James Hardie Industries SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

James Hardie’s SWOT highlights a strong global brand and product innovation in fiber cement, balanced by exposure to raw material costs and cyclical housing markets; opportunities include sustainable building trends and geographic expansion, while competition and regulatory risks threaten margin stability. Discover the complete picture with our full SWOT analysis—purchase the professionally formatted, editable report to plan, pitch, or invest with confidence.

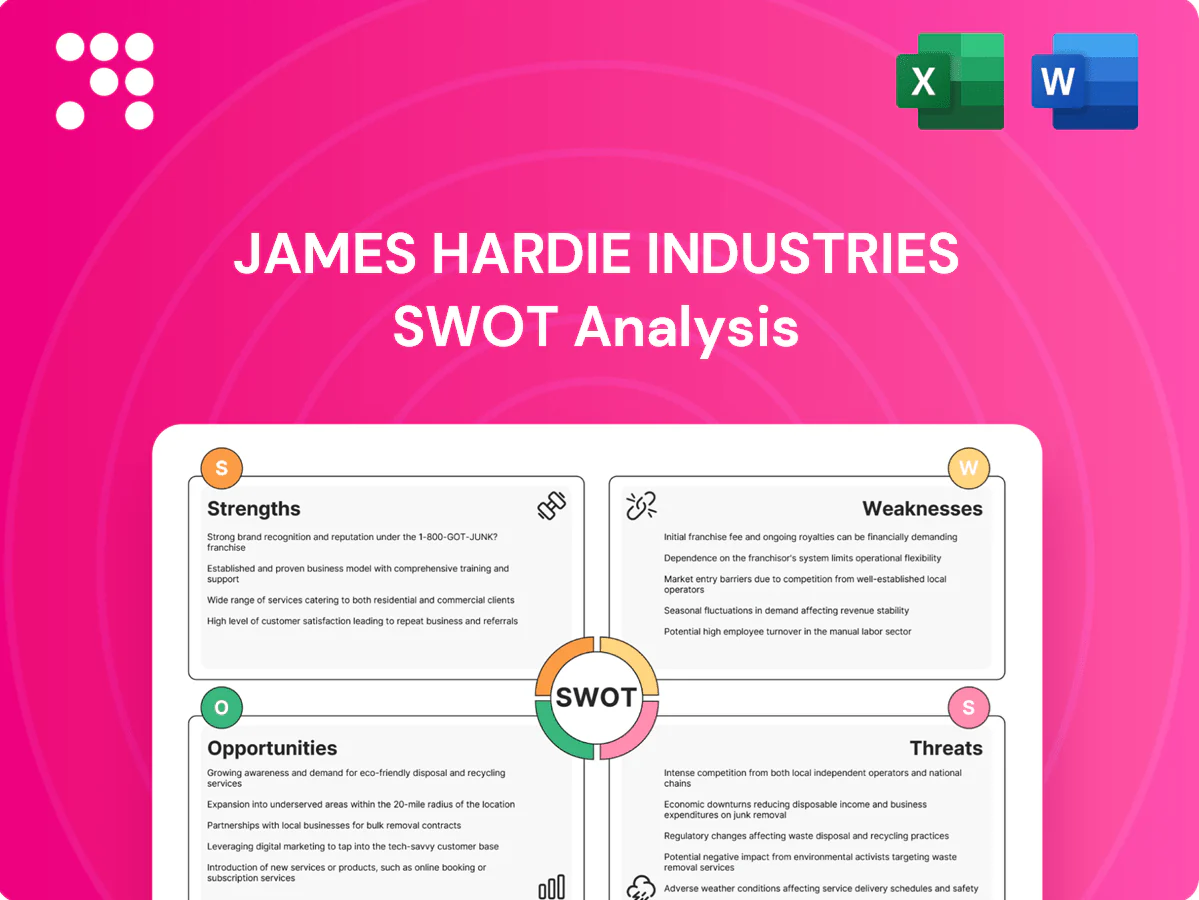

Strengths

Category leadership in fiber cement

As the global leader in fiber cement, James Hardie reported FY2024 net sales of about US$3.9 billion, giving it scale, brand recognition and pricing power. Leadership secures preferred-spec status with builders, architects and code officials, driving consistent demand. Dominant scale improves plant utilization and procurement leverage, underpinning stronger margins and resilience across cycles.

Durable, low-maintenance value proposition

Fiber cement’s inherent fire, rot and pest resistance matches rising homeowner demand for long-life, low-maintenance claddings, with typical service lives of 50+ years. Its superior performance versus wood and vinyl in harsh climates underpins James Hardie’s premium positioning. That durability drives market share gains across new-build and repair/remodel segments. It also supports a favorable total-cost-of-ownership case for homeowners.

