Jackson Financial SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Jackson Financial's SWOT snapshot highlights solid asset-management capabilities, demographic-driven growth opportunities, and regulatory and longevity-risk pressures. Want the full strategic picture and financial context? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to guide investment or strategic planning.

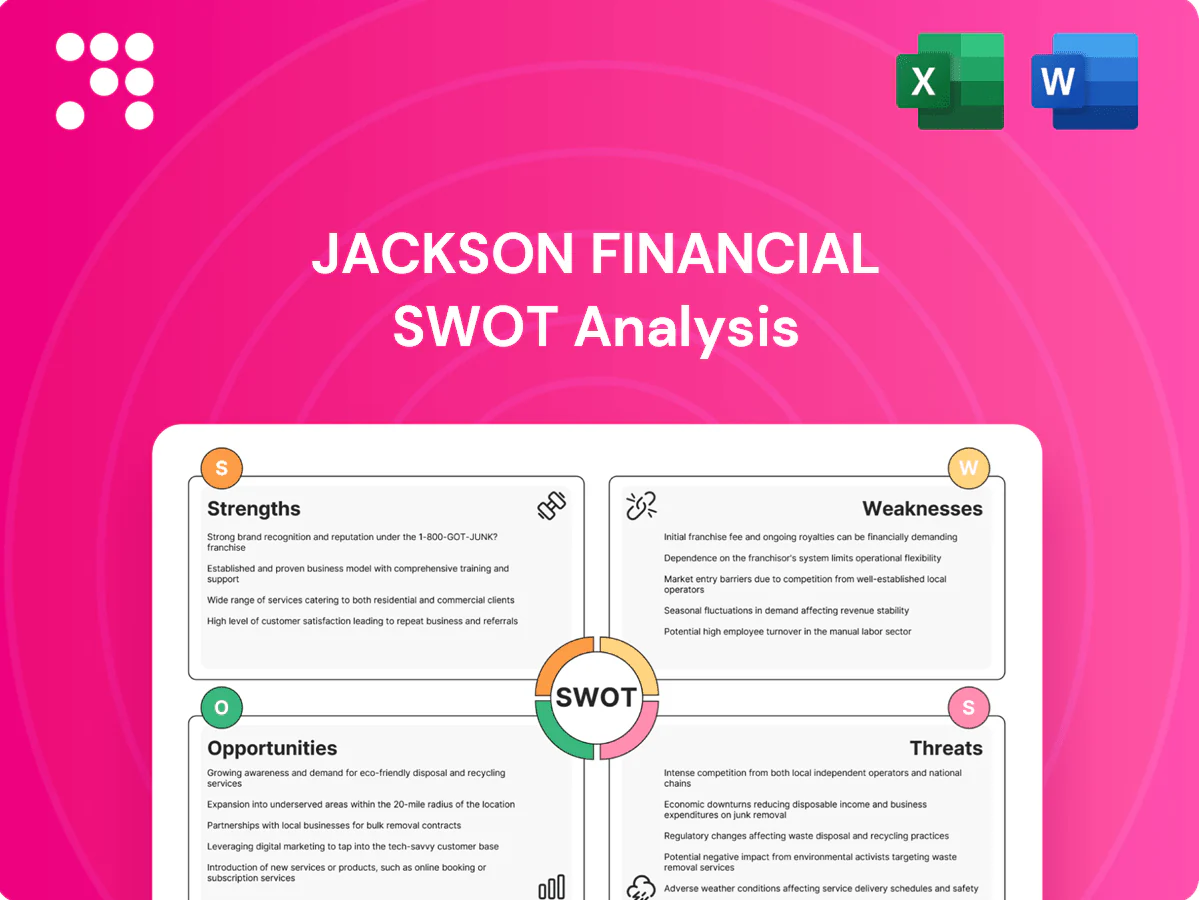

Strengths

Market-leading annuity franchise

Jackson's market-leading U.S. retail annuity franchise, with roughly 20% market share, about 2.6 million policyholders and approximately $320 billion of annuity account value as of year-end 2024, drives pricing power and scale economies. High brand recognition in retirement income boosts distributor confidence and client adoption, supporting resilient new business flows across cycles. Franchise leadership strengthens negotiating leverage with reinsurers and vendors, compressing costs and protecting margins.

Broad, diversified product suite

Offering variable, fixed and fixed index annuities plus life insurance lets Jackson tailor solutions to varied risk tolerances and income needs, supporting both accumulation and retirement income strategies. Its diversified suite helps balance sales across rate and equity cycles, stabilizing revenue and capital deployment. Cross-selling deepens client relationships and boosts persistency, while product mix flexibility enables margin optimization over time; Jackson manages over $200 billion in assets (2024).

