J.C. Bamford Excavators Limited (JCB) Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

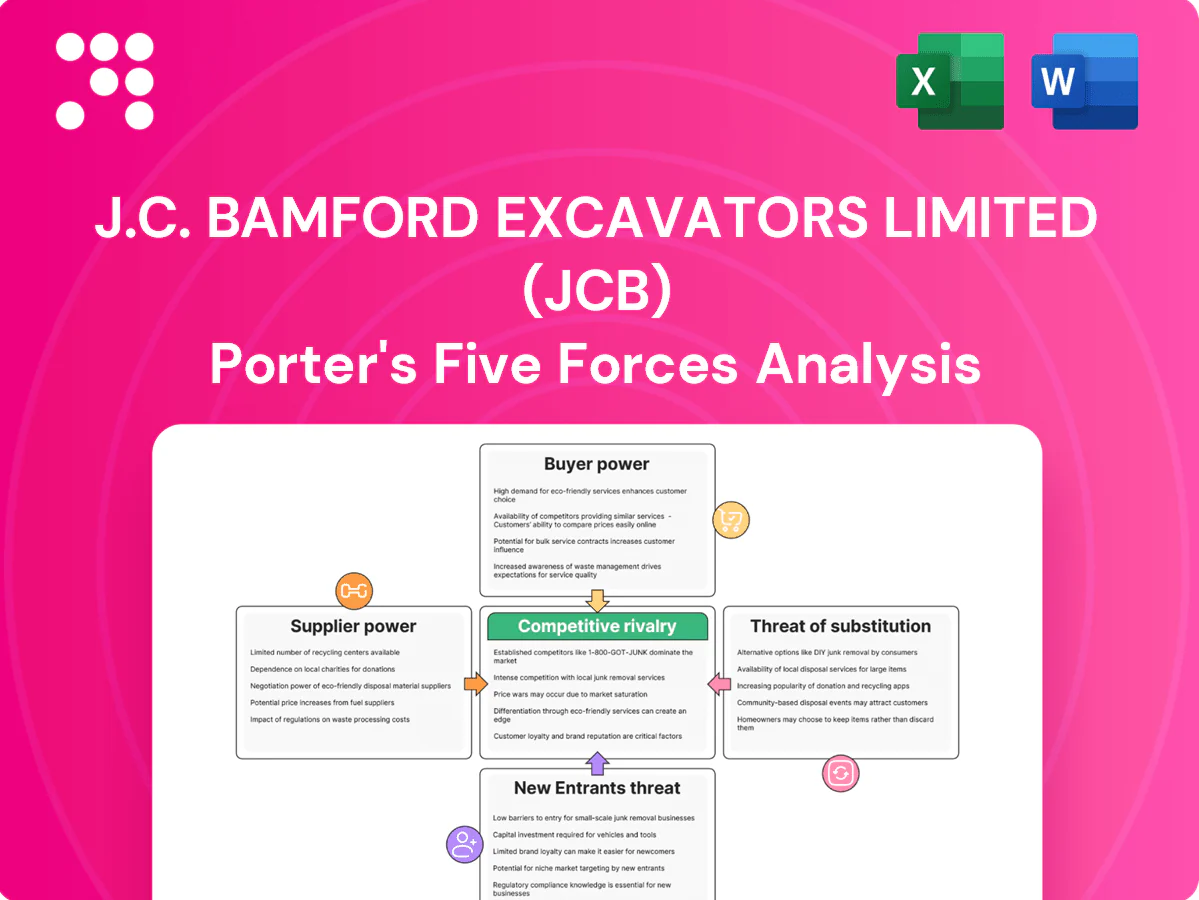

J.C. Bamford Excavators Limited (JCB) faces moderate rivalry from global OEMs, strong supplier influence on specialized components, and shifting buyer power as projects demand integrated solutions. Barriers to entry remain high but technology and rental models raise substitute risks. This snapshot highlights strategic pressure points—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical components

Hydraulics, advanced electronics and high‑spec steels for JCB come from a concentrated Tier‑1 base, giving select suppliers pricing and lead‑time leverage; in 2024 heavy‑equipment suppliers reported average lead times of ~20–24 weeks. Long qualification cycles driven by safety/durability standards slow switching, tightening supply in upcycles; JCB counters with approved‑vendor lists and dual‑sourcing where feasible.

