James Fisher and Sons Boston Consulting Group Matrix

Download Your Competitive Advantage

Quick snapshot: James Fisher and Sons’ product mix sits at an inflection point — a couple of strong performers, some steady earners, and a few units begging for a clear plan. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use Word + Excel pack that saves you hours and points straight to where capital and attention should go. Act now and turn this map into decisions you can implement tomorrow.

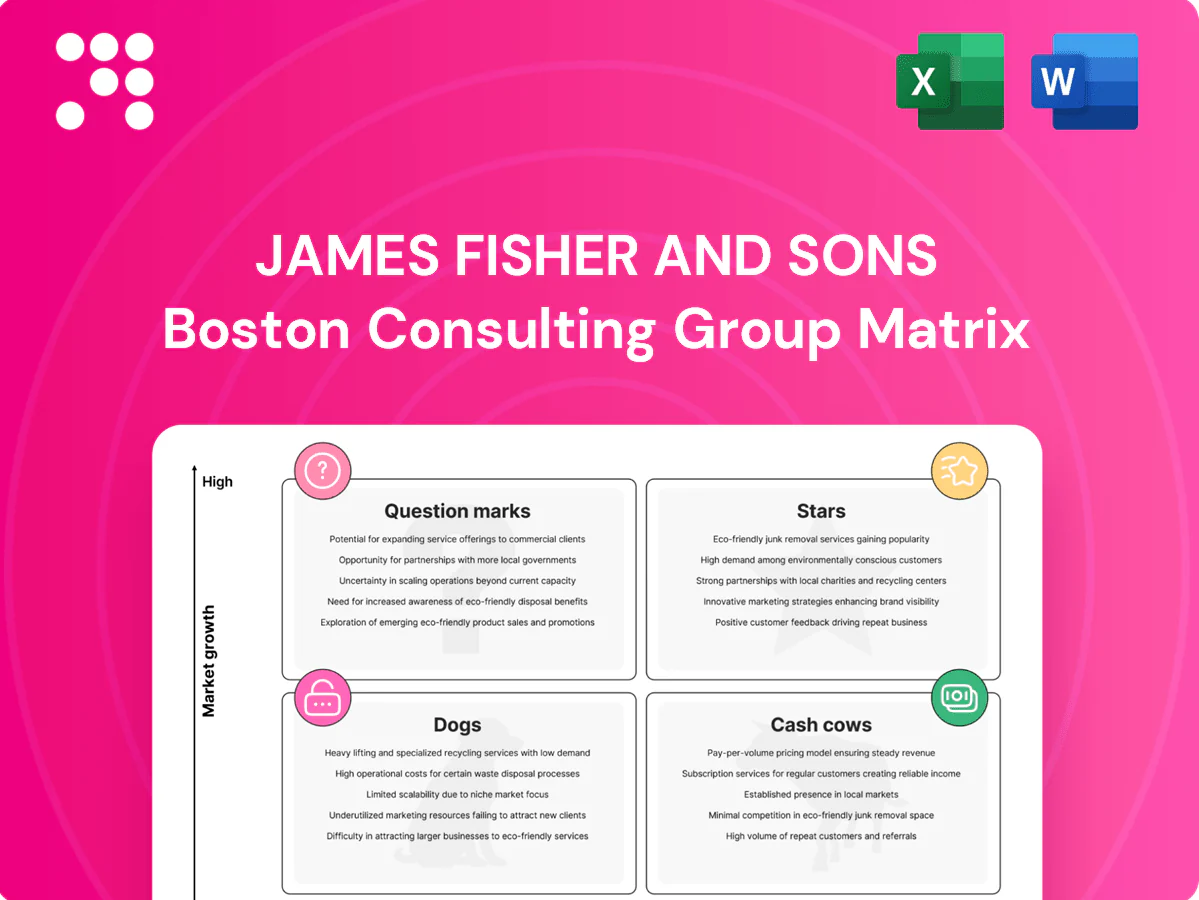

Stars

Subsea engineering for renewables

High-growth offshore wind and tidal work, underscored by the UK 50 GW by 2030 target, expands addressable market for James Fisher’s subsea engineering niches. The business holds a solid share in specialist subsea roles but current projects need heavy promotion and specialist placement, soaking cash in pre-construction and mobilisation. Keep winning frameworks and it can graduate into steady O&M dominance. Invest now to scale crews, assets and remote capability while the market is still sprinting.

