James Fisher and Sons PESTLE Analysis

Skip the Research. Get the Strategy.

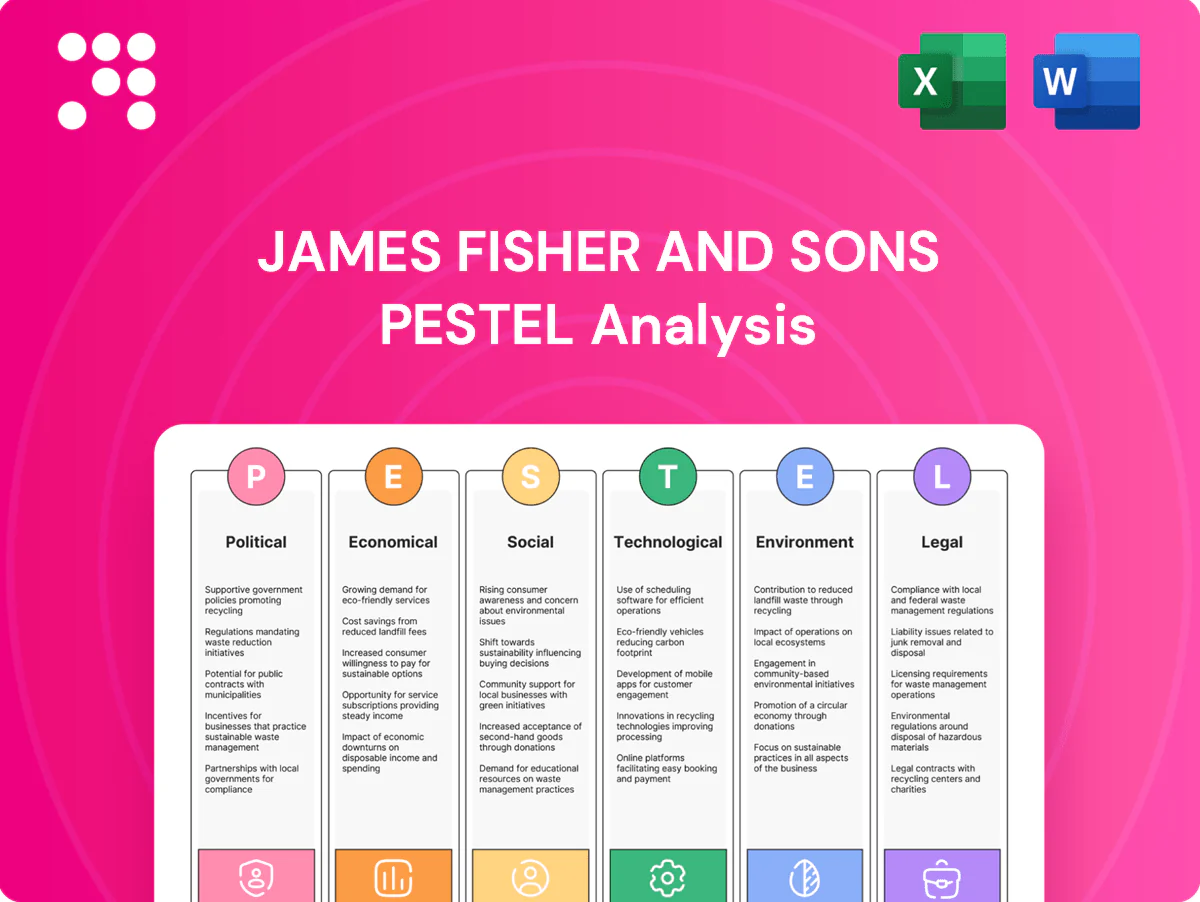

Unlock strategic advantage with our concise PESTLE Analysis of James Fisher and Sons—three to five expert-driven insights reveal how political, economic, social, technological, legal and environmental forces are reshaping its prospects. Ideal for investors and strategists, the full report delivers actionable intelligence and editable tools. Buy now for instant download and make decisions with confidence.

Political factors

Geopolitical maritime security and trade lanes

Naval tensions, piracy zones and chokepoint disruptions (Strait of Hormuz moves about 20% of seaborne oil; Suez ~12% of world seaborne trade) can reroute vessels, delay projects and raise insurance and war-risk premiums. Fisher’s ship management and subsea deployments need stable corridors for timely mobilization. Defense solutions may see counter-cyclical demand as navies expand patrols, while host-nation stability affects port and offshore access.

