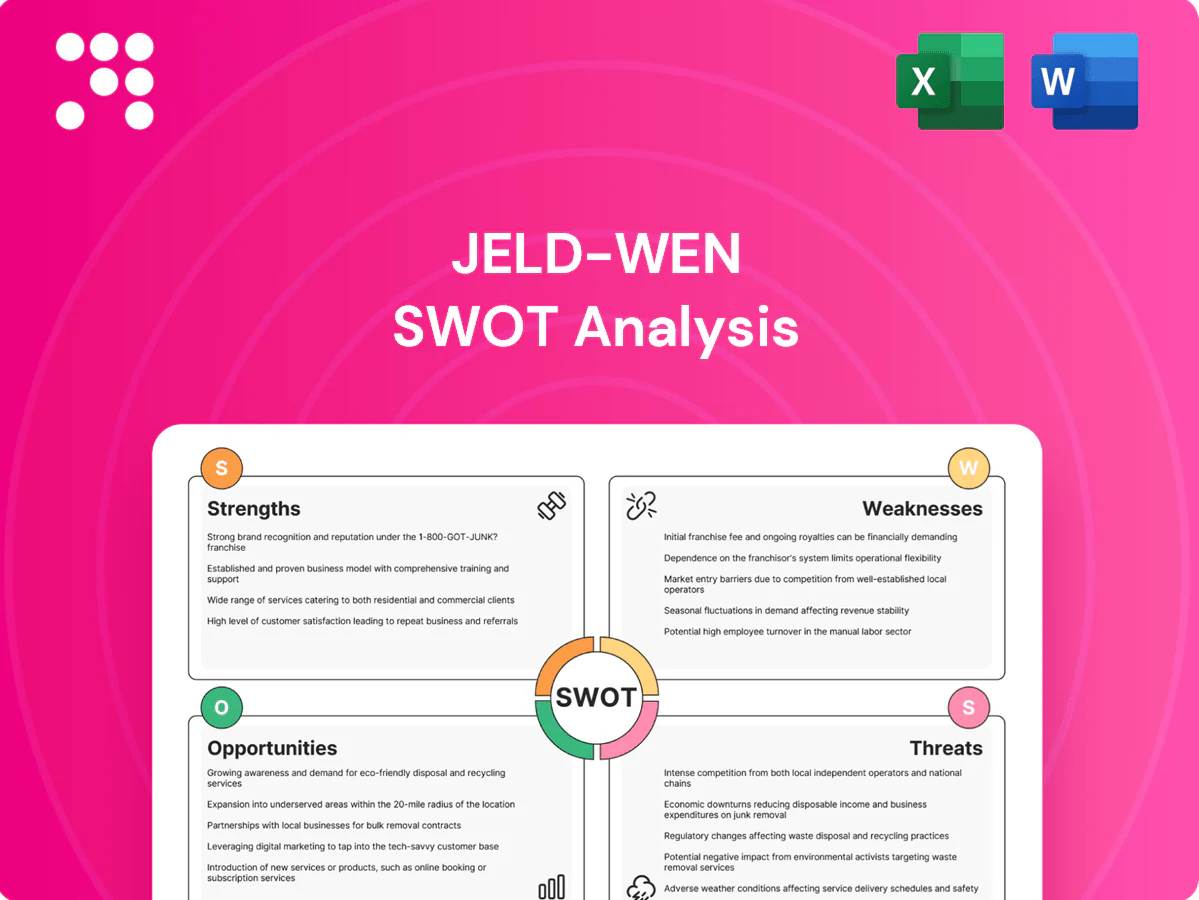

Jeld-Wen SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Jeld‑Wen’s SWOT analysis highlights durable manufacturing scale and global distribution as strengths, while cyclical housing markets and commodity exposure pose key threats; opportunities include sustainable product lines and aftermarket growth. This concise review pinpoints strategic priorities and risk levers for investors and managers. Purchase the full SWOT analysis to access a detailed, editable report and Excel matrix for planning and due diligence.

