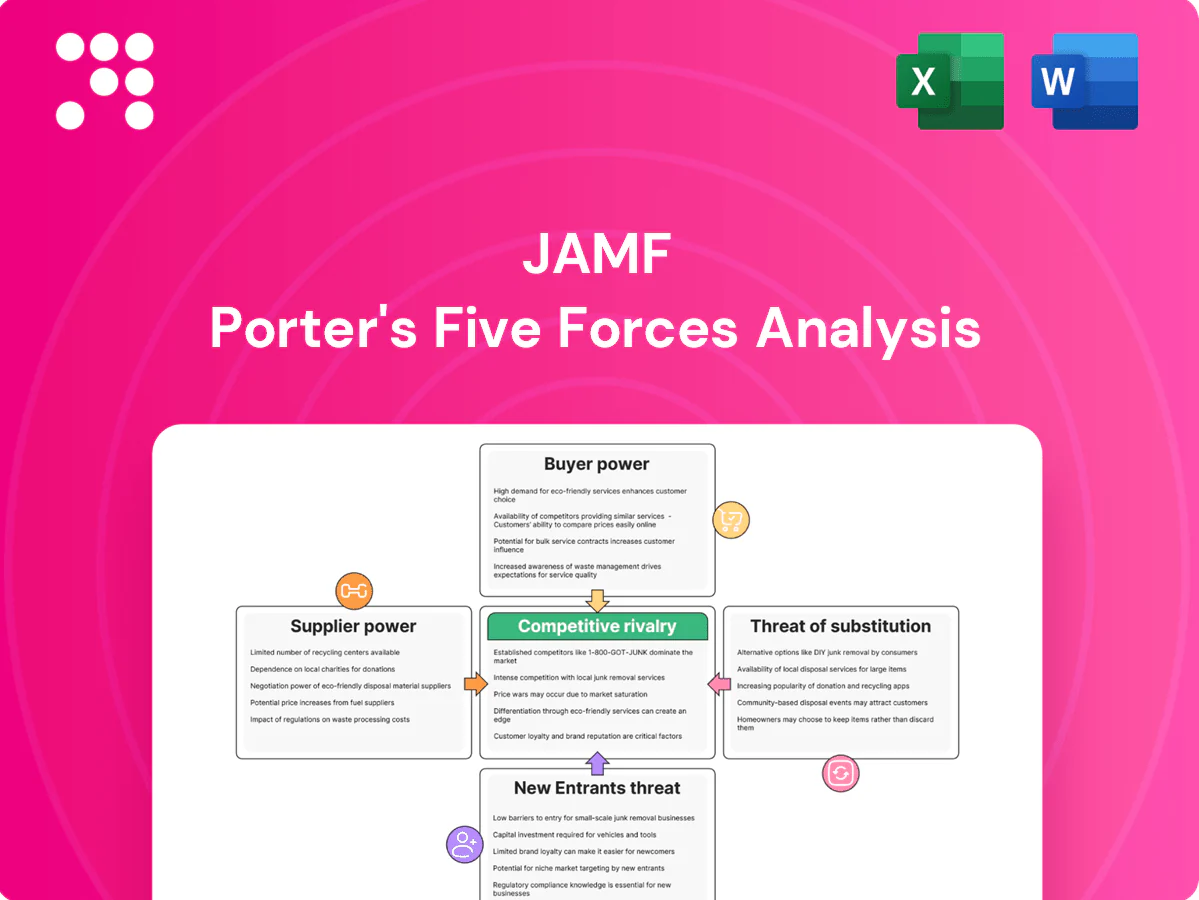

Jamf Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Jamf faces moderate supplier power, intense buyer expectations, and evolving substitute and entrant threats that shape its competitive dynamics across device management and security. This brief snapshot highlights key pressures but only scratches the surface of market intensity, strategic levers, and growth risks. Unlock the full Porter's Five Forces Analysis to explore Jamf’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Apple MDM frameworks

Jamf’s platform depends heavily on Apple MDM protocols, APNs and proprietary APIs, giving Apple outsized leverage over product roadmap and timing; Apple’s ecosystem totaled over 2 billion active devices by 2024, concentrating supplier power. Policy shifts or API deprecations can force costly rework and limit differentiation, while certification and ecosystem rules add measurable compliance overhead and time-to-market risk.

