timelines. Community institutions increasingly rely on vendors for compliance and connectivity, seeking turnkey RTP integrations. Jack Henry, which serves over 9,000 financial institutions, can convert RTP enablement into competitive wins. Clear policy reduces integration uncertainty and shortens time-to-market.

Rural and community banking policy support

Geopolitical supply chain and talent

Global tensions strain hardware sourcing, cloud capacity and security talent — the ISC2 2023 global cybersecurity workforce gap was about 3.4 million, limiting hires. US/EC export controls since 2022 constrain some partnerships and advanced tools. Jack Henry and peers mitigate via diversified vendors and nearshoring; continuity planning preserves institutional service levels.

- 3.4M cybersecurity workforce gap (ISC2 2023)

- Export controls (post-2022) limit some tech partnerships

- Diversified vendors + nearshoring reduce supply risk

- Continuity plans protect service SLAs

Regulatory push forces core banking vendor to shore up 9,000 clients, $1.6B

Regulatory focus on third-party risk, payments resilience and cyber rules (SEC/CISA 2024) forces Jack Henry to align roadmaps to protect 9,000 clients and $1.6B FY2024 revenue. FedNow and instant-pay policy accelerate RTP demand among ~3,300 community banks. Export controls and a 3.4M cyber talent gap raise sourcing and ops risk; proactive regulator engagement shortens remediations.

| Metric | Value |

|---|---|

| Clients | ~9,000 |

| Community banks | ~3,300 (2024) |

| FY2024 revenue | $1.6B |

| Cyber workforce gap | 3.4M (ISC2 2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Jack Henry across Political, Economic, Social, Technological, Environmental and Legal dimensions. Each section offers data-backed trends, forward-looking insights and actionable subpoints to help executives, investors and consultants identify risks, opportunities and strategic responses.

A clean, summarized and visually segmented Jack Henry PESTLE that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and action priorities.

Economic factors

Interest rate cycles and bank profitability

Rising policy rates (fed funds 5.25–5.50% in 2023–24) lifted bank net interest margins to roughly 3.4–3.6% (FDIC/2023), which boosted IT budgets and drove core upgrades plus digital add‑ons; when margins compress, deals stall and buyers favor lower‑cost modules; flexible pricing and clear ROI metrics have preserved bookings and shortened sales cycles.

Credit cycle and bank health

Credit stress raises operational-risk priorities at Jack Henry, driving demand for risk, fraud, and collections tools while healthy credit cycles enable broader platform migrations; Jack Henry serves over 9,000 financial institutions, and recurring maintenance/subscription revenues—a majority of its business—help stabilize cash flows amid cyclical credit pressures.

Consolidation among FIs

M&A among financial institutions reduces the number of buying centers but creates large platform-replacement opportunities as combined banks rationalize core systems.

Retention after deals hinges on conversion support and migration ease, with vendors that minimize downtime and data friction retaining more clients.

Winning the combined entity expands ARR and cross-sell services, and strong implementation capacity—proven during 2023–2024 wave of bank consolidation—is a clear differentiator.

SMB and consumer spending trends

Payments volume for Jack Henry tracks merchant and consumer activity: U.S. consumer spending rose 2.6% in 2024 (BEA), lifting transaction volumes, while SMB card volume softened ~1.2% in H1 2025 (payment network data), which dampens fee revenue; rebounds reverse this effect. Diversifying rails and value-added services reduces volatility, and data-driven insights enable targeted upsells into faster-growing sectors.

- Payments sensitivity: consumer +2.6% (2024, BEA)

- SMB pressure: -1.2% H1 2025 (payment networks)

- Mitigation: multiple rails + VAS

- Opportunity: data-led upsell into growth segments

Inflation and cost structure

Rising labor, cloud and third-party software costs have pressured Jack Henry margins, with fintech cloud spend across banks up roughly 15% year-over-year into 2024, pushing service delivery costs higher.

Index-linked client contracts and targeted efficiency gains (automation, standardized implementations) helped offset inflationary pressure in 2024, preserving recurring revenue predictability.

Automation and standardized implementations reduce delivery expense and time-to-value, while transparent, value-based pricing supports client retention and upsell.

