J. Crew PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, consumer trends, and sustainability pressures are reshaping J. Crew’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Gain actionable context on risks and opportunities to refine your decisions. Purchase the full, editable PESTLE for a complete, instantly downloadable analysis.

Political factors

Trade policy and tariffs

Changes in U.S. Section 301 tariffs and EU tariff measures directly raise landed costs for J.Crew, Madewell and Factory, squeezing gross margins unless absorbed or passed to consumers. Shifts in trade relations with China, Vietnam or India force supplier rebalancing and can trigger margin resets and longer lead times. Preferential trade programs such as GSP exclusions or reinstatements materially alter sourcing math and timing. Scenario planning for tariff volatility is essential to protect gross margins.

Geopolitical supply risk

Regional instability, port disruptions and chokepoints can delay seasonal assortments and erode full-price sell-through. Suez Canal handles about 12% of global trade and the 2021 Ever Given blockage disrupted roughly $9.6 billion/day of trade, underscoring Asia sourcing exposure. Diversifying country mix and nearshoring mitigate risk but add complexity and cost; insurance and inventory buffers trade off against cash conversion while transparent contingency sourcing supports continuity across brands.

Labor standards in sourcing hubs

Government enforcement of factory labor, wage and safety standards varies widely across Asia and Latin America, with Asia accounting for over 60% of global apparel exports (UN Comtrade 2023). Political pressure has increased audits and remediation cycles and raised potential exit costs from noncompliant suppliers as import authorities ramp up enforcement. For premium brands like J Crew, robust compliance programs materially reduce reputational risk and exposure to public procurement disclosures that are increasingly politically salient.

Minimum wage and incentives

Domestic wage floors (federal $7.25/hr) and state minima up to about $16/hr (California) raise store labor costs and drive DC/site choices; policy shifts in NY and CA curb scheduling flexibility, forcing more staff per shift. Hiring/training credits such as WOTC (commonly up to $2,400, up to $9,600 for select groups) can offset hourly inflation; NRF and retail coalitions lobby for pragmatic implementation.

- Wage pressure: federal $7.25; state highs ~16

- Scheduling rules affect staffing models

- WOTC credits reduce net labor expense

- Retail coalitions influence policy rollout

Tax and fiscal policy

Federal corporate tax remains 21% and net interest deductibility is limited to 30% of adjusted taxable income (IRC 163(j)), while the OECD GloBE minimum tax set a 15% floor—factors that reshape capital allocation and pricing; digital services taxes and local DSTs add complexity. After South Dakota v. Wayfair (2018) most states use nexus thresholds like $100,000 or 200 transactions for sales tax; tax holidays (eg back-to-school) cause traffic spikes and inventory planning challenges, so monitoring multistate changes is critical for omnichannel optimization.

- Corporate tax 21%

- Interest cap 30% (IRC 163(j))

- OECD minimum tax 15%

- Wayfair nexus: $100k/200 txns common

- Tax holidays → traffic spikes, inventory risk

Tariffs, chokepoints and wage/tax shifts squeeze margins; plan scenarios and nearshoring tradeoffs

Tariff shifts (US Section 301, EU measures) raise landed costs and squeeze margins; scenario planning and price elasticity analysis are essential. Geopolitical chokepoints and supplier-country risk (Suez ~12% global trade) threaten seasonal fill rates; nearshoring raises costs but lowers lead times. Labor, compliance and tax changes (federal min wage 7.25; CA ~16; corporate tax 21%; OECD GloBE 15%) reshape operating expense and sourcing.

| Metric | Value |

|---|---|

| Suez share | ~12% |

| Ever Given impact | $9.6B/day |

| Asia apparel exports | >60% (UN Comtrade 2023) |

| Fed min wage | $7.25 |

| CA min wage | ~$16 |

| Corp tax | 21% |

| OECD GloBE | 15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect J. Crew across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, it includes detailed sub-points, forward-looking insights and scenario guidance ready for business plans, decks and strategic decision-making.