Broad product portfolio and systems

James Hardie’s integrated siding, trim, panels, backer board and accessories create a systems offering that drives cross-selling and raises wallet share per project; the approach supports the company’s scale, reflected in FY2024 net sales of about $3.3 billion. Systems simplify procurement for contractors and improve installation consistency and perceived quality. This breadth increases switching costs for distribution channels and installers, reinforcing customer retention.

Geographic diversification and distribution

James Hardies operations across North America, ANZ and Europe spread end-market risk and capture regional construction cycles while selling through major big-box partners like The Home Depot and Lowe’s plus pro dealers and distributor networks. Its HardiePro contractor programs and training drive loyalty and repeat purchases among builders and contractors. Local manufacturing footprint in each region cuts freight costs and shortens lead times, supporting faster project delivery.

- Regional presence: North America, ANZ, Europe

- Channel reach: Home Depot, Lowe’s, pro dealers, distributors

- Pro support: HardiePro training and loyalty programs

- Operational edge: regional plants reduce freight and lead times

R&D and brand-driven marketing

- FY2024 sales: $3.8 billion

- Professional + DIY marketing targets: pros and homeowners

- Technical support reduces install errors and callbacks

Global fiber-cement leader: US$3.9bn sales, 50+ years life, regional scale & premium pricing

Global fiber-cement leader with FY2024 net sales US$3.9bn, delivering scale, pricing power and preferred-spec status with builders and code officials. Durable product (50+ year service life) supports premium pricing and total-cost-of-ownership advantages versus wood/vinyl. Integrated systems, HardiePro programs and regional plants (NA, ANZ, EU) boost margins, reduce freight and secure distribution via Home Depot, Lowe’s and pro dealers.

| Metric | Value |

|---|---|

| FY2024 net sales | US$3.9bn |

| Service life | 50+ years |

| Regions | North America, ANZ, Europe |

| Key channels | Home Depot, Lowe’s, pro dealers |

What is included in the product

Provides a clear SWOT framework that maps James Hardie Industries’s internal strengths and weaknesses alongside external opportunities and threats, highlighting competitive advantages, operational gaps, growth drivers, and market risks shaping its strategic outlook.

Relieves strategic uncertainty by providing a concise James Hardie Industries SWOT matrix for fast alignment on product, market and regulatory risks.

Weaknesses

Exposure to housing cycles

Revenue is closely tied to new construction and R&R activity, both highly sensitive to interest rates and consumer confidence; FY2024 net sales were about US$3.79bn, exposing cash flow to housing-cycle swings. Sharp downturns can compress volumes and pricing, while fixed-cost manufacturing magnifies margin swings in slowdowns. This cyclicality complicates capacity planning and inventory management, raising working-capital volatility.

Material and energy cost sensitivity

Inputs such as pulp, cement and energy are highly volatile, exposing James Hardie to raw-material and fuel-price swings that can suddenly raise production costs. Price-cost lag during inflationary episodes can compress margins before selling prices adjust. Hedging programs and customer surcharges only partially mitigate this volatility and cannot fully eliminate margin exposure. Frequent repricing can create channel friction and risk of share loss to lower-priced competitors.

Product concentration in fiber cement

James Hardie's dependence on fiber cement—which generated roughly 80% of fiscal 2024 net sales (about $3.19 billion)—concentrates technology and reputation risk. Failures in a high-profile product line could have outsized earnings and share-price impact. Diversification into fiber gypsum and adjacencies remains smaller scale, limiting optionality versus multi-material peers.

Capital-intensive manufacturing footprint

James Hardies capital‑intensive manufacturing footprint demands continuous capex for capacity, maintenance and environmental compliance, creating high fixed costs that reduce flexibility during demand shocks; ramp‑ups and commissioning add execution risk and plant shutdowns or bottlenecks can materially disrupt service levels and pricing.

- High ongoing capex

- Elevated fixed cost leverage

- Ramp‑up execution risk

- Shutdowns = service/pricing disruption

Installation complexity versus substitutes

Fiber cement is heavier and more labor-intensive than vinyl or some engineered wood, increasing installation time and costs; installer skill gaps can cause callbacks and perceived quality issues, and training requirements raise channel partner expenses. In tight labor markets contractors often choose faster, easier-to-install alternatives, squeezing James Hardie on adoption and margin.

