JE Dunn Construction Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

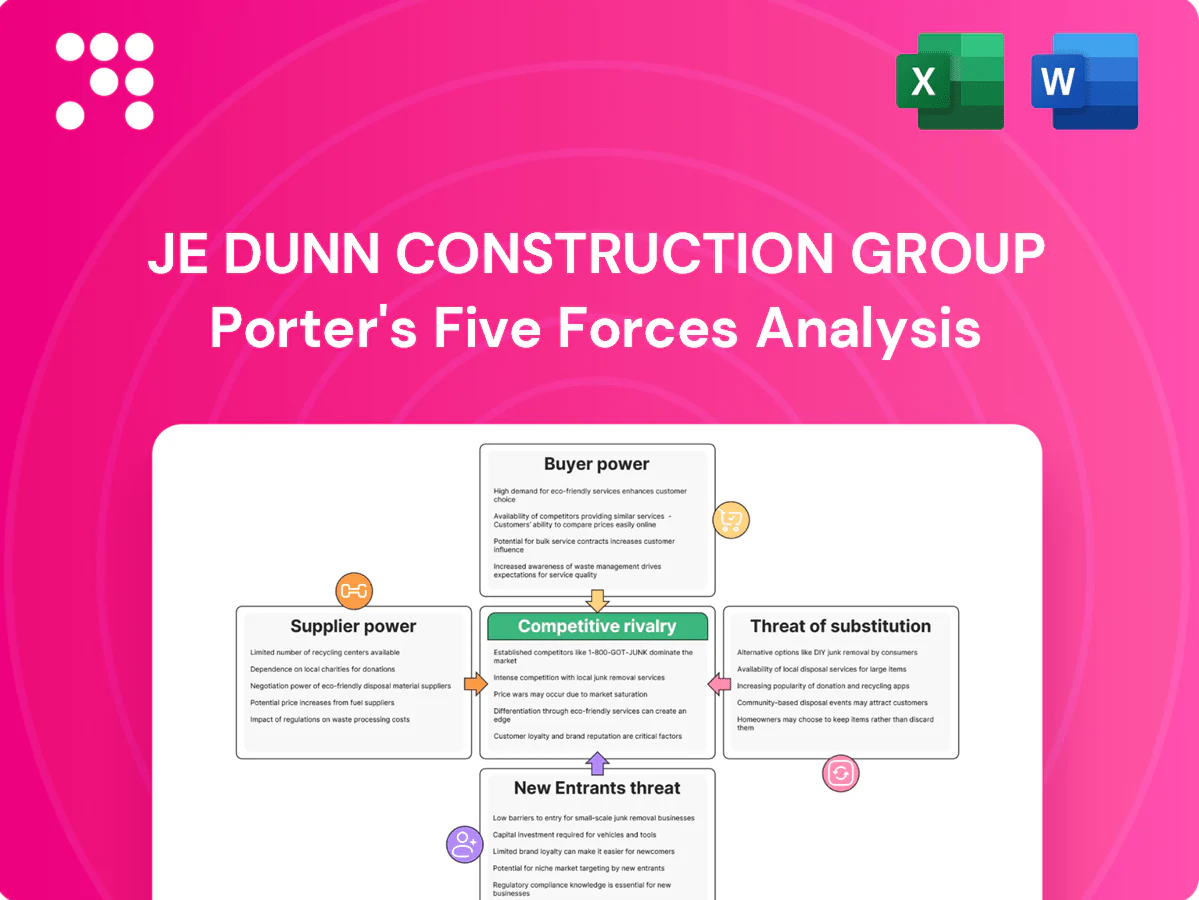

JE Dunn Construction Group faces moderate supplier leverage, strong buyer expectations, and disruptive competitive pressures that shape margins and growth prospects. Our snapshot highlights where strategic advantage can be gained—from bidding dynamics to scale benefits. This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JE Dunn’s competitive dynamics and actionable insights in depth.

