Jain Irrigation Systems PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental risks are shaping Jain Irrigation Systems’ strategic outlook; our concise PESTLE highlights key external drivers and blind spots. Purchase the full, ready-to-use analysis to unlock actionable insights, forecasts, and strategic recommendations for investment or planning.

Political factors

Agri subsidy and irrigation policy alignment

Government micro-irrigation incentives under PMKSY Per Drop More Crop (launched 2015) and the Rs 1 lakh crore Agriculture Infrastructure Fund support demand and farmer affordability for drip and sprinkler systems. Policy continuity at Union and state levels drives order visibility and receivables cycles for Jain Irrigation, while prioritization of water conservation in public budgets sustains project pipelines. Shifts in rural development focus or election cycles can materially alter funding pace and rollout timing.

State procurement and public tender exposure

Significant sales for Jain Irrigation flow through state-led tenders and scheme-linked procurement, notably under programmes such as PMKSY and MGNREGA, lengthening sales cycles when administrative delays, budget reallocations or model code of conduct arise. Vendor registration, local content norms and preference policies materially affect bid competitiveness and margins. Decentralized governance across 28 states and 8 union territories creates uneven state-level opportunities and risks.

Trade policy on polymers and components

Import duties and anti-dumping measures materially affect PVC/resin and component costs for Jain Irrigation, with trade remedies commonly adding up to 25% on targeted imports; FTAs such as India-UAE CEPA (2022) and India-Australia ECTA (2022) can lower tariffs and ease resin sourcing. Tariff shifts rapidly change margin structures and pricing strategy, while localization incentives and production-linked schemes favor expanding domestic manufacturing footprint. Global geopolitical shifts (supply-chain disruptions, sanctions) can abruptly limit input availability and spike spot resin prices.

Rural infrastructure and irrigation capex

Public investment in canals, water grids and solar pump rollouts materially accelerates micro‑irrigation uptake by reducing farmers' capital and operational barriers; convergence with horticulture and renewable energy schemes creates clear cross‑sell pathways for Jain Irrigation, while infrastructure prioritization improves logistics and service reach, though budget tightness or policy re‑prioritization can delay project rollouts.

- Public capex complements micro‑irrigation adoption

- Convergence enables cross‑selling (horticulture, renewables)

- Better infrastructure boosts logistics/service reach

- Budget cuts or reprioritization can defer projects

Agri export and food security stance

India's policy balancing food security with export promotion shapes demand for Jain Irrigation's horticulture, with agri exports at about USD 50.3 billion in FY2023-24 boosting tissue-culture and micro-irrigation sales; export incentives (RoDTEP/RCMP) raise input demand. Sanitary and phytosanitary diplomacy determines market access—rejections under SPS rules have trimmed shipments to EU/US in 2023–24. MSP shifts in 2024 altered cropping patterns, diverting area from pulses to paddy/wheat, affecting high-value crop supply.

- agri exports: USD 50.3bn FY2023-24

- export incentives ↑ tissue-culture demand

- SPS diplomacy = market access risk

- MSP shifts reallocate cropping patterns

Incentives and Rs 1 lakh crore fund boost micro-irrigation; exports USD 50.3bn, duties ~25%

Government incentives (PMKSY Per Drop More Crop since 2015) and the Rs 1 lakh crore Agriculture Infrastructure Fund sustain demand and farmer affordability for micro‑irrigation. State tenders and procurement cycles, plus import duties/anti‑dumping (up to ~25%), shape margins and receivables; agri exports were USD 50.3bn in FY2023‑24 supporting horticulture demand. Election cycles, MSP shifts in 2024 and budget reprioritisations pose timing risks.

| Item | Value/Impact |

|---|---|

| PMKSY | Demand driver since 2015 |

| Agriculture Infrastructure Fund | Rs 1 lakh crore — credit support |

| Agri exports | USD 50.3bn FY2023‑24 |

| Import duties/AD | Up to ~25% — input cost risk |

What is included in the product

Explores how macro-environmental factors uniquely affect Jain Irrigation Systems across Political, Economic, Social, Technological, Environmental and Legal dimensions, with sector- and region-specific examples. Each section is data-backed, forward-looking and designed to help executives and investors identify risks, opportunities and strategic responses.