JFD submarine rescue solutions

JFD submarine rescue is a mission-critical defense capability with few credible rivals and a global submarine fleet of roughly 430 vessels in 2024, driving demand. High-spec platforms and long-term support create strong customer stickiness, though bid cycles and readiness costs depress near-term cash flow. Protect share via readiness KPIs and regular tech refresh; as growth normalizes the unit can become a durable cash engine for James Fisher.

Offshore decommissioning services

Regulatory tailwinds and a rising backlog—UK decommissioning liability c.£60bn in 2024—push James Fisher’s offshore decommissioning into a clear growth lane. Their specialist subsea know‑how secures complex scopes, but heavy mobilization and HSE intensity pull cash forward and compress near‑term free cash flow. Keeping utilization high and standardizing methods is critical to defend share. Execution excellence now builds the pathway to future cash‑cow margins.

Specialist IRM for energy assets

Specialist IRM for energy assets is a Stars position: inspection, repair and maintenance demand rising in 2024 as fleets and fields age; strong reputation brings awards and repeat wins, but kit, skilled crews and standby costs are heavy. Securing 3–7 year programmes locks scale; pushing digital and remote inspection is essential to keep growth profitable.

- Inspection-led growth 2024

- High CAPEX: kit & standby

- Multi-year contracts 3–7 years

- Digital/remote efficiency

Marine project logistics and lifting

Marine project logistics and lifting sit in Stars as 2024 subsea and renewables build‑out fuels complex heavy‑lift moves; global offshore wind pipeline exceeds 400 GW in 2024, raising demand for coordinated lifts and logistics.

High coordination drives elevated working capital and promotional effort; flawless on‑time, on‑budget delivery preserves market share via referrals.

Systemize playbooks, standardize bids and cash conversion now to capture premium margins as headline growth normalizes.

- 2024: >400 GW offshore wind pipeline

- High working capital intensity

- Delivery reliability = organic protection

- Action: codify playbooks, optimize cash conversion

Invest in crews, assets & digital: 50 GW, £60bn, 430 subs

High-growth offshore wind/tidal (UK 50 GW by 2030) expands addressable market; specialist subsea roles are cash‑hungry in pre‑construction but can scale into O&M. JFD submarine rescue sees durable demand from ~430 global subs in 2024 but readiness ties up cash. Decommissioning (UK liability c.£60bn) and >400 GW offshore pipeline (2024) make IRM/logistics Stars—invest in crews, assets, digital and standardized bids.

| Segment | 2024 metric | Key action |

|---|---|---|

| Offshore/tidal | UK 50 GW by 2030 | Scale O&M, assets |

| Submarine rescue | ~430 subs | Protect readiness KPIs |

| Decom/IRM/logistics | UK £60bn; >400 GW pipeline | Standardize, digitize |

What is included in the product

BCG Matrix analysis of James Fisher & Sons: Stars, Cash Cows, Question Marks, Dogs with strategic investment, hold or divest guidance.

One-page BCG for James Fisher and Sons, placing each business unit in a clear quadrant to cut decision friction.

Cash Cows

Ship management contracts

Ship management contracts sit in a mature market with stable volumes and recurring fee streams; James Fisher reported group revenue of about £246.6m for 2023, with ship management a steady cash contributor. When utilization and safety metrics stay top-tier, margins hold up, supporting mid-single-digit operating margins in the segment. Low promotional needs make it retention-driven; targeted investment in tooling and process can raise cash per managed vessel.

Classical marine services (port, mooring)

Classical marine services (port, mooring) deliver steady demand and entrenched client relationships, contributing c.30% of James Fisher & Sons group revenue in 2024 and generating an operating margin near 14%. Predictable pricing and contract renewal cycles make them reliable cash generators with limited growth. Maintain tight service levels and lean costs; incremental tech and route efficiencies in 2024 widened the cash gap further.