Cloud infrastructure and scalability vendors

Jamf relies on hyperscalers and CDNs for uptime, performance and global reach—top three cloud providers held about 66% market share in 2024 (AWS 32%, Microsoft 23%, Google 11%, Synergy Research Group 2024)—so pricing shifts or reserved-capacity limits can squeeze margins. Tooling and data-service lock-in raises switching costs, and multi-cloud approaches reduce but do not eliminate supplier power.

Security and identity integrations

Integration with IdPs, EDR and SIEM vendors like Okta, Microsoft and CrowdStrike is mission-critical; Jamf listed 100+ identity and security integrations in 2024, making partner changes material to UX and feature timing. API or roadmap shifts can delay rollouts and raise support costs. Co-marketing and certification programs often require fees or engineering commitments, giving integration partners moderate bargaining power.

Apple hardware and OS release cadence

Apple’s annual OS cadence (iOS 18 in Sept 2024) plus interim security patches and WWDC betas create rushed compatibility windows; early access helps but unexpected breaking changes shift development and support costs onto Jamf, while customers demand day-zero support, increasing operational pressure and reinforcing timing-asymmetry supplier power.

- Annual major release: Sept (iOS 18, 2024)

- WWDC betas: June

- Day-zero support expected by enterprises

- Breaking changes transfer costs to Jamf

Specialized engineering talent supply

Experienced Apple enterprise engineers are relatively scarce, pushing labor costs higher and contributing to Jamf's R&D spend pressure; Jamf reported revenue of $474 million in FY2024, amplifying the need to control margin impacts from talent costs.

Competition with rivals and Big Tech for macOS/iOS engineers gives the labor market supplier-like power, increasing turnover and concentration of knowledge as operational risks that can slow delivery.

Retention challenges and hiring competition in 2024 have the potential to inflate R&D expense and delay product timelines, affecting time-to-market for enterprise features.

- Scarcity: experienced Apple engineers limited, raising wages and hiring costs

- Competition: Big Tech and rivals intensify talent bidding

- Risk: retention and knowledge concentration threaten delivery

- Financial: FY2024 revenue ~$474M heightens sensitivity to rising R&D/headcount costs

Endpoint security squeezed by Apple 2B, hyperscalers 66%

Jamf faces high supplier power from Apple (2 billion devices by 2024) and annual OS cadence (iOS 18, Sept 2024), forcing rapid compatibility work. Top-three cloud providers held ~66% share in 2024 (AWS 32%, Microsoft 23%, Google 11%), raising infrastructure exposure. Integrations (100+ IdP/EDR/SIEM) and FY2024 revenue $474M intensify margin sensitivity to supplier cost shifts.

| Metric | Value |

|---|---|

| Apple ecosystem | ~2.0B devices (2024) |

| Hyperscaler share | AWS 32% / MS 23% / GCP 11% (2024) |

| Integrations | 100+ (2024) |

| Revenue | $474M FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis of Jamf that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, and provides strategic commentary and industry data to inform investors, executives, and academics.

A concise one-sheet Porter's Five Forces for Jamf that surfaces key competitive pressures and actionable relief strategies—perfect for quick decision-making and pitch decks. Customize force levels with your data or toggle scenarios to illustrate relief from pricing, supplier dependency, or emerging entrants.

Customers Bargaining Power

Large enterprise and EDU procurement

Enterprises and school districts buy Jamf at scale via RFPs, extracting pricing leverage through volume discounts and multi‑year deals; in 2024 Jamf served roughly 70,000 customers, reinforcing institutional buying power. Compliance and security mandates (HIPAA, FERPA, NIST frameworks) add negotiation levers and service requirements. Buyer power is high for large accounts and moderate for SMBs.

Visible alternatives and trialability

Competing Apple MDMs and UEM suites are easy to evaluate via 30–90 day trials and pilots, enabling side-by-side comparisons. Feature parity in core MDM functions among leaders narrows differentiation and strengthens buyer leverage. Public pricing and transparent packaging accelerate vendor comparisons, and switching decisions often hinge on total cost of ownership and support quality, cited by roughly half of enterprise buyers.