A clean, summarized PESTLE of Jain Irrigation Systems, visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Monsoon variability and farm cash flows

Rainfall outcomes directly shape crop yields, farm incomes and micro‑irrigation uptake; weak monsoons raise urgency for water‑saving but strain liquidity, while good seasons improve affordability. Agriculture accounts for about 17.8% of India’s GDP (2023–24), and micro‑irrigation covers roughly 12.3 million ha (2023), supporting demand swings. Crop insurance and rural credit penetration partially mitigate volatility, and regional monsoon dispersion alters state‑wise sales mix for Jain Irrigation.

Raw material price volatility (PVC/resins)

PVC/resin costs at Jain track crude-linked naphtha/ethylene pricing—Brent averaged about $84/bbl in 2024—directly pressuring COGS and working capital. Timely pass-throughs to customers and inventory hedging are critical to protect margins. Historical supply shocks such as the 2022 Russia–Ukraine disruptions show how quickly resin spikes can occur. A shift toward higher-margin product mix and value-added services cushions volatility by reducing raw-material intensity.

Rural credit availability and interest rates

NBFC and bank lending appetite and Priority Sector Lending norms (40% of net credit) significantly drive farmer conversion; agricultural credit flow was about Rs 18.5 lakh crore in FY2023-24, supporting irrigation finance. Lower interest rates (100–200 bps cuts) improve payback economics for farmers and dealers, raising adoption. Government/NABARD refinance schemes and targeted refinance lines catalyze uptake, while tight credit cycles in 2024 slowed collections and squeezed dealer liquidity.

Currency and export market dynamics

FX movements directly affect Jain Irrigation’s import costs and export competitiveness; significant INR swings in recent years have increased margin pressure, making disciplined pricing and contract currency clauses critical. The company’s presence in over 120 countries diversifies revenue, reducing single-market risk while global demand for horticulture inputs and irrigation/solar projects supports growth. Currency volatility therefore necessitates formal hedging and treasury policies to protect margins.

- FX impact on margins

- Presence in 120+ countries (diversification)

- Rising global demand for irrigation/solar

- Need for robust hedging policies

Inflation and affordability of solutions

Inflation pressures—India's RBI target 4% band—raise input costs and squeeze farmer purchasing power, pushing demand toward lower-priced irrigation and drip solutions; Jain's tiered product range and dealer financing have historically preserved volumes by offering entry-level options. Emphasizing productivity ROI (higher yields, water savings) supports price acceptance, but prolonged inflation risks deferring discretionary upgrades.

- RBI target 4% (inflation context)

- Agriculture ~18% of GDP — productivity ROI key

- Tiered offerings + financing sustain volumes

- Prolonged inflation may delay upgrades

Incentives and Rs 1 lakh crore fund boost micro-irrigation; exports USD 50.3bn, duties ~25%

Rainfall variability and monsoon strength drive micro‑irrigation demand—agriculture ~17.8% of GDP (2023–24) and micro‑irrigation ~12.3m ha (2023). Resin/PVC costs track crude (Brent ~$84/bbl in 2024) affecting COGS; product mix and pass‑throughs protect margins. Agri credit ~Rs18.5 lakh crore (FY2023‑24) and RBI 4% target shape farmer affordability; 120+ country presence diversifies FX risk.

