JBT Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

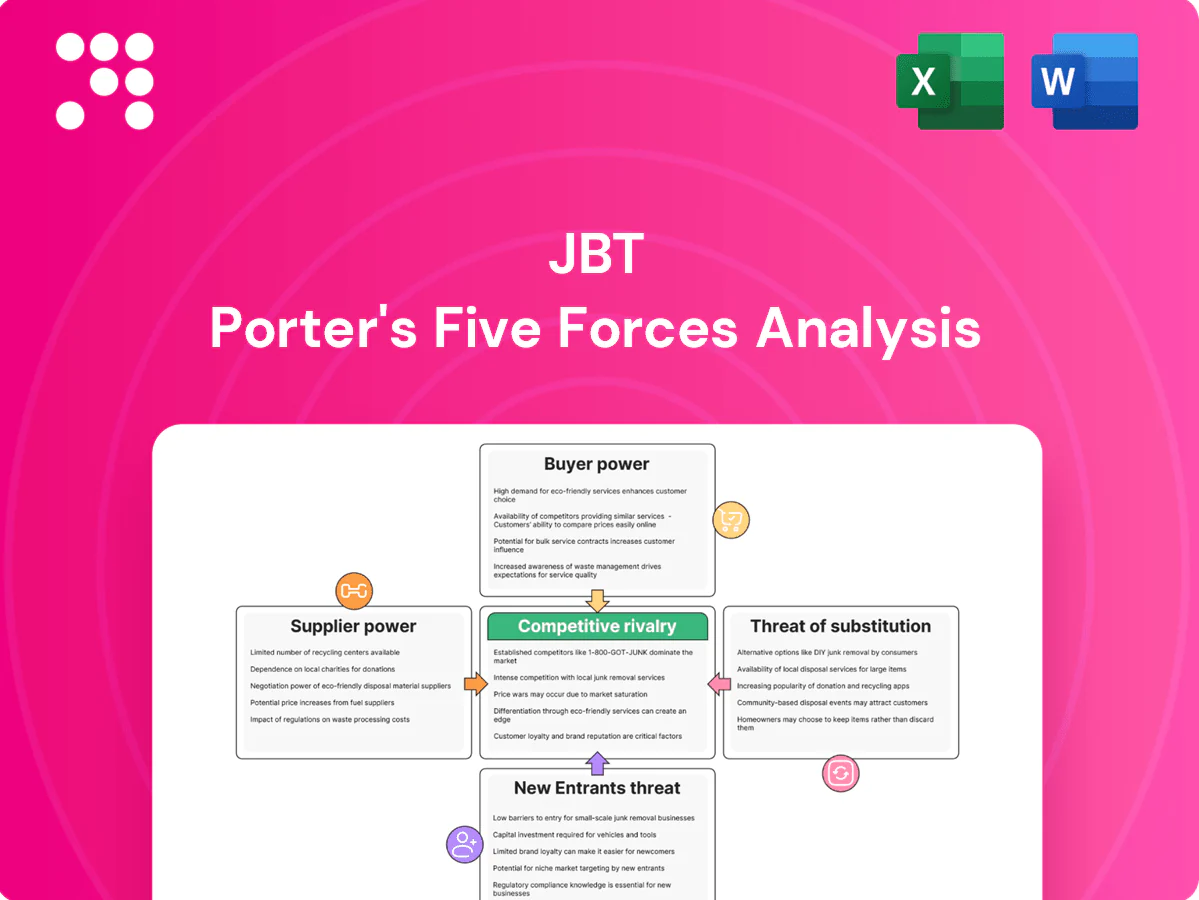

JBT’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute risks shaping its market position. This brief teases strategic implications and key pressure points. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialized inputs narrow supplier base

Precision metals, food-grade materials, and aviation-compliant components narrow JBTs supplier pool, with the global food processing equipment market estimated at about $68 billion in 2024, concentrating demand among certified vendors.

Fewer qualified suppliers can command higher prices and longer lead times; qualification and validation cycles of 6–12 months often entrench incumbents.

Resulting input-cost pressure and elevated supply risk can compress margins and increase working capital needs for JBT.

Switching costs and validation hurdles

Requalifying critical sanitary or airport-safety parts often takes 3–9 months due to engineering, testing and certification, with compliance testing budgets commonly in the tens of thousands of dollars. These validation hurdles and frequent production-disruption costs give incumbent suppliers leverage, sustaining moderate-to-high bargaining power for key vendors.