Suppliers Bargaining Power

Critical materials volatility

Steel, concrete, and electrical gear suppliers can exert power through price swings and allocations, with long-lead items often facing 12–30 week waits that amplify mid-project switching costs. JE Dunn uses prebuying, value engineering, and diversified sourcing to hedge volatility. Despite these measures, sudden shortages in 2024 still pressured margins on select projects.

Specialty subcontractor concentration

Skilled trades such as MEP, façade, and life-safety are often capacity-constrained locally, with the AGC 2024 survey reporting about 79% of contractors citing difficulty hiring craftworkers, increasing subcontractor leverage on pricing and schedules. Limited qualified subs push up bid premiums and schedule risk for JE Dunn projects. Deep relationships and preferred-partner programs help moderate this power, but peak-demand periods clearly shift bargaining toward subs.

Union and labor dynamics

Labor unions and craft availability shape JE Dunn’s wage rates and work rules, with 2024 construction labor tightness increasing bargaining leverage for organized trades. Tight markets elevate labor costs and heighten schedule slippage risk across projects. Workforce development programs and multi-market staffing strategies reduce exposure, yet project-critical trades retain strong negotiating power.

Equipment and tech dependencies

Crane, heavy‑equipment lessors and BIM/VDC software providers create notable switching frictions for JE Dunn as proprietary ecosystems and operator training raise supplier power; BIM adoption in US construction reached ~60% in 2024, reinforcing lock‑ins. Long‑term rentals and fleet planning can lower daily rates by roughly 10–20%, but niche tools or perpetual licenses still command premiums.

- High switching cost

- 60% BIM adoption (2024)

- Long‑term deals cut 10–20%

- Niche licenses = premium

Compliance and certification requirements

Compliance and certification for healthcare, industrial, and federal projects demand certified materials and QA documentation, increasing supplier leverage. Fewer suppliers meeting FDA, UL, Buy American and DOD spec standards tighten supply choices and raise pricing power. Early submittal coordination reduces risk and pricing surprises, while rigid specs limit substitution options.

- Certified materials required

- Supplier scarcity raises bargaining power

- Early submittals mitigate pricing risk

- Spec rigidity limits substitutions

Long lead times and skilled shortages boost supplier pricing power; rentals cut costs 10-20%

Suppliers of steel, concrete, long‑lead electrical gear and certified materials hold pricing and allocation power via 12–30 week lead times and limited spec-compliant sources, pressuring JE Dunn on some 2024 projects. Skilled subcontractor scarcity (AGC 2024: 79% report hiring difficulty) and 60% BIM adoption reinforce switching frictions; long‑term rentals cut equipment costs ~10–20%.

| Factor | 2024 stat/impact |

|---|---|

| Material lead times | 12–30 weeks |

| Skilled craft shortage | AGC 2024: 79% |

| BIM adoption | ~60% |

| Equipment rental savings | 10–20% |

What is included in the product

Tailored Porter's Five Forces for JE Dunn Construction Group, revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share.

A one-sheet Porter's Five Forces for JE Dunn that instantly surfaces competitive pain points—customizable pressure levels and a clear spider chart make strategic gaps and risks easy to prioritize for board decks or rapid decision-making.

Customers Bargaining Power

Owner sophistication

Healthcare systems, universities, and Fortune 500 owners increasingly use data-driven procurement, with 72% of large owners requiring BIM integration by 2024. They demand transparent pricing and schedule certainty, boosting their negotiation leverage. Sophistication allows owners to apply performance scorecards that can reduce award likelihood or lower fees. JE Dunn faces heightened margin pressure as these owners tie payments to measurable outcomes.

Competitive bidding pressure

Hard-bid and CMAR pursuits routinely pit 5–10 GCs against each other, increasing competitive bidding pressure. Increased price visibility in 2024 has pushed realized margins toward industry averages of roughly 3–5%, empowering owners to squeeze bids. Differentiation through robust preconstruction services and rigorous risk management can defend value. Low-bid norms, however, still cap upside on commoditized scopes.

