Jackson Financial Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

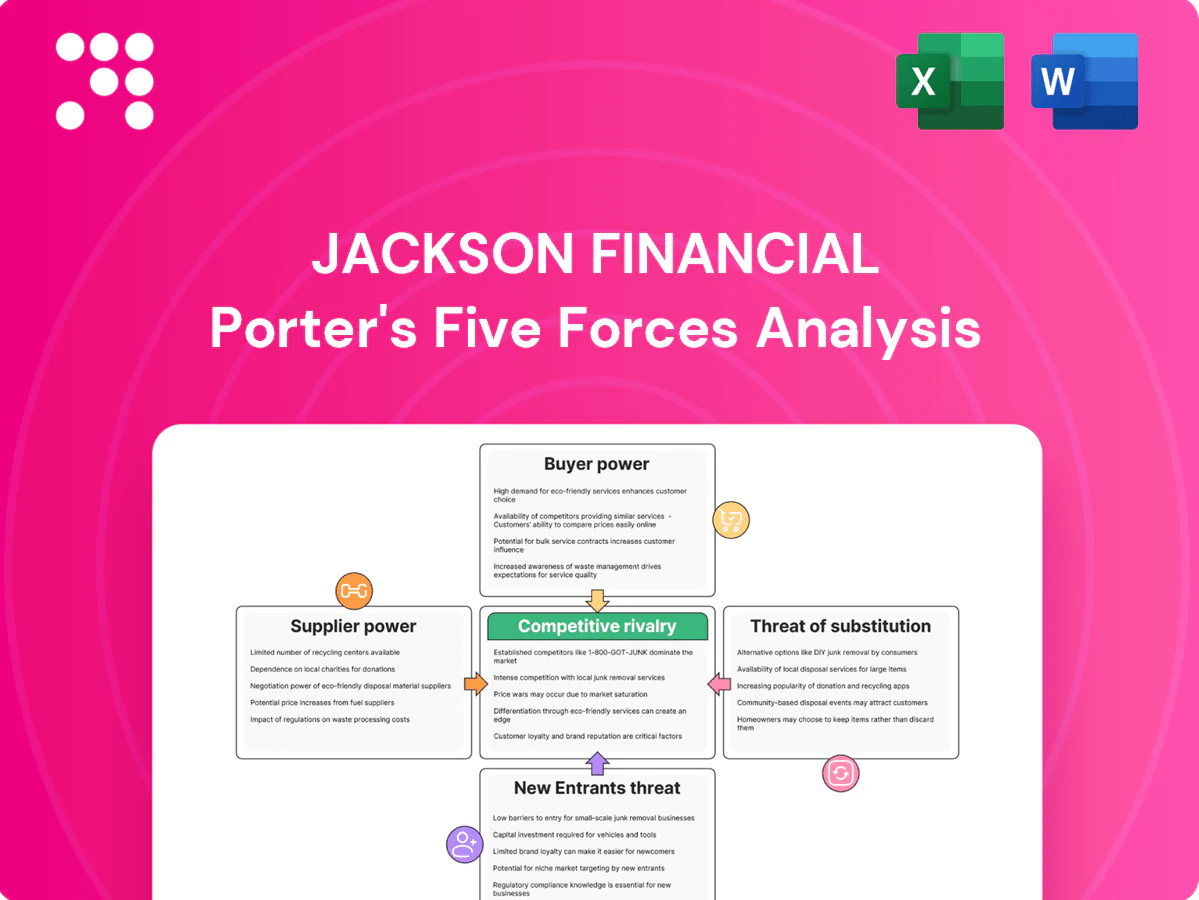

Jackson Financial faces moderate buyer power, concentrated regulatory risks, and persistent threat of substitutes as digital platforms reshape wealth management; supplier influence and capital requirements further define competitive boundaries. This snapshot highlights strategic pressure points and resilience factors for Jackson Financial. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurer capacity sets economics

Jackson relies heavily on external reinsurers to manage capital strain and guarantee risk on variable and fixed index annuities, so tightened reinsurance capacity or hardened pricing directly compresses product features and margins. Concentration among a few large global reinsurers raises their leverage in negotiations. Diversifying panels and using retrocession can temper but not eliminate this supplier power.