Strengths

Global manufacturing footprint

JELD-WEN operates more than 130 manufacturing and distribution sites across about 25 countries, enabling shorter lead times for both residential and commercial customers. Geographic diversity reduces single-market dependency and supports cross-border sourcing, with regional plants tailoring SKUs to local codes and preferences. This localized footprint helps mitigate logistics costs and supply-chain disruptions, improving service resilience and cost efficiency.

Diverse doors and windows portfolio

Diverse mix across interior/exterior doors and wood, vinyl and aluminum windows spans value to premium price points. This range supports new construction, repair/renovation and light commercial demand and helped drive FY2023 net sales of about $3.1 billion. Product breadth deepens channel relationships, boosts share of wallet and enables cross-selling and specification in multi-phase projects.

Multi-channel distribution

Jeld-Wen sells through retail home centers, wholesale distributors, and direct channels, widening market reach across DIY consumers, contractors, and large projects. Channel diversity cushions revenue swings when any single route softens and supports price optimization across segments. Retail drives visibility and replacement sales, while wholesale and direct focus on pro-spec and project volume, enhancing overall pricing flexibility and brand presence.

Scale-driven cost advantages

Scale-driven cost advantages: JELD-WEN's high production volumes support purchasing leverage across glass, wood, vinyl, and hardware, lowering input costs and improving gross margins vs smaller competitors.

Standardized platforms and shared components reduce unit complexity and costs; scale enables ongoing investment in automation and lean programs that drive productivity.

JELD-WEN reported approximately $3.6 billion in net sales in FY2023, underpinning these scale economics.

- Purchasing leverage: bulk buying power

- Standardization: lower unit costs

- Automation: capex-powered efficiency

- Margin edge: stronger vs smaller rivals

Established brand recognition

Founded in 1960, Jeld-Wen's long market presence builds trust with contractors, builders and homeowners, supporting specification in plans and encouraging repeat purchases. Its brand equity lowers customer acquisition costs in fragmented residential and commercial building-products markets and helps secure better shelf space and distributor priority. Presence in 20+ countries amplifies these advantages.

- Founded 1960

- Trusted by contractors/builders/homeowners

- Supports specification and repeat sales

- Reduces acquisition costs in fragmented markets

- Improves shelf space and distributor priority

Global doors and windows: 130+ sites in ~25 countries, $3.6B FY2023 sales

JELD-WEN operates 130+ manufacturing/distribution sites in ~25 countries, shortening lead times and lowering single-market risk. A broad portfolio of interior/exterior doors and wood/vinyl/aluminum windows supported approximately $3.6B net sales in FY2023 and enables cross-selling across retail, wholesale and direct channels. Scale drives purchasing leverage, standardization and automation, improving margins vs smaller rivals.

| Metric | Value |

|---|---|

| Manufacturing & distribution sites | 130+ |

| Countries | ~25 |

| FY2023 net sales | $3.6B |

| Primary channels | Retail, Wholesale, Direct |

| Product range | Doors; Wood/Vinyl/Aluminum windows |

What is included in the product

Delivers a strategic overview of Jeld‑Wen’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, identify growth drivers and operational gaps, and highlight market risks shaping future performance.

Provides a focused SWOT matrix tailored for JELD‑WEN to quickly identify competitive strengths, market risks, and operational gaps, enabling fast strategic adjustments and clearer stakeholder alignment.

Weaknesses

Exposure to cyclical housing and renovation

Doors and windows revenue is tightly linked to housing starts, R&R spending and commercial builds; US housing starts collapsed about 77% from 2.07M (2006) to 478k (2009), showing cyclical risk. Downturns quickly compress volumes and pricing, and operating leverage can magnify earnings swings. Forecasting and capacity planning become materially more challenging during such cycles, especially as the US home improvement market was roughly $420B in 2023.

Raw material and freight sensitivity

Costs for lumber, aluminum, glass and PVC resin remain highly volatile, with commodity swings often in the double-digit percent range that intermittently constrain supply. Fuel and freight spikes—historically driving container rates several-fold above pre-pandemic levels—raise delivered costs and extend lead times. Pricing pass-throughs typically lag market moves, squeezing margins quarter-to-quarter. Hedging options are limited or costly for several inputs, reducing risk mitigation flexibility.