- Installation weight and labor intensity

- Installer skill gaps -> callbacks/quality perception

- Training adds cost/time for channel partners

- Contractors favor quicker substitutes in tight labor markets

Housing cycles drive volatility; FY2024 US$3.79bn, fiber cement ~80%

Revenue and cash flow track housing cycles; FY2024 net sales US$3.79bn, exposing results to rate-driven volatility. Inputs (pulp, cement, energy) are volatile, creating margin risk as hedges/surcharges only partially mitigate. Product concentration: fiber cement ~80% of FY2024 sales (~US$3.19bn). Capital‑intensive manufacturing raises fixed costs, capex and execution risk.

| Metric | Value |

|---|---|

| FY2024 net sales | US$3.79bn |

| Fiber cement share | ~80% (~US$3.19bn) |

Full Version Awaits

James Hardie Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full James Hardie Industries SWOT report you'll get; buy to unlock the complete, editable version with full strengths, weaknesses, opportunities and threats.

Elevate Your Analysis with the Complete SWOT Report

James Hardie’s SWOT highlights a strong global brand and product innovation in fiber cement, balanced by exposure to raw material costs and cyclical housing markets; opportunities include sustainable building trends and geographic expansion, while competition and regulatory risks threaten margin stability. Discover the complete picture with our full SWOT analysis—purchase the professionally formatted, editable report to plan, pitch, or invest with confidence.

Strengths

Category leadership in fiber cement

As the global leader in fiber cement, James Hardie reported FY2024 net sales of about US$3.9 billion, giving it scale, brand recognition and pricing power. Leadership secures preferred-spec status with builders, architects and code officials, driving consistent demand. Dominant scale improves plant utilization and procurement leverage, underpinning stronger margins and resilience across cycles.

Durable, low-maintenance value proposition

Fiber cement’s inherent fire, rot and pest resistance matches rising homeowner demand for long-life, low-maintenance claddings, with typical service lives of 50+ years. Its superior performance versus wood and vinyl in harsh climates underpins James Hardie’s premium positioning. That durability drives market share gains across new-build and repair/remodel segments. It also supports a favorable total-cost-of-ownership case for homeowners.

Broad product portfolio and systems

James Hardie’s integrated siding, trim, panels, backer board and accessories create a systems offering that drives cross-selling and raises wallet share per project; the approach supports the company’s scale, reflected in FY2024 net sales of about $3.3 billion. Systems simplify procurement for contractors and improve installation consistency and perceived quality. This breadth increases switching costs for distribution channels and installers, reinforcing customer retention.

Geographic diversification and distribution

James Hardies operations across North America, ANZ and Europe spread end-market risk and capture regional construction cycles while selling through major big-box partners like The Home Depot and Lowe’s plus pro dealers and distributor networks. Its HardiePro contractor programs and training drive loyalty and repeat purchases among builders and contractors. Local manufacturing footprint in each region cuts freight costs and shortens lead times, supporting faster project delivery.

- Regional presence: North America, ANZ, Europe

- Channel reach: Home Depot, Lowe’s, pro dealers, distributors

- Pro support: HardiePro training and loyalty programs

- Operational edge: regional plants reduce freight and lead times

R&D and brand-driven marketing

- FY2024 sales: $3.8 billion

- Professional + DIY marketing targets: pros and homeowners

- Technical support reduces install errors and callbacks

Global fiber-cement leader: US$3.9bn sales, 50+ years life, regional scale & premium pricing

Global fiber-cement leader with FY2024 net sales US$3.9bn, delivering scale, pricing power and preferred-spec status with builders and code officials. Durable product (50+ year service life) supports premium pricing and total-cost-of-ownership advantages versus wood/vinyl. Integrated systems, HardiePro programs and regional plants (NA, ANZ, EU) boost margins, reduce freight and secure distribution via Home Depot, Lowe’s and pro dealers.

| Metric | Value |

|---|---|

| FY2024 net sales | US$3.9bn |

| Service life | 50+ years |

| Regions | North America, ANZ, Europe |

| Key channels | Home Depot, Lowe’s, pro dealers |

What is included in the product

Provides a clear SWOT framework that maps James Hardie Industries’s internal strengths and weaknesses alongside external opportunities and threats, highlighting competitive advantages, operational gaps, growth drivers, and market risks shaping its strategic outlook.

Relieves strategic uncertainty by providing a concise James Hardie Industries SWOT matrix for fast alignment on product, market and regulatory risks.

Weaknesses

Exposure to housing cycles

Revenue is closely tied to new construction and R&R activity, both highly sensitive to interest rates and consumer confidence; FY2024 net sales were about US$3.79bn, exposing cash flow to housing-cycle swings. Sharp downturns can compress volumes and pricing, while fixed-cost manufacturing magnifies margin swings in slowdowns. This cyclicality complicates capacity planning and inventory management, raising working-capital volatility.