Asset managers drive subaccount value

Variable annuities rely on third-party asset managers for competitive subaccount lineups and volatility-control indices; large managers like BlackRock (>$10 trillion AUM) and Vanguard (>$7 trillion AUM) can command platform fees or revenue-share terms that materially affect Jackson’s cost structure. Performance dispersion drives flows to top managers, increasing their bargaining leverage. Co-developed indices reduce dependence but demand ongoing licensing, data and governance support.

Derivatives counterparties enable hedging

FIAs and VAs with living benefits rely on swaps and options markets for hedging guarantees, and Jackson’s hedge costs and capacity are sensitive to dealer concentration, margin rules and collateral terms; top five global dealers account for roughly three quarters of dealer intermediation in OTC markets. In stress, spread widening and tighter counterparty limits raise supplier power and funding costs, as seen in past volatility spikes. Multi‑dealer programs and cleared structures mitigate but do not eliminate exposure.

Ratings agencies influence distribution

Ratings agencies influence advisor placement and distributor shelf access because financial-strength ratings steer wholesaler support and broker-dealer approvals; methodology changes or outlook revisions can force repricing, reserve boosts or capital adjustments, giving agencies indirect bargaining power over product strategy and mix; maintaining strong capital metrics and liquidity is essential to limit ratings-driven distribution constraints.

- Impact on distribution: advisor placement, shelf access

- Mechanism: methodology shifts force pricing/capital moves

- Power: indirect influence on strategy and product mix

- Mitigation: strong capital and liquidity metrics

Core admin and data vendors matter

Core admin systems, illustration tools and data integrations underpin advisor experience and compliance; in 2024 over 60% of insurers ranked policy admin modernization as a top priority, amplifying vendor influence. High switching costs and conversion risk—often tens of millions and many months of work—raise supplier bargaining power and can delay product launches or state filings. Building internal capabilities and modular architectures can gradually rebalance power.

- Policy admin systems: primary dependency

- Illustration tools: compliance and sales impact

- Switching costs: tens of millions, months of migration

- Delays: slow filings and launches

- Mitigation: internal build, modular architecture

Insurer faces concentrated supplier power, high hedging costs and costly admin switching

Jackson faces high supplier power from concentrated reinsurers, large asset managers (BlackRock >$10T, Vanguard >$7T) and five dealers supplying ~75% of OTC intermediation, raising hedging and product costs. Ratings agencies and high admin-system switching costs (tens of millions) add indirect leverage. Diversification, retrocession, multi-dealer hedges and modular tech reduce but do not remove pressure.

| Supplier | Metric | 2024/Fact |

|---|---|---|

| Asset managers | AUM | BlackRock >$10T; Vanguard >$7T |

| Dealers | OTC share | Top 5 ≈75% |

| Admin vendors | Priority | >60% insurers rank modernization top |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Jackson Financial, with detailed assessment of supplier and buyer power, substitutes, and rivalry. Highlights emerging disruptors and defensive barriers to protect market share, ideal for investor materials or strategic planning.

A concise one-sheet Porter's Five Forces for Jackson Financial—visualize competitive pressure instantly with an editable radar chart and clean, copy-ready layout for decks; no macros and easy to update for regulatory or market shifts.

Customers Bargaining Power

Advisor‑led distribution wields influence

Independent advisors, IMOs and broker‑dealers drive placement and can reallocate flow rapidly, with the top 10 distributors capturing roughly 60% of shelf space in 2024, concentrating bargaining power.

They routinely negotiate commissions, marketing support and product features, pressuring manufacturers on pricing and design to win preferred‑list status.

Jackson must invest in robust wholesaling and advisor education—data from 2024 show recommendation likelihood rises markedly with dedicated wholesaler coverage and CE programs.

Price sensitivity to fees and rates

Clients and advisors in 2024 compare M&E fees (industry average about 1.00%), rider charges (commonly 0.25–1.00%), caps, spreads and roll‑up rates across peers, so small pricing deltas can redirect sales in commoditized segments. Transparent illustrations amplify price competition and disclosure; loyalty is limited when guarantees and rider economics are similar. Jackson faces heightened churn risk as buyers chase marginally better net yields.