Switching costs are meaningful but manageable

Device enrollment, policy migration and user impact create tangible friction that tempers buyer power, but Apple reported over 1.5 billion active devices in 2024, meaning standardized Apple MDM protocols and broad tooling reduce barriers to switch. Migration tools and Jamf professional services can shorten cutover timelines and preserve configurations, enabling a credible threat of switch. Net effect: moderate switching costs.

Bundling pressure from platform suites

Microsoft (FY2024 revenue $211.91B) and VMware (FY2024 revenue $12.88B) can fold Apple management into larger UEM/security suites, and Ivanti pursues similar deals, creating bundling pressure that can compress Jamf pricing or displace its point solutions; buyers wield bundles as negotiation leverage and CFOs push vendor rationalization.

- bundling: major platform suites include Apple management

- rationalization: CFOs favor fewer vendors

- pricing: bundle pressure can force Jamf discounts

- leverage: buyers use bundles to negotiate

Outcome-based expectations

Customers now demand measurable security posture, compliance, and automation outcomes from Jamf, using SLAs, zero-day support, and integrations to force higher service levels.

Poor performance quickly triggers escalation or churn, increasing post-sale buyer influence and turning support metrics into renewal determinants.

- Outcome-driven SLAs

- Zero-day support as leverage

- Integrations required for compliance

- Support performance tied to retention

Large buyers extract discounts; feature parity and bundling compress pricing

Large buyers hold high leverage—Jamf served ~70,000 customers in 2024, extracting volume and multi‑year discounts; SMB power is moderate. Feature parity across MDM/UEM, 1.5B Apple devices (2024) and trial pilots reduce differentiation and strengthen buyer negotiation. Bundling by Microsoft ($211.91B FY2024) and VMware ($12.88B FY2024) compresses pricing; switching costs remain moderate.

| Metric | 2024 |

|---|---|

| Jamf customers | ~70,000 |

| Apple active devices | 1.5B |

| Microsoft revenue | $211.91B |

| VMware revenue | $12.88B |

Full Version Awaits

Jamf Porter's Five Forces Analysis

This Jamf Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—fully formatted and ready for immediate use. No mockups or placeholders are included. Once you complete payment, you’ll get instant access to this identical file. Use it as-is for decision-making, presentations, or reporting.

Don't Miss the Bigger Picture

Jamf faces moderate supplier power, intense buyer expectations, and evolving substitute and entrant threats that shape its competitive dynamics across device management and security. This brief snapshot highlights key pressures but only scratches the surface of market intensity, strategic levers, and growth risks. Unlock the full Porter's Five Forces Analysis to explore Jamf’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Apple MDM frameworks

Jamf’s platform depends heavily on Apple MDM protocols, APNs and proprietary APIs, giving Apple outsized leverage over product roadmap and timing; Apple’s ecosystem totaled over 2 billion active devices by 2024, concentrating supplier power. Policy shifts or API deprecations can force costly rework and limit differentiation, while certification and ecosystem rules add measurable compliance overhead and time-to-market risk.

Cloud infrastructure and scalability vendors

Jamf relies on hyperscalers and CDNs for uptime, performance and global reach—top three cloud providers held about 66% market share in 2024 (AWS 32%, Microsoft 23%, Google 11%, Synergy Research Group 2024)—so pricing shifts or reserved-capacity limits can squeeze margins. Tooling and data-service lock-in raises switching costs, and multi-cloud approaches reduce but do not eliminate supplier power.

Security and identity integrations

Integration with IdPs, EDR and SIEM vendors like Okta, Microsoft and CrowdStrike is mission-critical; Jamf listed 100+ identity and security integrations in 2024, making partner changes material to UX and feature timing. API or roadmap shifts can delay rollouts and raise support costs. Co-marketing and certification programs often require fees or engineering commitments, giving integration partners moderate bargaining power.

Apple hardware and OS release cadence

Apple’s annual OS cadence (iOS 18 in Sept 2024) plus interim security patches and WWDC betas create rushed compatibility windows; early access helps but unexpected breaking changes shift development and support costs onto Jamf, while customers demand day-zero support, increasing operational pressure and reinforcing timing-asymmetry supplier power.