- Labor pressure: wage inflation in tech sectors up mid-single digits (2024)

- Cloud spend: ~15% YoY rise (industry, 2023–24)

- Offset tools: index-linked contracts, automation, standardization

- Retention: transparent pricing improves renewal rates

Regulatory push forces core banking vendor to shore up 9,000 clients, $1.6B

Higher policy rates (fed funds 5.25–5.50% 2023–24) raised bank NIMs to ~3.4–3.6% (FDIC), boosting IT spend and core upgrades, while NIM compression slows deals; Jack Henry serves >9,000 FIs, with recurring revenues stabilizing cash flow. Credit stress increases demand for risk/fraud tools; M&A reduces buyers but creates platform-replacement opportunities. Payments/activity: consumer spend +2.6% (2024), SMB card -1.2% H1 2025; cloud spend +15% YoY raising delivery costs.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | IT budgets ↑/↓ deals |

| NIM | 3.4–3.6% | Vendor demand |

| FIs served | >9,000 | Stable ARR |

| Consumer spend | +2.6% (2024) | Txn vol ↑ |

| SMB card | -1.2% H1 2025 | Fee pressure |

| Cloud spend | +15% YoY | Margins ↓ |

What You See Is What You Get

Jack Henry PESTLE Analysis

The preview shown here is the exact Jack Henry PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors with actionable insights and clear structure for strategic planning. No placeholders or teasers—this is the final file available for instant download.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE analysis of Jack Henry. Explore political, economic, social, technological, legal, and environmental trends shaping its strategy and risk profile. Purchase the full, downloadable report for actionable insights and ready-to-use slides and spreadsheets.

Political factors

Regulatory oversight of banking tech

Supervision by banking regulators shapes Jack Henry product standards, certifications, and audit readiness, and in 2024 regulators emphasized third-party risk and payments resilience. Jack Henry must align roadmaps for core, digital, and payments to those supervisory priorities to protect its more than 9,000 client institutions. Policy shifts can accelerate or delay client upgrades, impacting deployment timelines and revenue recognition. Proactive engagement with regulators de-risks rollouts and shortens remediation cycles.

Government cybersecurity initiatives

National cyber directives and funding—backed by SEC incident rules in 2024 and growing CISA resources—push stronger controls across financial infrastructure, raising baseline expectations for vendors and clients. IBM 2024 reports average breach costs around $4.45M (financials ~$5–6M), so compliance raises costs but bolsters trust and sales. Participation in FS-ISAC and public–private intel sharing (7,000+ members) improves resilience.

Public sector payments and RTP policy

Government support for instant payments, including the Federal Reserve's FedNow launched July 2023, accelerates institutional adoption timelines. Community institutions increasingly rely on vendors for compliance and connectivity, seeking turnkey RTP integrations. Jack Henry, which serves over 9,000 financial institutions, can convert RTP enablement into competitive wins. Clear policy reduces integration uncertainty and shortens time-to-market.

Rural and community banking policy support

Geopolitical supply chain and talent

Global tensions strain hardware sourcing, cloud capacity and security talent — the ISC2 2023 global cybersecurity workforce gap was about 3.4 million, limiting hires. US/EC export controls since 2022 constrain some partnerships and advanced tools. Jack Henry and peers mitigate via diversified vendors and nearshoring; continuity planning preserves institutional service levels.

- 3.4M cybersecurity workforce gap (ISC2 2023)

- Export controls (post-2022) limit some tech partnerships

- Diversified vendors + nearshoring reduce supply risk

- Continuity plans protect service SLAs

Regulatory push forces core banking vendor to shore up 9,000 clients, $1.6B

Regulatory focus on third-party risk, payments resilience and cyber rules (SEC/CISA 2024) forces Jack Henry to align roadmaps to protect 9,000 clients and $1.6B FY2024 revenue. FedNow and instant-pay policy accelerate RTP demand among ~3,300 community banks. Export controls and a 3.4M cyber talent gap raise sourcing and ops risk; proactive regulator engagement shortens remediations.

| Metric | Value |

|---|---|

| Clients | ~9,000 |

| Community banks | ~3,300 (2024) |

| FY2024 revenue | $1.6B |

| Cyber workforce gap | 3.4M (ISC2 2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Jack Henry across Political, Economic, Social, Technological, Environmental and Legal dimensions. Each section offers data-backed trends, forward-looking insights and actionable subpoints to help executives, investors and consultants identify risks, opportunities and strategic responses.