Product comparability lowers switching costs

Many VA and FIA features remain standardized, enabling apples‑to‑apples comparisons and easing replacement activity and tax‑deferred 1035 exchanges under IRC Section 1035 (2024). This comparability lowers switching costs and raises buyer leverage. Clients increasingly treat fast underwriting, clean paperwork, and digital servicing as tie‑breakers. Clear product differentiation is required to resist churn.

Regulatory standards empower buyers

Best interest and Reg BI/suitability rules (Reg BI effective June 30, 2020) push firms toward lower costs and clearer value, while distributors in 2024 increasingly scrutinize conflicts, compensation and product complexity, strengthening buyers' negotiating stance on fees and features.

Robust disclosures and digital tools are now required to support and document recommendations, raising transparency and allowing clients to demand fee reductions or enhanced service terms.

- Reg BI effective June 30, 2020

- 2024: heightened distributor scrutiny on conflicts

- Buyers leverage transparency to negotiate fees/features

- Required: robust disclosures and recommendation tools

Institutional distributors negotiate hard

Large broker‑dealers and banks can mandate pricing, feature changes and SLAs, and often require data feeds, supervision support and training; concentration in 2024 — top 10 broker‑dealers control roughly 60% of U.S. brokerage assets — increases their leverage over Jackson’s terms, while diversifying channels helps offset this power.

- Mandate pricing & SLAs

- Require feeds, supervision, training

- Top‑10 concentration ~60% (2024)

- Channel diversification reduces leverage

Top 10 ≈60% shelf; advisor fee leverage drives churn — carrier must invest in wholesaling & digital

Distribution concentration (top 10 ≈60% shelf share) and active advisor negotiation in 2024 give customers strong leverage on fees, riders and product features; small pricing or guarantee deltas drive churn. Jackson must invest in wholesaling, CE and digital servicing to retain placement and justify premium pricing under Reg BI scrutiny.

| Metric | 2024 |

|---|---|

| Top‑10 distributor shelf share | ≈60% |

| Industry M&E avg | ≈1.00% |

| Common rider charges | 0.25–1.00% |

| Top‑10 brokerage assets | ≈60% |

What You See Is What You Get

Jackson Financial Porter's Five Forces Analysis

This preview shows the exact Jackson Financial Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted strategic assessment covering competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and actionable implications. It's ready for instant download and immediate use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Jackson Financial faces moderate buyer power, concentrated regulatory risks, and persistent threat of substitutes as digital platforms reshape wealth management; supplier influence and capital requirements further define competitive boundaries. This snapshot highlights strategic pressure points and resilience factors for Jackson Financial. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurer capacity sets economics

Jackson relies heavily on external reinsurers to manage capital strain and guarantee risk on variable and fixed index annuities, so tightened reinsurance capacity or hardened pricing directly compresses product features and margins. Concentration among a few large global reinsurers raises their leverage in negotiations. Diversifying panels and using retrocession can temper but not eliminate this supplier power.

Asset managers drive subaccount value

Variable annuities rely on third-party asset managers for competitive subaccount lineups and volatility-control indices; large managers like BlackRock (>$10 trillion AUM) and Vanguard (>$7 trillion AUM) can command platform fees or revenue-share terms that materially affect Jackson’s cost structure. Performance dispersion drives flows to top managers, increasing their bargaining leverage. Co-developed indices reduce dependence but demand ongoing licensing, data and governance support.

Derivatives counterparties enable hedging

FIAs and VAs with living benefits rely on swaps and options markets for hedging guarantees, and Jackson’s hedge costs and capacity are sensitive to dealer concentration, margin rules and collateral terms; top five global dealers account for roughly three quarters of dealer intermediation in OTC markets. In stress, spread widening and tighter counterparty limits raise supplier power and funding costs, as seen in past volatility spikes. Multi‑dealer programs and cleared structures mitigate but do not eliminate exposure.

Ratings agencies influence distribution

Ratings agencies influence advisor placement and distributor shelf access because financial-strength ratings steer wholesaler support and broker-dealer approvals; methodology changes or outlook revisions can force repricing, reserve boosts or capital adjustments, giving agencies indirect bargaining power over product strategy and mix; maintaining strong capital metrics and liquidity is essential to limit ratings-driven distribution constraints.