Equipment rental pools (marine/subsea)

Equipment rental pools (marine/subsea) are cash cows for James Fisher and Sons, holding high share positions in niche kits while operating in a low-growth overall market. With fleets largely paid down, returns are attractive when utilization is tightly managed and downtime is minimized. Minimal marketing is required—focus is on rapid turnaround and proven reliability, refreshing only assets that materially drive uptime and day rates.

Compliance testing and calibrations

Compliance testing and calibrations are regulatory-driven, repeatable, margin-friendly services for James Fisher, with the mature market in 2024 delivering consistent demand rather than expansion. These activities are cash positive with modest capex, generating steady free cash flow. Standardizing workflows and bundling services can lift throughput and profitability.

- Regulatory-driven

- Repeatable, margin-friendly

- Mature market—stable demand (2024)

- Cash positive; modest capex; standardize and bundle to boost throughput

Planned O&M frameworks

Planned O&M frameworks deliver steady, contractually-backed cash flows for James Fisher and Sons, characterised by low growth but high predictability and low counterparty risk.

Securing a single long-term package often guarantees multi-year revenue visibility and reduces the need for continuous sales cycles; protecting SLAs and negotiating term extensions preserves this cash stream.

- Reliable margins from recurring maintenance

- Low growth, high visibility

- Win-once, earn-for-years

- Protect SLAs; extend terms to sustain cash

Ship management and services: steady recurring revenue and dependable margins

Ship management, classical marine services, equipment rental and compliance testing are cash cows for James Fisher—stable demand, recurring fees and modest capex. Group revenue £246.6m (2023); classical services ~30% of 2024 revenue with ~14% op margin; ship management mid-single-digit op margin; high utilization sustains returns.

| Segment | 2023/24 Share | Op Margin | Notes |

|---|---|---|---|

| Ship management | — | Mid-single-digit | Recurring fees |

| Classical services | ~30% | ~14% | Stable contracts |

| Equipment rental | — | Attractive when utilised | Low growth |

| Compliance testing | — | Margin-friendly | Modest capex |

Delivered as Shown

James Fisher and Sons BCG Matrix

The file you're previewing here is the exact James Fisher and Sons BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted report ready for analysis. Crafted for strategic clarity and backed by market insight, it’s ready to edit, print, or present. Buy once and download immediately—what you see is what you get.

Download Your Competitive Advantage

Quick snapshot: James Fisher and Sons’ product mix sits at an inflection point — a couple of strong performers, some steady earners, and a few units begging for a clear plan. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use Word + Excel pack that saves you hours and points straight to where capital and attention should go. Act now and turn this map into decisions you can implement tomorrow.

Stars

Subsea engineering for renewables

High-growth offshore wind and tidal work, underscored by the UK 50 GW by 2030 target, expands addressable market for James Fisher’s subsea engineering niches. The business holds a solid share in specialist subsea roles but current projects need heavy promotion and specialist placement, soaking cash in pre-construction and mobilisation. Keep winning frameworks and it can graduate into steady O&M dominance. Invest now to scale crews, assets and remote capability while the market is still sprinting.

JFD submarine rescue solutions

JFD submarine rescue is a mission-critical defense capability with few credible rivals and a global submarine fleet of roughly 430 vessels in 2024, driving demand. High-spec platforms and long-term support create strong customer stickiness, though bid cycles and readiness costs depress near-term cash flow. Protect share via readiness KPIs and regular tech refresh; as growth normalizes the unit can become a durable cash engine for James Fisher.

Offshore decommissioning services

Regulatory tailwinds and a rising backlog—UK decommissioning liability c.£60bn in 2024—push James Fisher’s offshore decommissioning into a clear growth lane. Their specialist subsea know‑how secures complex scopes, but heavy mobilization and HSE intensity pull cash forward and compress near‑term free cash flow. Keeping utilization high and standardizing methods is critical to defend share. Execution excellence now builds the pathway to future cash‑cow margins.