Switching costs and requalification

Switching core parts such as pumps, ECUs and engines requires redesign, testing and certification, imposing high switching costs that strengthen incumbent suppliers. These costs grant suppliers bargaining power despite JCB’s 2024 engineering scale enabling partial standardization to reduce lock-in across platforms. Mission-critical components typically still need multi-month requalification (commonly 6–18 months), preserving supplier leverage.

Commodity volatility passthrough

Steel, energy and freight volatility can strengthen supplier hand during spikes, and JCB's contracts commonly include surcharges that pass costs downstream; the group uses hedging and multiyear supply agreements to smooth input costs, but sudden shocks can compress margins before prices are adjusted.

Vertical integration offsets

By 2024 JCB’s in-house engines and key attachments reduce dependence on external suppliers, improving supply assurance and strengthening negotiation leverage with outside vendors. Internal capacity delivers tighter cost control and enables product differentiation through bespoke integrations. Yet specialist supplier ecosystems remain essential for many advanced components and materials.

- In-house engines: improved supply assurance

- Cost control: lower variable procurement exposure

- Product differentiation: proprietary attachments

- Limit: cannot replace specialist suppliers

Emerging tech dependencies

Electrification, batteries, sensors and telematics raise JCB’s reliance on specialized vendors, concentrating leverage with specialists; top-5 battery cell makers controlled about 80% of global supply in 2024, with CATL ~37% (SNE Research 2024). Certification and safety regimes slow supplier turnover, while strategic partnerships secure access and roadmap alignment.

- Battery concentration: top-5 ≈80% (2024)

- Certification barrier: slows supplier replacement

- Partnerships: secure supply and tech alignment

20–24 weeks avg lead times; top-5 battery cells ≈80%

Concentrated Tier‑1 suppliers and long qualification cycles (6–18 months) give suppliers pricing and lead‑time leverage; average lead times ~20–24 weeks in 2024. JCB reduces exposure via approved vendors, dual‑sourcing and in‑house engines/attachments, but specialist EV components concentrate power (top‑5 battery cell makers ≈80%, CATL ≈37% in 2024).

| Metric | 2024 Value |

|---|---|

| Avg lead time | 20–24 weeks |

| Requalification | 6–18 months |

| Battery vendor concentration | Top‑5 ≈80% (CATL ≈37%) |

What is included in the product

Tailored Porter’s Five Forces analysis for J.C. Bamford Excavators Limited (JCB) uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/technology-driven disruption to assess pricing power, margins, and barriers protecting JCB’s market position.

A one-sheet Porter’s Five Forces analysis for J.C. Bamford Excavators pinpoints supplier, buyer, rivalry, substitutes and entry pain points and strategic levers; customizable pressure levels and clean visuals make it deck- and dashboard-ready.

Customers Bargaining Power

Large fleet buyers and governments

Major contractors, rental houses and public agencies buy JCB machines in large volumes, extracting discounts and contractual terms through competitive tenders that compress margins; fleet orders often dictate product specs and stringent after-sales SLAs, and losing a single national account can shave double-digit percentage volume from a regional sales book, materially affecting revenue and dealer network cash flow.

Dealer network intermediation

Dealers aggregate demand and negotiate pricing and service commitments on behalf of customers, materially shaping JCB's transaction terms; as of 2024 JCB's network exceeds 2,000 dealer outlets across 150 countries, concentrating bargaining power at the intermediary level. Strong dealer relationships and value-added services—financing, parts, training—can buffer price pressure and protect margins. Weak dealer coverage or patchy performance increases buyer leverage by lowering switching frictions, making JCB highly reliant on dealer execution to sustain pricing power.