- Impact on distribution: advisor placement, shelf access

- Mechanism: methodology shifts force pricing/capital moves

- Power: indirect influence on strategy and product mix

- Mitigation: strong capital and liquidity metrics

Core admin and data vendors matter

Core admin systems, illustration tools and data integrations underpin advisor experience and compliance; in 2024 over 60% of insurers ranked policy admin modernization as a top priority, amplifying vendor influence. High switching costs and conversion risk—often tens of millions and many months of work—raise supplier bargaining power and can delay product launches or state filings. Building internal capabilities and modular architectures can gradually rebalance power.

- Policy admin systems: primary dependency

- Illustration tools: compliance and sales impact

- Switching costs: tens of millions, months of migration

- Delays: slow filings and launches

- Mitigation: internal build, modular architecture

Insurer faces concentrated supplier power, high hedging costs and costly admin switching

Jackson faces high supplier power from concentrated reinsurers, large asset managers (BlackRock >$10T, Vanguard >$7T) and five dealers supplying ~75% of OTC intermediation, raising hedging and product costs. Ratings agencies and high admin-system switching costs (tens of millions) add indirect leverage. Diversification, retrocession, multi-dealer hedges and modular tech reduce but do not remove pressure.

| Supplier | Metric | 2024/Fact |

|---|---|---|

| Asset managers | AUM | BlackRock >$10T; Vanguard >$7T |

| Dealers | OTC share | Top 5 ≈75% |

| Admin vendors | Priority | >60% insurers rank modernization top |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Jackson Financial, with detailed assessment of supplier and buyer power, substitutes, and rivalry. Highlights emerging disruptors and defensive barriers to protect market share, ideal for investor materials or strategic planning.

A concise one-sheet Porter's Five Forces for Jackson Financial—visualize competitive pressure instantly with an editable radar chart and clean, copy-ready layout for decks; no macros and easy to update for regulatory or market shifts.

Customers Bargaining Power

Advisor‑led distribution wields influence

Independent advisors, IMOs and broker‑dealers drive placement and can reallocate flow rapidly, with the top 10 distributors capturing roughly 60% of shelf space in 2024, concentrating bargaining power.

They routinely negotiate commissions, marketing support and product features, pressuring manufacturers on pricing and design to win preferred‑list status.

Jackson must invest in robust wholesaling and advisor education—data from 2024 show recommendation likelihood rises markedly with dedicated wholesaler coverage and CE programs.

Price sensitivity to fees and rates

Clients and advisors in 2024 compare M&E fees (industry average about 1.00%), rider charges (commonly 0.25–1.00%), caps, spreads and roll‑up rates across peers, so small pricing deltas can redirect sales in commoditized segments. Transparent illustrations amplify price competition and disclosure; loyalty is limited when guarantees and rider economics are similar. Jackson faces heightened churn risk as buyers chase marginally better net yields.

Product comparability lowers switching costs

Many VA and FIA features remain standardized, enabling apples‑to‑apples comparisons and easing replacement activity and tax‑deferred 1035 exchanges under IRC Section 1035 (2024). This comparability lowers switching costs and raises buyer leverage. Clients increasingly treat fast underwriting, clean paperwork, and digital servicing as tie‑breakers. Clear product differentiation is required to resist churn.

Regulatory standards empower buyers

Best interest and Reg BI/suitability rules (Reg BI effective June 30, 2020) push firms toward lower costs and clearer value, while distributors in 2024 increasingly scrutinize conflicts, compensation and product complexity, strengthening buyers' negotiating stance on fees and features.

Robust disclosures and digital tools are now required to support and document recommendations, raising transparency and allowing clients to demand fee reductions or enhanced service terms.

- Reg BI effective June 30, 2020

- 2024: heightened distributor scrutiny on conflicts

- Buyers leverage transparency to negotiate fees/features

- Required: robust disclosures and recommendation tools

Institutional distributors negotiate hard

Large broker‑dealers and banks can mandate pricing, feature changes and SLAs, and often require data feeds, supervision support and training; concentration in 2024 — top 10 broker‑dealers control roughly 60% of U.S. brokerage assets — increases their leverage over Jackson’s terms, while diversifying channels helps offset this power.