A concise, PESTLE-segmented summary of J.Crew’s external risks and opportunities, ready to drop into presentations or share across teams; editable notes let users tailor insights by region or product line to support strategic planning and risk mitigation.

Economic factors

Consumer spending cycles

Apparel demand is highly discretionary and closely tracks real disposable personal income (up ~1.8% in 2024) and labor market strength (U.S. unemployment ~3.7% in 2025), with consumer confidence recovering to near 2021 levels. J.Crew’s classic positioning depends on full-price sell-through, while J.Crew Factory provides value elasticity in downturns. Broad assortment lets customers trade up or down without attrition, and disciplined promotional cadence preserves brand equity through cycles.

Inflation and input costs

Cotton futures near $0.90/lb, wool EMI around AU$10/kg and hides/leather costs up ~10% year-over-year, while diesel averaged ~$3.80/gal and Shanghai–LA spot 40ft rates hovered near $2,000/FEU in 2024, swinging J.Crew COGS and receipt timing. Persistent inflation lifts AURs by mid-single digits and can nudge apparel return rates above the typical ~15%. Vendor renegotiation and design-to-cost protect margins without diluting quality cues; early raw-material commitments hedge price volatility but raise demand-mismatch risk.

FX and sourcing currencies

Dollar strength—US Dollar Index rose roughly 8% in 2022–23—lowers dollar-denominated import costs for J.Crew but can compress export and tourist-driven sales abroad. Currency volatility in supplier markets (China, Vietnam, Bangladesh) feeds through to FOB prices and tighter payment terms from factories. Diversified sourcing across multiple countries creates natural hedges that help stabilize gross margins. Layered hedging policies (typical 6–12 month forward coverage) balance cost and flexibility.

Interest rates and credit

Higher policy rates (federal funds ~5.25–5.50% in mid‑2025) raise J. Crew’s working capital and inventory carrying costs and squeeze margins; tighter consumer credit and elevated card APRs (~20%+) reduce basket size for big-ticket outerwear and boots. Madewell denim sales show resilience but cannot fully offset macro tightening. Leaner inventory and faster turns cut financing needs and interest exposure.

- Higher policy rate: ~5.25–5.50% (mid‑2025)

- Card APRs elevated: ~20%+

- Madewell offsets part of decline

- Lean inventory = lower financing need

E-commerce growth and mix

Online growth expands J.Crew’s reach but carries e-commerce apparel return rates that often exceed 20% and higher last-mile costs; well-executed omnichannel features raise conversion and store productivity. Profitability hinges on packaging, routing and dynamic markdowns, while data-driven allocation aligning digital and store demand limits margin leakage.

- returns >20%

- omnichannel → higher conversion & store productivity

- profitability levers: packaging, routing, markdowns

- data-driven allocation limits margin leakage

Tariffs, chokepoints and wage/tax shifts squeeze margins; plan scenarios and nearshoring tradeoffs

Apparel demand tracks real disposable income (+1.8% in 2024) and low unemployment (~3.7% in 2025), supporting J.Crew full-price mix while Factory provides downside elasticity. Inflation, cotton ~$0.90/lb and diesel ~$3.80/gal lift COGS; fed funds ~5.25–5.50% and card APRs ~20%+ raise carrying costs. Online returns >20% strain margins; omnichannel and lean inventory improve turns.