Price transparency and benchmarking

Global rivals and online channels make cross-quote comparisons routine, as the construction equipment market (about USD 187 billion in 2024) sees digital listings surge; buyers now benchmark total cost of ownership across brands, pressing for stronger warranties, financing and residual-value support. Transparent specs narrow differentiation, forcing JCB to justify any premium via measurable gains in productivity, uptime and telematics-driven insights (telematics adoption ~40% in 2024).

High switching but TCO focus

Switching brands involves operator retraining, spare-parts stocking and fleet integration costs, so buyers weigh reliability, fuel economy and resale uplift; many customers switch despite these frictions when uptime or lifecycle cost advantages exceed transition expense. Procurement decisions are TCO-driven in 2024, lowering pure price sensitivity, while JCB’s global service footprint — over 700 dealer outlets — and uptime guarantees constrain buyer bargaining power.

- Operator training, parts, integration

- Switches for reliability/fuel/resale

- TCO reduces price-only buying

- 700+ dealers (2024) limit buyer leverage

Cyclical demand amplifiers

In downturns excess capacity shifts bargaining power to buyers, forcing JCB into discounts and incentives; in upcycles tight supply and lead times reduce buyer leverage. Rental channels and fleets buffer swings but demand remains cyclical, and flexible financing plus buyback programs help preserve pricing discipline and residual values.

- Downturns: buyer discounts

- Upcycles: tighter supply

- Rental buffers volatility

- Financing/buybacks stabilize pricing

Bulk tenders, dealer finance and telematics reshape equipment margins and TCO

Large contractors, rental firms and public agencies exert strong bargaining power via bulk tenders, driving discounts and strict SLAs that can cut regional volumes by double digits. Dealers (JCB network ~2,000 outlets in 150 countries in 2024) aggregate customer leverage but also protect margins through financing, parts and uptime guarantees. Transparent TCO benchmarking (market ~USD 187bn; telematics adoption ~40% in 2024) raises service and residual-value demands.

| Metric | 2024 value |

|---|---|

| Global market size | USD 187bn |

| JCB dealer outlets | ~2,000 |

| Telematics adoption | ~40% |

Preview Before You Purchase

J.C. Bamford Excavators Limited (JCB) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for J.C. Bamford Excavators Limited you'll receive immediately after purchase—fully formatted and ready to use. It assesses industry rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for JCB's competitive positioning and margins.

Go Beyond the Preview—Access the Full Strategic Report

J.C. Bamford Excavators Limited (JCB) faces moderate rivalry from global OEMs, strong supplier influence on specialized components, and shifting buyer power as projects demand integrated solutions. Barriers to entry remain high but technology and rental models raise substitute risks. This snapshot highlights strategic pressure points—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical components

Hydraulics, advanced electronics and high‑spec steels for JCB come from a concentrated Tier‑1 base, giving select suppliers pricing and lead‑time leverage; in 2024 heavy‑equipment suppliers reported average lead times of ~20–24 weeks. Long qualification cycles driven by safety/durability standards slow switching, tightening supply in upcycles; JCB counters with approved‑vendor lists and dual‑sourcing where feasible.

Switching costs and requalification

Switching core parts such as pumps, ECUs and engines requires redesign, testing and certification, imposing high switching costs that strengthen incumbent suppliers. These costs grant suppliers bargaining power despite JCB’s 2024 engineering scale enabling partial standardization to reduce lock-in across platforms. Mission-critical components typically still need multi-month requalification (commonly 6–18 months), preserving supplier leverage.

Commodity volatility passthrough

Steel, energy and freight volatility can strengthen supplier hand during spikes, and JCB's contracts commonly include surcharges that pass costs downstream; the group uses hedging and multiyear supply agreements to smooth input costs, but sudden shocks can compress margins before prices are adjusted.