Specialist IRM for energy assets

Specialist IRM for energy assets is a Stars position: inspection, repair and maintenance demand rising in 2024 as fleets and fields age; strong reputation brings awards and repeat wins, but kit, skilled crews and standby costs are heavy. Securing 3–7 year programmes locks scale; pushing digital and remote inspection is essential to keep growth profitable.

- Inspection-led growth 2024

- High CAPEX: kit & standby

- Multi-year contracts 3–7 years

- Digital/remote efficiency

Marine project logistics and lifting

Marine project logistics and lifting sit in Stars as 2024 subsea and renewables build‑out fuels complex heavy‑lift moves; global offshore wind pipeline exceeds 400 GW in 2024, raising demand for coordinated lifts and logistics.

High coordination drives elevated working capital and promotional effort; flawless on‑time, on‑budget delivery preserves market share via referrals.

Systemize playbooks, standardize bids and cash conversion now to capture premium margins as headline growth normalizes.

- 2024: >400 GW offshore wind pipeline

- High working capital intensity

- Delivery reliability = organic protection

- Action: codify playbooks, optimize cash conversion

Invest in crews, assets & digital: 50 GW, £60bn, 430 subs

High-growth offshore wind/tidal (UK 50 GW by 2030) expands addressable market; specialist subsea roles are cash‑hungry in pre‑construction but can scale into O&M. JFD submarine rescue sees durable demand from ~430 global subs in 2024 but readiness ties up cash. Decommissioning (UK liability c.£60bn) and >400 GW offshore pipeline (2024) make IRM/logistics Stars—invest in crews, assets, digital and standardized bids.

| Segment | 2024 metric | Key action |

|---|---|---|

| Offshore/tidal | UK 50 GW by 2030 | Scale O&M, assets |

| Submarine rescue | ~430 subs | Protect readiness KPIs |

| Decom/IRM/logistics | UK £60bn; >400 GW pipeline | Standardize, digitize |

What is included in the product

BCG Matrix analysis of James Fisher & Sons: Stars, Cash Cows, Question Marks, Dogs with strategic investment, hold or divest guidance.

One-page BCG for James Fisher and Sons, placing each business unit in a clear quadrant to cut decision friction.

Cash Cows

Ship management contracts

Ship management contracts sit in a mature market with stable volumes and recurring fee streams; James Fisher reported group revenue of about £246.6m for 2023, with ship management a steady cash contributor. When utilization and safety metrics stay top-tier, margins hold up, supporting mid-single-digit operating margins in the segment. Low promotional needs make it retention-driven; targeted investment in tooling and process can raise cash per managed vessel.

Classical marine services (port, mooring)

Classical marine services (port, mooring) deliver steady demand and entrenched client relationships, contributing c.30% of James Fisher & Sons group revenue in 2024 and generating an operating margin near 14%. Predictable pricing and contract renewal cycles make them reliable cash generators with limited growth. Maintain tight service levels and lean costs; incremental tech and route efficiencies in 2024 widened the cash gap further.

Equipment rental pools (marine/subsea)

Equipment rental pools (marine/subsea) are cash cows for James Fisher and Sons, holding high share positions in niche kits while operating in a low-growth overall market. With fleets largely paid down, returns are attractive when utilization is tightly managed and downtime is minimized. Minimal marketing is required—focus is on rapid turnaround and proven reliability, refreshing only assets that materially drive uptime and day rates.

Compliance testing and calibrations

Compliance testing and calibrations are regulatory-driven, repeatable, margin-friendly services for James Fisher, with the mature market in 2024 delivering consistent demand rather than expansion. These activities are cash positive with modest capex, generating steady free cash flow. Standardizing workflows and bundling services can lift throughput and profitability.

- Regulatory-driven

- Repeatable, margin-friendly

- Mature market—stable demand (2024)

- Cash positive; modest capex; standardize and bundle to boost throughput

Planned O&M frameworks

Planned O&M frameworks deliver steady, contractually-backed cash flows for James Fisher and Sons, characterised by low growth but high predictability and low counterparty risk.