Complex operations and product variability

High SKU counts and customization across Jeld-Wen’s product lines increase manufacturing complexity, straining shop-floor flexibility and changeover efficiency; this complexity is notable given FY2024 net sales of about $3.4 billion. Without tight process discipline, quality control and on-time delivery metrics can deteriorate, raising scrap and warranty costs. Complexity elevates overhead and working capital requirements and tends to lengthen lead times during peak seasonal demand.

Capital intensity and maintenance capex

Jeld-Wen faces high capital intensity as manufacturing plants, tooling and automation require steady investment, with 2024 company filings noting elevated maintenance capex and inventory needs that can constrain financial flexibility in downturns; ROI hinges on sustained plant utilization and volume recovery, while network rationalization may trigger one-time restructuring costs.

- Capital intensity: ongoing plant, tooling, automation spend

- Financial strain: elevated capex and inventory limit downside flexibility

- ROI risk: depends on sustained utilization rates

- Restructuring: network rationalization can incur significant one-time costs

Margin pressure from competitive pricing

Margin pressure from competitive pricing is acute as large rivals Andersen, Pella and Masonite and private labels push down prices on commoditized SKUs, compressing JELD‑WEN’s gross margins. Sustained differentiation requires ongoing R&D and elevated marketing spend, raising operating costs. Distributors increasingly demand rebates and promotional support, further squeezing profitability.

- Price-based competition from large rivals and private labels

- Commoditized SKUs compress gross margins

- Ongoing innovation and marketing required

- Distributor rebate and promo demands

Building-products revenue cyclical with housing starts; FY2024 sales $3.4B

Jeld‑Wen’s revenue is cyclical, tied to housing starts and the $420B US home‑improvement market (2023), amplifying volume and pricing swings. Input-cost volatility (lumber, glass, resin) and freight spikes compress margins; FY2024 sales ~ $3.4B. High SKU complexity and capital intensity raise OPEX, working capital and restructuring risk.

| Metric | Value |

|---|---|

| FY2024 sales | $3.4B |

| US home‑improv (2023) | $420B |

Full Version Awaits

Jeld-Wen SWOT Analysis

This is the actual Jeld‑Wen SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Make Insightful Decisions Backed by Expert Research

Jeld‑Wen’s SWOT analysis highlights durable manufacturing scale and global distribution as strengths, while cyclical housing markets and commodity exposure pose key threats; opportunities include sustainable product lines and aftermarket growth. This concise review pinpoints strategic priorities and risk levers for investors and managers. Purchase the full SWOT analysis to access a detailed, editable report and Excel matrix for planning and due diligence.

Strengths

Global manufacturing footprint

JELD-WEN operates more than 130 manufacturing and distribution sites across about 25 countries, enabling shorter lead times for both residential and commercial customers. Geographic diversity reduces single-market dependency and supports cross-border sourcing, with regional plants tailoring SKUs to local codes and preferences. This localized footprint helps mitigate logistics costs and supply-chain disruptions, improving service resilience and cost efficiency.

Diverse doors and windows portfolio

Diverse mix across interior/exterior doors and wood, vinyl and aluminum windows spans value to premium price points. This range supports new construction, repair/renovation and light commercial demand and helped drive FY2023 net sales of about $3.1 billion. Product breadth deepens channel relationships, boosts share of wallet and enables cross-selling and specification in multi-phase projects.

Multi-channel distribution

Jeld-Wen sells through retail home centers, wholesale distributors, and direct channels, widening market reach across DIY consumers, contractors, and large projects. Channel diversity cushions revenue swings when any single route softens and supports price optimization across segments. Retail drives visibility and replacement sales, while wholesale and direct focus on pro-spec and project volume, enhancing overall pricing flexibility and brand presence.