Energy policy and offshore licensing regimes

Hydrocarbon exploration approvals and tightening decommissioning mandates reshape oil and gas project pipelines, influencing timing and scope of subsea work. Supportive policies for offshore wind and grid interconnectors—UK target of 50 GW offshore wind by 2030—are accelerating renewable service demand. Sudden licensing pauses or fiscal regime shifts can stall specialist-vessel utilization, so Fisher must balance exposure across jurisdictions to smooth procurement cycles.

Defense budgets and procurement priorities

Government spending on mine countermeasures, subsea surveillance and maritime readiness—driven by the UK and NATO 2% GDP defence commitments and a UK defence budget of roughly £50–55bn—sustains steady project flow for James Fisher and Sons. Long procurement cycles and stringent safety records favor incumbents with proven delivery and quality. The shift toward unmanned systems and digital readiness opens adjacent service and retrofit opportunities. Budget tightening or reshoring preferences can quickly reshape competitive dynamics.

Sanctions, export controls, and cabotage rules

Sanctions continue to restrict customer eligibility, complicating supply chains and closing certain payment channels, notably under ongoing 2024/25 UK, EU and US measures targeting Russia and Iran.

Export controls constrain transfer of dual-use and defense-related technologies central to subsea and naval workflows, tightening procurement and partnering options.

Cabotage laws such as the US Jones Act restrict foreign-flag vessels on domestic routes, affecting fleet deployment and chartering flexibility.

Robust compliance capability is increasingly strategic for bid eligibility and reputation in 2024/25 contracting environments.

- Sanctions impact: customer eligibility, payments, supply chains

- Export controls: limit subsea/defense tech transfers

- Cabotage: domestic route restrictions (eg Jones Act)

- Compliance: key to bids and reputation in 2024/25

Public funding for infrastructure and decommissioning

Government-backed port upgrades, hydrogen hubs and grid reinforcement tied to the UK 50GW offshore wind and 5GW hydrogen-by-2030 targets are driving marine construction demand; OGA estimates c.£58bn of North Sea decommissioning liabilities create mandated work streams; green finance and grants lower client risk and Fisher can align capabilities to priority corridors set by policymakers.

- Policy catalysts: 50GW offshore, 5GW hydrogen (UK targets)

- Decommissioning: ~£58bn North Sea

- Finance: grants/green bonds reduce project risk

- Opportunity: align to policy corridors

Chokepoints, sanctions and UK targets push up compliance, energy and defence costs

Geopolitical chokepoints (Hormuz ~20% seaborne oil; Suez ~12% trade) and 2024/25 sanctions disrupt routes, insurance and supply chains. UK policy drives demand: 50GW offshore wind by 2030, 5GW hydrogen and ~£58bn North Sea decommissioning liabilities; defence budgets ~£50–55bn and NATO 2% GDP sustain MCM and surveillance work. Cabotage, export controls and tight procurement cycles raise compliance premiums.

| Item | 2024/25 Metric |

|---|---|

| Hormuz | ~20% oil |

| Suez | ~12% trade |

| UK offshore | 50GW by 2030 |

| Decom liabilities | ~£58bn |

| UK defence | £50–55bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect James Fisher and Sons, with data-backed trends and industry-specific examples to reveal risks and opportunities; designed for executives and investors, the analysis includes forward-looking insights and clean formatting for immediate use in plans, decks, or reports.

A concise, visually segmented PESTLE summary of James Fisher and Sons for quick inclusion in presentations or strategy packs, editable for region- or business-specific notes and ideal for aligning teams on external risks and market positioning.

Economic factors

Commodity price cycles and project FIDs

Brent averaging around $85/bbl in 2024 drove renewed FIDs for offshore oil and gas, while price troughs shift owner focus to maintenance and decommissioning. Offshore wind cadence is tied to power prices and PPA levels—recent European PPAs traded roughly €40–60/MWh, supporting new builds. Specialist vessel utilization has rebounded to about 60–75% with day rates broadly in the $20k–60k/day range, tracking these cycles.

Interest rates and capital availability

Higher interest rates (UK Bank Rate ~5.25% mid‑2025) raise hurdle returns for developers and increase vessel leasing/dayrates, prompting clients to defer projects or renegotiate timelines under tighter financing. Conversely, lower rates unlock larger offshore wind arrays and grid works. James Fisher’s refinancing terms, including its syndicated facilities, directly constrain fleet and technology investment capacity.