Portfolio and repeat work

Multi-project clients can bundle work and extract favorable terms from JE Dunn, leveraging portfolio buying power and pipeline optionality to increase negotiation leverage. JE Dunn's relationship capital and documented repeat outcomes lower buyer churn and raise switching costs, reinforcing long-term engagements. Use of framework and IDIQ contracts trades modest margin for volume and schedule predictability, while clients with broader pipelines retain the strongest bargaining power.

Delivery method selection

Design-build, IPD, and GMP contracts shift contingency and performance risk onto the contractor, prompting JE Dunn to price for transferred risk and allocate contingencies into bids. Owners use these delivery methods to share or transfer contingencies, while early contractor engagement allows JE Dunn to influence scope, value-engineer, and reduce downstream change orders. Despite contractor influence, buyers ultimately control risk allocation through contract selection and terms.

- Risk transfer: contractor bears contingency exposure

- Early engagement: enables scope and cost influence

- Buyer control: clients set risk allocation via contract form

Schedule and performance incentives

Schedule and performance incentives—liquidated damages, milestone payments, and KPI-based fees—tighten accountability and let buyers enforce cost and time discipline; in 2024 owners increasingly used milestone/KPI clauses to shift risk. JE Dunn’s advanced planning and VDC capabilities position it to meet stringent targets, but high-stakes penalties amplify buyer bargaining power in negotiations.

- Liquidated damages: enforce time discipline

- Milestones: link payments to delivery

- KPI fees: reward/punish performance

- 2024 trend: rising owner use boosts buyer leverage

Owners demand pricing certainty: 72% BIM, margins 3-5%, 5-10 GCs

Large owners (72% required BIM by 2024) demand transparent pricing, schedule certainty and KPI-linked payments, raising negotiation leverage. Typical pursuits pit 5–10 GCs and pushed realized margins toward 3–5% in 2024, compressing bids. Framework/IDIQ deals trade margin for volume while buyers keep leverage via contract form and penalties.

| Metric | 2024 |

|---|---|

| BIM requirement | 72% |

| Realized margins | 3–5% |

| GCs per bid | 5–10 |

Full Version Awaits

JE Dunn Construction Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for JE Dunn Construction Group you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted and ready for download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with evidence-based insights. You’re viewing the final deliverable, available instantly after payment.

A Must-Have Tool for Decision-Makers

JE Dunn Construction Group faces moderate supplier leverage, strong buyer expectations, and disruptive competitive pressures that shape margins and growth prospects. Our snapshot highlights where strategic advantage can be gained—from bidding dynamics to scale benefits. This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JE Dunn’s competitive dynamics and actionable insights in depth.

Suppliers Bargaining Power

Critical materials volatility

Steel, concrete, and electrical gear suppliers can exert power through price swings and allocations, with long-lead items often facing 12–30 week waits that amplify mid-project switching costs. JE Dunn uses prebuying, value engineering, and diversified sourcing to hedge volatility. Despite these measures, sudden shortages in 2024 still pressured margins on select projects.

Specialty subcontractor concentration

Skilled trades such as MEP, façade, and life-safety are often capacity-constrained locally, with the AGC 2024 survey reporting about 79% of contractors citing difficulty hiring craftworkers, increasing subcontractor leverage on pricing and schedules. Limited qualified subs push up bid premiums and schedule risk for JE Dunn projects. Deep relationships and preferred-partner programs help moderate this power, but peak-demand periods clearly shift bargaining toward subs.

Union and labor dynamics

Labor unions and craft availability shape JE Dunn’s wage rates and work rules, with 2024 construction labor tightness increasing bargaining leverage for organized trades. Tight markets elevate labor costs and heighten schedule slippage risk across projects. Workforce development programs and multi-market staffing strategies reduce exposure, yet project-critical trades retain strong negotiating power.