| Metric | Value (2024–mid‑2025) |

|---|---|

| Real DPI growth | +1.8% |

| Unemployment | ~3.7% |

| Fed funds | 5.25–5.50% |

| Cotton | $0.90/lb |

| Diesel | $3.80/gal |

| Returns | >20% |

What You See Is What You Get

J. Crew PESTLE Analysis

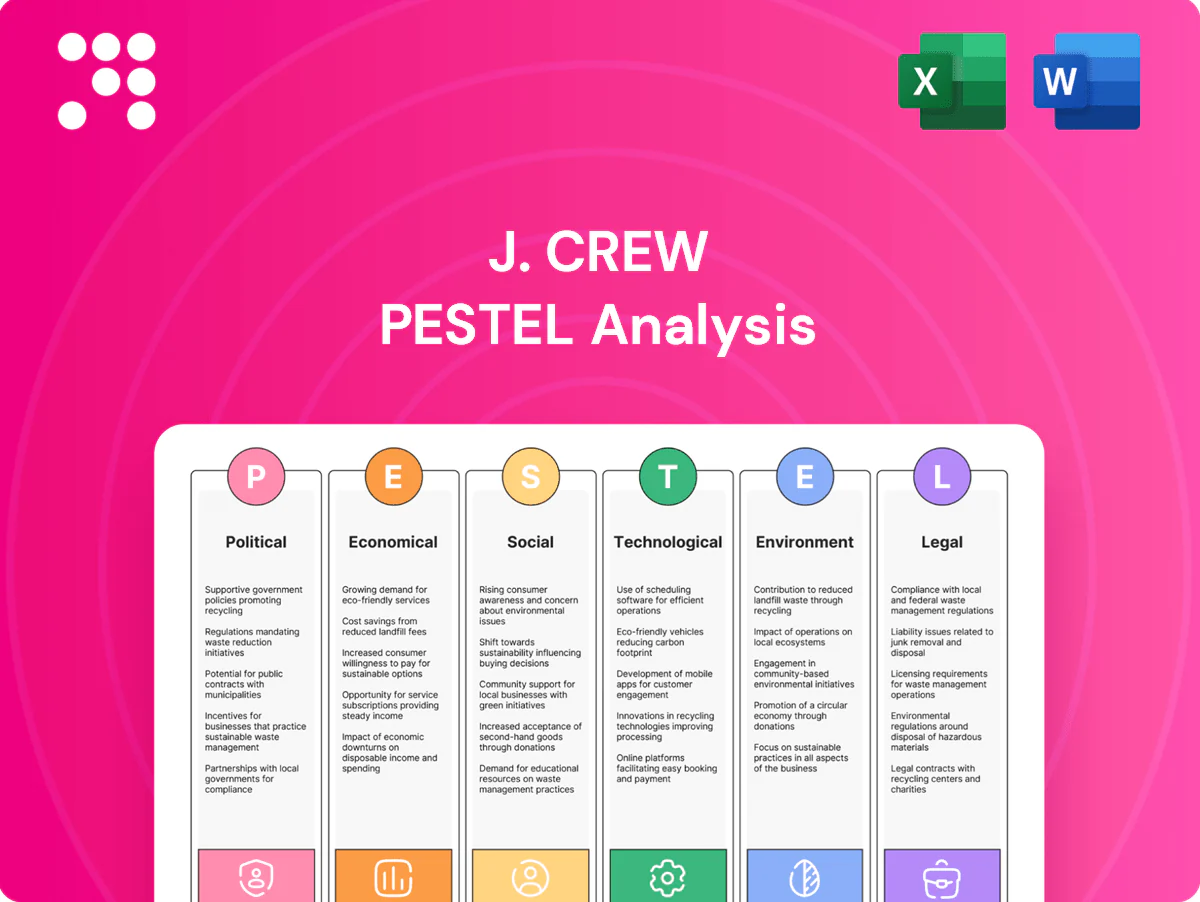

The J. Crew PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase, covering political, economic, social, technological, legal, and environmental factors tailored to J. Crew. The layout, content, and structure are final and ready to download. No placeholders or surprises—this is the real file you’ll own after checkout.

Your Competitive Advantage Starts with This Report

Unlock how political shifts, consumer trends, and sustainability pressures are reshaping J. Crew’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Gain actionable context on risks and opportunities to refine your decisions. Purchase the full, editable PESTLE for a complete, instantly downloadable analysis.