Extensive distribution network

Relationships with independent advisors and broker-dealers give Jackson national reach, supporting distribution into diverse channels and contributing to roughly $318 billion in assets under management at year-end 2024. Distribution breadth reduces single-channel dependency and helped drive steady annuity inflows in 2024. Strong wholesaling and practice-support teams boost advisor productivity, creating a network that is costly and time-consuming for new entrants to replicate.

Risk management and ALM capabilities

Jackson Financial's established hedging programs and ALM frameworks mitigate market and interest-rate risk in annuity guarantees, supported by roughly $260 billion of invested assets as of 2024 and advanced derivative governance.

Prudent capital management sustaining ratings and product competitiveness enhances resilience, with stress-tested strategies reducing volatility exposure and preserving solvency.

- Hedging coverage: broad ALM + derivatives

- Scale: ~$260B invested assets (2024)

- Capital: rating-backed prudence

- Outcome: stronger volatility resilience

Focus on retirement mission and brand trust

Jackson Financials clear retirement-income mission and brand trust bolster credibility with advisors and clients; as a top U.S. annuity provider with over $200 billion in assets under management (2024), its service, education and planning tools foster long-term relationships and lower lapse risk, supporting premium pricing for guarantees and driving advisor word-of-mouth.

- Mission-led brand

- >$200B AUM (2024)

- Lower lapse risk

- Stronger advisory referrals

Market-leading U.S. annuity franchise: ~20% share, 2.6M policyholders, $320B AAV

Market-leading U.S. annuity franchise (~20% share) with ~2.6M policyholders and $320B annuity account value (YE 2024) delivers scale, pricing power and distributor trust. Diversified product suite and distribution (>$200B AUM) stabilizes flows across cycles. Robust ALM/hedging and ~$260B invested assets (2024) support guarantee risk management.

| Metric | 2024 |

|---|---|

| Annuity AAV | $320B |

| Policyholders | 2.6M |

| Invested assets | $260B |

| AUM | $200B+ |

What is included in the product

Delivers a strategic overview of Jackson Financial’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, and key risks shaping future performance.

Provides a focused SWOT snapshot of Jackson Financial to quickly identify risks and opportunities, easing strategic alignment, stakeholder updates, and rapid decision-making.

Weaknesses

Concentration in annuities

As of 2024 Jackson remains heavily concentrated in annuities, heightening exposure to regulatory shifts and market volatility tied to one product class. Limited expansion into fee-based asset management constrains earnings stability and recurring fee income. Product concentration can amplify capital strain under stress scenarios and narrows strategic optionality versus multi-line peers.

Sensitivity to market and rate volatility

Jackson’s variable annuities with guarantees link earnings to equity markets and volatility (VIX averaged about 17 in 2024), exposing results to market swings. Interest-rate moves — the 10-year Treasury near 4.5% in 2024 — affect spreads, reserve requirements and hedging costs. Prolonged low or rapidly shifting rates compress new-business economics and amplify earnings variability.

Complex products and perceived high fees

Annuities are complex products that slow sales and invite scrutiny; surrender periods commonly span 5–10 years and early surrender charges can exceed 7% in initial years, deterring cost‑sensitive advisors and clients. Complexity raises suitability and disclosure risks and increases servicing and compliance costs.

Dependence on third-party distributors

Dependence on independent advisors limits Jackson Financials direct control over the end-client experience, since a majority of retail annuity sales (>50%) pass through broker-dealers and RIAs, reducing brand influence and client retention. Shelf space and selling focus can shift quickly with competitor incentives, while margin sharing with intermediaries compresses economics versus direct channels and channel conflicts slow rapid product pivots.

- Majority channel: >50% via third parties

- Margin pressure: shared commissions reduce net yield

- Shelf risk: competitors can re-prioritize advisors

- Speed to market: channel conflicts hinder pivots

Capital- and hedge-intensive guarantees

Living benefit riders require significant capital and continuous hedging; with the Fed funds rate around 5.25–5.50% in 2024, funding and duration mismatches remain sensitive to rate moves. Elevated market volatility can sharply spike hedge costs and basis risk, while potential regulatory or rating-agency changes could raise required capital, constraining buybacks or growth in stress.