Equipment and tech dependencies

Crane, heavy‑equipment lessors and BIM/VDC software providers create notable switching frictions for JE Dunn as proprietary ecosystems and operator training raise supplier power; BIM adoption in US construction reached ~60% in 2024, reinforcing lock‑ins. Long‑term rentals and fleet planning can lower daily rates by roughly 10–20%, but niche tools or perpetual licenses still command premiums.

- High switching cost

- 60% BIM adoption (2024)

- Long‑term deals cut 10–20%

- Niche licenses = premium

Compliance and certification requirements

Compliance and certification for healthcare, industrial, and federal projects demand certified materials and QA documentation, increasing supplier leverage. Fewer suppliers meeting FDA, UL, Buy American and DOD spec standards tighten supply choices and raise pricing power. Early submittal coordination reduces risk and pricing surprises, while rigid specs limit substitution options.

- Certified materials required

- Supplier scarcity raises bargaining power

- Early submittals mitigate pricing risk

- Spec rigidity limits substitutions

Long lead times and skilled shortages boost supplier pricing power; rentals cut costs 10-20%

Suppliers of steel, concrete, long‑lead electrical gear and certified materials hold pricing and allocation power via 12–30 week lead times and limited spec-compliant sources, pressuring JE Dunn on some 2024 projects. Skilled subcontractor scarcity (AGC 2024: 79% report hiring difficulty) and 60% BIM adoption reinforce switching frictions; long‑term rentals cut equipment costs ~10–20%.

| Factor | 2024 stat/impact |

|---|---|

| Material lead times | 12–30 weeks |

| Skilled craft shortage | AGC 2024: 79% |

| BIM adoption | ~60% |

| Equipment rental savings | 10–20% |

What is included in the product

Tailored Porter's Five Forces for JE Dunn Construction Group, revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share.

A one-sheet Porter's Five Forces for JE Dunn that instantly surfaces competitive pain points—customizable pressure levels and a clear spider chart make strategic gaps and risks easy to prioritize for board decks or rapid decision-making.

Customers Bargaining Power

Owner sophistication

Healthcare systems, universities, and Fortune 500 owners increasingly use data-driven procurement, with 72% of large owners requiring BIM integration by 2024. They demand transparent pricing and schedule certainty, boosting their negotiation leverage. Sophistication allows owners to apply performance scorecards that can reduce award likelihood or lower fees. JE Dunn faces heightened margin pressure as these owners tie payments to measurable outcomes.

Competitive bidding pressure

Hard-bid and CMAR pursuits routinely pit 5–10 GCs against each other, increasing competitive bidding pressure. Increased price visibility in 2024 has pushed realized margins toward industry averages of roughly 3–5%, empowering owners to squeeze bids. Differentiation through robust preconstruction services and rigorous risk management can defend value. Low-bid norms, however, still cap upside on commoditized scopes.

Portfolio and repeat work

Multi-project clients can bundle work and extract favorable terms from JE Dunn, leveraging portfolio buying power and pipeline optionality to increase negotiation leverage. JE Dunn's relationship capital and documented repeat outcomes lower buyer churn and raise switching costs, reinforcing long-term engagements. Use of framework and IDIQ contracts trades modest margin for volume and schedule predictability, while clients with broader pipelines retain the strongest bargaining power.

Delivery method selection

Design-build, IPD, and GMP contracts shift contingency and performance risk onto the contractor, prompting JE Dunn to price for transferred risk and allocate contingencies into bids. Owners use these delivery methods to share or transfer contingencies, while early contractor engagement allows JE Dunn to influence scope, value-engineer, and reduce downstream change orders. Despite contractor influence, buyers ultimately control risk allocation through contract selection and terms.