| Metric | Value |

|---|---|

| Agriculture % GDP | 17.8% (2023‑24) |

| Micro‑irrigation area | 12.3m ha (2023) |

| Brent avg | $84/bbl (2024) |

| Agri credit | Rs18.5L cr (FY2023‑24) |

| Global presence | 120+ countries |

What You See Is What You Get

Jain Irrigation Systems PESTLE Analysis

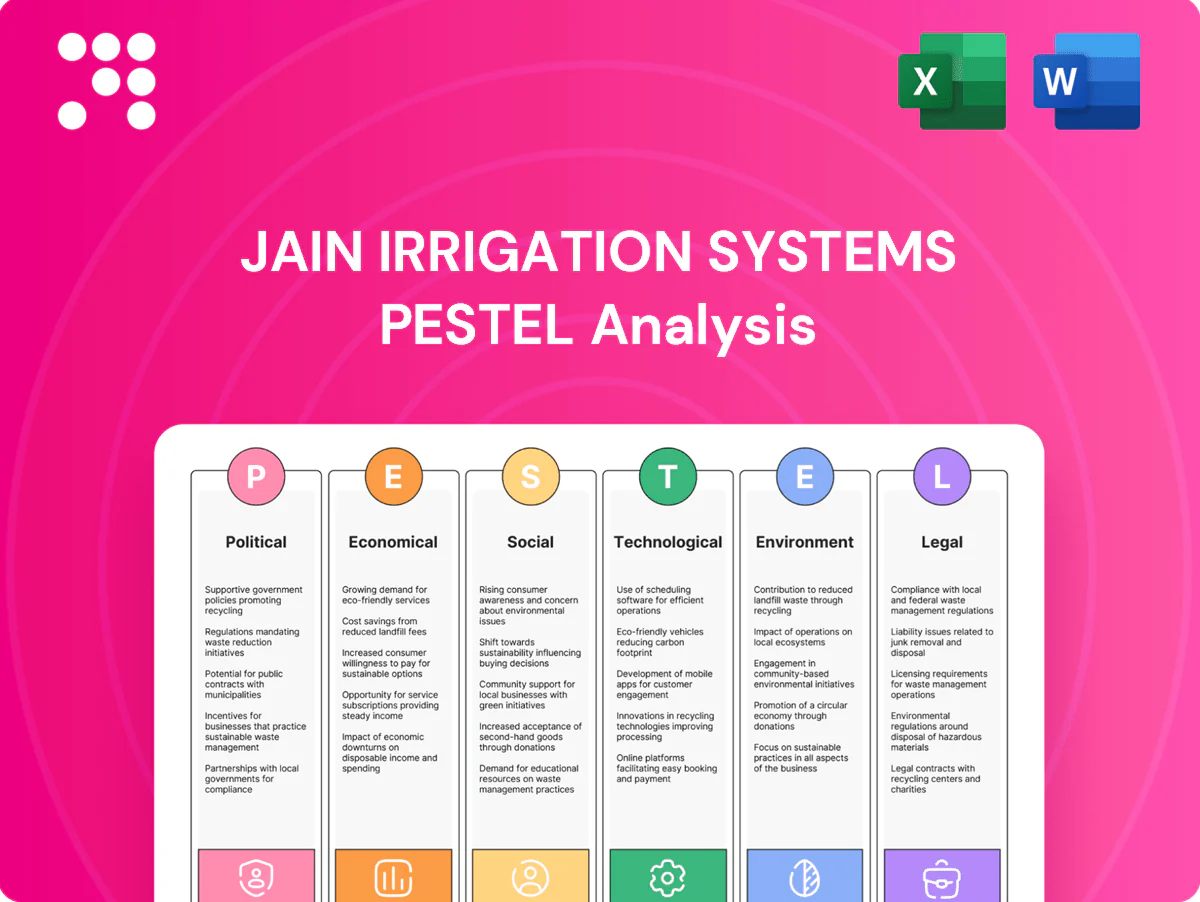

The Jain Irrigation Systems PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the real, finished file. After checkout you’ll download the same professionally structured document instantly.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental risks are shaping Jain Irrigation Systems’ strategic outlook; our concise PESTLE highlights key external drivers and blind spots. Purchase the full, ready-to-use analysis to unlock actionable insights, forecasts, and strategic recommendations for investment or planning.