Electronics and controls exposure

PLCs, sensors and drives remain concentrated among Siemens, Rockwell and Schneider, which together control roughly 55–65% of the PLC/drives market; platform lock‑ins and component shortages (lead times still often 12–16 weeks in 2024) pressure pricing and availability. Firmware and software integration deepens supplier dependence, so JBT must dual‑source critical parts and redesign platforms to reduce single‑vendor risk and margin volatility.

Commodity volatility pass-through

Steel, aluminum and energy price swings in 2024 (steel and aluminum moved roughly 15–30% across markets; Brent rose ~20% YoY) compressed JBT margins as suppliers passed costs quickly while JBT’s customer pricing lagged, elevating supplier leverage during inflationary spikes. Hedging and indexed contracts provided partial relief but imperfectly matched timing, increasing short-term margin pressure.

- Supplier pass-through speed ↑; JBT pricing lag

- Commodity swings ~15–30% in 2024

- Brent crude ~+20% YoY 2024

- Hedges/indexing mitigate but don’t eliminate timing mismatch

Global logistics and compliance constraints

Sanitary, aviation & automation suppliers: moderate-to-high supplier power amid margin pressure

Specialized sanitary, aviation and automation suppliers give JBT moderate-to-high supplier power: global food-processing equip market ~$68B (2024), PLC/drives share 55–65%, lead times 12–16 weeks, requalification 3–12 months. Commodity swings 15–30% and Brent +20% YoY (2024) increased input-cost pass-through and margin pressure, forcing dual-sourcing and nearshoring trade-offs.

| Metric | 2024 value |

|---|---|

| Market size | $68B |

| PLC/drives share | 55–65% |

| Lead times | 12–16 wks |

| Commodity swings | 15–30% |

| Brent YoY | +20% |

What is included in the product

Tailored Porter’s Five Forces for JBT uncover key drivers of competition, buyer and supplier power, substitution risk, and entry barriers, highlighting disruptive threats and strategic levers to protect and grow market position.

Single-sheet Porter's Five Forces for JBT—visual radar and editable pressure levels that clarify competitive pain points instantly, require no macros, and drop seamlessly into decks or dashboards for faster strategic decisions.

Customers Bargaining Power

Concentrated, sophisticated customers

Large food processors and airlines/airports maintain centralized procurement and technical teams that demand tailored specs, lifecycle guarantees and aggressive commercial terms; in 2024 global air passenger traffic recovered to roughly 4.5 billion, reinforcing airline buyer scale and bargaining clout. Competitive tenders for capital equipment are common and intensify price pressure, often compressing supplier margins. On marquee deals this dynamic creates high buyer leverage, forcing suppliers to concede extended warranties, service commitments and lower ECMs.

High switching costs, but negotiated upfront

Integration with plant layouts, HACCP programs and airport ops produces high post-install stickiness, making aftermarket parts and service a durable revenue stream (industry lifecycle service share typically ~30%).

Buyers exert strong bargaining power pre-sale, exploiting vendor competition to lock in price cuts often up to 15–20% and tight SLAs; after installation JBT-like suppliers regain leverage through spare parts and service margins.

Total cost of ownership focus

Customers prioritize uptime, yield and energy use over list price alone, often accepting higher capex if payback is within 3 years; performance guarantees and KPIs (service-level uptime targets, yield improvement commitments) shift procurement to long-term value. When JBT documents ROI and uptime improvements, pure price pressure eases, and data/analytics offerings that demonstrate continuous savings further tilt bargaining power toward suppliers.

Budget cycles and project deferrals

Capex is cyclical and tied to commodity and consumer swings, so JBT buyers can delay or phase projects to extract price or lead-time concessions; backlog timing gives customers extra leverage in downturns. In 2024, higher borrowing costs (Federal funds 5.25–5.50%) raise the value of flexible financing and modular offers as mitigation.

- Buyers delay projects

- Backlog = leverage

- Concessions common

- Flexible finance mitigates

Aftermarket leverage trade-off

OEM parts, service contracts and paid upgrades lock recurring revenue for JBT, with industry studies in 2024 showing aftermarket can account for roughly 25-35% of lifecycle revenue; buyers counter by demanding open-architecture and multi-vendor compatibility to cut dependency. Warranty terms are used as negotiation levers while value-added services (training, predictive maintenance) justify OEM premiums and sustain loyalty despite higher prices.