Global trade volume and logistics costs

Global container and bulk trade volumes drive demand for James Fisher and Sons port and logistics services; container throughput dipped during 2022–23 then rebounded, with global container trade roughly recovering to pre‑pandemic levels by 2024, while seaborne bulk trade rose modestly. Freight volatility — WCI/SCFI spot rates averaged about $1,000–1,400 per FEU in 2024 — and marine insurance premiums (up roughly 10–15% in 2023–24) raise customers’ total operating costs. Disruptions reprice spot markets for tugs, OSVs and barges, boosting margins when tight or creating idle time when volumes fall; diversification across energy, ports, defence and renewables mitigates cyclicality for James Fisher.

Labor market tightness and wage inflation

Currency fluctuations and cost pass-through

Multi-currency revenues and costs expose James Fisher and Sons earnings to FX swings; GBP/USD averaged about 1.28 in 2024, amplifying reported profit volatility. A strong dollar raises equipment import prices and increases sterling debt servicing costs for USD liabilities. Active hedging (forward contracts/options) reduces P&L volatility but incurred hedging costs in 2024, while FX-linked contract clauses improved revenue predictability.

- Multi-currency exposure: high

- GBP/USD 2024 average: ~1.28

- Hedging: lowers volatility, raises costs

- FX clauses: improve cashflow predictability

Chokepoints, sanctions and UK targets push up compliance, energy and defence costs

Brent ~85$/bbl (2024) and European PPAs €40–60/MWh underpin renewed offshore FIDs while specialist vessel utilisation ~60–75% with dayrates $20k–60k/d. UK Bank Rate ~5.25% (mid‑2025) raises financing hurdles and constrains fleet investment. GBP/USD ~1.28 and a seafarer shortfall ~147,500 (BIMCO/ICS 2025) drive FX/crew cost risk; hedging and training mitigate volatility.

| Metric | Value |

|---|---|

| Brent 2024 | ~$85/bbl |

| EU PPA | €40–60/MWh |

| Vessel util. | 60–75% |

| UK Bank Rate | ~5.25% |

| GBP/USD 2024 | ~1.28 |

| Seafarer gap 2025 | ~147,500 |

What You See Is What You Get

James Fisher and Sons PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This James Fisher and Sons PESTLE Analysis provides clear political, economic, social, technological, legal and environmental insights tailored for investors and strategists. No placeholders, no surprises—download the final file instantly after checkout.

Skip the Research. Get the Strategy.

Unlock strategic advantage with our concise PESTLE Analysis of James Fisher and Sons—three to five expert-driven insights reveal how political, economic, social, technological, legal and environmental forces are reshaping its prospects. Ideal for investors and strategists, the full report delivers actionable intelligence and editable tools. Buy now for instant download and make decisions with confidence.

Political factors

Geopolitical maritime security and trade lanes

Naval tensions, piracy zones and chokepoint disruptions (Strait of Hormuz moves about 20% of seaborne oil; Suez ~12% of world seaborne trade) can reroute vessels, delay projects and raise insurance and war-risk premiums. Fisher’s ship management and subsea deployments need stable corridors for timely mobilization. Defense solutions may see counter-cyclical demand as navies expand patrols, while host-nation stability affects port and offshore access.

Energy policy and offshore licensing regimes

Hydrocarbon exploration approvals and tightening decommissioning mandates reshape oil and gas project pipelines, influencing timing and scope of subsea work. Supportive policies for offshore wind and grid interconnectors—UK target of 50 GW offshore wind by 2030—are accelerating renewable service demand. Sudden licensing pauses or fiscal regime shifts can stall specialist-vessel utilization, so Fisher must balance exposure across jurisdictions to smooth procurement cycles.

Defense budgets and procurement priorities

Government spending on mine countermeasures, subsea surveillance and maritime readiness—driven by the UK and NATO 2% GDP defence commitments and a UK defence budget of roughly £50–55bn—sustains steady project flow for James Fisher and Sons. Long procurement cycles and stringent safety records favor incumbents with proven delivery and quality. The shift toward unmanned systems and digital readiness opens adjacent service and retrofit opportunities. Budget tightening or reshoring preferences can quickly reshape competitive dynamics.

Sanctions, export controls, and cabotage rules

Sanctions continue to restrict customer eligibility, complicating supply chains and closing certain payment channels, notably under ongoing 2024/25 UK, EU and US measures targeting Russia and Iran.