Securing a single long-term package often guarantees multi-year revenue visibility and reduces the need for continuous sales cycles; protecting SLAs and negotiating term extensions preserves this cash stream.

- Reliable margins from recurring maintenance

- Low growth, high visibility

- Win-once, earn-for-years

- Protect SLAs; extend terms to sustain cash

Ship management and services: steady recurring revenue and dependable margins

Ship management, classical marine services, equipment rental and compliance testing are cash cows for James Fisher—stable demand, recurring fees and modest capex. Group revenue £246.6m (2023); classical services ~30% of 2024 revenue with ~14% op margin; ship management mid-single-digit op margin; high utilization sustains returns.

| Segment | 2023/24 Share | Op Margin | Notes |

|---|---|---|---|

| Ship management | — | Mid-single-digit | Recurring fees |

| Classical services | ~30% | ~14% | Stable contracts |

| Equipment rental | — | Attractive when utilised | Low growth |

| Compliance testing | — | Margin-friendly | Modest capex |

Delivered as Shown

James Fisher and Sons BCG Matrix

The file you're previewing here is the exact James Fisher and Sons BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted report ready for analysis. Crafted for strategic clarity and backed by market insight, it’s ready to edit, print, or present. Buy once and download immediately—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

Quick snapshot: James Fisher and Sons’ product mix sits at an inflection point — a couple of strong performers, some steady earners, and a few units begging for a clear plan. Want the full picture? Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-use Word + Excel pack that saves you hours and points straight to where capital and attention should go. Act now and turn this map into decisions you can implement tomorrow.

Stars

Subsea engineering for renewables

High-growth offshore wind and tidal work, underscored by the UK 50 GW by 2030 target, expands addressable market for James Fisher’s subsea engineering niches. The business holds a solid share in specialist subsea roles but current projects need heavy promotion and specialist placement, soaking cash in pre-construction and mobilisation. Keep winning frameworks and it can graduate into steady O&M dominance. Invest now to scale crews, assets and remote capability while the market is still sprinting.

JFD submarine rescue solutions

JFD submarine rescue is a mission-critical defense capability with few credible rivals and a global submarine fleet of roughly 430 vessels in 2024, driving demand. High-spec platforms and long-term support create strong customer stickiness, though bid cycles and readiness costs depress near-term cash flow. Protect share via readiness KPIs and regular tech refresh; as growth normalizes the unit can become a durable cash engine for James Fisher.

Offshore decommissioning services

Regulatory tailwinds and a rising backlog—UK decommissioning liability c.£60bn in 2024—push James Fisher’s offshore decommissioning into a clear growth lane. Their specialist subsea know‑how secures complex scopes, but heavy mobilization and HSE intensity pull cash forward and compress near‑term free cash flow. Keeping utilization high and standardizing methods is critical to defend share. Execution excellence now builds the pathway to future cash‑cow margins.

Specialist IRM for energy assets

Specialist IRM for energy assets is a Stars position: inspection, repair and maintenance demand rising in 2024 as fleets and fields age; strong reputation brings awards and repeat wins, but kit, skilled crews and standby costs are heavy. Securing 3–7 year programmes locks scale; pushing digital and remote inspection is essential to keep growth profitable.

- Inspection-led growth 2024

- High CAPEX: kit & standby

- Multi-year contracts 3–7 years

- Digital/remote efficiency

Marine project logistics and lifting

Marine project logistics and lifting sit in Stars as 2024 subsea and renewables build‑out fuels complex heavy‑lift moves; global offshore wind pipeline exceeds 400 GW in 2024, raising demand for coordinated lifts and logistics.

High coordination drives elevated working capital and promotional effort; flawless on‑time, on‑budget delivery preserves market share via referrals.

Systemize playbooks, standardize bids and cash conversion now to capture premium margins as headline growth normalizes.