Political factors

Trade policy and tariffs

Changes in U.S. Section 301 tariffs and EU tariff measures directly raise landed costs for J.Crew, Madewell and Factory, squeezing gross margins unless absorbed or passed to consumers. Shifts in trade relations with China, Vietnam or India force supplier rebalancing and can trigger margin resets and longer lead times. Preferential trade programs such as GSP exclusions or reinstatements materially alter sourcing math and timing. Scenario planning for tariff volatility is essential to protect gross margins.

Geopolitical supply risk

Regional instability, port disruptions and chokepoints can delay seasonal assortments and erode full-price sell-through. Suez Canal handles about 12% of global trade and the 2021 Ever Given blockage disrupted roughly $9.6 billion/day of trade, underscoring Asia sourcing exposure. Diversifying country mix and nearshoring mitigate risk but add complexity and cost; insurance and inventory buffers trade off against cash conversion while transparent contingency sourcing supports continuity across brands.

Labor standards in sourcing hubs

Government enforcement of factory labor, wage and safety standards varies widely across Asia and Latin America, with Asia accounting for over 60% of global apparel exports (UN Comtrade 2023). Political pressure has increased audits and remediation cycles and raised potential exit costs from noncompliant suppliers as import authorities ramp up enforcement. For premium brands like J Crew, robust compliance programs materially reduce reputational risk and exposure to public procurement disclosures that are increasingly politically salient.

Minimum wage and incentives

Domestic wage floors (federal $7.25/hr) and state minima up to about $16/hr (California) raise store labor costs and drive DC/site choices; policy shifts in NY and CA curb scheduling flexibility, forcing more staff per shift. Hiring/training credits such as WOTC (commonly up to $2,400, up to $9,600 for select groups) can offset hourly inflation; NRF and retail coalitions lobby for pragmatic implementation.

- Wage pressure: federal $7.25; state highs ~16

- Scheduling rules affect staffing models

- WOTC credits reduce net labor expense

- Retail coalitions influence policy rollout

Tax and fiscal policy

Federal corporate tax remains 21% and net interest deductibility is limited to 30% of adjusted taxable income (IRC 163(j)), while the OECD GloBE minimum tax set a 15% floor—factors that reshape capital allocation and pricing; digital services taxes and local DSTs add complexity. After South Dakota v. Wayfair (2018) most states use nexus thresholds like $100,000 or 200 transactions for sales tax; tax holidays (eg back-to-school) cause traffic spikes and inventory planning challenges, so monitoring multistate changes is critical for omnichannel optimization.

- Corporate tax 21%

- Interest cap 30% (IRC 163(j))

- OECD minimum tax 15%

- Wayfair nexus: $100k/200 txns common

- Tax holidays → traffic spikes, inventory risk

Tariffs, chokepoints and wage/tax shifts squeeze margins; plan scenarios and nearshoring tradeoffs

Tariff shifts (US Section 301, EU measures) raise landed costs and squeeze margins; scenario planning and price elasticity analysis are essential. Geopolitical chokepoints and supplier-country risk (Suez ~12% global trade) threaten seasonal fill rates; nearshoring raises costs but lowers lead times. Labor, compliance and tax changes (federal min wage 7.25; CA ~16; corporate tax 21%; OECD GloBE 15%) reshape operating expense and sourcing.

| Metric | Value |

|---|---|

| Suez share | ~12% |

| Ever Given impact | $9.6B/day |

| Asia apparel exports | >60% (UN Comtrade 2023) |

| Fed min wage | $7.25 |

| CA min wage | ~$16 |

| Corp tax | 21% |

| OECD GloBE | 15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect J. Crew across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, it includes detailed sub-points, forward-looking insights and scenario guidance ready for business plans, decks and strategic decision-making.