- Annual major release: Sept (iOS 18, 2024)

- WWDC betas: June

- Day-zero support expected by enterprises

- Breaking changes transfer costs to Jamf

Specialized engineering talent supply

Experienced Apple enterprise engineers are relatively scarce, pushing labor costs higher and contributing to Jamf's R&D spend pressure; Jamf reported revenue of $474 million in FY2024, amplifying the need to control margin impacts from talent costs.

Competition with rivals and Big Tech for macOS/iOS engineers gives the labor market supplier-like power, increasing turnover and concentration of knowledge as operational risks that can slow delivery.

Retention challenges and hiring competition in 2024 have the potential to inflate R&D expense and delay product timelines, affecting time-to-market for enterprise features.

- Scarcity: experienced Apple engineers limited, raising wages and hiring costs

- Competition: Big Tech and rivals intensify talent bidding

- Risk: retention and knowledge concentration threaten delivery

- Financial: FY2024 revenue ~$474M heightens sensitivity to rising R&D/headcount costs

Endpoint security squeezed by Apple 2B, hyperscalers 66%

Jamf faces high supplier power from Apple (2 billion devices by 2024) and annual OS cadence (iOS 18, Sept 2024), forcing rapid compatibility work. Top-three cloud providers held ~66% share in 2024 (AWS 32%, Microsoft 23%, Google 11%), raising infrastructure exposure. Integrations (100+ IdP/EDR/SIEM) and FY2024 revenue $474M intensify margin sensitivity to supplier cost shifts.

| Metric | Value |

|---|---|

| Apple ecosystem | ~2.0B devices (2024) |

| Hyperscaler share | AWS 32% / MS 23% / GCP 11% (2024) |

| Integrations | 100+ (2024) |

| Revenue | $474M FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis of Jamf that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, and provides strategic commentary and industry data to inform investors, executives, and academics.

A concise one-sheet Porter's Five Forces for Jamf that surfaces key competitive pressures and actionable relief strategies—perfect for quick decision-making and pitch decks. Customize force levels with your data or toggle scenarios to illustrate relief from pricing, supplier dependency, or emerging entrants.

Customers Bargaining Power

Large enterprise and EDU procurement

Enterprises and school districts buy Jamf at scale via RFPs, extracting pricing leverage through volume discounts and multi‑year deals; in 2024 Jamf served roughly 70,000 customers, reinforcing institutional buying power. Compliance and security mandates (HIPAA, FERPA, NIST frameworks) add negotiation levers and service requirements. Buyer power is high for large accounts and moderate for SMBs.

Visible alternatives and trialability

Competing Apple MDMs and UEM suites are easy to evaluate via 30–90 day trials and pilots, enabling side-by-side comparisons. Feature parity in core MDM functions among leaders narrows differentiation and strengthens buyer leverage. Public pricing and transparent packaging accelerate vendor comparisons, and switching decisions often hinge on total cost of ownership and support quality, cited by roughly half of enterprise buyers.

Switching costs are meaningful but manageable

Device enrollment, policy migration and user impact create tangible friction that tempers buyer power, but Apple reported over 1.5 billion active devices in 2024, meaning standardized Apple MDM protocols and broad tooling reduce barriers to switch. Migration tools and Jamf professional services can shorten cutover timelines and preserve configurations, enabling a credible threat of switch. Net effect: moderate switching costs.

Bundling pressure from platform suites

Microsoft (FY2024 revenue $211.91B) and VMware (FY2024 revenue $12.88B) can fold Apple management into larger UEM/security suites, and Ivanti pursues similar deals, creating bundling pressure that can compress Jamf pricing or displace its point solutions; buyers wield bundles as negotiation leverage and CFOs push vendor rationalization.

- bundling: major platform suites include Apple management

- rationalization: CFOs favor fewer vendors

- pricing: bundle pressure can force Jamf discounts

- leverage: buyers use bundles to negotiate

Outcome-based expectations

Customers now demand measurable security posture, compliance, and automation outcomes from Jamf, using SLAs, zero-day support, and integrations to force higher service levels.