A clean, summarized and visually segmented Jack Henry PESTLE that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and action priorities.

Economic factors

Interest rate cycles and bank profitability

Rising policy rates (fed funds 5.25–5.50% in 2023–24) lifted bank net interest margins to roughly 3.4–3.6% (FDIC/2023), which boosted IT budgets and drove core upgrades plus digital add‑ons; when margins compress, deals stall and buyers favor lower‑cost modules; flexible pricing and clear ROI metrics have preserved bookings and shortened sales cycles.

Credit cycle and bank health

Credit stress raises operational-risk priorities at Jack Henry, driving demand for risk, fraud, and collections tools while healthy credit cycles enable broader platform migrations; Jack Henry serves over 9,000 financial institutions, and recurring maintenance/subscription revenues—a majority of its business—help stabilize cash flows amid cyclical credit pressures.

Consolidation among FIs

M&A among financial institutions reduces the number of buying centers but creates large platform-replacement opportunities as combined banks rationalize core systems.

Retention after deals hinges on conversion support and migration ease, with vendors that minimize downtime and data friction retaining more clients.

Winning the combined entity expands ARR and cross-sell services, and strong implementation capacity—proven during 2023–2024 wave of bank consolidation—is a clear differentiator.

SMB and consumer spending trends

Payments volume for Jack Henry tracks merchant and consumer activity: U.S. consumer spending rose 2.6% in 2024 (BEA), lifting transaction volumes, while SMB card volume softened ~1.2% in H1 2025 (payment network data), which dampens fee revenue; rebounds reverse this effect. Diversifying rails and value-added services reduces volatility, and data-driven insights enable targeted upsells into faster-growing sectors.

- Payments sensitivity: consumer +2.6% (2024, BEA)

- SMB pressure: -1.2% H1 2025 (payment networks)

- Mitigation: multiple rails + VAS

- Opportunity: data-led upsell into growth segments

Inflation and cost structure

Rising labor, cloud and third-party software costs have pressured Jack Henry margins, with fintech cloud spend across banks up roughly 15% year-over-year into 2024, pushing service delivery costs higher.

Index-linked client contracts and targeted efficiency gains (automation, standardized implementations) helped offset inflationary pressure in 2024, preserving recurring revenue predictability.

Automation and standardized implementations reduce delivery expense and time-to-value, while transparent, value-based pricing supports client retention and upsell.

- Labor pressure: wage inflation in tech sectors up mid-single digits (2024)

- Cloud spend: ~15% YoY rise (industry, 2023–24)

- Offset tools: index-linked contracts, automation, standardization

- Retention: transparent pricing improves renewal rates

Regulatory push forces core banking vendor to shore up 9,000 clients, $1.6B

Higher policy rates (fed funds 5.25–5.50% 2023–24) raised bank NIMs to ~3.4–3.6% (FDIC), boosting IT spend and core upgrades, while NIM compression slows deals; Jack Henry serves >9,000 FIs, with recurring revenues stabilizing cash flow. Credit stress increases demand for risk/fraud tools; M&A reduces buyers but creates platform-replacement opportunities. Payments/activity: consumer spend +2.6% (2024), SMB card -1.2% H1 2025; cloud spend +15% YoY raising delivery costs.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | IT budgets ↑/↓ deals |

| NIM | 3.4–3.6% | Vendor demand |

| FIs served | >9,000 | Stable ARR |

| Consumer spend | +2.6% (2024) | Txn vol ↑ |

| SMB card | -1.2% H1 2025 | Fee pressure |

| Cloud spend | +15% YoY | Margins ↓ |

What You See Is What You Get

Jack Henry PESTLE Analysis

The preview shown here is the exact Jack Henry PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors with actionable insights and clear structure for strategic planning. No placeholders or teasers—this is the final file available for instant download.