- Mandate pricing & SLAs

- Require feeds, supervision, training

- Top‑10 concentration ~60% (2024)

- Channel diversification reduces leverage

Top 10 ≈60% shelf; advisor fee leverage drives churn — carrier must invest in wholesaling & digital

Distribution concentration (top 10 ≈60% shelf share) and active advisor negotiation in 2024 give customers strong leverage on fees, riders and product features; small pricing or guarantee deltas drive churn. Jackson must invest in wholesaling, CE and digital servicing to retain placement and justify premium pricing under Reg BI scrutiny.

| Metric | 2024 |

|---|---|

| Top‑10 distributor shelf share | ≈60% |

| Industry M&E avg | ≈1.00% |

| Common rider charges | 0.25–1.00% |

| Top‑10 brokerage assets | ≈60% |

What You See Is What You Get

Jackson Financial Porter's Five Forces Analysis

This preview shows the exact Jackson Financial Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted strategic assessment covering competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and actionable implications. It's ready for instant download and immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Jackson Financial faces moderate buyer power, concentrated regulatory risks, and persistent threat of substitutes as digital platforms reshape wealth management; supplier influence and capital requirements further define competitive boundaries. This snapshot highlights strategic pressure points and resilience factors for Jackson Financial. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurer capacity sets economics

Jackson relies heavily on external reinsurers to manage capital strain and guarantee risk on variable and fixed index annuities, so tightened reinsurance capacity or hardened pricing directly compresses product features and margins. Concentration among a few large global reinsurers raises their leverage in negotiations. Diversifying panels and using retrocession can temper but not eliminate this supplier power.

Asset managers drive subaccount value

Variable annuities rely on third-party asset managers for competitive subaccount lineups and volatility-control indices; large managers like BlackRock (>$10 trillion AUM) and Vanguard (>$7 trillion AUM) can command platform fees or revenue-share terms that materially affect Jackson’s cost structure. Performance dispersion drives flows to top managers, increasing their bargaining leverage. Co-developed indices reduce dependence but demand ongoing licensing, data and governance support.

Derivatives counterparties enable hedging

FIAs and VAs with living benefits rely on swaps and options markets for hedging guarantees, and Jackson’s hedge costs and capacity are sensitive to dealer concentration, margin rules and collateral terms; top five global dealers account for roughly three quarters of dealer intermediation in OTC markets. In stress, spread widening and tighter counterparty limits raise supplier power and funding costs, as seen in past volatility spikes. Multi‑dealer programs and cleared structures mitigate but do not eliminate exposure.

Ratings agencies influence distribution

Ratings agencies influence advisor placement and distributor shelf access because financial-strength ratings steer wholesaler support and broker-dealer approvals; methodology changes or outlook revisions can force repricing, reserve boosts or capital adjustments, giving agencies indirect bargaining power over product strategy and mix; maintaining strong capital metrics and liquidity is essential to limit ratings-driven distribution constraints.

- Impact on distribution: advisor placement, shelf access

- Mechanism: methodology shifts force pricing/capital moves

- Power: indirect influence on strategy and product mix

- Mitigation: strong capital and liquidity metrics

Core admin and data vendors matter

Core admin systems, illustration tools and data integrations underpin advisor experience and compliance; in 2024 over 60% of insurers ranked policy admin modernization as a top priority, amplifying vendor influence. High switching costs and conversion risk—often tens of millions and many months of work—raise supplier bargaining power and can delay product launches or state filings. Building internal capabilities and modular architectures can gradually rebalance power.