A concise, PESTLE-segmented summary of J.Crew’s external risks and opportunities, ready to drop into presentations or share across teams; editable notes let users tailor insights by region or product line to support strategic planning and risk mitigation.

Economic factors

Consumer spending cycles

Apparel demand is highly discretionary and closely tracks real disposable personal income (up ~1.8% in 2024) and labor market strength (U.S. unemployment ~3.7% in 2025), with consumer confidence recovering to near 2021 levels. J.Crew’s classic positioning depends on full-price sell-through, while J.Crew Factory provides value elasticity in downturns. Broad assortment lets customers trade up or down without attrition, and disciplined promotional cadence preserves brand equity through cycles.

Inflation and input costs

Cotton futures near $0.90/lb, wool EMI around AU$10/kg and hides/leather costs up ~10% year-over-year, while diesel averaged ~$3.80/gal and Shanghai–LA spot 40ft rates hovered near $2,000/FEU in 2024, swinging J.Crew COGS and receipt timing. Persistent inflation lifts AURs by mid-single digits and can nudge apparel return rates above the typical ~15%. Vendor renegotiation and design-to-cost protect margins without diluting quality cues; early raw-material commitments hedge price volatility but raise demand-mismatch risk.

FX and sourcing currencies

Dollar strength—US Dollar Index rose roughly 8% in 2022–23—lowers dollar-denominated import costs for J.Crew but can compress export and tourist-driven sales abroad. Currency volatility in supplier markets (China, Vietnam, Bangladesh) feeds through to FOB prices and tighter payment terms from factories. Diversified sourcing across multiple countries creates natural hedges that help stabilize gross margins. Layered hedging policies (typical 6–12 month forward coverage) balance cost and flexibility.

Interest rates and credit

Higher policy rates (federal funds ~5.25–5.50% in mid‑2025) raise J. Crew’s working capital and inventory carrying costs and squeeze margins; tighter consumer credit and elevated card APRs (~20%+) reduce basket size for big-ticket outerwear and boots. Madewell denim sales show resilience but cannot fully offset macro tightening. Leaner inventory and faster turns cut financing needs and interest exposure.

- Higher policy rate: ~5.25–5.50% (mid‑2025)

- Card APRs elevated: ~20%+

- Madewell offsets part of decline

- Lean inventory = lower financing need

E-commerce growth and mix

Online growth expands J.Crew’s reach but carries e-commerce apparel return rates that often exceed 20% and higher last-mile costs; well-executed omnichannel features raise conversion and store productivity. Profitability hinges on packaging, routing and dynamic markdowns, while data-driven allocation aligning digital and store demand limits margin leakage.

- returns >20%

- omnichannel → higher conversion & store productivity

- profitability levers: packaging, routing, markdowns

- data-driven allocation limits margin leakage

Tariffs, chokepoints and wage/tax shifts squeeze margins; plan scenarios and nearshoring tradeoffs

Apparel demand tracks real disposable income (+1.8% in 2024) and low unemployment (~3.7% in 2025), supporting J.Crew full-price mix while Factory provides downside elasticity. Inflation, cotton ~$0.90/lb and diesel ~$3.80/gal lift COGS; fed funds ~5.25–5.50% and card APRs ~20%+ raise carrying costs. Online returns >20% strain margins; omnichannel and lean inventory improve turns.

| Metric | Value (2024–mid‑2025) |

|---|---|

| Real DPI growth | +1.8% |

| Unemployment | ~3.7% |

| Fed funds | 5.25–5.50% |

| Cotton | $0.90/lb |

| Diesel | $3.80/gal |

| Returns | >20% |

What You See Is What You Get

J. Crew PESTLE Analysis

The J. Crew PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase, covering political, economic, social, technological, legal, and environmental factors tailored to J. Crew. The layout, content, and structure are final and ready to download. No placeholders or surprises—this is the real file you’ll own after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, consumer trends, and sustainability pressures are reshaping J. Crew’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Gain actionable context on risks and opportunities to refine your decisions. Purchase the full, editable PESTLE for a complete, instantly downloadable analysis.