Vertical integration offsets

By 2024 JCB’s in-house engines and key attachments reduce dependence on external suppliers, improving supply assurance and strengthening negotiation leverage with outside vendors. Internal capacity delivers tighter cost control and enables product differentiation through bespoke integrations. Yet specialist supplier ecosystems remain essential for many advanced components and materials.

- In-house engines: improved supply assurance

- Cost control: lower variable procurement exposure

- Product differentiation: proprietary attachments

- Limit: cannot replace specialist suppliers

Emerging tech dependencies

Electrification, batteries, sensors and telematics raise JCB’s reliance on specialized vendors, concentrating leverage with specialists; top-5 battery cell makers controlled about 80% of global supply in 2024, with CATL ~37% (SNE Research 2024). Certification and safety regimes slow supplier turnover, while strategic partnerships secure access and roadmap alignment.

- Battery concentration: top-5 ≈80% (2024)

- Certification barrier: slows supplier replacement

- Partnerships: secure supply and tech alignment

20–24 weeks avg lead times; top-5 battery cells ≈80%

Concentrated Tier‑1 suppliers and long qualification cycles (6–18 months) give suppliers pricing and lead‑time leverage; average lead times ~20–24 weeks in 2024. JCB reduces exposure via approved vendors, dual‑sourcing and in‑house engines/attachments, but specialist EV components concentrate power (top‑5 battery cell makers ≈80%, CATL ≈37% in 2024).

| Metric | 2024 Value |

|---|---|

| Avg lead time | 20–24 weeks |

| Requalification | 6–18 months |

| Battery vendor concentration | Top‑5 ≈80% (CATL ≈37%) |

What is included in the product

Tailored Porter’s Five Forces analysis for J.C. Bamford Excavators Limited (JCB) uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/technology-driven disruption to assess pricing power, margins, and barriers protecting JCB’s market position.

A one-sheet Porter’s Five Forces analysis for J.C. Bamford Excavators pinpoints supplier, buyer, rivalry, substitutes and entry pain points and strategic levers; customizable pressure levels and clean visuals make it deck- and dashboard-ready.

Customers Bargaining Power

Large fleet buyers and governments

Major contractors, rental houses and public agencies buy JCB machines in large volumes, extracting discounts and contractual terms through competitive tenders that compress margins; fleet orders often dictate product specs and stringent after-sales SLAs, and losing a single national account can shave double-digit percentage volume from a regional sales book, materially affecting revenue and dealer network cash flow.

Dealer network intermediation

Dealers aggregate demand and negotiate pricing and service commitments on behalf of customers, materially shaping JCB's transaction terms; as of 2024 JCB's network exceeds 2,000 dealer outlets across 150 countries, concentrating bargaining power at the intermediary level. Strong dealer relationships and value-added services—financing, parts, training—can buffer price pressure and protect margins. Weak dealer coverage or patchy performance increases buyer leverage by lowering switching frictions, making JCB highly reliant on dealer execution to sustain pricing power.

Price transparency and benchmarking

Global rivals and online channels make cross-quote comparisons routine, as the construction equipment market (about USD 187 billion in 2024) sees digital listings surge; buyers now benchmark total cost of ownership across brands, pressing for stronger warranties, financing and residual-value support. Transparent specs narrow differentiation, forcing JCB to justify any premium via measurable gains in productivity, uptime and telematics-driven insights (telematics adoption ~40% in 2024).

High switching but TCO focus

Switching brands involves operator retraining, spare-parts stocking and fleet integration costs, so buyers weigh reliability, fuel economy and resale uplift; many customers switch despite these frictions when uptime or lifecycle cost advantages exceed transition expense. Procurement decisions are TCO-driven in 2024, lowering pure price sensitivity, while JCB’s global service footprint — over 700 dealer outlets — and uptime guarantees constrain buyer bargaining power.

- Operator training, parts, integration

- Switches for reliability/fuel/resale

- TCO reduces price-only buying

- 700+ dealers (2024) limit buyer leverage

Cyclical demand amplifiers

In downturns excess capacity shifts bargaining power to buyers, forcing JCB into discounts and incentives; in upcycles tight supply and lead times reduce buyer leverage. Rental channels and fleets buffer swings but demand remains cyclical, and flexible financing plus buyback programs help preserve pricing discipline and residual values.