Scale-driven cost advantages

Scale-driven cost advantages: JELD-WEN's high production volumes support purchasing leverage across glass, wood, vinyl, and hardware, lowering input costs and improving gross margins vs smaller competitors.

Standardized platforms and shared components reduce unit complexity and costs; scale enables ongoing investment in automation and lean programs that drive productivity.

JELD-WEN reported approximately $3.6 billion in net sales in FY2023, underpinning these scale economics.

- Purchasing leverage: bulk buying power

- Standardization: lower unit costs

- Automation: capex-powered efficiency

- Margin edge: stronger vs smaller rivals

Established brand recognition

Founded in 1960, Jeld-Wen's long market presence builds trust with contractors, builders and homeowners, supporting specification in plans and encouraging repeat purchases. Its brand equity lowers customer acquisition costs in fragmented residential and commercial building-products markets and helps secure better shelf space and distributor priority. Presence in 20+ countries amplifies these advantages.

- Founded 1960

- Trusted by contractors/builders/homeowners

- Supports specification and repeat sales

- Reduces acquisition costs in fragmented markets

- Improves shelf space and distributor priority

Global doors and windows: 130+ sites in ~25 countries, $3.6B FY2023 sales

JELD-WEN operates 130+ manufacturing/distribution sites in ~25 countries, shortening lead times and lowering single-market risk. A broad portfolio of interior/exterior doors and wood/vinyl/aluminum windows supported approximately $3.6B net sales in FY2023 and enables cross-selling across retail, wholesale and direct channels. Scale drives purchasing leverage, standardization and automation, improving margins vs smaller rivals.

| Metric | Value |

|---|---|

| Manufacturing & distribution sites | 130+ |

| Countries | ~25 |

| FY2023 net sales | $3.6B |

| Primary channels | Retail, Wholesale, Direct |

| Product range | Doors; Wood/Vinyl/Aluminum windows |

What is included in the product

Delivers a strategic overview of Jeld‑Wen’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, identify growth drivers and operational gaps, and highlight market risks shaping future performance.

Provides a focused SWOT matrix tailored for JELD‑WEN to quickly identify competitive strengths, market risks, and operational gaps, enabling fast strategic adjustments and clearer stakeholder alignment.

Weaknesses

Exposure to cyclical housing and renovation

Doors and windows revenue is tightly linked to housing starts, R&R spending and commercial builds; US housing starts collapsed about 77% from 2.07M (2006) to 478k (2009), showing cyclical risk. Downturns quickly compress volumes and pricing, and operating leverage can magnify earnings swings. Forecasting and capacity planning become materially more challenging during such cycles, especially as the US home improvement market was roughly $420B in 2023.

Raw material and freight sensitivity

Costs for lumber, aluminum, glass and PVC resin remain highly volatile, with commodity swings often in the double-digit percent range that intermittently constrain supply. Fuel and freight spikes—historically driving container rates several-fold above pre-pandemic levels—raise delivered costs and extend lead times. Pricing pass-throughs typically lag market moves, squeezing margins quarter-to-quarter. Hedging options are limited or costly for several inputs, reducing risk mitigation flexibility.

Complex operations and product variability

High SKU counts and customization across Jeld-Wen’s product lines increase manufacturing complexity, straining shop-floor flexibility and changeover efficiency; this complexity is notable given FY2024 net sales of about $3.4 billion. Without tight process discipline, quality control and on-time delivery metrics can deteriorate, raising scrap and warranty costs. Complexity elevates overhead and working capital requirements and tends to lengthen lead times during peak seasonal demand.

Capital intensity and maintenance capex

Jeld-Wen faces high capital intensity as manufacturing plants, tooling and automation require steady investment, with 2024 company filings noting elevated maintenance capex and inventory needs that can constrain financial flexibility in downturns; ROI hinges on sustained plant utilization and volume recovery, while network rationalization may trigger one-time restructuring costs.