- Capital- and hedge-intensive riders

- Fed funds ~5.25–5.50% (2024)

- Volatility increases hedge costs & basis risk

- Higher regulatory/rating requirements limit flexibility

Annuity-heavy insurer faces earnings and capital stress from market volatility and rising rates

Jackson remains highly concentrated in annuities (>50% sales via third parties), exposing earnings to equity volatility (VIX ~17 in 2024) and rates (10‑yr ~4.5%, Fed funds 5.25–5.50% in 2024). Product complexity and lengthy surrenders raise compliance and servicing costs; living benefits are capital- and hedge‑intensive, amplifying stress on capital and margins.

| Metric | 2024 |

|---|---|

| Channel share via intermediaries | >50% |

| VIX (avg) | ~17 |

| 10‑yr Treasury | ~4.5% |

| Fed funds | 5.25–5.50% |

Same Document Delivered

Jackson Financial SWOT Analysis

This is the actual Jackson Financial SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchasing unlocks the complete, editable version. Use it as-is for research, presentations, or further customization.

Dive Deeper Into the Company’s Strategic Blueprint

Jackson Financial's SWOT snapshot highlights solid asset-management capabilities, demographic-driven growth opportunities, and regulatory and longevity-risk pressures. Want the full strategic picture and financial context? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to guide investment or strategic planning.

Strengths

Market-leading annuity franchise

Jackson's market-leading U.S. retail annuity franchise, with roughly 20% market share, about 2.6 million policyholders and approximately $320 billion of annuity account value as of year-end 2024, drives pricing power and scale economies. High brand recognition in retirement income boosts distributor confidence and client adoption, supporting resilient new business flows across cycles. Franchise leadership strengthens negotiating leverage with reinsurers and vendors, compressing costs and protecting margins.

Broad, diversified product suite

Offering variable, fixed and fixed index annuities plus life insurance lets Jackson tailor solutions to varied risk tolerances and income needs, supporting both accumulation and retirement income strategies. Its diversified suite helps balance sales across rate and equity cycles, stabilizing revenue and capital deployment. Cross-selling deepens client relationships and boosts persistency, while product mix flexibility enables margin optimization over time; Jackson manages over $200 billion in assets (2024).

Extensive distribution network

Relationships with independent advisors and broker-dealers give Jackson national reach, supporting distribution into diverse channels and contributing to roughly $318 billion in assets under management at year-end 2024. Distribution breadth reduces single-channel dependency and helped drive steady annuity inflows in 2024. Strong wholesaling and practice-support teams boost advisor productivity, creating a network that is costly and time-consuming for new entrants to replicate.

Risk management and ALM capabilities

Jackson Financial's established hedging programs and ALM frameworks mitigate market and interest-rate risk in annuity guarantees, supported by roughly $260 billion of invested assets as of 2024 and advanced derivative governance.

Prudent capital management sustaining ratings and product competitiveness enhances resilience, with stress-tested strategies reducing volatility exposure and preserving solvency.

- Hedging coverage: broad ALM + derivatives

- Scale: ~$260B invested assets (2024)

- Capital: rating-backed prudence

- Outcome: stronger volatility resilience

Focus on retirement mission and brand trust

Jackson Financials clear retirement-income mission and brand trust bolster credibility with advisors and clients; as a top U.S. annuity provider with over $200 billion in assets under management (2024), its service, education and planning tools foster long-term relationships and lower lapse risk, supporting premium pricing for guarantees and driving advisor word-of-mouth.

- Mission-led brand

- >$200B AUM (2024)

- Lower lapse risk

- Stronger advisory referrals

Market-leading U.S. annuity franchise: ~20% share, 2.6M policyholders, $320B AAV

Market-leading U.S. annuity franchise (~20% share) with ~2.6M policyholders and $320B annuity account value (YE 2024) delivers scale, pricing power and distributor trust. Diversified product suite and distribution (>$200B AUM) stabilizes flows across cycles. Robust ALM/hedging and ~$260B invested assets (2024) support guarantee risk management.

| Metric | 2024 |

|---|---|

| Annuity AAV | $320B |

| Policyholders | 2.6M |

| Invested assets | $260B |

| AUM | $200B+ |

What is included in the product

Delivers a strategic overview of Jackson Financial’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, and key risks shaping future performance.

Provides a focused SWOT snapshot of Jackson Financial to quickly identify risks and opportunities, easing strategic alignment, stakeholder updates, and rapid decision-making.

Weaknesses

Concentration in annuities

As of 2024 Jackson remains heavily concentrated in annuities, heightening exposure to regulatory shifts and market volatility tied to one product class. Limited expansion into fee-based asset management constrains earnings stability and recurring fee income. Product concentration can amplify capital strain under stress scenarios and narrows strategic optionality versus multi-line peers.