Poor performance quickly triggers escalation or churn, increasing post-sale buyer influence and turning support metrics into renewal determinants.

- Outcome-driven SLAs

- Zero-day support as leverage

- Integrations required for compliance

- Support performance tied to retention

Large buyers extract discounts; feature parity and bundling compress pricing

Large buyers hold high leverage—Jamf served ~70,000 customers in 2024, extracting volume and multi‑year discounts; SMB power is moderate. Feature parity across MDM/UEM, 1.5B Apple devices (2024) and trial pilots reduce differentiation and strengthen buyer negotiation. Bundling by Microsoft ($211.91B FY2024) and VMware ($12.88B FY2024) compresses pricing; switching costs remain moderate.

| Metric | 2024 |

|---|---|

| Jamf customers | ~70,000 |

| Apple active devices | 1.5B |

| Microsoft revenue | $211.91B |

| VMware revenue | $12.88B |

Full Version Awaits

Jamf Porter's Five Forces Analysis

This Jamf Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—fully formatted and ready for immediate use. No mockups or placeholders are included. Once you complete payment, you’ll get instant access to this identical file. Use it as-is for decision-making, presentations, or reporting.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Jamf faces moderate supplier power, intense buyer expectations, and evolving substitute and entrant threats that shape its competitive dynamics across device management and security. This brief snapshot highlights key pressures but only scratches the surface of market intensity, strategic levers, and growth risks. Unlock the full Porter's Five Forces Analysis to explore Jamf’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Apple MDM frameworks

Jamf’s platform depends heavily on Apple MDM protocols, APNs and proprietary APIs, giving Apple outsized leverage over product roadmap and timing; Apple’s ecosystem totaled over 2 billion active devices by 2024, concentrating supplier power. Policy shifts or API deprecations can force costly rework and limit differentiation, while certification and ecosystem rules add measurable compliance overhead and time-to-market risk.

Cloud infrastructure and scalability vendors

Jamf relies on hyperscalers and CDNs for uptime, performance and global reach—top three cloud providers held about 66% market share in 2024 (AWS 32%, Microsoft 23%, Google 11%, Synergy Research Group 2024)—so pricing shifts or reserved-capacity limits can squeeze margins. Tooling and data-service lock-in raises switching costs, and multi-cloud approaches reduce but do not eliminate supplier power.

Security and identity integrations

Integration with IdPs, EDR and SIEM vendors like Okta, Microsoft and CrowdStrike is mission-critical; Jamf listed 100+ identity and security integrations in 2024, making partner changes material to UX and feature timing. API or roadmap shifts can delay rollouts and raise support costs. Co-marketing and certification programs often require fees or engineering commitments, giving integration partners moderate bargaining power.

Apple hardware and OS release cadence

Apple’s annual OS cadence (iOS 18 in Sept 2024) plus interim security patches and WWDC betas create rushed compatibility windows; early access helps but unexpected breaking changes shift development and support costs onto Jamf, while customers demand day-zero support, increasing operational pressure and reinforcing timing-asymmetry supplier power.

- Annual major release: Sept (iOS 18, 2024)

- WWDC betas: June

- Day-zero support expected by enterprises

- Breaking changes transfer costs to Jamf

Specialized engineering talent supply

Experienced Apple enterprise engineers are relatively scarce, pushing labor costs higher and contributing to Jamf's R&D spend pressure; Jamf reported revenue of $474 million in FY2024, amplifying the need to control margin impacts from talent costs.

Competition with rivals and Big Tech for macOS/iOS engineers gives the labor market supplier-like power, increasing turnover and concentration of knowledge as operational risks that can slow delivery.

Retention challenges and hiring competition in 2024 have the potential to inflate R&D expense and delay product timelines, affecting time-to-market for enterprise features.