- Downturns: buyer discounts

- Upcycles: tighter supply

- Rental buffers volatility

- Financing/buybacks stabilize pricing

Bulk tenders, dealer finance and telematics reshape equipment margins and TCO

Large contractors, rental firms and public agencies exert strong bargaining power via bulk tenders, driving discounts and strict SLAs that can cut regional volumes by double digits. Dealers (JCB network ~2,000 outlets in 150 countries in 2024) aggregate customer leverage but also protect margins through financing, parts and uptime guarantees. Transparent TCO benchmarking (market ~USD 187bn; telematics adoption ~40% in 2024) raises service and residual-value demands.

| Metric | 2024 value |

|---|---|

| Global market size | USD 187bn |

| JCB dealer outlets | ~2,000 |

| Telematics adoption | ~40% |

Preview Before You Purchase

J.C. Bamford Excavators Limited (JCB) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for J.C. Bamford Excavators Limited you'll receive immediately after purchase—fully formatted and ready to use. It assesses industry rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for JCB's competitive positioning and margins.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

J.C. Bamford Excavators Limited (JCB) faces moderate rivalry from global OEMs, strong supplier influence on specialized components, and shifting buyer power as projects demand integrated solutions. Barriers to entry remain high but technology and rental models raise substitute risks. This snapshot highlights strategic pressure points—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical components

Hydraulics, advanced electronics and high‑spec steels for JCB come from a concentrated Tier‑1 base, giving select suppliers pricing and lead‑time leverage; in 2024 heavy‑equipment suppliers reported average lead times of ~20–24 weeks. Long qualification cycles driven by safety/durability standards slow switching, tightening supply in upcycles; JCB counters with approved‑vendor lists and dual‑sourcing where feasible.

Switching costs and requalification

Switching core parts such as pumps, ECUs and engines requires redesign, testing and certification, imposing high switching costs that strengthen incumbent suppliers. These costs grant suppliers bargaining power despite JCB’s 2024 engineering scale enabling partial standardization to reduce lock-in across platforms. Mission-critical components typically still need multi-month requalification (commonly 6–18 months), preserving supplier leverage.

Commodity volatility passthrough

Steel, energy and freight volatility can strengthen supplier hand during spikes, and JCB's contracts commonly include surcharges that pass costs downstream; the group uses hedging and multiyear supply agreements to smooth input costs, but sudden shocks can compress margins before prices are adjusted.

Vertical integration offsets

By 2024 JCB’s in-house engines and key attachments reduce dependence on external suppliers, improving supply assurance and strengthening negotiation leverage with outside vendors. Internal capacity delivers tighter cost control and enables product differentiation through bespoke integrations. Yet specialist supplier ecosystems remain essential for many advanced components and materials.

- In-house engines: improved supply assurance

- Cost control: lower variable procurement exposure

- Product differentiation: proprietary attachments

- Limit: cannot replace specialist suppliers

Emerging tech dependencies

Electrification, batteries, sensors and telematics raise JCB’s reliance on specialized vendors, concentrating leverage with specialists; top-5 battery cell makers controlled about 80% of global supply in 2024, with CATL ~37% (SNE Research 2024). Certification and safety regimes slow supplier turnover, while strategic partnerships secure access and roadmap alignment.

- Battery concentration: top-5 ≈80% (2024)

- Certification barrier: slows supplier replacement

- Partnerships: secure supply and tech alignment

20–24 weeks avg lead times; top-5 battery cells ≈80%

Concentrated Tier‑1 suppliers and long qualification cycles (6–18 months) give suppliers pricing and lead‑time leverage; average lead times ~20–24 weeks in 2024. JCB reduces exposure via approved vendors, dual‑sourcing and in‑house engines/attachments, but specialist EV components concentrate power (top‑5 battery cell makers ≈80%, CATL ≈37% in 2024).

| Metric | 2024 Value |

|---|---|

| Avg lead time | 20–24 weeks |

| Requalification | 6–18 months |

| Battery vendor concentration | Top‑5 ≈80% (CATL ≈37%) |

What is included in the product

Tailored Porter’s Five Forces analysis for J.C. Bamford Excavators Limited (JCB) uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/technology-driven disruption to assess pricing power, margins, and barriers protecting JCB’s market position.