- OEM parts: recurring revenue

- Open-architecture: buyer leverage

- Warranties: negotiation tool

- Services: justify premium

Buyers force 15–20% cuts; aftermarket 25–35% restores margins amid high-rate finance demand

Large airline/food buyers (global air traffic ~4.5B in 2024) exert strong pre-sale leverage, extracting 15–20% price cuts and tight SLAs; aftermarket yields 25–35% of lifecycle revenue, restoring supplier margins post-sale. High rates (Fed funds 5.25–5.50% in 2024) increase demand for flexible finance and phased projects. Open-architecture requests and service bundles shape long-term bargaining.

| Metric | 2024 Value |

|---|---|

| Global air passengers | ~4.5B |

| Buyer price cuts | 15–20% |

| Aftermarket share | 25–35% |

| Fed funds rate | 5.25–5.50% |

Preview Before You Purchase

JBT Porter's Five Forces Analysis

This preview shows the exact JBT Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders or mockups. The document is complete, professionally formatted, and ready to download instantly upon payment. Use it as-is for strategic planning, valuation inputs, or stakeholder briefings.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

JBT’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute risks shaping its market position. This brief teases strategic implications and key pressure points. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialized inputs narrow supplier base

Precision metals, food-grade materials, and aviation-compliant components narrow JBTs supplier pool, with the global food processing equipment market estimated at about $68 billion in 2024, concentrating demand among certified vendors.

Fewer qualified suppliers can command higher prices and longer lead times; qualification and validation cycles of 6–12 months often entrench incumbents.

Resulting input-cost pressure and elevated supply risk can compress margins and increase working capital needs for JBT.

Switching costs and validation hurdles

Requalifying critical sanitary or airport-safety parts often takes 3–9 months due to engineering, testing and certification, with compliance testing budgets commonly in the tens of thousands of dollars. These validation hurdles and frequent production-disruption costs give incumbent suppliers leverage, sustaining moderate-to-high bargaining power for key vendors.

Electronics and controls exposure

PLCs, sensors and drives remain concentrated among Siemens, Rockwell and Schneider, which together control roughly 55–65% of the PLC/drives market; platform lock‑ins and component shortages (lead times still often 12–16 weeks in 2024) pressure pricing and availability. Firmware and software integration deepens supplier dependence, so JBT must dual‑source critical parts and redesign platforms to reduce single‑vendor risk and margin volatility.

Commodity volatility pass-through

Steel, aluminum and energy price swings in 2024 (steel and aluminum moved roughly 15–30% across markets; Brent rose ~20% YoY) compressed JBT margins as suppliers passed costs quickly while JBT’s customer pricing lagged, elevating supplier leverage during inflationary spikes. Hedging and indexed contracts provided partial relief but imperfectly matched timing, increasing short-term margin pressure.

- Supplier pass-through speed ↑; JBT pricing lag

- Commodity swings ~15–30% in 2024

- Brent crude ~+20% YoY 2024

- Hedges/indexing mitigate but don’t eliminate timing mismatch

Global logistics and compliance constraints

Sanitary, aviation & automation suppliers: moderate-to-high supplier power amid margin pressure

Specialized sanitary, aviation and automation suppliers give JBT moderate-to-high supplier power: global food-processing equip market ~$68B (2024), PLC/drives share 55–65%, lead times 12–16 weeks, requalification 3–12 months. Commodity swings 15–30% and Brent +20% YoY (2024) increased input-cost pass-through and margin pressure, forcing dual-sourcing and nearshoring trade-offs.

| Metric | 2024 value |

|---|---|

| Market size | $68B |

| PLC/drives share | 55–65% |

| Lead times | 12–16 wks |

| Commodity swings | 15–30% |

| Brent YoY | +20% |

What is included in the product

Tailored Porter’s Five Forces for JBT uncover key drivers of competition, buyer and supplier power, substitution risk, and entry barriers, highlighting disruptive threats and strategic levers to protect and grow market position.

Single-sheet Porter's Five Forces for JBT—visual radar and editable pressure levels that clarify competitive pain points instantly, require no macros, and drop seamlessly into decks or dashboards for faster strategic decisions.

Customers Bargaining Power

Concentrated, sophisticated customers

Large food processors and airlines/airports maintain centralized procurement and technical teams that demand tailored specs, lifecycle guarantees and aggressive commercial terms; in 2024 global air passenger traffic recovered to roughly 4.5 billion, reinforcing airline buyer scale and bargaining clout. Competitive tenders for capital equipment are common and intensify price pressure, often compressing supplier margins. On marquee deals this dynamic creates high buyer leverage, forcing suppliers to concede extended warranties, service commitments and lower ECMs.