- 2024: >400 GW offshore wind pipeline

- High working capital intensity

- Delivery reliability = organic protection

- Action: codify playbooks, optimize cash conversion

Invest in crews, assets & digital: 50 GW, £60bn, 430 subs

High-growth offshore wind/tidal (UK 50 GW by 2030) expands addressable market; specialist subsea roles are cash‑hungry in pre‑construction but can scale into O&M. JFD submarine rescue sees durable demand from ~430 global subs in 2024 but readiness ties up cash. Decommissioning (UK liability c.£60bn) and >400 GW offshore pipeline (2024) make IRM/logistics Stars—invest in crews, assets, digital and standardized bids.

| Segment | 2024 metric | Key action |

|---|---|---|

| Offshore/tidal | UK 50 GW by 2030 | Scale O&M, assets |

| Submarine rescue | ~430 subs | Protect readiness KPIs |

| Decom/IRM/logistics | UK £60bn; >400 GW pipeline | Standardize, digitize |

What is included in the product

BCG Matrix analysis of James Fisher & Sons: Stars, Cash Cows, Question Marks, Dogs with strategic investment, hold or divest guidance.

One-page BCG for James Fisher and Sons, placing each business unit in a clear quadrant to cut decision friction.

Cash Cows

Ship management contracts

Ship management contracts sit in a mature market with stable volumes and recurring fee streams; James Fisher reported group revenue of about £246.6m for 2023, with ship management a steady cash contributor. When utilization and safety metrics stay top-tier, margins hold up, supporting mid-single-digit operating margins in the segment. Low promotional needs make it retention-driven; targeted investment in tooling and process can raise cash per managed vessel.

Classical marine services (port, mooring)

Classical marine services (port, mooring) deliver steady demand and entrenched client relationships, contributing c.30% of James Fisher & Sons group revenue in 2024 and generating an operating margin near 14%. Predictable pricing and contract renewal cycles make them reliable cash generators with limited growth. Maintain tight service levels and lean costs; incremental tech and route efficiencies in 2024 widened the cash gap further.

Equipment rental pools (marine/subsea)

Equipment rental pools (marine/subsea) are cash cows for James Fisher and Sons, holding high share positions in niche kits while operating in a low-growth overall market. With fleets largely paid down, returns are attractive when utilization is tightly managed and downtime is minimized. Minimal marketing is required—focus is on rapid turnaround and proven reliability, refreshing only assets that materially drive uptime and day rates.

Compliance testing and calibrations

Compliance testing and calibrations are regulatory-driven, repeatable, margin-friendly services for James Fisher, with the mature market in 2024 delivering consistent demand rather than expansion. These activities are cash positive with modest capex, generating steady free cash flow. Standardizing workflows and bundling services can lift throughput and profitability.

- Regulatory-driven

- Repeatable, margin-friendly

- Mature market—stable demand (2024)

- Cash positive; modest capex; standardize and bundle to boost throughput

Planned O&M frameworks

Planned O&M frameworks deliver steady, contractually-backed cash flows for James Fisher and Sons, characterised by low growth but high predictability and low counterparty risk.

Securing a single long-term package often guarantees multi-year revenue visibility and reduces the need for continuous sales cycles; protecting SLAs and negotiating term extensions preserves this cash stream.

- Reliable margins from recurring maintenance

- Low growth, high visibility

- Win-once, earn-for-years

- Protect SLAs; extend terms to sustain cash

Ship management and services: steady recurring revenue and dependable margins

Ship management, classical marine services, equipment rental and compliance testing are cash cows for James Fisher—stable demand, recurring fees and modest capex. Group revenue £246.6m (2023); classical services ~30% of 2024 revenue with ~14% op margin; ship management mid-single-digit op margin; high utilization sustains returns.

| Segment | 2023/24 Share | Op Margin | Notes |

|---|---|---|---|

| Ship management | — | Mid-single-digit | Recurring fees |

| Classical services | ~30% | ~14% | Stable contracts |

| Equipment rental | — | Attractive when utilised | Low growth |

| Compliance testing | — | Margin-friendly | Modest capex |

Delivered as Shown

James Fisher and Sons BCG Matrix

The file you're previewing here is the exact James Fisher and Sons BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the finished, fully formatted report ready for analysis. Crafted for strategic clarity and backed by market insight, it’s ready to edit, print, or present. Buy once and download immediately—what you see is what you get.