Political factors

Agri subsidy and irrigation policy alignment

Government micro-irrigation incentives under PMKSY Per Drop More Crop (launched 2015) and the Rs 1 lakh crore Agriculture Infrastructure Fund support demand and farmer affordability for drip and sprinkler systems. Policy continuity at Union and state levels drives order visibility and receivables cycles for Jain Irrigation, while prioritization of water conservation in public budgets sustains project pipelines. Shifts in rural development focus or election cycles can materially alter funding pace and rollout timing.

State procurement and public tender exposure

Significant sales for Jain Irrigation flow through state-led tenders and scheme-linked procurement, notably under programmes such as PMKSY and MGNREGA, lengthening sales cycles when administrative delays, budget reallocations or model code of conduct arise. Vendor registration, local content norms and preference policies materially affect bid competitiveness and margins. Decentralized governance across 28 states and 8 union territories creates uneven state-level opportunities and risks.

Trade policy on polymers and components

Import duties and anti-dumping measures materially affect PVC/resin and component costs for Jain Irrigation, with trade remedies commonly adding up to 25% on targeted imports; FTAs such as India-UAE CEPA (2022) and India-Australia ECTA (2022) can lower tariffs and ease resin sourcing. Tariff shifts rapidly change margin structures and pricing strategy, while localization incentives and production-linked schemes favor expanding domestic manufacturing footprint. Global geopolitical shifts (supply-chain disruptions, sanctions) can abruptly limit input availability and spike spot resin prices.

Rural infrastructure and irrigation capex

Public investment in canals, water grids and solar pump rollouts materially accelerates micro‑irrigation uptake by reducing farmers' capital and operational barriers; convergence with horticulture and renewable energy schemes creates clear cross‑sell pathways for Jain Irrigation, while infrastructure prioritization improves logistics and service reach, though budget tightness or policy re‑prioritization can delay project rollouts.

- Public capex complements micro‑irrigation adoption

- Convergence enables cross‑selling (horticulture, renewables)

- Better infrastructure boosts logistics/service reach

- Budget cuts or reprioritization can defer projects

Agri export and food security stance

India's policy balancing food security with export promotion shapes demand for Jain Irrigation's horticulture, with agri exports at about USD 50.3 billion in FY2023-24 boosting tissue-culture and micro-irrigation sales; export incentives (RoDTEP/RCMP) raise input demand. Sanitary and phytosanitary diplomacy determines market access—rejections under SPS rules have trimmed shipments to EU/US in 2023–24. MSP shifts in 2024 altered cropping patterns, diverting area from pulses to paddy/wheat, affecting high-value crop supply.

- agri exports: USD 50.3bn FY2023-24

- export incentives ↑ tissue-culture demand

- SPS diplomacy = market access risk

- MSP shifts reallocate cropping patterns

Incentives and Rs 1 lakh crore fund boost micro-irrigation; exports USD 50.3bn, duties ~25%

Government incentives (PMKSY Per Drop More Crop since 2015) and the Rs 1 lakh crore Agriculture Infrastructure Fund sustain demand and farmer affordability for micro‑irrigation. State tenders and procurement cycles, plus import duties/anti‑dumping (up to ~25%), shape margins and receivables; agri exports were USD 50.3bn in FY2023‑24 supporting horticulture demand. Election cycles, MSP shifts in 2024 and budget reprioritisations pose timing risks.

| Item | Value/Impact |

|---|---|

| PMKSY | Demand driver since 2015 |

| Agriculture Infrastructure Fund | Rs 1 lakh crore — credit support |

| Agri exports | USD 50.3bn FY2023‑24 |

| Import duties/AD | Up to ~25% — input cost risk |

What is included in the product

Explores how macro-environmental factors uniquely affect Jain Irrigation Systems across Political, Economic, Social, Technological, Environmental and Legal dimensions, with sector- and region-specific examples. Each section is data-backed, forward-looking and designed to help executives and investors identify risks, opportunities and strategic responses.