Sensitivity to market and rate volatility

Jackson’s variable annuities with guarantees link earnings to equity markets and volatility (VIX averaged about 17 in 2024), exposing results to market swings. Interest-rate moves — the 10-year Treasury near 4.5% in 2024 — affect spreads, reserve requirements and hedging costs. Prolonged low or rapidly shifting rates compress new-business economics and amplify earnings variability.

Complex products and perceived high fees

Annuities are complex products that slow sales and invite scrutiny; surrender periods commonly span 5–10 years and early surrender charges can exceed 7% in initial years, deterring cost‑sensitive advisors and clients. Complexity raises suitability and disclosure risks and increases servicing and compliance costs.

Dependence on third-party distributors

Dependence on independent advisors limits Jackson Financials direct control over the end-client experience, since a majority of retail annuity sales (>50%) pass through broker-dealers and RIAs, reducing brand influence and client retention. Shelf space and selling focus can shift quickly with competitor incentives, while margin sharing with intermediaries compresses economics versus direct channels and channel conflicts slow rapid product pivots.

- Majority channel: >50% via third parties

- Margin pressure: shared commissions reduce net yield

- Shelf risk: competitors can re-prioritize advisors

- Speed to market: channel conflicts hinder pivots

Capital- and hedge-intensive guarantees

Living benefit riders require significant capital and continuous hedging; with the Fed funds rate around 5.25–5.50% in 2024, funding and duration mismatches remain sensitive to rate moves. Elevated market volatility can sharply spike hedge costs and basis risk, while potential regulatory or rating-agency changes could raise required capital, constraining buybacks or growth in stress.

- Capital- and hedge-intensive riders

- Fed funds ~5.25–5.50% (2024)

- Volatility increases hedge costs & basis risk

- Higher regulatory/rating requirements limit flexibility

Annuity-heavy insurer faces earnings and capital stress from market volatility and rising rates

Jackson remains highly concentrated in annuities (>50% sales via third parties), exposing earnings to equity volatility (VIX ~17 in 2024) and rates (10‑yr ~4.5%, Fed funds 5.25–5.50% in 2024). Product complexity and lengthy surrenders raise compliance and servicing costs; living benefits are capital- and hedge‑intensive, amplifying stress on capital and margins.

| Metric | 2024 |

|---|---|

| Channel share via intermediaries | >50% |

| VIX (avg) | ~17 |

| 10‑yr Treasury | ~4.5% |

| Fed funds | 5.25–5.50% |

Same Document Delivered

Jackson Financial SWOT Analysis

This is the actual Jackson Financial SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchasing unlocks the complete, editable version. Use it as-is for research, presentations, or further customization.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Jackson Financial's SWOT snapshot highlights solid asset-management capabilities, demographic-driven growth opportunities, and regulatory and longevity-risk pressures. Want the full strategic picture and financial context? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to guide investment or strategic planning.

Strengths

Market-leading annuity franchise

Jackson's market-leading U.S. retail annuity franchise, with roughly 20% market share, about 2.6 million policyholders and approximately $320 billion of annuity account value as of year-end 2024, drives pricing power and scale economies. High brand recognition in retirement income boosts distributor confidence and client adoption, supporting resilient new business flows across cycles. Franchise leadership strengthens negotiating leverage with reinsurers and vendors, compressing costs and protecting margins.

Broad, diversified product suite

Offering variable, fixed and fixed index annuities plus life insurance lets Jackson tailor solutions to varied risk tolerances and income needs, supporting both accumulation and retirement income strategies. Its diversified suite helps balance sales across rate and equity cycles, stabilizing revenue and capital deployment. Cross-selling deepens client relationships and boosts persistency, while product mix flexibility enables margin optimization over time; Jackson manages over $200 billion in assets (2024).

Extensive distribution network

Relationships with independent advisors and broker-dealers give Jackson national reach, supporting distribution into diverse channels and contributing to roughly $318 billion in assets under management at year-end 2024. Distribution breadth reduces single-channel dependency and helped drive steady annuity inflows in 2024. Strong wholesaling and practice-support teams boost advisor productivity, creating a network that is costly and time-consuming for new entrants to replicate.

Risk management and ALM capabilities

Jackson Financial's established hedging programs and ALM frameworks mitigate market and interest-rate risk in annuity guarantees, supported by roughly $260 billion of invested assets as of 2024 and advanced derivative governance.

Prudent capital management sustaining ratings and product competitiveness enhances resilience, with stress-tested strategies reducing volatility exposure and preserving solvency.