Material and energy cost sensitivity

Inputs such as pulp, cement and energy are highly volatile, exposing James Hardie to raw-material and fuel-price swings that can suddenly raise production costs. Price-cost lag during inflationary episodes can compress margins before selling prices adjust. Hedging programs and customer surcharges only partially mitigate this volatility and cannot fully eliminate margin exposure. Frequent repricing can create channel friction and risk of share loss to lower-priced competitors.

Product concentration in fiber cement

James Hardie's dependence on fiber cement—which generated roughly 80% of fiscal 2024 net sales (about $3.19 billion)—concentrates technology and reputation risk. Failures in a high-profile product line could have outsized earnings and share-price impact. Diversification into fiber gypsum and adjacencies remains smaller scale, limiting optionality versus multi-material peers.

Capital-intensive manufacturing footprint

James Hardies capital‑intensive manufacturing footprint demands continuous capex for capacity, maintenance and environmental compliance, creating high fixed costs that reduce flexibility during demand shocks; ramp‑ups and commissioning add execution risk and plant shutdowns or bottlenecks can materially disrupt service levels and pricing.

- High ongoing capex

- Elevated fixed cost leverage

- Ramp‑up execution risk

- Shutdowns = service/pricing disruption

Installation complexity versus substitutes

Fiber cement is heavier and more labor-intensive than vinyl or some engineered wood, increasing installation time and costs; installer skill gaps can cause callbacks and perceived quality issues, and training requirements raise channel partner expenses. In tight labor markets contractors often choose faster, easier-to-install alternatives, squeezing James Hardie on adoption and margin.

- Installation weight and labor intensity

- Installer skill gaps -> callbacks/quality perception

- Training adds cost/time for channel partners

- Contractors favor quicker substitutes in tight labor markets

Housing cycles drive volatility; FY2024 US$3.79bn, fiber cement ~80%

Revenue and cash flow track housing cycles; FY2024 net sales US$3.79bn, exposing results to rate-driven volatility. Inputs (pulp, cement, energy) are volatile, creating margin risk as hedges/surcharges only partially mitigate. Product concentration: fiber cement ~80% of FY2024 sales (~US$3.19bn). Capital‑intensive manufacturing raises fixed costs, capex and execution risk.

| Metric | Value |

|---|---|

| FY2024 net sales | US$3.79bn |

| Fiber cement share | ~80% (~US$3.19bn) |

Full Version Awaits

James Hardie Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full James Hardie Industries SWOT report you'll get; buy to unlock the complete, editable version with full strengths, weaknesses, opportunities and threats.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

James Hardie’s SWOT highlights a strong global brand and product innovation in fiber cement, balanced by exposure to raw material costs and cyclical housing markets; opportunities include sustainable building trends and geographic expansion, while competition and regulatory risks threaten margin stability. Discover the complete picture with our full SWOT analysis—purchase the professionally formatted, editable report to plan, pitch, or invest with confidence.

Strengths

Category leadership in fiber cement

As the global leader in fiber cement, James Hardie reported FY2024 net sales of about US$3.9 billion, giving it scale, brand recognition and pricing power. Leadership secures preferred-spec status with builders, architects and code officials, driving consistent demand. Dominant scale improves plant utilization and procurement leverage, underpinning stronger margins and resilience across cycles.

Durable, low-maintenance value proposition

Fiber cement’s inherent fire, rot and pest resistance matches rising homeowner demand for long-life, low-maintenance claddings, with typical service lives of 50+ years. Its superior performance versus wood and vinyl in harsh climates underpins James Hardie’s premium positioning. That durability drives market share gains across new-build and repair/remodel segments. It also supports a favorable total-cost-of-ownership case for homeowners.

Broad product portfolio and systems

James Hardie’s integrated siding, trim, panels, backer board and accessories create a systems offering that drives cross-selling and raises wallet share per project; the approach supports the company’s scale, reflected in FY2024 net sales of about $3.3 billion. Systems simplify procurement for contractors and improve installation consistency and perceived quality. This breadth increases switching costs for distribution channels and installers, reinforcing customer retention.

Geographic diversification and distribution

James Hardies operations across North America, ANZ and Europe spread end-market risk and capture regional construction cycles while selling through major big-box partners like The Home Depot and Lowe’s plus pro dealers and distributor networks. Its HardiePro contractor programs and training drive loyalty and repeat purchases among builders and contractors. Local manufacturing footprint in each region cuts freight costs and shortens lead times, supporting faster project delivery.