High switching costs, but negotiated upfront

Integration with plant layouts, HACCP programs and airport ops produces high post-install stickiness, making aftermarket parts and service a durable revenue stream (industry lifecycle service share typically ~30%).

Buyers exert strong bargaining power pre-sale, exploiting vendor competition to lock in price cuts often up to 15–20% and tight SLAs; after installation JBT-like suppliers regain leverage through spare parts and service margins.

Total cost of ownership focus

Customers prioritize uptime, yield and energy use over list price alone, often accepting higher capex if payback is within 3 years; performance guarantees and KPIs (service-level uptime targets, yield improvement commitments) shift procurement to long-term value. When JBT documents ROI and uptime improvements, pure price pressure eases, and data/analytics offerings that demonstrate continuous savings further tilt bargaining power toward suppliers.

Budget cycles and project deferrals

Capex is cyclical and tied to commodity and consumer swings, so JBT buyers can delay or phase projects to extract price or lead-time concessions; backlog timing gives customers extra leverage in downturns. In 2024, higher borrowing costs (Federal funds 5.25–5.50%) raise the value of flexible financing and modular offers as mitigation.

- Buyers delay projects

- Backlog = leverage

- Concessions common

- Flexible finance mitigates

Aftermarket leverage trade-off

OEM parts, service contracts and paid upgrades lock recurring revenue for JBT, with industry studies in 2024 showing aftermarket can account for roughly 25-35% of lifecycle revenue; buyers counter by demanding open-architecture and multi-vendor compatibility to cut dependency. Warranty terms are used as negotiation levers while value-added services (training, predictive maintenance) justify OEM premiums and sustain loyalty despite higher prices.

- OEM parts: recurring revenue

- Open-architecture: buyer leverage

- Warranties: negotiation tool

- Services: justify premium

Buyers force 15–20% cuts; aftermarket 25–35% restores margins amid high-rate finance demand

Large airline/food buyers (global air traffic ~4.5B in 2024) exert strong pre-sale leverage, extracting 15–20% price cuts and tight SLAs; aftermarket yields 25–35% of lifecycle revenue, restoring supplier margins post-sale. High rates (Fed funds 5.25–5.50% in 2024) increase demand for flexible finance and phased projects. Open-architecture requests and service bundles shape long-term bargaining.

| Metric | 2024 Value |

|---|---|

| Global air passengers | ~4.5B |

| Buyer price cuts | 15–20% |

| Aftermarket share | 25–35% |

| Fed funds rate | 5.25–5.50% |

Preview Before You Purchase

JBT Porter's Five Forces Analysis

This preview shows the exact JBT Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders or mockups. The document is complete, professionally formatted, and ready to download instantly upon payment. Use it as-is for strategic planning, valuation inputs, or stakeholder briefings.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

JBT’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, barriers to entry, and substitute risks shaping its market position. This brief teases strategic implications and key pressure points. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialized inputs narrow supplier base

Precision metals, food-grade materials, and aviation-compliant components narrow JBTs supplier pool, with the global food processing equipment market estimated at about $68 billion in 2024, concentrating demand among certified vendors.

Fewer qualified suppliers can command higher prices and longer lead times; qualification and validation cycles of 6–12 months often entrench incumbents.

Resulting input-cost pressure and elevated supply risk can compress margins and increase working capital needs for JBT.

Switching costs and validation hurdles

Requalifying critical sanitary or airport-safety parts often takes 3–9 months due to engineering, testing and certification, with compliance testing budgets commonly in the tens of thousands of dollars. These validation hurdles and frequent production-disruption costs give incumbent suppliers leverage, sustaining moderate-to-high bargaining power for key vendors.

Electronics and controls exposure

PLCs, sensors and drives remain concentrated among Siemens, Rockwell and Schneider, which together control roughly 55–65% of the PLC/drives market; platform lock‑ins and component shortages (lead times still often 12–16 weeks in 2024) pressure pricing and availability. Firmware and software integration deepens supplier dependence, so JBT must dual‑source critical parts and redesign platforms to reduce single‑vendor risk and margin volatility.

Commodity volatility pass-through

Steel, aluminum and energy price swings in 2024 (steel and aluminum moved roughly 15–30% across markets; Brent rose ~20% YoY) compressed JBT margins as suppliers passed costs quickly while JBT’s customer pricing lagged, elevating supplier leverage during inflationary spikes. Hedging and indexed contracts provided partial relief but imperfectly matched timing, increasing short-term margin pressure.