- Hedging coverage: broad ALM + derivatives

- Scale: ~$260B invested assets (2024)

- Capital: rating-backed prudence

- Outcome: stronger volatility resilience

Focus on retirement mission and brand trust

Jackson Financials clear retirement-income mission and brand trust bolster credibility with advisors and clients; as a top U.S. annuity provider with over $200 billion in assets under management (2024), its service, education and planning tools foster long-term relationships and lower lapse risk, supporting premium pricing for guarantees and driving advisor word-of-mouth.

- Mission-led brand

- >$200B AUM (2024)

- Lower lapse risk

- Stronger advisory referrals

Market-leading U.S. annuity franchise: ~20% share, 2.6M policyholders, $320B AAV

Market-leading U.S. annuity franchise (~20% share) with ~2.6M policyholders and $320B annuity account value (YE 2024) delivers scale, pricing power and distributor trust. Diversified product suite and distribution (>$200B AUM) stabilizes flows across cycles. Robust ALM/hedging and ~$260B invested assets (2024) support guarantee risk management.

| Metric | 2024 |

|---|---|

| Annuity AAV | $320B |

| Policyholders | 2.6M |

| Invested assets | $260B |

| AUM | $200B+ |

What is included in the product

Delivers a strategic overview of Jackson Financial’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, and key risks shaping future performance.

Provides a focused SWOT snapshot of Jackson Financial to quickly identify risks and opportunities, easing strategic alignment, stakeholder updates, and rapid decision-making.

Weaknesses

Concentration in annuities

As of 2024 Jackson remains heavily concentrated in annuities, heightening exposure to regulatory shifts and market volatility tied to one product class. Limited expansion into fee-based asset management constrains earnings stability and recurring fee income. Product concentration can amplify capital strain under stress scenarios and narrows strategic optionality versus multi-line peers.

Sensitivity to market and rate volatility

Jackson’s variable annuities with guarantees link earnings to equity markets and volatility (VIX averaged about 17 in 2024), exposing results to market swings. Interest-rate moves — the 10-year Treasury near 4.5% in 2024 — affect spreads, reserve requirements and hedging costs. Prolonged low or rapidly shifting rates compress new-business economics and amplify earnings variability.

Complex products and perceived high fees

Annuities are complex products that slow sales and invite scrutiny; surrender periods commonly span 5–10 years and early surrender charges can exceed 7% in initial years, deterring cost‑sensitive advisors and clients. Complexity raises suitability and disclosure risks and increases servicing and compliance costs.

Dependence on third-party distributors

Dependence on independent advisors limits Jackson Financials direct control over the end-client experience, since a majority of retail annuity sales (>50%) pass through broker-dealers and RIAs, reducing brand influence and client retention. Shelf space and selling focus can shift quickly with competitor incentives, while margin sharing with intermediaries compresses economics versus direct channels and channel conflicts slow rapid product pivots.

- Majority channel: >50% via third parties

- Margin pressure: shared commissions reduce net yield

- Shelf risk: competitors can re-prioritize advisors

- Speed to market: channel conflicts hinder pivots

Capital- and hedge-intensive guarantees

Living benefit riders require significant capital and continuous hedging; with the Fed funds rate around 5.25–5.50% in 2024, funding and duration mismatches remain sensitive to rate moves. Elevated market volatility can sharply spike hedge costs and basis risk, while potential regulatory or rating-agency changes could raise required capital, constraining buybacks or growth in stress.

- Capital- and hedge-intensive riders

- Fed funds ~5.25–5.50% (2024)

- Volatility increases hedge costs & basis risk

- Higher regulatory/rating requirements limit flexibility

Annuity-heavy insurer faces earnings and capital stress from market volatility and rising rates

Jackson remains highly concentrated in annuities (>50% sales via third parties), exposing earnings to equity volatility (VIX ~17 in 2024) and rates (10‑yr ~4.5%, Fed funds 5.25–5.50% in 2024). Product complexity and lengthy surrenders raise compliance and servicing costs; living benefits are capital- and hedge‑intensive, amplifying stress on capital and margins.

| Metric | 2024 |

|---|---|

| Channel share via intermediaries | >50% |

| VIX (avg) | ~17 |

| 10‑yr Treasury | ~4.5% |

| Fed funds | 5.25–5.50% |

Same Document Delivered

Jackson Financial SWOT Analysis

This is the actual Jackson Financial SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchasing unlocks the complete, editable version. Use it as-is for research, presentations, or further customization.