- Risk transfer: contractor bears contingency exposure

- Early engagement: enables scope and cost influence

- Buyer control: clients set risk allocation via contract form

Schedule and performance incentives

Schedule and performance incentives—liquidated damages, milestone payments, and KPI-based fees—tighten accountability and let buyers enforce cost and time discipline; in 2024 owners increasingly used milestone/KPI clauses to shift risk. JE Dunn’s advanced planning and VDC capabilities position it to meet stringent targets, but high-stakes penalties amplify buyer bargaining power in negotiations.

- Liquidated damages: enforce time discipline

- Milestones: link payments to delivery

- KPI fees: reward/punish performance

- 2024 trend: rising owner use boosts buyer leverage

Owners demand pricing certainty: 72% BIM, margins 3-5%, 5-10 GCs

Large owners (72% required BIM by 2024) demand transparent pricing, schedule certainty and KPI-linked payments, raising negotiation leverage. Typical pursuits pit 5–10 GCs and pushed realized margins toward 3–5% in 2024, compressing bids. Framework/IDIQ deals trade margin for volume while buyers keep leverage via contract form and penalties.

| Metric | 2024 |

|---|---|

| BIM requirement | 72% |

| Realized margins | 3–5% |

| GCs per bid | 5–10 |

Full Version Awaits

JE Dunn Construction Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for JE Dunn Construction Group you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted and ready for download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with evidence-based insights. You’re viewing the final deliverable, available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

JE Dunn Construction Group faces moderate supplier leverage, strong buyer expectations, and disruptive competitive pressures that shape margins and growth prospects. Our snapshot highlights where strategic advantage can be gained—from bidding dynamics to scale benefits. This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JE Dunn’s competitive dynamics and actionable insights in depth.

Suppliers Bargaining Power

Critical materials volatility

Steel, concrete, and electrical gear suppliers can exert power through price swings and allocations, with long-lead items often facing 12–30 week waits that amplify mid-project switching costs. JE Dunn uses prebuying, value engineering, and diversified sourcing to hedge volatility. Despite these measures, sudden shortages in 2024 still pressured margins on select projects.

Specialty subcontractor concentration

Skilled trades such as MEP, façade, and life-safety are often capacity-constrained locally, with the AGC 2024 survey reporting about 79% of contractors citing difficulty hiring craftworkers, increasing subcontractor leverage on pricing and schedules. Limited qualified subs push up bid premiums and schedule risk for JE Dunn projects. Deep relationships and preferred-partner programs help moderate this power, but peak-demand periods clearly shift bargaining toward subs.

Union and labor dynamics

Labor unions and craft availability shape JE Dunn’s wage rates and work rules, with 2024 construction labor tightness increasing bargaining leverage for organized trades. Tight markets elevate labor costs and heighten schedule slippage risk across projects. Workforce development programs and multi-market staffing strategies reduce exposure, yet project-critical trades retain strong negotiating power.

Equipment and tech dependencies

Crane, heavy‑equipment lessors and BIM/VDC software providers create notable switching frictions for JE Dunn as proprietary ecosystems and operator training raise supplier power; BIM adoption in US construction reached ~60% in 2024, reinforcing lock‑ins. Long‑term rentals and fleet planning can lower daily rates by roughly 10–20%, but niche tools or perpetual licenses still command premiums.

- High switching cost

- 60% BIM adoption (2024)

- Long‑term deals cut 10–20%

- Niche licenses = premium

Compliance and certification requirements

Compliance and certification for healthcare, industrial, and federal projects demand certified materials and QA documentation, increasing supplier leverage. Fewer suppliers meeting FDA, UL, Buy American and DOD spec standards tighten supply choices and raise pricing power. Early submittal coordination reduces risk and pricing surprises, while rigid specs limit substitution options.