- Capital intensity: ongoing plant, tooling, automation spend

- Financial strain: elevated capex and inventory limit downside flexibility

- ROI risk: depends on sustained utilization rates

- Restructuring: network rationalization can incur significant one-time costs

Margin pressure from competitive pricing

Margin pressure from competitive pricing is acute as large rivals Andersen, Pella and Masonite and private labels push down prices on commoditized SKUs, compressing JELD‑WEN’s gross margins. Sustained differentiation requires ongoing R&D and elevated marketing spend, raising operating costs. Distributors increasingly demand rebates and promotional support, further squeezing profitability.

- Price-based competition from large rivals and private labels

- Commoditized SKUs compress gross margins

- Ongoing innovation and marketing required

- Distributor rebate and promo demands

Building-products revenue cyclical with housing starts; FY2024 sales $3.4B

Jeld‑Wen’s revenue is cyclical, tied to housing starts and the $420B US home‑improvement market (2023), amplifying volume and pricing swings. Input-cost volatility (lumber, glass, resin) and freight spikes compress margins; FY2024 sales ~ $3.4B. High SKU complexity and capital intensity raise OPEX, working capital and restructuring risk.

| Metric | Value |

|---|---|

| FY2024 sales | $3.4B |

| US home‑improv (2023) | $420B |

Full Version Awaits

Jeld-Wen SWOT Analysis

This is the actual Jeld‑Wen SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Description

Make Insightful Decisions Backed by Expert Research

Jeld‑Wen’s SWOT analysis highlights durable manufacturing scale and global distribution as strengths, while cyclical housing markets and commodity exposure pose key threats; opportunities include sustainable product lines and aftermarket growth. This concise review pinpoints strategic priorities and risk levers for investors and managers. Purchase the full SWOT analysis to access a detailed, editable report and Excel matrix for planning and due diligence.

Strengths

Global manufacturing footprint

JELD-WEN operates more than 130 manufacturing and distribution sites across about 25 countries, enabling shorter lead times for both residential and commercial customers. Geographic diversity reduces single-market dependency and supports cross-border sourcing, with regional plants tailoring SKUs to local codes and preferences. This localized footprint helps mitigate logistics costs and supply-chain disruptions, improving service resilience and cost efficiency.

Diverse doors and windows portfolio

Diverse mix across interior/exterior doors and wood, vinyl and aluminum windows spans value to premium price points. This range supports new construction, repair/renovation and light commercial demand and helped drive FY2023 net sales of about $3.1 billion. Product breadth deepens channel relationships, boosts share of wallet and enables cross-selling and specification in multi-phase projects.

Multi-channel distribution

Jeld-Wen sells through retail home centers, wholesale distributors, and direct channels, widening market reach across DIY consumers, contractors, and large projects. Channel diversity cushions revenue swings when any single route softens and supports price optimization across segments. Retail drives visibility and replacement sales, while wholesale and direct focus on pro-spec and project volume, enhancing overall pricing flexibility and brand presence.

Scale-driven cost advantages

Scale-driven cost advantages: JELD-WEN's high production volumes support purchasing leverage across glass, wood, vinyl, and hardware, lowering input costs and improving gross margins vs smaller competitors.

Standardized platforms and shared components reduce unit complexity and costs; scale enables ongoing investment in automation and lean programs that drive productivity.

JELD-WEN reported approximately $3.6 billion in net sales in FY2023, underpinning these scale economics.

- Purchasing leverage: bulk buying power

- Standardization: lower unit costs

- Automation: capex-powered efficiency

- Margin edge: stronger vs smaller rivals

Established brand recognition

Founded in 1960, Jeld-Wen's long market presence builds trust with contractors, builders and homeowners, supporting specification in plans and encouraging repeat purchases. Its brand equity lowers customer acquisition costs in fragmented residential and commercial building-products markets and helps secure better shelf space and distributor priority. Presence in 20+ countries amplifies these advantages.