- Scarcity: experienced Apple engineers limited, raising wages and hiring costs

- Competition: Big Tech and rivals intensify talent bidding

- Risk: retention and knowledge concentration threaten delivery

- Financial: FY2024 revenue ~$474M heightens sensitivity to rising R&D/headcount costs

Endpoint security squeezed by Apple 2B, hyperscalers 66%

Jamf faces high supplier power from Apple (2 billion devices by 2024) and annual OS cadence (iOS 18, Sept 2024), forcing rapid compatibility work. Top-three cloud providers held ~66% share in 2024 (AWS 32%, Microsoft 23%, Google 11%), raising infrastructure exposure. Integrations (100+ IdP/EDR/SIEM) and FY2024 revenue $474M intensify margin sensitivity to supplier cost shifts.

| Metric | Value |

|---|---|

| Apple ecosystem | ~2.0B devices (2024) |

| Hyperscaler share | AWS 32% / MS 23% / GCP 11% (2024) |

| Integrations | 100+ (2024) |

| Revenue | $474M FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis of Jamf that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, and provides strategic commentary and industry data to inform investors, executives, and academics.

A concise one-sheet Porter's Five Forces for Jamf that surfaces key competitive pressures and actionable relief strategies—perfect for quick decision-making and pitch decks. Customize force levels with your data or toggle scenarios to illustrate relief from pricing, supplier dependency, or emerging entrants.

Customers Bargaining Power

Large enterprise and EDU procurement

Enterprises and school districts buy Jamf at scale via RFPs, extracting pricing leverage through volume discounts and multi‑year deals; in 2024 Jamf served roughly 70,000 customers, reinforcing institutional buying power. Compliance and security mandates (HIPAA, FERPA, NIST frameworks) add negotiation levers and service requirements. Buyer power is high for large accounts and moderate for SMBs.

Visible alternatives and trialability

Competing Apple MDMs and UEM suites are easy to evaluate via 30–90 day trials and pilots, enabling side-by-side comparisons. Feature parity in core MDM functions among leaders narrows differentiation and strengthens buyer leverage. Public pricing and transparent packaging accelerate vendor comparisons, and switching decisions often hinge on total cost of ownership and support quality, cited by roughly half of enterprise buyers.

Switching costs are meaningful but manageable

Device enrollment, policy migration and user impact create tangible friction that tempers buyer power, but Apple reported over 1.5 billion active devices in 2024, meaning standardized Apple MDM protocols and broad tooling reduce barriers to switch. Migration tools and Jamf professional services can shorten cutover timelines and preserve configurations, enabling a credible threat of switch. Net effect: moderate switching costs.

Bundling pressure from platform suites

Microsoft (FY2024 revenue $211.91B) and VMware (FY2024 revenue $12.88B) can fold Apple management into larger UEM/security suites, and Ivanti pursues similar deals, creating bundling pressure that can compress Jamf pricing or displace its point solutions; buyers wield bundles as negotiation leverage and CFOs push vendor rationalization.

- bundling: major platform suites include Apple management

- rationalization: CFOs favor fewer vendors

- pricing: bundle pressure can force Jamf discounts

- leverage: buyers use bundles to negotiate

Outcome-based expectations

Customers now demand measurable security posture, compliance, and automation outcomes from Jamf, using SLAs, zero-day support, and integrations to force higher service levels.

Poor performance quickly triggers escalation or churn, increasing post-sale buyer influence and turning support metrics into renewal determinants.

- Outcome-driven SLAs

- Zero-day support as leverage

- Integrations required for compliance

- Support performance tied to retention

Large buyers extract discounts; feature parity and bundling compress pricing

Large buyers hold high leverage—Jamf served ~70,000 customers in 2024, extracting volume and multi‑year discounts; SMB power is moderate. Feature parity across MDM/UEM, 1.5B Apple devices (2024) and trial pilots reduce differentiation and strengthen buyer negotiation. Bundling by Microsoft ($211.91B FY2024) and VMware ($12.88B FY2024) compresses pricing; switching costs remain moderate.

| Metric | 2024 |

|---|---|

| Jamf customers | ~70,000 |

| Apple active devices | 1.5B |

| Microsoft revenue | $211.91B |

| VMware revenue | $12.88B |

Full Version Awaits

Jamf Porter's Five Forces Analysis

This Jamf Porter's Five Forces Analysis preview is the exact document you'll receive after purchase—fully formatted and ready for immediate use. No mockups or placeholders are included. Once you complete payment, you’ll get instant access to this identical file. Use it as-is for decision-making, presentations, or reporting.