- Certified materials required

- Supplier scarcity raises bargaining power

- Early submittals mitigate pricing risk

- Spec rigidity limits substitutions

Long lead times and skilled shortages boost supplier pricing power; rentals cut costs 10-20%

Suppliers of steel, concrete, long‑lead electrical gear and certified materials hold pricing and allocation power via 12–30 week lead times and limited spec-compliant sources, pressuring JE Dunn on some 2024 projects. Skilled subcontractor scarcity (AGC 2024: 79% report hiring difficulty) and 60% BIM adoption reinforce switching frictions; long‑term rentals cut equipment costs ~10–20%.

| Factor | 2024 stat/impact |

|---|---|

| Material lead times | 12–30 weeks |

| Skilled craft shortage | AGC 2024: 79% |

| BIM adoption | ~60% |

| Equipment rental savings | 10–20% |

What is included in the product

Tailored Porter's Five Forces for JE Dunn Construction Group, revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market share.

A one-sheet Porter's Five Forces for JE Dunn that instantly surfaces competitive pain points—customizable pressure levels and a clear spider chart make strategic gaps and risks easy to prioritize for board decks or rapid decision-making.

Customers Bargaining Power

Owner sophistication

Healthcare systems, universities, and Fortune 500 owners increasingly use data-driven procurement, with 72% of large owners requiring BIM integration by 2024. They demand transparent pricing and schedule certainty, boosting their negotiation leverage. Sophistication allows owners to apply performance scorecards that can reduce award likelihood or lower fees. JE Dunn faces heightened margin pressure as these owners tie payments to measurable outcomes.

Competitive bidding pressure

Hard-bid and CMAR pursuits routinely pit 5–10 GCs against each other, increasing competitive bidding pressure. Increased price visibility in 2024 has pushed realized margins toward industry averages of roughly 3–5%, empowering owners to squeeze bids. Differentiation through robust preconstruction services and rigorous risk management can defend value. Low-bid norms, however, still cap upside on commoditized scopes.

Portfolio and repeat work

Multi-project clients can bundle work and extract favorable terms from JE Dunn, leveraging portfolio buying power and pipeline optionality to increase negotiation leverage. JE Dunn's relationship capital and documented repeat outcomes lower buyer churn and raise switching costs, reinforcing long-term engagements. Use of framework and IDIQ contracts trades modest margin for volume and schedule predictability, while clients with broader pipelines retain the strongest bargaining power.

Delivery method selection

Design-build, IPD, and GMP contracts shift contingency and performance risk onto the contractor, prompting JE Dunn to price for transferred risk and allocate contingencies into bids. Owners use these delivery methods to share or transfer contingencies, while early contractor engagement allows JE Dunn to influence scope, value-engineer, and reduce downstream change orders. Despite contractor influence, buyers ultimately control risk allocation through contract selection and terms.

- Risk transfer: contractor bears contingency exposure

- Early engagement: enables scope and cost influence

- Buyer control: clients set risk allocation via contract form

Schedule and performance incentives

Schedule and performance incentives—liquidated damages, milestone payments, and KPI-based fees—tighten accountability and let buyers enforce cost and time discipline; in 2024 owners increasingly used milestone/KPI clauses to shift risk. JE Dunn’s advanced planning and VDC capabilities position it to meet stringent targets, but high-stakes penalties amplify buyer bargaining power in negotiations.

- Liquidated damages: enforce time discipline

- Milestones: link payments to delivery

- KPI fees: reward/punish performance

- 2024 trend: rising owner use boosts buyer leverage

Owners demand pricing certainty: 72% BIM, margins 3-5%, 5-10 GCs

Large owners (72% required BIM by 2024) demand transparent pricing, schedule certainty and KPI-linked payments, raising negotiation leverage. Typical pursuits pit 5–10 GCs and pushed realized margins toward 3–5% in 2024, compressing bids. Framework/IDIQ deals trade margin for volume while buyers keep leverage via contract form and penalties.

| Metric | 2024 |

|---|---|

| BIM requirement | 72% |

| Realized margins | 3–5% |

| GCs per bid | 5–10 |

Full Version Awaits

JE Dunn Construction Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for JE Dunn Construction Group you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted and ready for download and use the moment you buy, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with evidence-based insights. You’re viewing the final deliverable, available instantly after payment.