- Regional presence: North America, ANZ, Europe

- Channel reach: Home Depot, Lowe’s, pro dealers, distributors

- Pro support: HardiePro training and loyalty programs

- Operational edge: regional plants reduce freight and lead times

R&D and brand-driven marketing

- FY2024 sales: $3.8 billion

- Professional + DIY marketing targets: pros and homeowners

- Technical support reduces install errors and callbacks

Global fiber-cement leader: US$3.9bn sales, 50+ years life, regional scale & premium pricing

Global fiber-cement leader with FY2024 net sales US$3.9bn, delivering scale, pricing power and preferred-spec status with builders and code officials. Durable product (50+ year service life) supports premium pricing and total-cost-of-ownership advantages versus wood/vinyl. Integrated systems, HardiePro programs and regional plants (NA, ANZ, EU) boost margins, reduce freight and secure distribution via Home Depot, Lowe’s and pro dealers.

| Metric | Value |

|---|---|

| FY2024 net sales | US$3.9bn |

| Service life | 50+ years |

| Regions | North America, ANZ, Europe |

| Key channels | Home Depot, Lowe’s, pro dealers |

What is included in the product

Provides a clear SWOT framework that maps James Hardie Industries’s internal strengths and weaknesses alongside external opportunities and threats, highlighting competitive advantages, operational gaps, growth drivers, and market risks shaping its strategic outlook.

Relieves strategic uncertainty by providing a concise James Hardie Industries SWOT matrix for fast alignment on product, market and regulatory risks.

Weaknesses

Exposure to housing cycles

Revenue is closely tied to new construction and R&R activity, both highly sensitive to interest rates and consumer confidence; FY2024 net sales were about US$3.79bn, exposing cash flow to housing-cycle swings. Sharp downturns can compress volumes and pricing, while fixed-cost manufacturing magnifies margin swings in slowdowns. This cyclicality complicates capacity planning and inventory management, raising working-capital volatility.

Material and energy cost sensitivity

Inputs such as pulp, cement and energy are highly volatile, exposing James Hardie to raw-material and fuel-price swings that can suddenly raise production costs. Price-cost lag during inflationary episodes can compress margins before selling prices adjust. Hedging programs and customer surcharges only partially mitigate this volatility and cannot fully eliminate margin exposure. Frequent repricing can create channel friction and risk of share loss to lower-priced competitors.

Product concentration in fiber cement

James Hardie's dependence on fiber cement—which generated roughly 80% of fiscal 2024 net sales (about $3.19 billion)—concentrates technology and reputation risk. Failures in a high-profile product line could have outsized earnings and share-price impact. Diversification into fiber gypsum and adjacencies remains smaller scale, limiting optionality versus multi-material peers.

Capital-intensive manufacturing footprint

James Hardies capital‑intensive manufacturing footprint demands continuous capex for capacity, maintenance and environmental compliance, creating high fixed costs that reduce flexibility during demand shocks; ramp‑ups and commissioning add execution risk and plant shutdowns or bottlenecks can materially disrupt service levels and pricing.

- High ongoing capex

- Elevated fixed cost leverage

- Ramp‑up execution risk

- Shutdowns = service/pricing disruption

Installation complexity versus substitutes

Fiber cement is heavier and more labor-intensive than vinyl or some engineered wood, increasing installation time and costs; installer skill gaps can cause callbacks and perceived quality issues, and training requirements raise channel partner expenses. In tight labor markets contractors often choose faster, easier-to-install alternatives, squeezing James Hardie on adoption and margin.

- Installation weight and labor intensity

- Installer skill gaps -> callbacks/quality perception

- Training adds cost/time for channel partners

- Contractors favor quicker substitutes in tight labor markets

Housing cycles drive volatility; FY2024 US$3.79bn, fiber cement ~80%

Revenue and cash flow track housing cycles; FY2024 net sales US$3.79bn, exposing results to rate-driven volatility. Inputs (pulp, cement, energy) are volatile, creating margin risk as hedges/surcharges only partially mitigate. Product concentration: fiber cement ~80% of FY2024 sales (~US$3.19bn). Capital‑intensive manufacturing raises fixed costs, capex and execution risk.

| Metric | Value |

|---|---|

| FY2024 net sales | US$3.79bn |

| Fiber cement share | ~80% (~US$3.19bn) |

Full Version Awaits

James Hardie Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full James Hardie Industries SWOT report you'll get; buy to unlock the complete, editable version with full strengths, weaknesses, opportunities and threats.