Political factors

Trade policy and tariffs

Changes in U.S. Section 301 tariffs and EU tariff measures directly raise landed costs for J.Crew, Madewell and Factory, squeezing gross margins unless absorbed or passed to consumers. Shifts in trade relations with China, Vietnam or India force supplier rebalancing and can trigger margin resets and longer lead times. Preferential trade programs such as GSP exclusions or reinstatements materially alter sourcing math and timing. Scenario planning for tariff volatility is essential to protect gross margins.

Geopolitical supply risk

Regional instability, port disruptions and chokepoints can delay seasonal assortments and erode full-price sell-through. Suez Canal handles about 12% of global trade and the 2021 Ever Given blockage disrupted roughly $9.6 billion/day of trade, underscoring Asia sourcing exposure. Diversifying country mix and nearshoring mitigate risk but add complexity and cost; insurance and inventory buffers trade off against cash conversion while transparent contingency sourcing supports continuity across brands.

Labor standards in sourcing hubs

Government enforcement of factory labor, wage and safety standards varies widely across Asia and Latin America, with Asia accounting for over 60% of global apparel exports (UN Comtrade 2023). Political pressure has increased audits and remediation cycles and raised potential exit costs from noncompliant suppliers as import authorities ramp up enforcement. For premium brands like J Crew, robust compliance programs materially reduce reputational risk and exposure to public procurement disclosures that are increasingly politically salient.

Minimum wage and incentives

Domestic wage floors (federal $7.25/hr) and state minima up to about $16/hr (California) raise store labor costs and drive DC/site choices; policy shifts in NY and CA curb scheduling flexibility, forcing more staff per shift. Hiring/training credits such as WOTC (commonly up to $2,400, up to $9,600 for select groups) can offset hourly inflation; NRF and retail coalitions lobby for pragmatic implementation.

- Wage pressure: federal $7.25; state highs ~16

- Scheduling rules affect staffing models

- WOTC credits reduce net labor expense

- Retail coalitions influence policy rollout

Tax and fiscal policy

Federal corporate tax remains 21% and net interest deductibility is limited to 30% of adjusted taxable income (IRC 163(j)), while the OECD GloBE minimum tax set a 15% floor—factors that reshape capital allocation and pricing; digital services taxes and local DSTs add complexity. After South Dakota v. Wayfair (2018) most states use nexus thresholds like $100,000 or 200 transactions for sales tax; tax holidays (eg back-to-school) cause traffic spikes and inventory planning challenges, so monitoring multistate changes is critical for omnichannel optimization.

- Corporate tax 21%

- Interest cap 30% (IRC 163(j))

- OECD minimum tax 15%

- Wayfair nexus: $100k/200 txns common

- Tax holidays → traffic spikes, inventory risk

Tariffs, chokepoints and wage/tax shifts squeeze margins; plan scenarios and nearshoring tradeoffs

Tariff shifts (US Section 301, EU measures) raise landed costs and squeeze margins; scenario planning and price elasticity analysis are essential. Geopolitical chokepoints and supplier-country risk (Suez ~12% global trade) threaten seasonal fill rates; nearshoring raises costs but lowers lead times. Labor, compliance and tax changes (federal min wage 7.25; CA ~16; corporate tax 21%; OECD GloBE 15%) reshape operating expense and sourcing.

| Metric | Value |

|---|---|

| Suez share | ~12% |

| Ever Given impact | $9.6B/day |

| Asia apparel exports | >60% (UN Comtrade 2023) |

| Fed min wage | $7.25 |

| CA min wage | ~$16 |

| Corp tax | 21% |

| OECD GloBE | 15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect J. Crew across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, consultants and investors, it includes detailed sub-points, forward-looking insights and scenario guidance ready for business plans, decks and strategic decision-making.