Export controls constrain transfer of dual-use and defense-related technologies central to subsea and naval workflows, tightening procurement and partnering options.

Cabotage laws such as the US Jones Act restrict foreign-flag vessels on domestic routes, affecting fleet deployment and chartering flexibility.

Robust compliance capability is increasingly strategic for bid eligibility and reputation in 2024/25 contracting environments.

- Sanctions impact: customer eligibility, payments, supply chains

- Export controls: limit subsea/defense tech transfers

- Cabotage: domestic route restrictions (eg Jones Act)

- Compliance: key to bids and reputation in 2024/25

Public funding for infrastructure and decommissioning

Government-backed port upgrades, hydrogen hubs and grid reinforcement tied to the UK 50GW offshore wind and 5GW hydrogen-by-2030 targets are driving marine construction demand; OGA estimates c.£58bn of North Sea decommissioning liabilities create mandated work streams; green finance and grants lower client risk and Fisher can align capabilities to priority corridors set by policymakers.

- Policy catalysts: 50GW offshore, 5GW hydrogen (UK targets)

- Decommissioning: ~£58bn North Sea

- Finance: grants/green bonds reduce project risk

- Opportunity: align to policy corridors

Chokepoints, sanctions and UK targets push up compliance, energy and defence costs

Geopolitical chokepoints (Hormuz ~20% seaborne oil; Suez ~12% trade) and 2024/25 sanctions disrupt routes, insurance and supply chains. UK policy drives demand: 50GW offshore wind by 2030, 5GW hydrogen and ~£58bn North Sea decommissioning liabilities; defence budgets ~£50–55bn and NATO 2% GDP sustain MCM and surveillance work. Cabotage, export controls and tight procurement cycles raise compliance premiums.

| Item | 2024/25 Metric |

|---|---|

| Hormuz | ~20% oil |

| Suez | ~12% trade |

| UK offshore | 50GW by 2030 |

| Decom liabilities | ~£58bn |

| UK defence | £50–55bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect James Fisher and Sons, with data-backed trends and industry-specific examples to reveal risks and opportunities; designed for executives and investors, the analysis includes forward-looking insights and clean formatting for immediate use in plans, decks, or reports.

A concise, visually segmented PESTLE summary of James Fisher and Sons for quick inclusion in presentations or strategy packs, editable for region- or business-specific notes and ideal for aligning teams on external risks and market positioning.

Economic factors

Commodity price cycles and project FIDs

Brent averaging around $85/bbl in 2024 drove renewed FIDs for offshore oil and gas, while price troughs shift owner focus to maintenance and decommissioning. Offshore wind cadence is tied to power prices and PPA levels—recent European PPAs traded roughly €40–60/MWh, supporting new builds. Specialist vessel utilization has rebounded to about 60–75% with day rates broadly in the $20k–60k/day range, tracking these cycles.

Interest rates and capital availability

Higher interest rates (UK Bank Rate ~5.25% mid‑2025) raise hurdle returns for developers and increase vessel leasing/dayrates, prompting clients to defer projects or renegotiate timelines under tighter financing. Conversely, lower rates unlock larger offshore wind arrays and grid works. James Fisher’s refinancing terms, including its syndicated facilities, directly constrain fleet and technology investment capacity.

Global trade volume and logistics costs

Global container and bulk trade volumes drive demand for James Fisher and Sons port and logistics services; container throughput dipped during 2022–23 then rebounded, with global container trade roughly recovering to pre‑pandemic levels by 2024, while seaborne bulk trade rose modestly. Freight volatility — WCI/SCFI spot rates averaged about $1,000–1,400 per FEU in 2024 — and marine insurance premiums (up roughly 10–15% in 2023–24) raise customers’ total operating costs. Disruptions reprice spot markets for tugs, OSVs and barges, boosting margins when tight or creating idle time when volumes fall; diversification across energy, ports, defence and renewables mitigates cyclicality for James Fisher.

Labor market tightness and wage inflation

Currency fluctuations and cost pass-through

Multi-currency revenues and costs expose James Fisher and Sons earnings to FX swings; GBP/USD averaged about 1.28 in 2024, amplifying reported profit volatility. A strong dollar raises equipment import prices and increases sterling debt servicing costs for USD liabilities. Active hedging (forward contracts/options) reduces P&L volatility but incurred hedging costs in 2024, while FX-linked contract clauses improved revenue predictability.