- Founded 1960

- Trusted by contractors/builders/homeowners

- Supports specification and repeat sales

- Reduces acquisition costs in fragmented markets

- Improves shelf space and distributor priority

Global doors and windows: 130+ sites in ~25 countries, $3.6B FY2023 sales

JELD-WEN operates 130+ manufacturing/distribution sites in ~25 countries, shortening lead times and lowering single-market risk. A broad portfolio of interior/exterior doors and wood/vinyl/aluminum windows supported approximately $3.6B net sales in FY2023 and enables cross-selling across retail, wholesale and direct channels. Scale drives purchasing leverage, standardization and automation, improving margins vs smaller rivals.

| Metric | Value |

|---|---|

| Manufacturing & distribution sites | 130+ |

| Countries | ~25 |

| FY2023 net sales | $3.6B |

| Primary channels | Retail, Wholesale, Direct |

| Product range | Doors; Wood/Vinyl/Aluminum windows |

What is included in the product

Delivers a strategic overview of Jeld‑Wen’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, identify growth drivers and operational gaps, and highlight market risks shaping future performance.

Provides a focused SWOT matrix tailored for JELD‑WEN to quickly identify competitive strengths, market risks, and operational gaps, enabling fast strategic adjustments and clearer stakeholder alignment.

Weaknesses

Exposure to cyclical housing and renovation

Doors and windows revenue is tightly linked to housing starts, R&R spending and commercial builds; US housing starts collapsed about 77% from 2.07M (2006) to 478k (2009), showing cyclical risk. Downturns quickly compress volumes and pricing, and operating leverage can magnify earnings swings. Forecasting and capacity planning become materially more challenging during such cycles, especially as the US home improvement market was roughly $420B in 2023.

Raw material and freight sensitivity

Costs for lumber, aluminum, glass and PVC resin remain highly volatile, with commodity swings often in the double-digit percent range that intermittently constrain supply. Fuel and freight spikes—historically driving container rates several-fold above pre-pandemic levels—raise delivered costs and extend lead times. Pricing pass-throughs typically lag market moves, squeezing margins quarter-to-quarter. Hedging options are limited or costly for several inputs, reducing risk mitigation flexibility.

Complex operations and product variability

High SKU counts and customization across Jeld-Wen’s product lines increase manufacturing complexity, straining shop-floor flexibility and changeover efficiency; this complexity is notable given FY2024 net sales of about $3.4 billion. Without tight process discipline, quality control and on-time delivery metrics can deteriorate, raising scrap and warranty costs. Complexity elevates overhead and working capital requirements and tends to lengthen lead times during peak seasonal demand.

Capital intensity and maintenance capex

Jeld-Wen faces high capital intensity as manufacturing plants, tooling and automation require steady investment, with 2024 company filings noting elevated maintenance capex and inventory needs that can constrain financial flexibility in downturns; ROI hinges on sustained plant utilization and volume recovery, while network rationalization may trigger one-time restructuring costs.

- Capital intensity: ongoing plant, tooling, automation spend

- Financial strain: elevated capex and inventory limit downside flexibility

- ROI risk: depends on sustained utilization rates

- Restructuring: network rationalization can incur significant one-time costs

Margin pressure from competitive pricing

Margin pressure from competitive pricing is acute as large rivals Andersen, Pella and Masonite and private labels push down prices on commoditized SKUs, compressing JELD‑WEN’s gross margins. Sustained differentiation requires ongoing R&D and elevated marketing spend, raising operating costs. Distributors increasingly demand rebates and promotional support, further squeezing profitability.

- Price-based competition from large rivals and private labels

- Commoditized SKUs compress gross margins

- Ongoing innovation and marketing required

- Distributor rebate and promo demands

Building-products revenue cyclical with housing starts; FY2024 sales $3.4B

Jeld‑Wen’s revenue is cyclical, tied to housing starts and the $420B US home‑improvement market (2023), amplifying volume and pricing swings. Input-cost volatility (lumber, glass, resin) and freight spikes compress margins; FY2024 sales ~ $3.4B. High SKU complexity and capital intensity raise OPEX, working capital and restructuring risk.

| Metric | Value |

|---|---|

| FY2024 sales | $3.4B |

| US home‑improv (2023) | $420B |

Full Version Awaits

Jeld-Wen SWOT Analysis

This is the actual Jeld‑Wen SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, detailed version immediately after checkout.