A concise, PESTLE-segmented summary of J.Crew’s external risks and opportunities, ready to drop into presentations or share across teams; editable notes let users tailor insights by region or product line to support strategic planning and risk mitigation.

Economic factors

Consumer spending cycles

Apparel demand is highly discretionary and closely tracks real disposable personal income (up ~1.8% in 2024) and labor market strength (U.S. unemployment ~3.7% in 2025), with consumer confidence recovering to near 2021 levels. J.Crew’s classic positioning depends on full-price sell-through, while J.Crew Factory provides value elasticity in downturns. Broad assortment lets customers trade up or down without attrition, and disciplined promotional cadence preserves brand equity through cycles.

Inflation and input costs

Cotton futures near $0.90/lb, wool EMI around AU$10/kg and hides/leather costs up ~10% year-over-year, while diesel averaged ~$3.80/gal and Shanghai–LA spot 40ft rates hovered near $2,000/FEU in 2024, swinging J.Crew COGS and receipt timing. Persistent inflation lifts AURs by mid-single digits and can nudge apparel return rates above the typical ~15%. Vendor renegotiation and design-to-cost protect margins without diluting quality cues; early raw-material commitments hedge price volatility but raise demand-mismatch risk.

FX and sourcing currencies

Dollar strength—US Dollar Index rose roughly 8% in 2022–23—lowers dollar-denominated import costs for J.Crew but can compress export and tourist-driven sales abroad. Currency volatility in supplier markets (China, Vietnam, Bangladesh) feeds through to FOB prices and tighter payment terms from factories. Diversified sourcing across multiple countries creates natural hedges that help stabilize gross margins. Layered hedging policies (typical 6–12 month forward coverage) balance cost and flexibility.

Interest rates and credit

Higher policy rates (federal funds ~5.25–5.50% in mid‑2025) raise J. Crew’s working capital and inventory carrying costs and squeeze margins; tighter consumer credit and elevated card APRs (~20%+) reduce basket size for big-ticket outerwear and boots. Madewell denim sales show resilience but cannot fully offset macro tightening. Leaner inventory and faster turns cut financing needs and interest exposure.

- Higher policy rate: ~5.25–5.50% (mid‑2025)

- Card APRs elevated: ~20%+

- Madewell offsets part of decline

- Lean inventory = lower financing need

E-commerce growth and mix

Online growth expands J.Crew’s reach but carries e-commerce apparel return rates that often exceed 20% and higher last-mile costs; well-executed omnichannel features raise conversion and store productivity. Profitability hinges on packaging, routing and dynamic markdowns, while data-driven allocation aligning digital and store demand limits margin leakage.

- returns >20%

- omnichannel → higher conversion & store productivity

- profitability levers: packaging, routing, markdowns

- data-driven allocation limits margin leakage

Tariffs, chokepoints and wage/tax shifts squeeze margins; plan scenarios and nearshoring tradeoffs

Apparel demand tracks real disposable income (+1.8% in 2024) and low unemployment (~3.7% in 2025), supporting J.Crew full-price mix while Factory provides downside elasticity. Inflation, cotton ~$0.90/lb and diesel ~$3.80/gal lift COGS; fed funds ~5.25–5.50% and card APRs ~20%+ raise carrying costs. Online returns >20% strain margins; omnichannel and lean inventory improve turns.

| Metric | Value (2024–mid‑2025) |

|---|---|

| Real DPI growth | +1.8% |

| Unemployment | ~3.7% |

| Fed funds | 5.25–5.50% |

| Cotton | $0.90/lb |

| Diesel | $3.80/gal |

| Returns | >20% |

What You See Is What You Get

J. Crew PESTLE Analysis

The J. Crew PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase, covering political, economic, social, technological, legal, and environmental factors tailored to J. Crew. The layout, content, and structure are final and ready to download. No placeholders or surprises—this is the real file you’ll own after checkout.