- Multi-currency exposure: high

- GBP/USD 2024 average: ~1.28

- Hedging: lowers volatility, raises costs

- FX clauses: improve cashflow predictability

Chokepoints, sanctions and UK targets push up compliance, energy and defence costs

Brent ~85$/bbl (2024) and European PPAs €40–60/MWh underpin renewed offshore FIDs while specialist vessel utilisation ~60–75% with dayrates $20k–60k/d. UK Bank Rate ~5.25% (mid‑2025) raises financing hurdles and constrains fleet investment. GBP/USD ~1.28 and a seafarer shortfall ~147,500 (BIMCO/ICS 2025) drive FX/crew cost risk; hedging and training mitigate volatility.

| Metric | Value |

|---|---|

| Brent 2024 | ~$85/bbl |

| EU PPA | €40–60/MWh |

| Vessel util. | 60–75% |

| UK Bank Rate | ~5.25% |

| GBP/USD 2024 | ~1.28 |

| Seafarer gap 2025 | ~147,500 |

What You See Is What You Get

James Fisher and Sons PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This James Fisher and Sons PESTLE Analysis provides clear political, economic, social, technological, legal and environmental insights tailored for investors and strategists. No placeholders, no surprises—download the final file instantly after checkout.

Description

Skip the Research. Get the Strategy.

Unlock strategic advantage with our concise PESTLE Analysis of James Fisher and Sons—three to five expert-driven insights reveal how political, economic, social, technological, legal and environmental forces are reshaping its prospects. Ideal for investors and strategists, the full report delivers actionable intelligence and editable tools. Buy now for instant download and make decisions with confidence.

Political factors

Geopolitical maritime security and trade lanes

Naval tensions, piracy zones and chokepoint disruptions (Strait of Hormuz moves about 20% of seaborne oil; Suez ~12% of world seaborne trade) can reroute vessels, delay projects and raise insurance and war-risk premiums. Fisher’s ship management and subsea deployments need stable corridors for timely mobilization. Defense solutions may see counter-cyclical demand as navies expand patrols, while host-nation stability affects port and offshore access.

Energy policy and offshore licensing regimes

Hydrocarbon exploration approvals and tightening decommissioning mandates reshape oil and gas project pipelines, influencing timing and scope of subsea work. Supportive policies for offshore wind and grid interconnectors—UK target of 50 GW offshore wind by 2030—are accelerating renewable service demand. Sudden licensing pauses or fiscal regime shifts can stall specialist-vessel utilization, so Fisher must balance exposure across jurisdictions to smooth procurement cycles.

Defense budgets and procurement priorities

Government spending on mine countermeasures, subsea surveillance and maritime readiness—driven by the UK and NATO 2% GDP defence commitments and a UK defence budget of roughly £50–55bn—sustains steady project flow for James Fisher and Sons. Long procurement cycles and stringent safety records favor incumbents with proven delivery and quality. The shift toward unmanned systems and digital readiness opens adjacent service and retrofit opportunities. Budget tightening or reshoring preferences can quickly reshape competitive dynamics.

Sanctions, export controls, and cabotage rules

Sanctions continue to restrict customer eligibility, complicating supply chains and closing certain payment channels, notably under ongoing 2024/25 UK, EU and US measures targeting Russia and Iran.

Export controls constrain transfer of dual-use and defense-related technologies central to subsea and naval workflows, tightening procurement and partnering options.

Cabotage laws such as the US Jones Act restrict foreign-flag vessels on domestic routes, affecting fleet deployment and chartering flexibility.

Robust compliance capability is increasingly strategic for bid eligibility and reputation in 2024/25 contracting environments.

- Sanctions impact: customer eligibility, payments, supply chains

- Export controls: limit subsea/defense tech transfers

- Cabotage: domestic route restrictions (eg Jones Act)

- Compliance: key to bids and reputation in 2024/25

Public funding for infrastructure and decommissioning

Government-backed port upgrades, hydrogen hubs and grid reinforcement tied to the UK 50GW offshore wind and 5GW hydrogen-by-2030 targets are driving marine construction demand; OGA estimates c.£58bn of North Sea decommissioning liabilities create mandated work streams; green finance and grants lower client risk and Fisher can align capabilities to priority corridors set by policymakers.