A clean, summarized PESTLE of Jain Irrigation Systems, visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Monsoon variability and farm cash flows

Rainfall outcomes directly shape crop yields, farm incomes and micro‑irrigation uptake; weak monsoons raise urgency for water‑saving but strain liquidity, while good seasons improve affordability. Agriculture accounts for about 17.8% of India’s GDP (2023–24), and micro‑irrigation covers roughly 12.3 million ha (2023), supporting demand swings. Crop insurance and rural credit penetration partially mitigate volatility, and regional monsoon dispersion alters state‑wise sales mix for Jain Irrigation.

Raw material price volatility (PVC/resins)

PVC/resin costs at Jain track crude-linked naphtha/ethylene pricing—Brent averaged about $84/bbl in 2024—directly pressuring COGS and working capital. Timely pass-throughs to customers and inventory hedging are critical to protect margins. Historical supply shocks such as the 2022 Russia–Ukraine disruptions show how quickly resin spikes can occur. A shift toward higher-margin product mix and value-added services cushions volatility by reducing raw-material intensity.

Rural credit availability and interest rates

NBFC and bank lending appetite and Priority Sector Lending norms (40% of net credit) significantly drive farmer conversion; agricultural credit flow was about Rs 18.5 lakh crore in FY2023-24, supporting irrigation finance. Lower interest rates (100–200 bps cuts) improve payback economics for farmers and dealers, raising adoption. Government/NABARD refinance schemes and targeted refinance lines catalyze uptake, while tight credit cycles in 2024 slowed collections and squeezed dealer liquidity.

Currency and export market dynamics

FX movements directly affect Jain Irrigation’s import costs and export competitiveness; significant INR swings in recent years have increased margin pressure, making disciplined pricing and contract currency clauses critical. The company’s presence in over 120 countries diversifies revenue, reducing single-market risk while global demand for horticulture inputs and irrigation/solar projects supports growth. Currency volatility therefore necessitates formal hedging and treasury policies to protect margins.

- FX impact on margins

- Presence in 120+ countries (diversification)

- Rising global demand for irrigation/solar

- Need for robust hedging policies

Inflation and affordability of solutions

Inflation pressures—India's RBI target 4% band—raise input costs and squeeze farmer purchasing power, pushing demand toward lower-priced irrigation and drip solutions; Jain's tiered product range and dealer financing have historically preserved volumes by offering entry-level options. Emphasizing productivity ROI (higher yields, water savings) supports price acceptance, but prolonged inflation risks deferring discretionary upgrades.

- RBI target 4% (inflation context)

- Agriculture ~18% of GDP — productivity ROI key

- Tiered offerings + financing sustain volumes

- Prolonged inflation may delay upgrades

Incentives and Rs 1 lakh crore fund boost micro-irrigation; exports USD 50.3bn, duties ~25%

Rainfall variability and monsoon strength drive micro‑irrigation demand—agriculture ~17.8% of GDP (2023–24) and micro‑irrigation ~12.3m ha (2023). Resin/PVC costs track crude (Brent ~$84/bbl in 2024) affecting COGS; product mix and pass‑throughs protect margins. Agri credit ~Rs18.5 lakh crore (FY2023‑24) and RBI 4% target shape farmer affordability; 120+ country presence diversifies FX risk.

| Metric | Value |

|---|---|

| Agriculture % GDP | 17.8% (2023‑24) |

| Micro‑irrigation area | 12.3m ha (2023) |

| Brent avg | $84/bbl (2024) |

| Agri credit | Rs18.5L cr (FY2023‑24) |

| Global presence | 120+ countries |

What You See Is What You Get

Jain Irrigation Systems PESTLE Analysis

The Jain Irrigation Systems PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the real, finished file. After checkout you’ll download the same professionally structured document instantly.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic pressures, social trends, technological advances, legal changes, and environmental risks are shaping Jain Irrigation Systems’ strategic outlook; our concise PESTLE highlights key external drivers and blind spots. Purchase the full, ready-to-use analysis to unlock actionable insights, forecasts, and strategic recommendations for investment or planning.