- Policy admin systems: primary dependency

- Illustration tools: compliance and sales impact

- Switching costs: tens of millions, months of migration

- Delays: slow filings and launches

- Mitigation: internal build, modular architecture

Insurer faces concentrated supplier power, high hedging costs and costly admin switching

Jackson faces high supplier power from concentrated reinsurers, large asset managers (BlackRock >$10T, Vanguard >$7T) and five dealers supplying ~75% of OTC intermediation, raising hedging and product costs. Ratings agencies and high admin-system switching costs (tens of millions) add indirect leverage. Diversification, retrocession, multi-dealer hedges and modular tech reduce but do not remove pressure.

| Supplier | Metric | 2024/Fact |

|---|---|---|

| Asset managers | AUM | BlackRock >$10T; Vanguard >$7T |

| Dealers | OTC share | Top 5 ≈75% |

| Admin vendors | Priority | >60% insurers rank modernization top |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Jackson Financial, with detailed assessment of supplier and buyer power, substitutes, and rivalry. Highlights emerging disruptors and defensive barriers to protect market share, ideal for investor materials or strategic planning.

A concise one-sheet Porter's Five Forces for Jackson Financial—visualize competitive pressure instantly with an editable radar chart and clean, copy-ready layout for decks; no macros and easy to update for regulatory or market shifts.

Customers Bargaining Power

Advisor‑led distribution wields influence

Independent advisors, IMOs and broker‑dealers drive placement and can reallocate flow rapidly, with the top 10 distributors capturing roughly 60% of shelf space in 2024, concentrating bargaining power.

They routinely negotiate commissions, marketing support and product features, pressuring manufacturers on pricing and design to win preferred‑list status.

Jackson must invest in robust wholesaling and advisor education—data from 2024 show recommendation likelihood rises markedly with dedicated wholesaler coverage and CE programs.

Price sensitivity to fees and rates

Clients and advisors in 2024 compare M&E fees (industry average about 1.00%), rider charges (commonly 0.25–1.00%), caps, spreads and roll‑up rates across peers, so small pricing deltas can redirect sales in commoditized segments. Transparent illustrations amplify price competition and disclosure; loyalty is limited when guarantees and rider economics are similar. Jackson faces heightened churn risk as buyers chase marginally better net yields.

Product comparability lowers switching costs

Many VA and FIA features remain standardized, enabling apples‑to‑apples comparisons and easing replacement activity and tax‑deferred 1035 exchanges under IRC Section 1035 (2024). This comparability lowers switching costs and raises buyer leverage. Clients increasingly treat fast underwriting, clean paperwork, and digital servicing as tie‑breakers. Clear product differentiation is required to resist churn.

Regulatory standards empower buyers

Best interest and Reg BI/suitability rules (Reg BI effective June 30, 2020) push firms toward lower costs and clearer value, while distributors in 2024 increasingly scrutinize conflicts, compensation and product complexity, strengthening buyers' negotiating stance on fees and features.

Robust disclosures and digital tools are now required to support and document recommendations, raising transparency and allowing clients to demand fee reductions or enhanced service terms.

- Reg BI effective June 30, 2020

- 2024: heightened distributor scrutiny on conflicts

- Buyers leverage transparency to negotiate fees/features

- Required: robust disclosures and recommendation tools

Institutional distributors negotiate hard

Large broker‑dealers and banks can mandate pricing, feature changes and SLAs, and often require data feeds, supervision support and training; concentration in 2024 — top 10 broker‑dealers control roughly 60% of U.S. brokerage assets — increases their leverage over Jackson’s terms, while diversifying channels helps offset this power.

- Mandate pricing & SLAs

- Require feeds, supervision, training

- Top‑10 concentration ~60% (2024)

- Channel diversification reduces leverage

Top 10 ≈60% shelf; advisor fee leverage drives churn — carrier must invest in wholesaling & digital

Distribution concentration (top 10 ≈60% shelf share) and active advisor negotiation in 2024 give customers strong leverage on fees, riders and product features; small pricing or guarantee deltas drive churn. Jackson must invest in wholesaling, CE and digital servicing to retain placement and justify premium pricing under Reg BI scrutiny.

| Metric | 2024 |

|---|---|

| Top‑10 distributor shelf share | ≈60% |

| Industry M&E avg | ≈1.00% |

| Common rider charges | 0.25–1.00% |

| Top‑10 brokerage assets | ≈60% |

What You See Is What You Get

Jackson Financial Porter's Five Forces Analysis

This preview shows the exact Jackson Financial Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted strategic assessment covering competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and actionable implications. It's ready for instant download and immediate use.