- Policy catalysts: 50GW offshore, 5GW hydrogen (UK targets)

- Decommissioning: ~£58bn North Sea

- Finance: grants/green bonds reduce project risk

- Opportunity: align to policy corridors

Chokepoints, sanctions and UK targets push up compliance, energy and defence costs

Geopolitical chokepoints (Hormuz ~20% seaborne oil; Suez ~12% trade) and 2024/25 sanctions disrupt routes, insurance and supply chains. UK policy drives demand: 50GW offshore wind by 2030, 5GW hydrogen and ~£58bn North Sea decommissioning liabilities; defence budgets ~£50–55bn and NATO 2% GDP sustain MCM and surveillance work. Cabotage, export controls and tight procurement cycles raise compliance premiums.

| Item | 2024/25 Metric |

|---|---|

| Hormuz | ~20% oil |

| Suez | ~12% trade |

| UK offshore | 50GW by 2030 |

| Decom liabilities | ~£58bn |

| UK defence | £50–55bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect James Fisher and Sons, with data-backed trends and industry-specific examples to reveal risks and opportunities; designed for executives and investors, the analysis includes forward-looking insights and clean formatting for immediate use in plans, decks, or reports.

A concise, visually segmented PESTLE summary of James Fisher and Sons for quick inclusion in presentations or strategy packs, editable for region- or business-specific notes and ideal for aligning teams on external risks and market positioning.

Economic factors

Commodity price cycles and project FIDs

Brent averaging around $85/bbl in 2024 drove renewed FIDs for offshore oil and gas, while price troughs shift owner focus to maintenance and decommissioning. Offshore wind cadence is tied to power prices and PPA levels—recent European PPAs traded roughly €40–60/MWh, supporting new builds. Specialist vessel utilization has rebounded to about 60–75% with day rates broadly in the $20k–60k/day range, tracking these cycles.

Interest rates and capital availability

Higher interest rates (UK Bank Rate ~5.25% mid‑2025) raise hurdle returns for developers and increase vessel leasing/dayrates, prompting clients to defer projects or renegotiate timelines under tighter financing. Conversely, lower rates unlock larger offshore wind arrays and grid works. James Fisher’s refinancing terms, including its syndicated facilities, directly constrain fleet and technology investment capacity.

Global trade volume and logistics costs

Global container and bulk trade volumes drive demand for James Fisher and Sons port and logistics services; container throughput dipped during 2022–23 then rebounded, with global container trade roughly recovering to pre‑pandemic levels by 2024, while seaborne bulk trade rose modestly. Freight volatility — WCI/SCFI spot rates averaged about $1,000–1,400 per FEU in 2024 — and marine insurance premiums (up roughly 10–15% in 2023–24) raise customers’ total operating costs. Disruptions reprice spot markets for tugs, OSVs and barges, boosting margins when tight or creating idle time when volumes fall; diversification across energy, ports, defence and renewables mitigates cyclicality for James Fisher.

Labor market tightness and wage inflation

Currency fluctuations and cost pass-through

Multi-currency revenues and costs expose James Fisher and Sons earnings to FX swings; GBP/USD averaged about 1.28 in 2024, amplifying reported profit volatility. A strong dollar raises equipment import prices and increases sterling debt servicing costs for USD liabilities. Active hedging (forward contracts/options) reduces P&L volatility but incurred hedging costs in 2024, while FX-linked contract clauses improved revenue predictability.

- Multi-currency exposure: high

- GBP/USD 2024 average: ~1.28

- Hedging: lowers volatility, raises costs

- FX clauses: improve cashflow predictability

Chokepoints, sanctions and UK targets push up compliance, energy and defence costs

Brent ~85$/bbl (2024) and European PPAs €40–60/MWh underpin renewed offshore FIDs while specialist vessel utilisation ~60–75% with dayrates $20k–60k/d. UK Bank Rate ~5.25% (mid‑2025) raises financing hurdles and constrains fleet investment. GBP/USD ~1.28 and a seafarer shortfall ~147,500 (BIMCO/ICS 2025) drive FX/crew cost risk; hedging and training mitigate volatility.

| Metric | Value |

|---|---|

| Brent 2024 | ~$85/bbl |

| EU PPA | €40–60/MWh |

| Vessel util. | 60–75% |

| UK Bank Rate | ~5.25% |

| GBP/USD 2024 | ~1.28 |

| Seafarer gap 2025 | ~147,500 |

What You See Is What You Get

James Fisher and Sons PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This James Fisher and Sons PESTLE Analysis provides clear political, economic, social, technological, legal and environmental insights tailored for investors and strategists. No placeholders, no surprises—download the final file instantly after checkout.