Political factors

Agri subsidy and irrigation policy alignment

Government micro-irrigation incentives under PMKSY Per Drop More Crop (launched 2015) and the Rs 1 lakh crore Agriculture Infrastructure Fund support demand and farmer affordability for drip and sprinkler systems. Policy continuity at Union and state levels drives order visibility and receivables cycles for Jain Irrigation, while prioritization of water conservation in public budgets sustains project pipelines. Shifts in rural development focus or election cycles can materially alter funding pace and rollout timing.

State procurement and public tender exposure

Significant sales for Jain Irrigation flow through state-led tenders and scheme-linked procurement, notably under programmes such as PMKSY and MGNREGA, lengthening sales cycles when administrative delays, budget reallocations or model code of conduct arise. Vendor registration, local content norms and preference policies materially affect bid competitiveness and margins. Decentralized governance across 28 states and 8 union territories creates uneven state-level opportunities and risks.

Trade policy on polymers and components

Import duties and anti-dumping measures materially affect PVC/resin and component costs for Jain Irrigation, with trade remedies commonly adding up to 25% on targeted imports; FTAs such as India-UAE CEPA (2022) and India-Australia ECTA (2022) can lower tariffs and ease resin sourcing. Tariff shifts rapidly change margin structures and pricing strategy, while localization incentives and production-linked schemes favor expanding domestic manufacturing footprint. Global geopolitical shifts (supply-chain disruptions, sanctions) can abruptly limit input availability and spike spot resin prices.

Rural infrastructure and irrigation capex

Public investment in canals, water grids and solar pump rollouts materially accelerates micro‑irrigation uptake by reducing farmers' capital and operational barriers; convergence with horticulture and renewable energy schemes creates clear cross‑sell pathways for Jain Irrigation, while infrastructure prioritization improves logistics and service reach, though budget tightness or policy re‑prioritization can delay project rollouts.

- Public capex complements micro‑irrigation adoption

- Convergence enables cross‑selling (horticulture, renewables)

- Better infrastructure boosts logistics/service reach

- Budget cuts or reprioritization can defer projects

Agri export and food security stance

India's policy balancing food security with export promotion shapes demand for Jain Irrigation's horticulture, with agri exports at about USD 50.3 billion in FY2023-24 boosting tissue-culture and micro-irrigation sales; export incentives (RoDTEP/RCMP) raise input demand. Sanitary and phytosanitary diplomacy determines market access—rejections under SPS rules have trimmed shipments to EU/US in 2023–24. MSP shifts in 2024 altered cropping patterns, diverting area from pulses to paddy/wheat, affecting high-value crop supply.

- agri exports: USD 50.3bn FY2023-24

- export incentives ↑ tissue-culture demand

- SPS diplomacy = market access risk

- MSP shifts reallocate cropping patterns

Incentives and Rs 1 lakh crore fund boost micro-irrigation; exports USD 50.3bn, duties ~25%

Government incentives (PMKSY Per Drop More Crop since 2015) and the Rs 1 lakh crore Agriculture Infrastructure Fund sustain demand and farmer affordability for micro‑irrigation. State tenders and procurement cycles, plus import duties/anti‑dumping (up to ~25%), shape margins and receivables; agri exports were USD 50.3bn in FY2023‑24 supporting horticulture demand. Election cycles, MSP shifts in 2024 and budget reprioritisations pose timing risks.

| Item | Value/Impact |

|---|---|

| PMKSY | Demand driver since 2015 |

| Agriculture Infrastructure Fund | Rs 1 lakh crore — credit support |

| Agri exports | USD 50.3bn FY2023‑24 |

| Import duties/AD | Up to ~25% — input cost risk |

What is included in the product

Explores how macro-environmental factors uniquely affect Jain Irrigation Systems across Political, Economic, Social, Technological, Environmental and Legal dimensions, with sector- and region-specific examples. Each section is data-backed, forward-looking and designed to help executives and investors identify risks, opportunities and strategic responses.