- Supplier pass-through speed ↑; JBT pricing lag

- Commodity swings ~15–30% in 2024

- Brent crude ~+20% YoY 2024

- Hedges/indexing mitigate but don’t eliminate timing mismatch

Global logistics and compliance constraints

Sanitary, aviation & automation suppliers: moderate-to-high supplier power amid margin pressure

Specialized sanitary, aviation and automation suppliers give JBT moderate-to-high supplier power: global food-processing equip market ~$68B (2024), PLC/drives share 55–65%, lead times 12–16 weeks, requalification 3–12 months. Commodity swings 15–30% and Brent +20% YoY (2024) increased input-cost pass-through and margin pressure, forcing dual-sourcing and nearshoring trade-offs.

| Metric | 2024 value |

|---|---|

| Market size | $68B |

| PLC/drives share | 55–65% |

| Lead times | 12–16 wks |

| Commodity swings | 15–30% |

| Brent YoY | +20% |

What is included in the product

Tailored Porter’s Five Forces for JBT uncover key drivers of competition, buyer and supplier power, substitution risk, and entry barriers, highlighting disruptive threats and strategic levers to protect and grow market position.

Single-sheet Porter's Five Forces for JBT—visual radar and editable pressure levels that clarify competitive pain points instantly, require no macros, and drop seamlessly into decks or dashboards for faster strategic decisions.

Customers Bargaining Power

Concentrated, sophisticated customers

Large food processors and airlines/airports maintain centralized procurement and technical teams that demand tailored specs, lifecycle guarantees and aggressive commercial terms; in 2024 global air passenger traffic recovered to roughly 4.5 billion, reinforcing airline buyer scale and bargaining clout. Competitive tenders for capital equipment are common and intensify price pressure, often compressing supplier margins. On marquee deals this dynamic creates high buyer leverage, forcing suppliers to concede extended warranties, service commitments and lower ECMs.

High switching costs, but negotiated upfront

Integration with plant layouts, HACCP programs and airport ops produces high post-install stickiness, making aftermarket parts and service a durable revenue stream (industry lifecycle service share typically ~30%).

Buyers exert strong bargaining power pre-sale, exploiting vendor competition to lock in price cuts often up to 15–20% and tight SLAs; after installation JBT-like suppliers regain leverage through spare parts and service margins.

Total cost of ownership focus

Customers prioritize uptime, yield and energy use over list price alone, often accepting higher capex if payback is within 3 years; performance guarantees and KPIs (service-level uptime targets, yield improvement commitments) shift procurement to long-term value. When JBT documents ROI and uptime improvements, pure price pressure eases, and data/analytics offerings that demonstrate continuous savings further tilt bargaining power toward suppliers.

Budget cycles and project deferrals

Capex is cyclical and tied to commodity and consumer swings, so JBT buyers can delay or phase projects to extract price or lead-time concessions; backlog timing gives customers extra leverage in downturns. In 2024, higher borrowing costs (Federal funds 5.25–5.50%) raise the value of flexible financing and modular offers as mitigation.

- Buyers delay projects

- Backlog = leverage

- Concessions common

- Flexible finance mitigates

Aftermarket leverage trade-off

OEM parts, service contracts and paid upgrades lock recurring revenue for JBT, with industry studies in 2024 showing aftermarket can account for roughly 25-35% of lifecycle revenue; buyers counter by demanding open-architecture and multi-vendor compatibility to cut dependency. Warranty terms are used as negotiation levers while value-added services (training, predictive maintenance) justify OEM premiums and sustain loyalty despite higher prices.

- OEM parts: recurring revenue

- Open-architecture: buyer leverage

- Warranties: negotiation tool

- Services: justify premium

Buyers force 15–20% cuts; aftermarket 25–35% restores margins amid high-rate finance demand

Large airline/food buyers (global air traffic ~4.5B in 2024) exert strong pre-sale leverage, extracting 15–20% price cuts and tight SLAs; aftermarket yields 25–35% of lifecycle revenue, restoring supplier margins post-sale. High rates (Fed funds 5.25–5.50% in 2024) increase demand for flexible finance and phased projects. Open-architecture requests and service bundles shape long-term bargaining.

| Metric | 2024 Value |

|---|---|

| Global air passengers | ~4.5B |

| Buyer price cuts | 15–20% |

| Aftermarket share | 25–35% |

| Fed funds rate | 5.25–5.50% |

Preview Before You Purchase

JBT Porter's Five Forces Analysis

This preview shows the exact JBT Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders or mockups. The document is complete, professionally formatted, and ready to download instantly upon payment. Use it as-is for strategic planning, valuation inputs, or stakeholder briefings.