A one-sheet Porter’s Five Forces analysis for J.C. Bamford Excavators pinpoints supplier, buyer, rivalry, substitutes and entry pain points and strategic levers; customizable pressure levels and clean visuals make it deck- and dashboard-ready.

Customers Bargaining Power

Large fleet buyers and governments

Major contractors, rental houses and public agencies buy JCB machines in large volumes, extracting discounts and contractual terms through competitive tenders that compress margins; fleet orders often dictate product specs and stringent after-sales SLAs, and losing a single national account can shave double-digit percentage volume from a regional sales book, materially affecting revenue and dealer network cash flow.

Dealer network intermediation

Dealers aggregate demand and negotiate pricing and service commitments on behalf of customers, materially shaping JCB's transaction terms; as of 2024 JCB's network exceeds 2,000 dealer outlets across 150 countries, concentrating bargaining power at the intermediary level. Strong dealer relationships and value-added services—financing, parts, training—can buffer price pressure and protect margins. Weak dealer coverage or patchy performance increases buyer leverage by lowering switching frictions, making JCB highly reliant on dealer execution to sustain pricing power.

Price transparency and benchmarking

Global rivals and online channels make cross-quote comparisons routine, as the construction equipment market (about USD 187 billion in 2024) sees digital listings surge; buyers now benchmark total cost of ownership across brands, pressing for stronger warranties, financing and residual-value support. Transparent specs narrow differentiation, forcing JCB to justify any premium via measurable gains in productivity, uptime and telematics-driven insights (telematics adoption ~40% in 2024).

High switching but TCO focus

Switching brands involves operator retraining, spare-parts stocking and fleet integration costs, so buyers weigh reliability, fuel economy and resale uplift; many customers switch despite these frictions when uptime or lifecycle cost advantages exceed transition expense. Procurement decisions are TCO-driven in 2024, lowering pure price sensitivity, while JCB’s global service footprint — over 700 dealer outlets — and uptime guarantees constrain buyer bargaining power.

- Operator training, parts, integration

- Switches for reliability/fuel/resale

- TCO reduces price-only buying

- 700+ dealers (2024) limit buyer leverage

Cyclical demand amplifiers

In downturns excess capacity shifts bargaining power to buyers, forcing JCB into discounts and incentives; in upcycles tight supply and lead times reduce buyer leverage. Rental channels and fleets buffer swings but demand remains cyclical, and flexible financing plus buyback programs help preserve pricing discipline and residual values.

- Downturns: buyer discounts

- Upcycles: tighter supply

- Rental buffers volatility

- Financing/buybacks stabilize pricing

Bulk tenders, dealer finance and telematics reshape equipment margins and TCO

Large contractors, rental firms and public agencies exert strong bargaining power via bulk tenders, driving discounts and strict SLAs that can cut regional volumes by double digits. Dealers (JCB network ~2,000 outlets in 150 countries in 2024) aggregate customer leverage but also protect margins through financing, parts and uptime guarantees. Transparent TCO benchmarking (market ~USD 187bn; telematics adoption ~40% in 2024) raises service and residual-value demands.

| Metric | 2024 value |

|---|---|

| Global market size | USD 187bn |

| JCB dealer outlets | ~2,000 |

| Telematics adoption | ~40% |

Preview Before You Purchase

J.C. Bamford Excavators Limited (JCB) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for J.C. Bamford Excavators Limited you'll receive immediately after purchase—fully formatted and ready to use. It assesses industry rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for JCB's competitive positioning and margins.