A clean, summarized PESTLE of Jain Irrigation Systems, visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Monsoon variability and farm cash flows

Rainfall outcomes directly shape crop yields, farm incomes and micro‑irrigation uptake; weak monsoons raise urgency for water‑saving but strain liquidity, while good seasons improve affordability. Agriculture accounts for about 17.8% of India’s GDP (2023–24), and micro‑irrigation covers roughly 12.3 million ha (2023), supporting demand swings. Crop insurance and rural credit penetration partially mitigate volatility, and regional monsoon dispersion alters state‑wise sales mix for Jain Irrigation.

Raw material price volatility (PVC/resins)

PVC/resin costs at Jain track crude-linked naphtha/ethylene pricing—Brent averaged about $84/bbl in 2024—directly pressuring COGS and working capital. Timely pass-throughs to customers and inventory hedging are critical to protect margins. Historical supply shocks such as the 2022 Russia–Ukraine disruptions show how quickly resin spikes can occur. A shift toward higher-margin product mix and value-added services cushions volatility by reducing raw-material intensity.

Rural credit availability and interest rates

NBFC and bank lending appetite and Priority Sector Lending norms (40% of net credit) significantly drive farmer conversion; agricultural credit flow was about Rs 18.5 lakh crore in FY2023-24, supporting irrigation finance. Lower interest rates (100–200 bps cuts) improve payback economics for farmers and dealers, raising adoption. Government/NABARD refinance schemes and targeted refinance lines catalyze uptake, while tight credit cycles in 2024 slowed collections and squeezed dealer liquidity.

Currency and export market dynamics

FX movements directly affect Jain Irrigation’s import costs and export competitiveness; significant INR swings in recent years have increased margin pressure, making disciplined pricing and contract currency clauses critical. The company’s presence in over 120 countries diversifies revenue, reducing single-market risk while global demand for horticulture inputs and irrigation/solar projects supports growth. Currency volatility therefore necessitates formal hedging and treasury policies to protect margins.

- FX impact on margins

- Presence in 120+ countries (diversification)

- Rising global demand for irrigation/solar

- Need for robust hedging policies

Inflation and affordability of solutions

Inflation pressures—India's RBI target 4% band—raise input costs and squeeze farmer purchasing power, pushing demand toward lower-priced irrigation and drip solutions; Jain's tiered product range and dealer financing have historically preserved volumes by offering entry-level options. Emphasizing productivity ROI (higher yields, water savings) supports price acceptance, but prolonged inflation risks deferring discretionary upgrades.

- RBI target 4% (inflation context)

- Agriculture ~18% of GDP — productivity ROI key

- Tiered offerings + financing sustain volumes

- Prolonged inflation may delay upgrades

Incentives and Rs 1 lakh crore fund boost micro-irrigation; exports USD 50.3bn, duties ~25%

Rainfall variability and monsoon strength drive micro‑irrigation demand—agriculture ~17.8% of GDP (2023–24) and micro‑irrigation ~12.3m ha (2023). Resin/PVC costs track crude (Brent ~$84/bbl in 2024) affecting COGS; product mix and pass‑throughs protect margins. Agri credit ~Rs18.5 lakh crore (FY2023‑24) and RBI 4% target shape farmer affordability; 120+ country presence diversifies FX risk.

| Metric | Value |

|---|---|

| Agriculture % GDP | 17.8% (2023‑24) |

| Micro‑irrigation area | 12.3m ha (2023) |

| Brent avg | $84/bbl (2024) |

| Agri credit | Rs18.5L cr (FY2023‑24) |

| Global presence | 120+ countries |

What You See Is What You Get

Jain Irrigation Systems PESTLE Analysis

The Jain Irrigation Systems PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers—this is the real, finished file. After checkout you’ll download the same professionally structured document instantly.